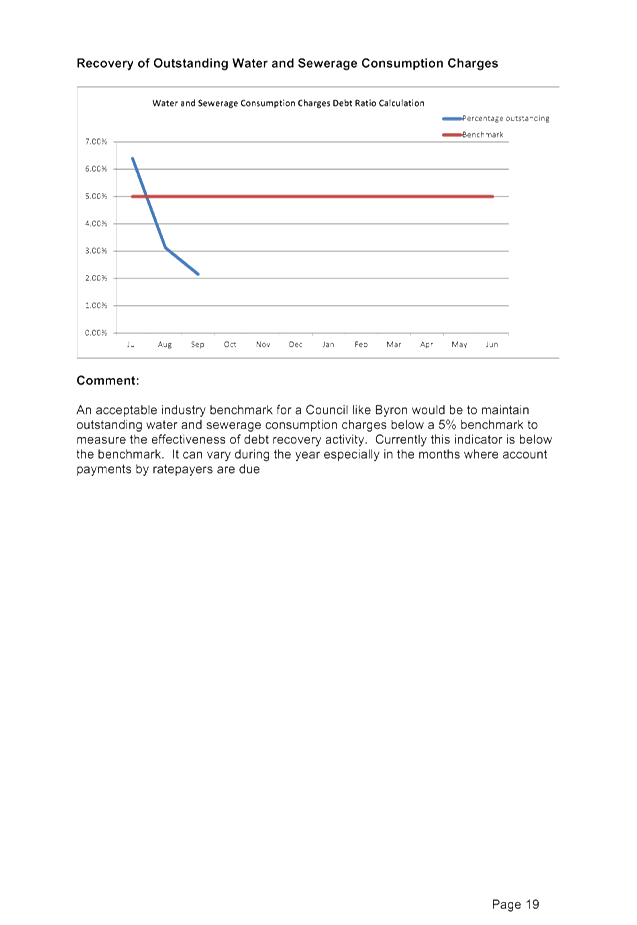

Finance Advisory Committee Meeting

A Finance Advisory Committee Meeting of

Byron Shire Council will be held as follows:

|

Venue

|

Conference Room, Station Street, Mullumbimby

|

|

Date

|

Thursday, 10 November 2016

|

|

Time

|

2.00pm

|

Mark Arnold

Director Corporate and Community Services I2016/1165

Distributed 04/11/16

What is a “Conflict of Interests” - A conflict of

interests can be of two types:

Pecuniary - an interest that a person has in a matter because of a reasonable

likelihood or expectation of appreciable financial gain or loss to the person

or another person with whom the person is associated.

Non-pecuniary – a private or personal interest that a Council

official has that does not amount to a pecuniary interest as defined in the

Local Government Act (eg. A friendship, membership of an association, society

or trade union or involvement or interest in an activity and may include an

interest of a financial nature).

Remoteness – a person does not have a pecuniary interest in a matter

if the interest is so remote or insignificant that it could not reasonably be

regarded as likely to influence any decision the person might make in relation

to a matter or if the interest is of a kind specified in Section 448 of the

Local Government Act.

Who has a Pecuniary Interest? - a person has a pecuniary interest in a

matter if the pecuniary interest is the interest of the person, or another

person with whom the person is associated (see below).

Relatives, Partners - a person is taken to have a pecuniary interest in a

matter if:

§ The person’s

spouse or de facto partner or a relative of the person has a pecuniary interest

in the matter, or

§ The person, or a

nominee, partners or employer of the person, is a member of a company or other

body that has a pecuniary interest in the matter.

N.B. “Relative”, in relation to a person means any of the

following:

(a) the

parent, grandparent, brother, sister, uncle, aunt, nephew, niece, lineal

descends or adopted child of the person or of the person’s spouse;

(b) the

spouse or de facto partners of the person or of a person referred to in

paragraph (a)

No Interest in the Matter - however, a person is not taken to have a

pecuniary interest in a matter:

§ If the person is

unaware of the relevant pecuniary interest of the spouse, de facto partner,

relative or company or other body, or

§ Just because the

person is a member of, or is employed by, the Council.

§ Just because the

person is a member of, or a delegate of the Council to, a company or other body

that has a pecuniary interest in the matter provided that the person has no

beneficial interest in any shares of the company or body.

Disclosure and participation in meetings

§ A Councillor or a

member of a Council Committee who has a pecuniary interest in any matter with

which the Council is concerned and who is present at a meeting of the Council

or Committee at which the matter is being considered must disclose the nature

of the interest to the meeting as soon as practicable.

§ The Councillor or

member must not be present at, or in sight of, the meeting of the Council or

Committee:

(a) at any

time during which the matter is being considered or discussed by the Council or

Committee, or

(b) at any

time during which the Council or Committee is voting on any question in

relation to the matter.

No Knowledge - a person does not breach this Clause if the person did

not know and could not reasonably be expected to have known that the matter

under consideration at the meeting was a matter in which he or she had a

pecuniary interest.

Participation in Meetings Despite Pecuniary Interest (S 452 Act)

A Councillor is not prevented from taking part in the consideration or

discussion of, or from voting on, any of the matters/questions detailed in

Section 452 of the Local Government Act.

Non-pecuniary Interests - Must be disclosed in meetings.

There are a broad range of options available for managing conflicts &

the option chosen will depend on an assessment of the circumstances of the

matter, the nature of the interest and the significance of the issue being

dealt with. Non-pecuniary conflicts of interests must be dealt with in at

least one of the following ways:

§ It may be appropriate

that no action be taken where the potential for conflict is minimal.

However, Councillors should consider providing an explanation of why they

consider a conflict does not exist.

§ Limit involvement if

practical (eg. Participate in discussion but not in decision making or

vice-versa). Care needs to be taken when exercising this option.

§ Remove the source of

the conflict (eg. Relinquishing or divesting the personal interest that creates

the conflict)

§ Have no involvement by

absenting yourself from and not taking part in any debate or voting on the

issue as if the provisions in S451 of the Local Government Act apply

(particularly if you have a significant non-pecuniary interest)

RECORDING OF VOTING ON PLANNING MATTERS

Clause 375A of the Local Government Act 1993

– Recording of voting on planning matters

(1) In this section, planning

decision means a decision made in the exercise of a function of a council

under the Environmental Planning and Assessment Act 1979:

(a) including a decision

relating to a development application, an environmental planning instrument, a

development control plan or a development contribution plan under that Act, but

(b) not including the making of

an order under Division 2A of Part 6 of that Act.

(2) The general manager is

required to keep a register containing, for each planning decision made at a

meeting of the council or a council committee, the names of the councillors who

supported the decision and the names of any councillors who opposed (or are

taken to have opposed) the decision.

(3) For the purpose of

maintaining the register, a division is required to be called whenever a motion

for a planning decision is put at a meeting of the council or a council

committee.

(4) Each decision recorded in

the register is to be described in the register or identified in a manner that

enables the description to be obtained from another publicly available

document, and is to include the information required by the regulations.

(5) This section extends to a

meeting that is closed to the public.

Finance Advisory Committee Meeting

BUSINESS OF MEETING

1. Apologies

2. Declarations of Interest

– Pecuniary and Non-Pecuniary

3. Adoption of Minutes from

Previous Meetings

3.1 Finance

Advisory Committee Meeting held on 18 August 2016

4. Staff Reports

Corporate and Community Services

4.1 Monthly

Financial Reporting.............................................................................................. 4

4.2 Unrestricted

Cash and Reserves at 30 June 2016......................................................... 28

4.3 Council

Budget Review - 1 July 2016 to 30 September 2016........................................ 37

4.4 Financial

Sustainability Plan 2016/2017........................................................................ 130

Staff Reports - Corporate and Community Services 4.1

Staff Reports - Corporate and Community

Services

Report No. 4.1 Monthly

Financial Reporting

Directorate: Corporate

and Community Services

Report

Author: James

Brickley, Manager Finance

File No: I2016/1114

Theme: Corporate Management

Financial Services

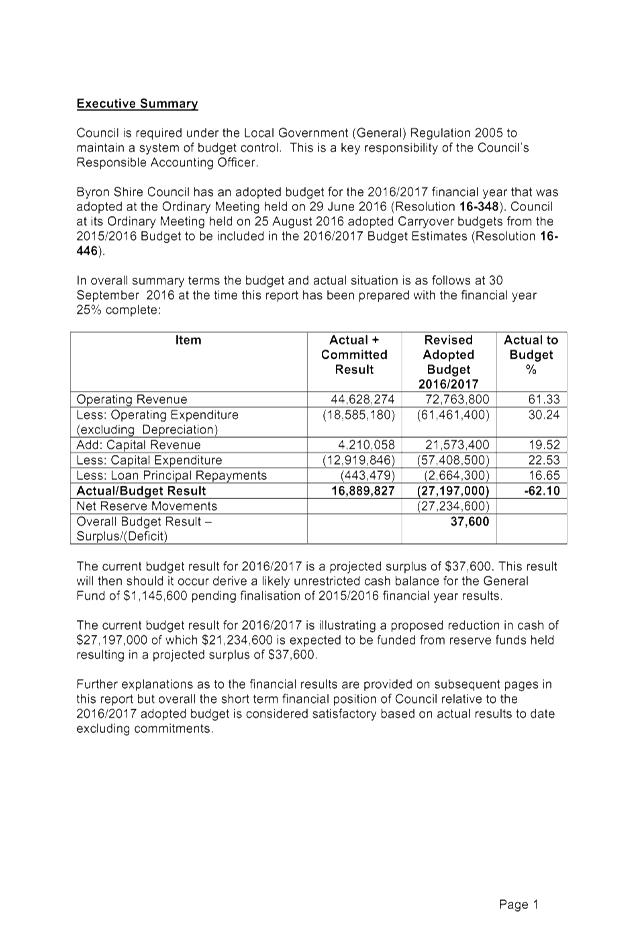

Summary:

Currently each month a financial report is prepared and

distributed to Councillors.

This report is prepared for the Finance Advisory Committee

to provide background information on the form and content of the monthly

financial report provided to Councillors for the information of the new Finance

Advisory Committee members.

It is proposed to continue the production of a monthly

finance report for Councillors.

|

RECOMMENDATION:

That the Finance Advisory Committee recommend to

Council:

1. That

the Report on monthly financial reporting to Councillors be noted.

2. That

the monthly financial report distributed to Councillors be continued

in the format as indicated in Attachment 1 (#E2016/93806)

|

Attachments:

1 Proposed

Monthly Finance Report for Councillors, E2016/93806

, page 6

Report

During the least term of Council, monthly financial

reporting was introduced where each month a financial report was distributed to

Councillors. The report prepared is distributed to Councillors via email

for their information. It is not reported formally to Council in the Council

Meeting Agenda as there is currently no legislative requirement. However, it is

proposed to continue the production of a monthly finance report for

Councillors.

The intent of the monthly finance report is to provide

information to Councillors to outline actual financial performance against the

adopted Council budget and as subsequently modified through the Quarterly

Budget Review process. In terms of monitoring performance, a monthly

budget profile has been established based on historical experience or proposed

activity where actual outcomes each month are tracked against that profile and

the overall annual budget. The benefit of the monthly tracking is to

identify any potential budget issues (if any) early which will enable the

ability to address any issues. Given the Council’s overall budget

is in excess of $120million, such reporting is considered good practice.

The format monthly finance report distributed to Councillors

is outlined at Attachment 1 and contains data at 30 September 2016 to

demonstrate an example of a produced report.

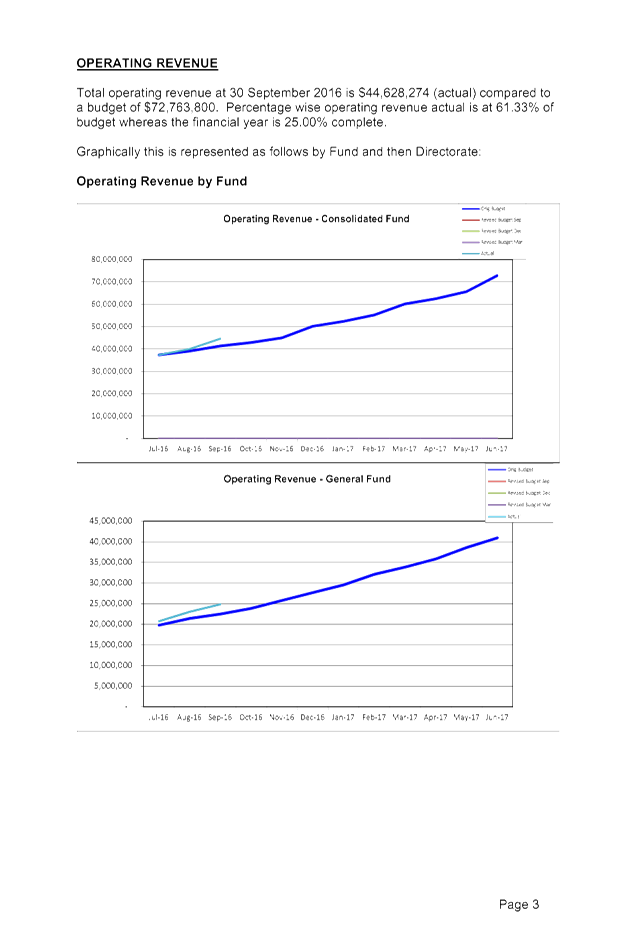

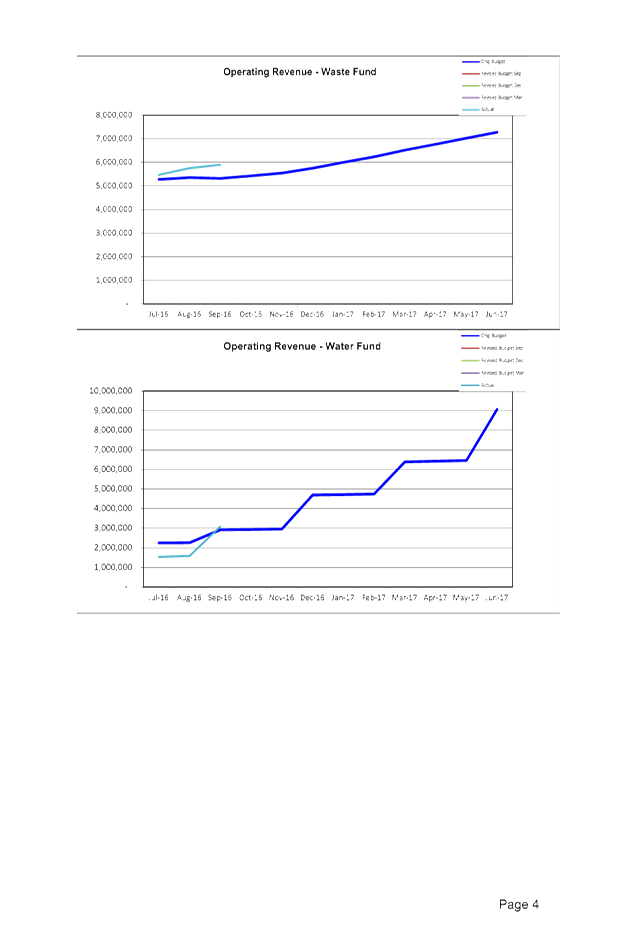

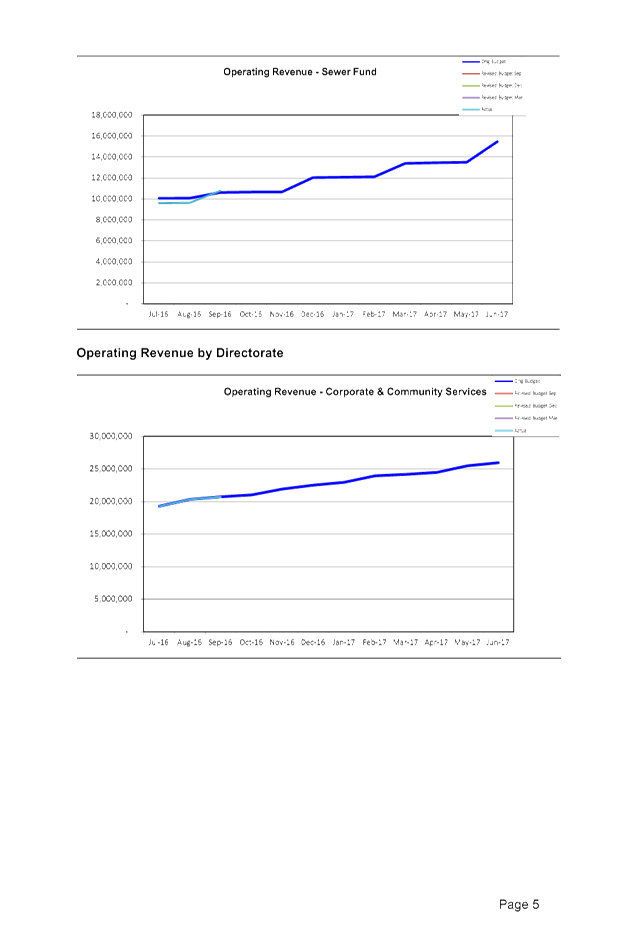

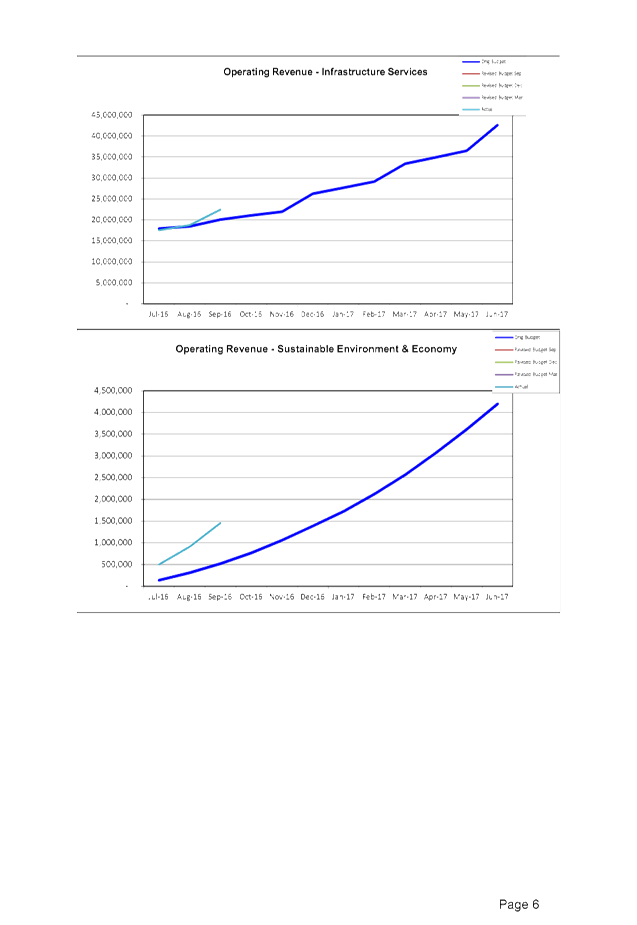

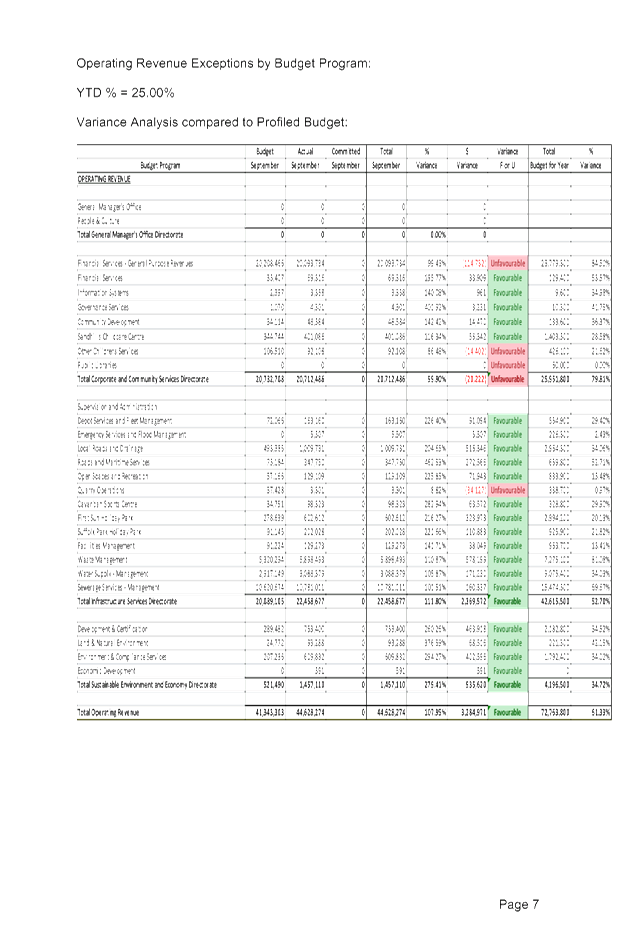

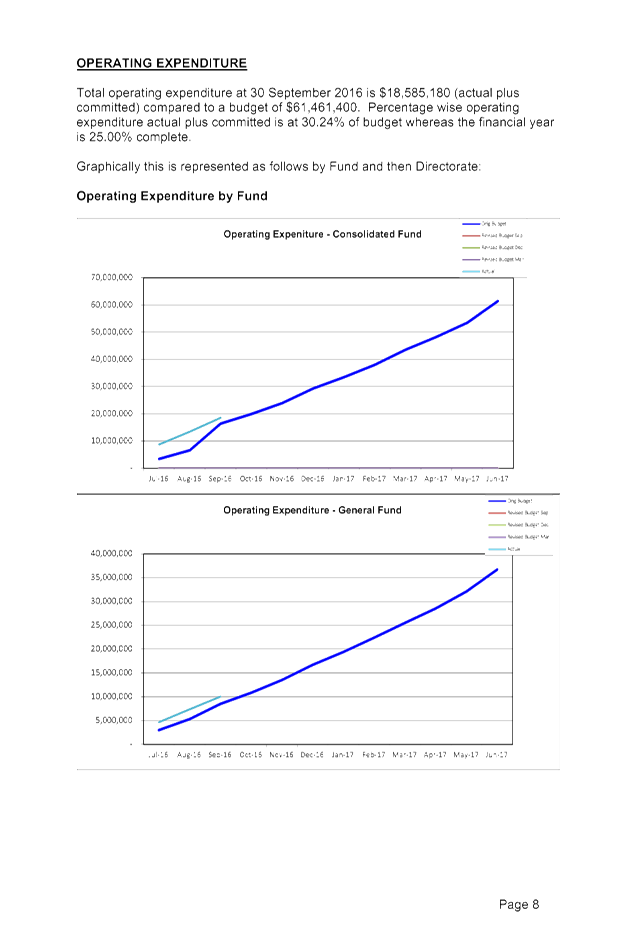

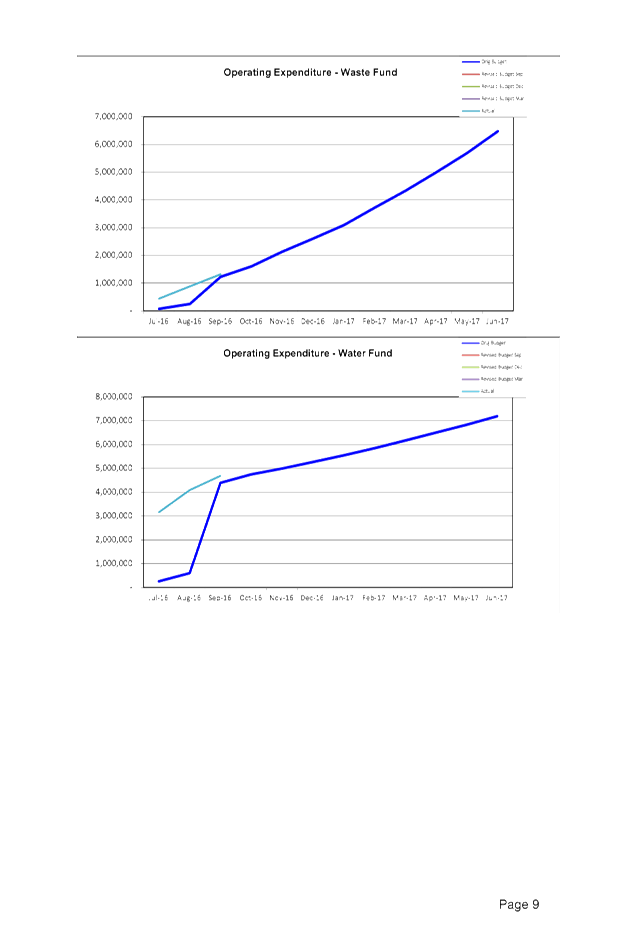

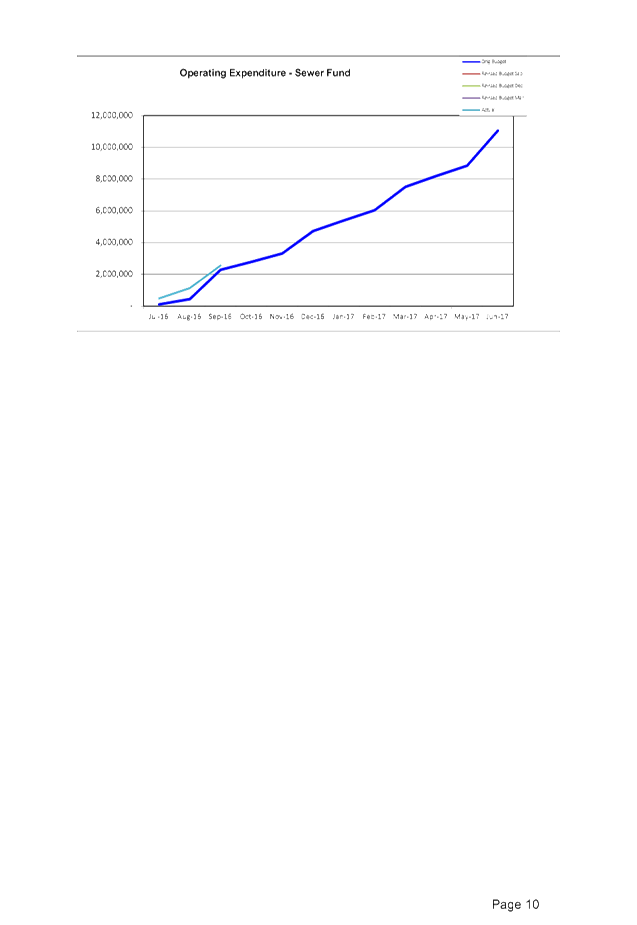

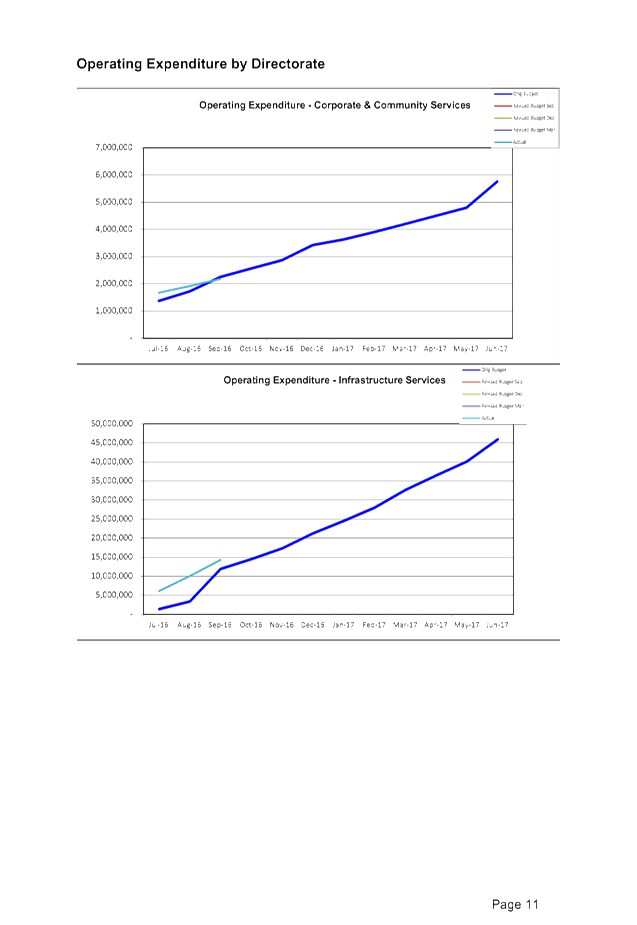

Specifically the report has the following sections:

· Executive Summary

providing a snapshot of the overall budget.

· Introduction.

· Assumptions and

parameters used in preparing the report.

· Comparison of

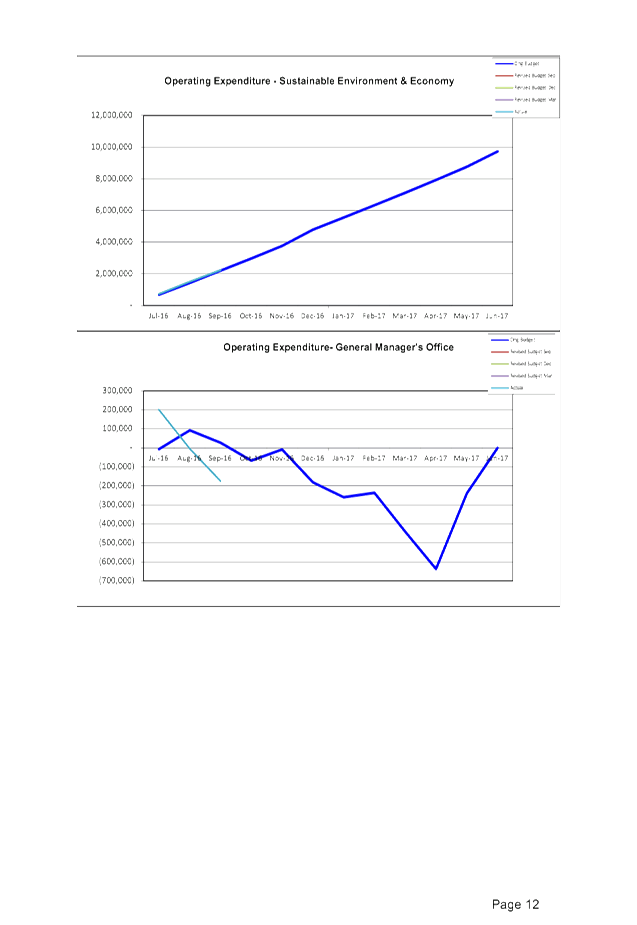

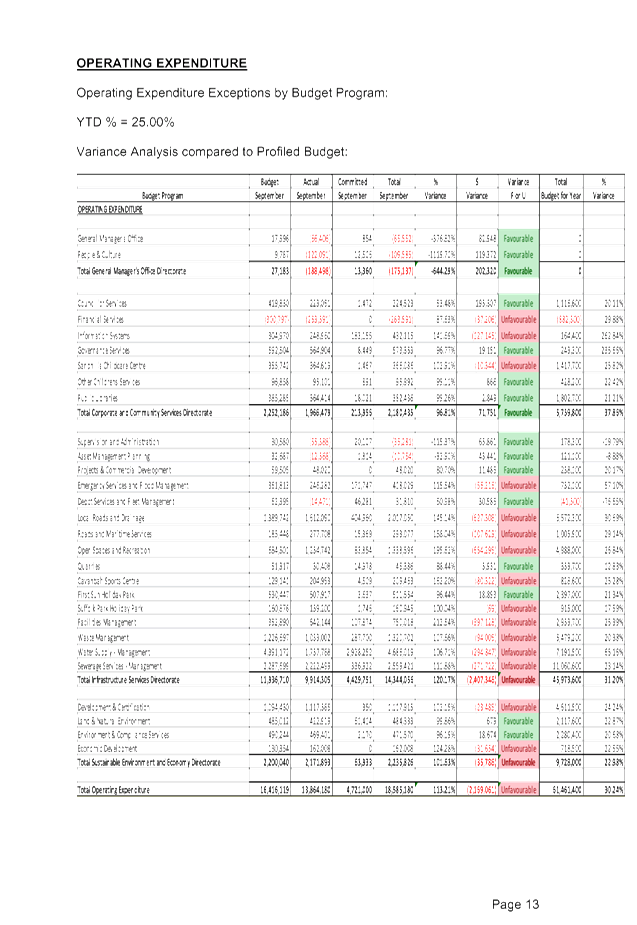

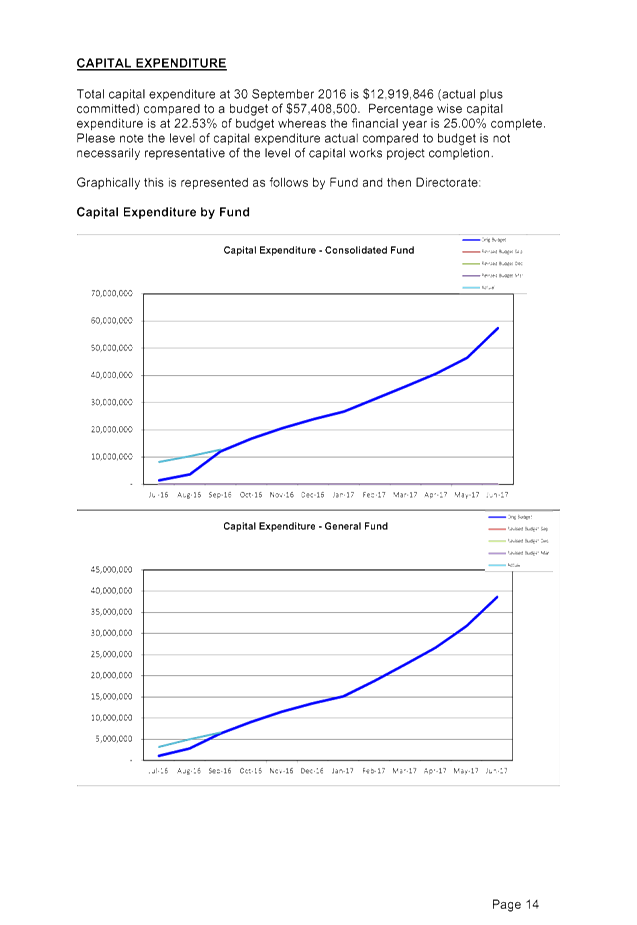

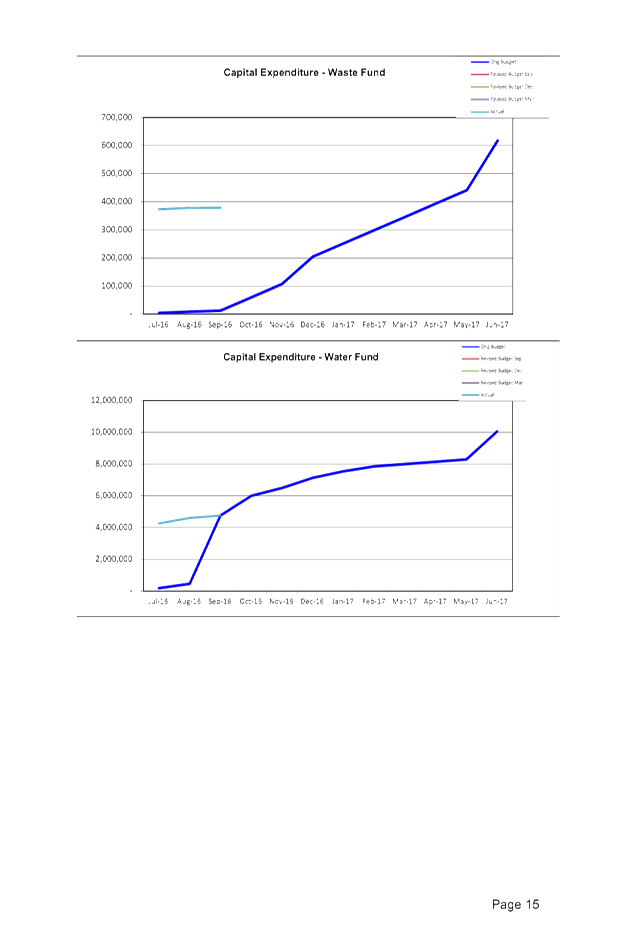

Operating Revenue, Operating Expenditure and Capital Expenditure through

utilising graphs by Fund/Directorate plus variance analysis for each budget program.

· Other Financial

Indicators including:

o Recovery of outstanding rates

and annual charges.

o Recovery of outstanding water

and sewerage consumption charges.

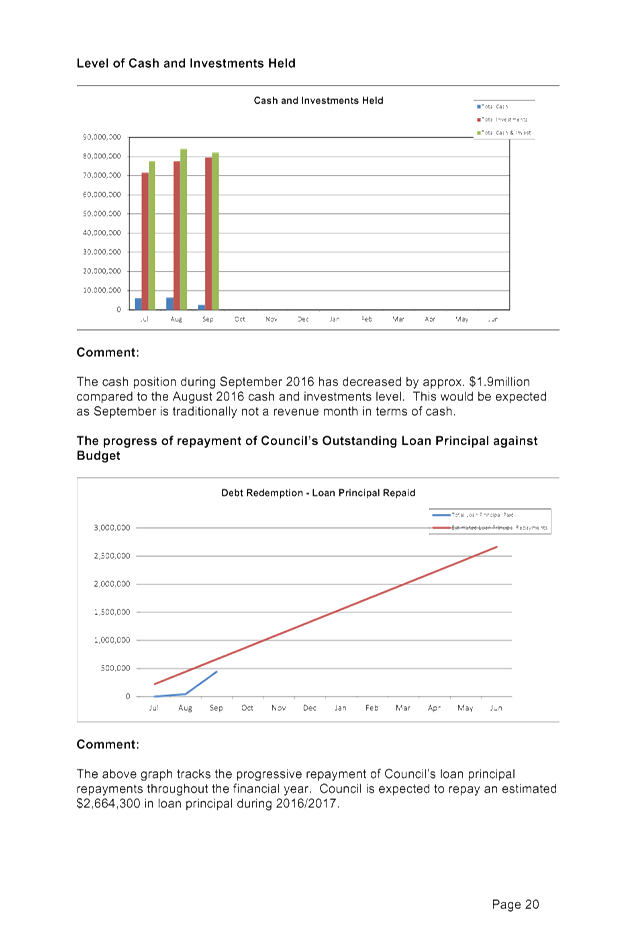

o Level of cash and investments

held.

o The progress on repayment of

Council’s outstanding loan principal against budget.

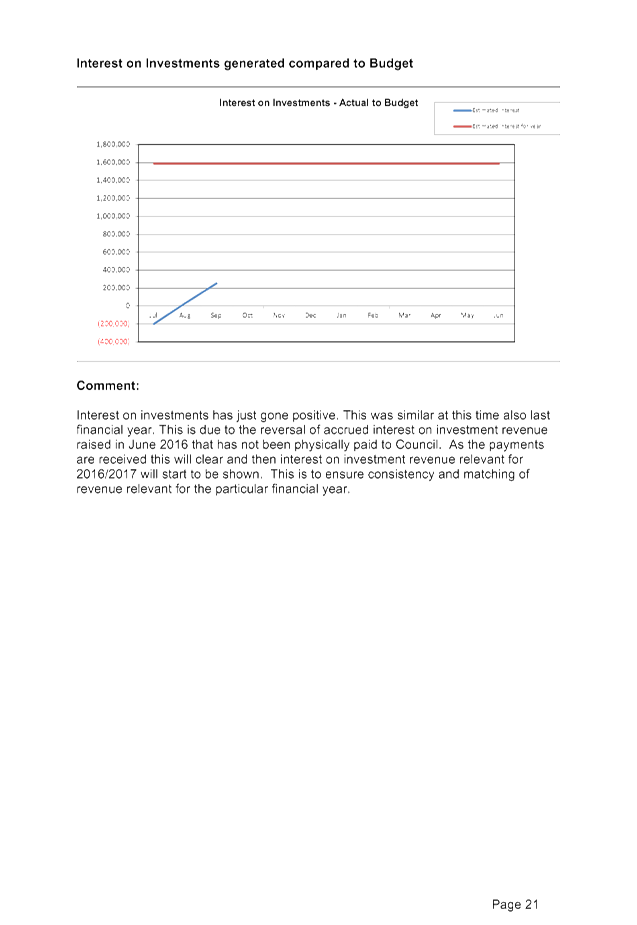

o Interest on investments

generated compared to budget.

The basis for the report distributed to Councillors is in

similar form to a report presented to the Executive Team at the monthly

Performance Meeting of the Executive Team. After the report is considered

by the Executive Team, it is then distributed to Councillors so as such it

contains the same reported financial outcomes.

The format of the report has evolved over time but is able

to be changed if reporting requirements of the Council change.

Financial Implications

There are no financial implications associated with this

report.

Statutory and Policy Compliance Implications

There is currently no requirement contained within the Local

Government Act (1993) or the Local Government (General) Regulation 2005 to

undertake monthly financial reporting to Council. Having said that, there

is an obligation on the Responsible Accounting Officer of Council through

Regulation 202 of the Local Government (General) Regulation 2005 to establish a

system of budgetary control to monitor actual incomes/expenditures monthly with

any material variations required to be reported to Council at the next meeting

of the Council.

Staff Reports - Corporate and Community Services 4.1 - Attachment 1

Staff Reports - Corporate and Community Services 4.2

Report No. 4.2 Unrestricted

Cash and Reserves at 30 June 2016

Directorate: Corporate

and Community Services

Report

Author: James

Brickley, Manager Finance

File No: I2016/1118

Theme: Corporate Management

Financial Services

Summary:

This report has been prepared to allow the Finance Advisory

Committee to note the Reserve balances as at 30 June 2016, and to consider the

recommendation that Council replace the Accumulated Surplus (Working Funds) as

an indicator of Council’s liquidity position.

It is recommended that the Accumulated Surplus (Working

Funds) indicator be replaced with the alternate indicator of the Unrestricted

Cash Balance for the quarterly budget reporting during the 2016/17 Financial

Year.

Council at its Ordinary Meeting held on 27 October 2016

adopted the 2015/2016 Financial Statements that incorporate the results

indicated in this report.

|

RECOMMENDATION:

1. That

the Reserve balances as outlined in Attachment 1 (#E2016/94067) at 30

June 2016 be noted by the Finance Advisory Committee.

2. That

the Unrestricted Cash Balance of $1,145,200 as at 30 June 2016 be noted by

the Finance Advisory Committee.

3. That

the Finance Advisory Committee recommend to Council that for the 2016/17

Financial Year that the Accumulated Surplus (Working Funds) not be used as

an indicator of Council’s liquidity position for the

General, Water and Sewerage Funds and that for the General Fund that the

Accumulated Surplus (Working Funds) be replaced with the Unrestricted Cash

Balance indicator.

|

Attachments:

1 2015/2016

Reserves Schedule, E2016/94067 ,

page 33

Report

This report has been prepared to allow the Finance Advisory

Committee to note the Reserve balances as at 30 June 2016, and to consider the

recommendation that Council replace the Accumulated Surplus (Working Funds) as

an indicator of Council’s liquidity position.

It is recommended that the Accumulated Surplus (Working

Funds) indicator be replaced with the alternate indicator of the Unrestricted

Cash Balance for the quarterly budget reporting during the 2016/17 Financial

Year.

Council at its Ordinary Meeting held on 27 October 2016

adopted the 2015/2016 Financial Statements that incorporate the results

indicated in this report.

Liquidity in terms of Council being able to fulfil its short

term financial commitments is critical and an indicator in the short term of

Council’s financial health. There is no set indicator that is absolutely

used to identify the liquidity position of a Council, however there are the

following indicators:

· Unrestricted Cash

– this represents the total available cash and investments Council has,

that is not restricted for any reason either by legislation, condition or

Council resolution. This amount is determined at 30 June each year and

disclosed at note 6(c) of Council’s annual Financial Statements. It is

calculated by deducting from total cash and investments held the total amount

of internal and external restrictions or reserves.

· Unrestricted

Current Ratio – this ratio assesses the short term adequacy of working

capital. It compares unrestricted current assets to unrestricted current

liabilities. Any ratio that has at least $1.50 of unrestricted current

assets to each $1 of unrestricted current liabilities is generally considered

satisfactory. This indicator is determined at 30 June each year and

disclosed at note 13(a) of Council’s annual Financial Statements.

This indicator is usually provided on a consolidated basis ie amalgamating all

of Council’s General, Water and Sewerage Funds. However since the

2009/2010 financial year, Councils are now required to calculate this ratio and

other ratios by Fund for additional disclosure as outlined in note 13(b) of

Council’s annual Financial Statements. On a consolidated basis at 30 June

2016, Council had $2.96 of unrestricted current assets to each $1 of unrestricted

current liabilities.

· Accumulated

Surplus (Working Funds) – this indicator is a traditional measure of

Councils working capital adequacy and is something Byron Shire Council has used

for some time and established targets for adequacy in each of the Funds

operated being General, Water and Sewerage. Accumulated Surplus (Working Funds)

are not disclosed anywhere in Council’s annual Financial Statements.

· Cash Expense Cover

Ratio – this indicator commenced disclosure from the 2013/2014 financial

year that is disclosed at note 13(a) of Council’s annual Financial

Statements. It measures the number of months Council would be able to pay

its immediate expenses without additional cash inflow. The benchmark for

this ratio is 3 months and at 30 June 2016, Council was at 14.55 months.

Accumulated Surplus (Working Funds)

This measure of working capital has been utilised by Council

historically as an indicator of its short term liquidity position. To

this end, Council has adopted the following targets by Fund:

· General Fund - $1,000,000

· Water Fund - $600,000

· Sewerage Fund - $600,000

This indicator attempts to identify the working capital

position of Council by comparing the following items:

· Current Assets

(cash at bank, investments, current receivables, inventories and other current

assets (generally prepayments)) less restricted assets or reserves (unexpended

grants, contributions, bonds and deposits, unexpended loans, crown reserves and

internal reserves)

less

· Current

Liabilities (creditors, loan repayments due the next year, and provisions) less

any restricted current liabilities, provisions and loan repayments.

Provisions and loan repayments are generally excluded from the calculation as

they form part of Council’s committed budget for the following financial

year ie they are provided for there plus the immediate settlement of these

items is generally not required.

One of the issues associated with the use of Accumulated

Surplus (Working Funds) as a financial indicator relates to what items are

included, and what items are not. An example of this is that the value of

Council’s stores and materials is included as a current asset but these

are not easily converted to cash. Firstly to utilise stores and materials

as cash requires the stores and materials to be sold so whilst considered a

current asset, if needed to in an emergency, the process to convert stores and

materials to cash would take time, and therefore in terms of timing there is a

question as to whether stores and materials are an appropriate component of

Accumulated Surplus (Working Funds) balance. The theme follows that not all of

Council’s current assets can be converted to cash immediately.

The notion of Accumulated Surplus (Working Funds), whilst an

indicator of working capital cannot be construed as available cash, as its

composure is simply not cash alone. This is something that an alternative

measure such as the Unrestricted Cash Balance which is disclosed at Note 6(c)

to Council’s annual Financial Statements, is considered as a stronger

indicator, as it is based solely on available cash not restricted for any other

purpose.

Unrestricted Cash Balance

The Unrestricted Cash Balance disclosed in the Financial

Statements indicates that as at 30 June 2016 an amount of $1,145,211 was

available whereas in 2014/2015 it was $1,143,412. This means that all

cash held by Council as at 30 June 2016 was restricted for a purpose by

legislation, funding condition or Council resolution except for $1,145,211.

Whilst Council has considered Accumulated Surplus (Working

Funds) as its traditional guide to working capital or short term liquidity, it

is also important to consider the amount of unrestricted cash as an alternate

indicator. This is argued as it is clearly a more valid measure of the

available cash position of Council. Council has considered this

proposition at its Ordinary Meeting held on 8 August 2013 where it also adopted

an Unrestricted Cash Balance target of $1,000,000 for the General Fund as a measure

of its short term unrestricted liquidity from 1 July 2013 (Resolution: 13-378).

Council’s other funds being Water and Sewerage will always have a $0

(Nil) Unrestricted Cash Balance given the legislative requirements of water and

sewerage revenues which requires and unexpended funds to be reserved as an

external restriction. Any reported Unrestricted Cash Balance will always

relate to the General Fund.

It is recommended that the Accumulated Surplus (Working

Funds) indicator be replaced with the alternate indicator of the Unrestricted

Cash Balance for the quarterly budget reporting during the 2016/17 Financial

Year for the following reasons:

1. It

is subjective in calculation (interpreting what is included) and incorporates

non-cash items even though it is purported to be a liquidity measure.

2. It

is an indicator that is not recognised in Council’s Annual Financial

Statements.

3. There

is no reporting of this indicator to the Office of Local Government annually as

part of the Council’s Financial Data Return.

4. It

has not been used by any recent external financial assessments of Council such

as the financial sustainability assessments conducted by NSW Treasury

Corporation and the Independent Pricing and Regulatory Tribunal (IPART).

5. Current

performance benchmarking in Local Government such as that conducted by Price

Waterhouse Coopers (PWC) does not consider this indicator.

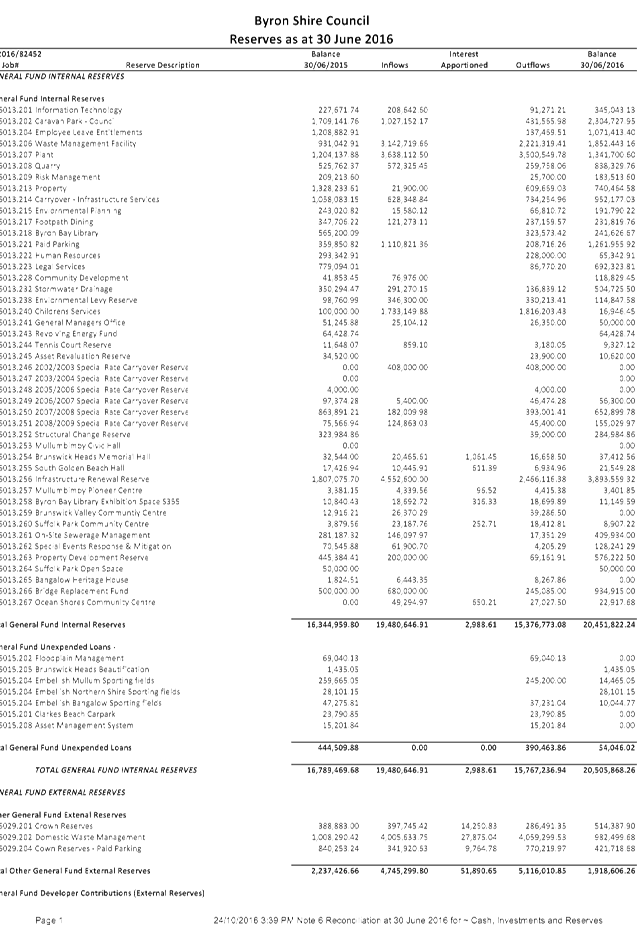

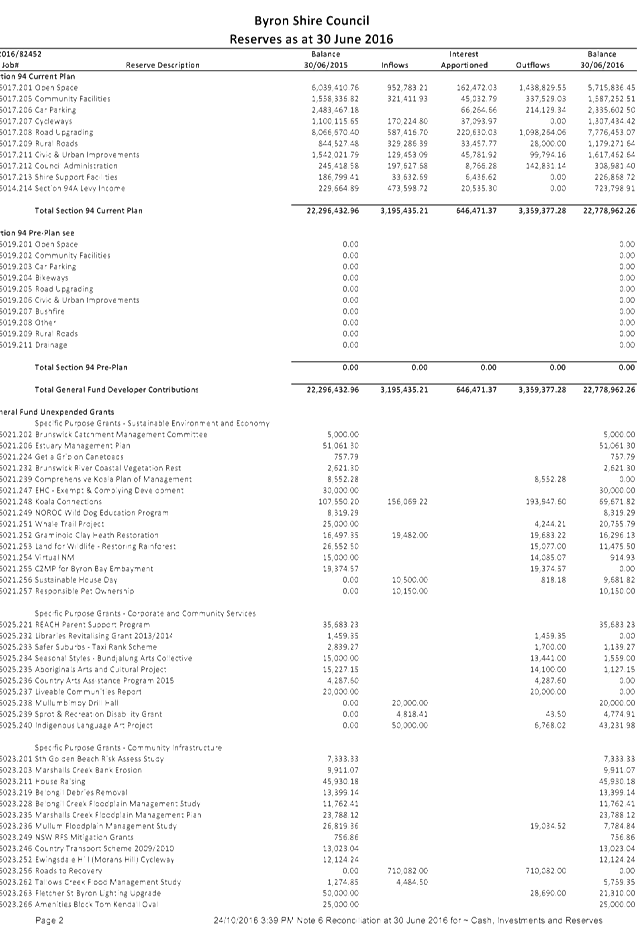

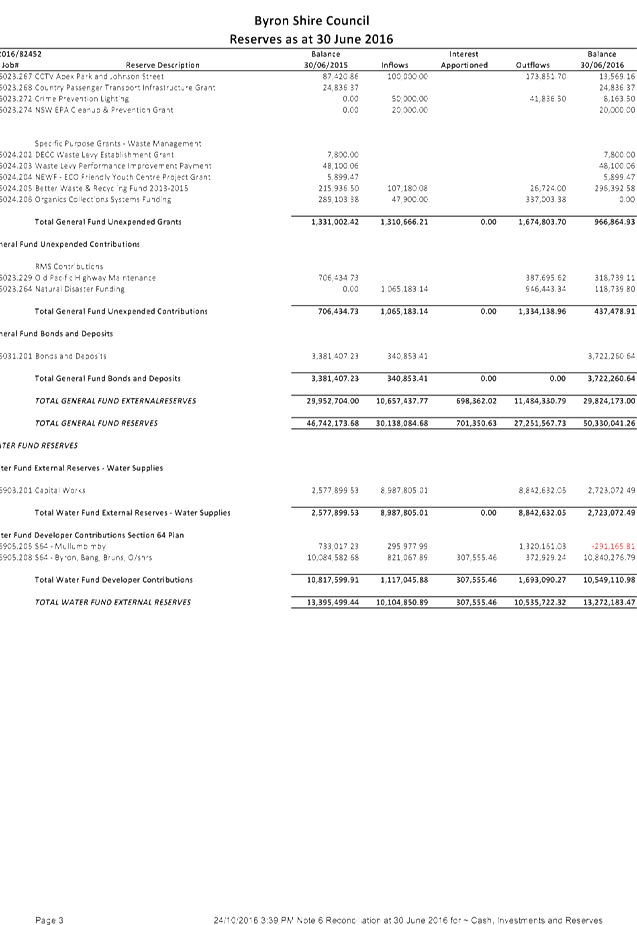

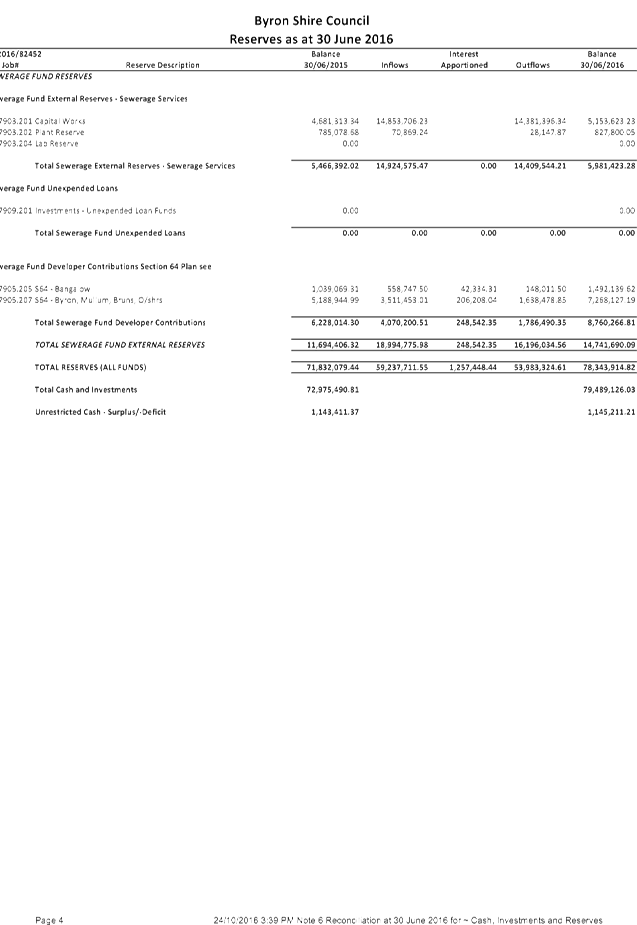

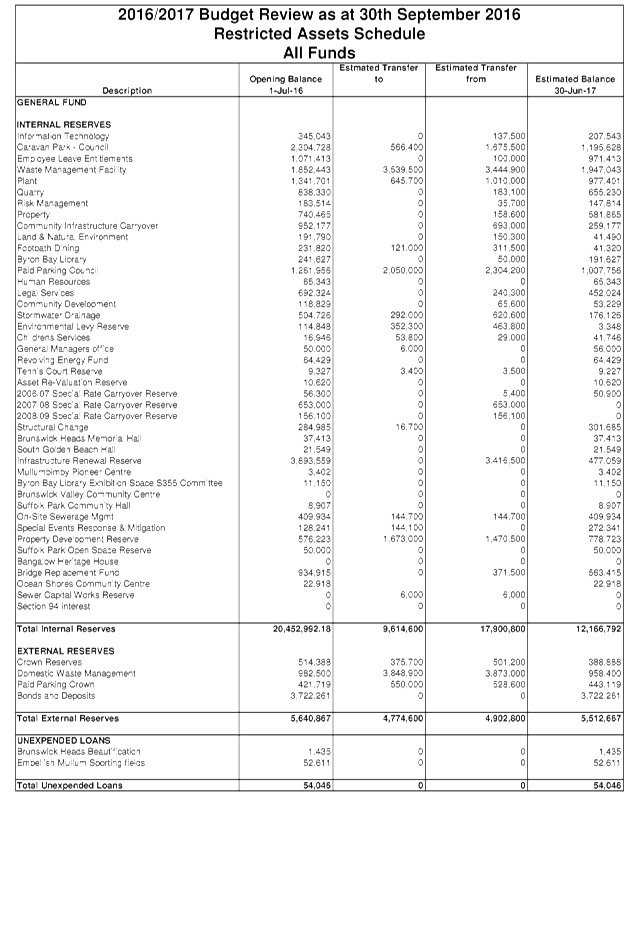

Reserves

Detailed at Attachment 1 is a listing of Council’s

cash funded reserves. Contained in this listing is the detail of and

value as at 30 June 2016 of the various reserve types. Reserve types are

broken down into the following components:

· External

Restrictions – these reserves relate to unexpended grants, developer

contributions, bonds and deposits, unexpended loans (non-General Fund), Crown

reserves, domestic waste management, water, sewerage and Roads and Maritime

Services (RMS) contributions unexpended.

· Internal

restrictions – these are reserves set by Council for specific purposes

that are not required to be restricted for external reasons ie legislation,

condition etc. These reserves though are generally created to isolate

self-financing activities and their accumulated funds or if Council by

resolution wants funds specifically set aside. Examples of internal

restrictions are also listed in Attachment 1 and also in note 6(c) to

Council’s annual Financial Statements.

In summary, as at 30 June 2016 detailed in Note 6(c) to the

annual Financial Statements are the following values relating to reserves

restricted against available cash and investments:

· Total available cash and

investments $79,489,126

· Total external restrictions

(reserves) $57,838,047

· Total internal restrictions

(reserves) $20,505,868

· Total unrestricted cash and

investments $1,145,211.

It is appropriate that Council consider its reserves which

are restricted against available cash and investments and resolve by resolution

to adopt their description and value. By default this occurred when

Council adopted the 2015/2016 Financial Statements at its Ordinary Meeting held

on 27 October 2016. Council further reviews the position of held reserves

through setting the annual budget and subsequent reviews of the budget at each

quarterly budget review.

Financial Implications

There are no direct financial implications associated with

this report. the report is identifying to the Finance Advisory Committee the

overall liquidity and reserves position of Council at 30 June 2016 for

information.

Statutory and Policy Compliance Implications

The requirement of Council to restrict aspects of its

available cash and investments follows from the requirement to maintain

appropriate accounting records to verify the expenditure of funds and

recognition of funds required to be detailed as unexpended. This is a

canvassed by the Local Government Code of Accounting Practice and Financial

Reporting (as amended) upon which Council must adhere to as outlined Section

413(3) of the Local Government Act 1993 and Regulation 214 of the Local

Government (General) Regulation 2005.

Section 409 of the Local Government Act 1993 and Regulation

205 of the Local Government (General) Regulation also outline conditions on the

use of funds received by Council.

Staff Reports - Corporate and Community Services 4.2 - Attachment 1

Staff Reports - Corporate and Community Services 4.3

Report No. 4.3 Council

Budget Review - 1 July 2016 to 30 September 2016

Directorate: Corporate

and Community Services

Report

Author: James

Brickley, Manager Finance

File No: I2016/1120

Theme: Corporate Management

Financial Services

Summary:

This report is prepared to comply with Regulation 203 of the

Local Government (General) Regulation 2005 and to inform Council and the

Community of Council’s estimated financial position for the 2016/2017

financial year, reviewed as at 30 September 2016.

This report contains an overview of the proposed budget

variations for the General Fund, Water Fund and Sewerage Fund. The

specific details of these proposed variations are included in Attachment 1 and 2

for Council’s consideration and authorisation.

Attachment 3 contains the Integrated Planning and Reporting

Framework (IP&R) Quarterly Budget Review Statement (QBRS) as outlined by

the Division of Local Government in circular 10-32.

|

RECOMMENDATION:

That the Finance Advisory

Committee recommend to Council:

1. That

Council authorise the itemised budget variations as shown in Attachment 2 (#E2016/94992)

which includes the following results in the 30 September 2016 Quarterly Review

of the 2016/2017 Budget:

a) General

Fund – No change in the Estimated Unrestricted Cash Result

b) General

Fund - $1,831,800 decrease in reserves

c) Water

Fund - $1,216,300 increase in reserves

d) Sewerage

Fund - $2,152,300 increase in reserves

2. That

Council adopt the revised General Fund Estimated Unrestricted Cash Result of

$1,182,800 for the 2016/2017 financial year as at 30 September 2016.

|

Attachments:

1 Budget

Variations for General, Water and Sewerage Funds, E2016/95846 , page 47

2 Itemised

Listing of Budget Variations for General, Water and Sewerage Funds, E2016/94992 ,

page 111

3 Integrated

Planning and Reporting Framework (IP&R) Quarterly Review Statement, E2016/95847 ,

page 115

Report

Council adopted the 2016/2017 budget on 29 June 2016 via

Resolution 16-348. It also considered and adopted the budget

carryovers from the 2015/2016 financial year, to be incorporated into the

2016/2017 budget at its Ordinary Meeting held on 25 August 2016 via Resolution 16-446.

Since that date, Council has reviewed the budget taking into consideration the

2015/2016 Financial Statement results and progress through the first quarter of

the 2016/2017 financial year. This report considers the September 2016

Quarter Budget Review.

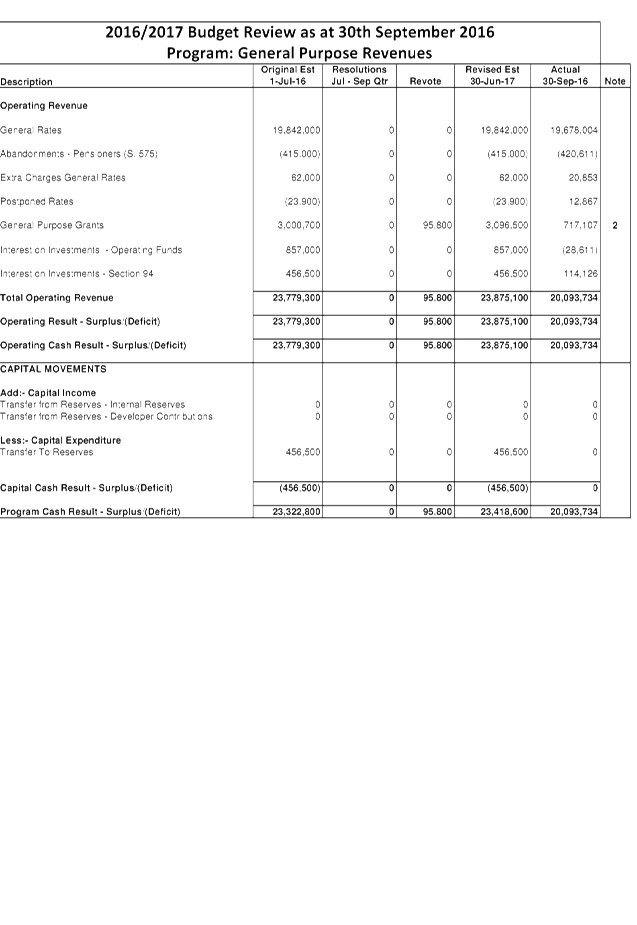

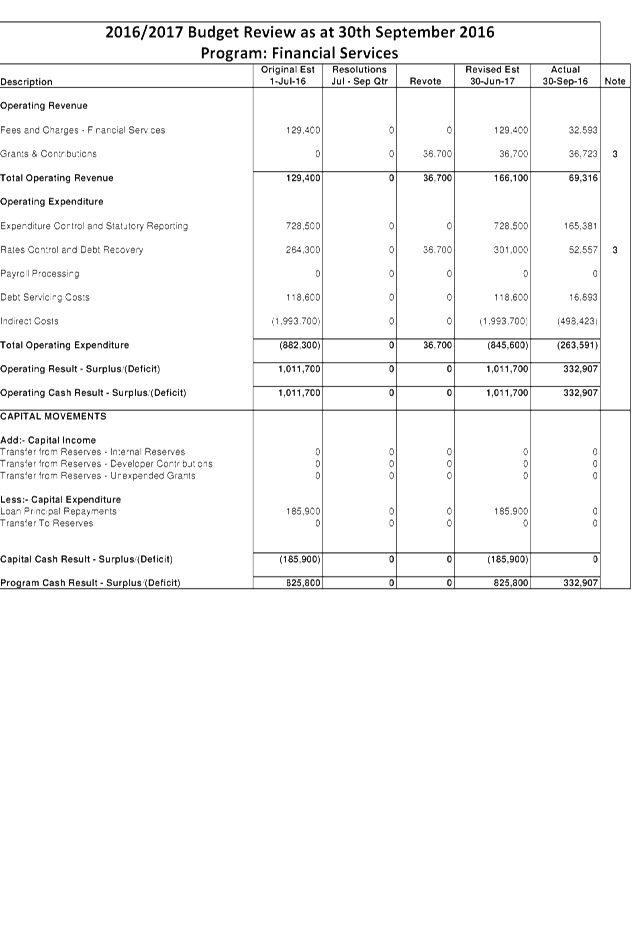

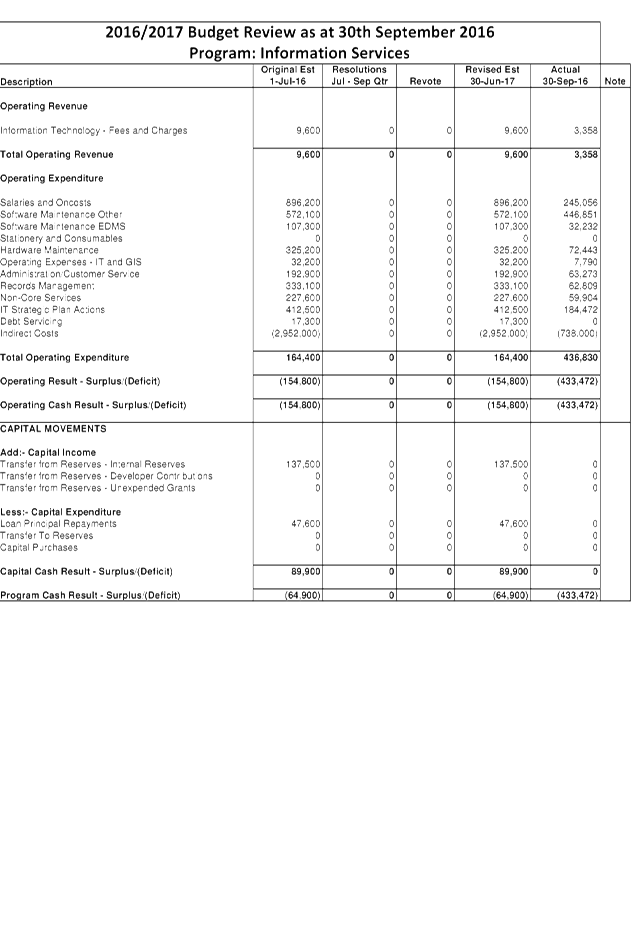

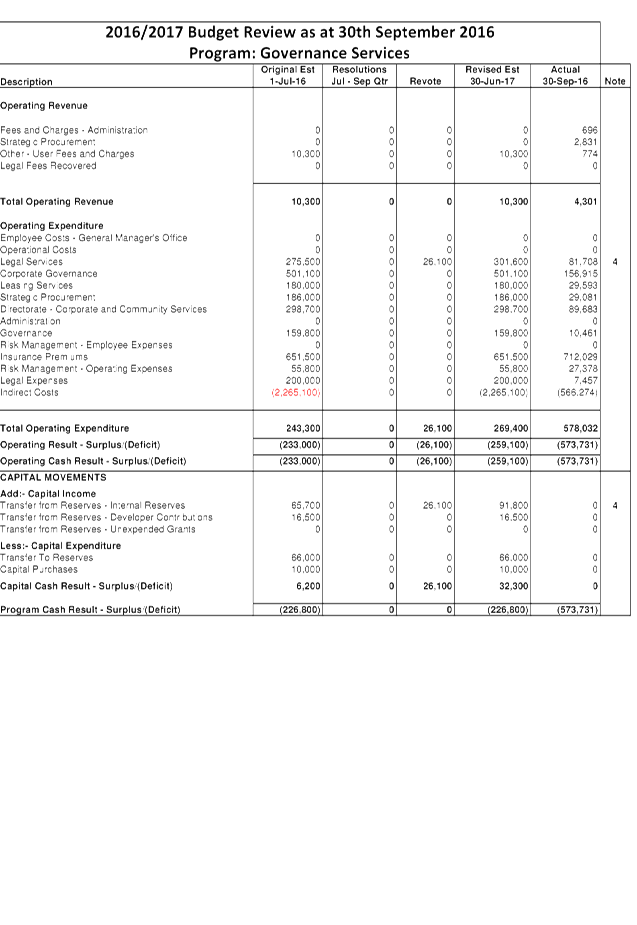

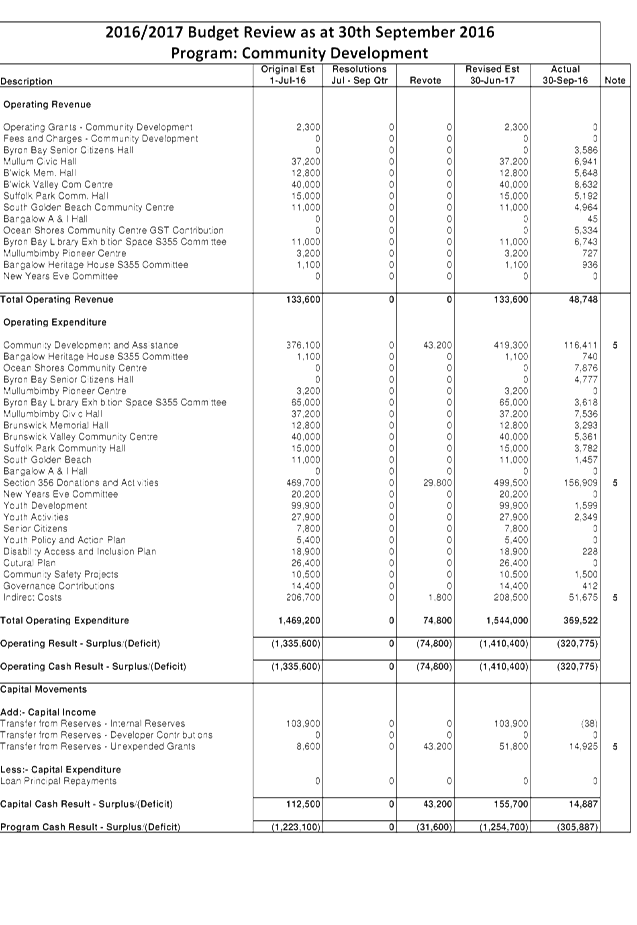

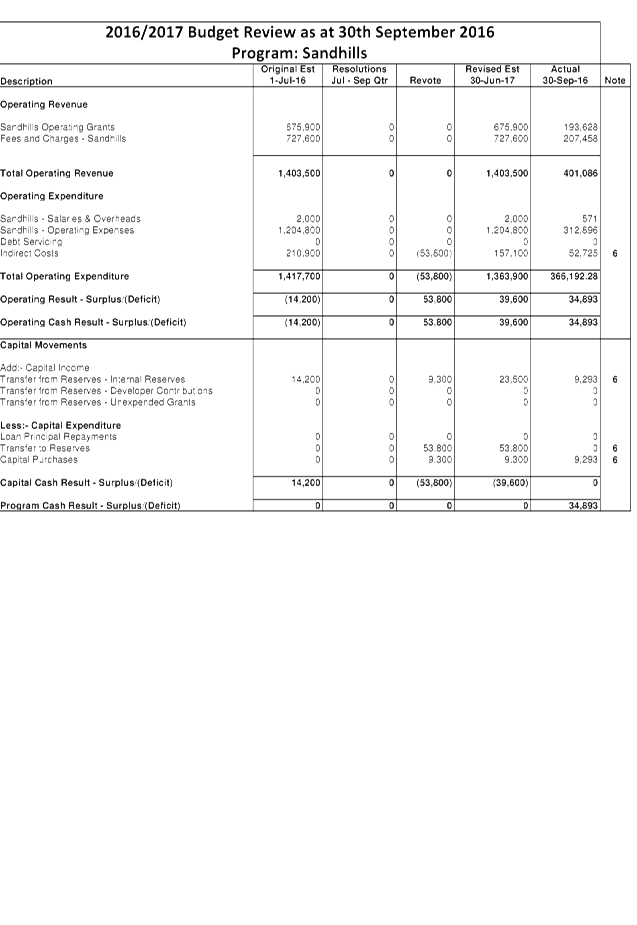

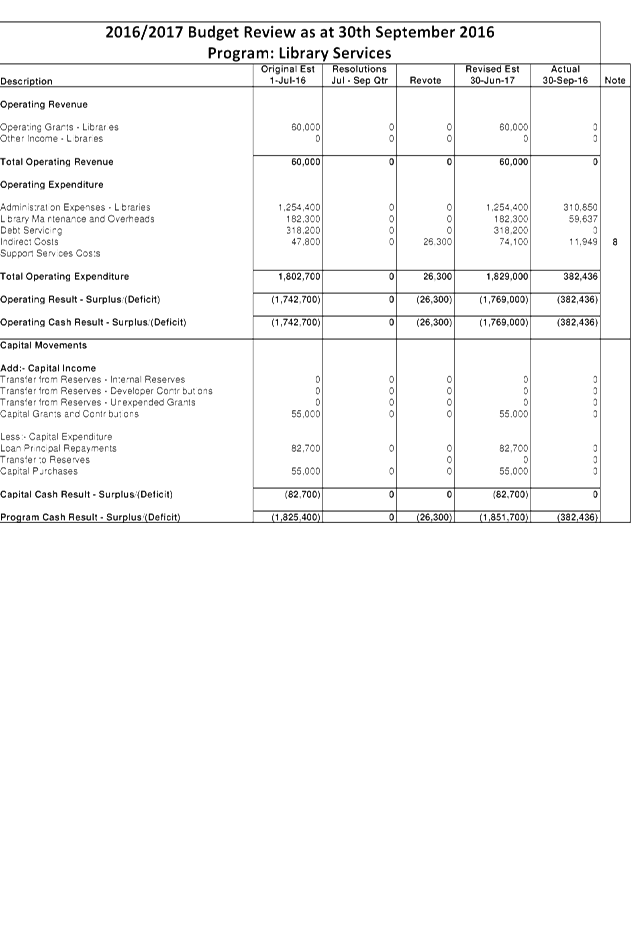

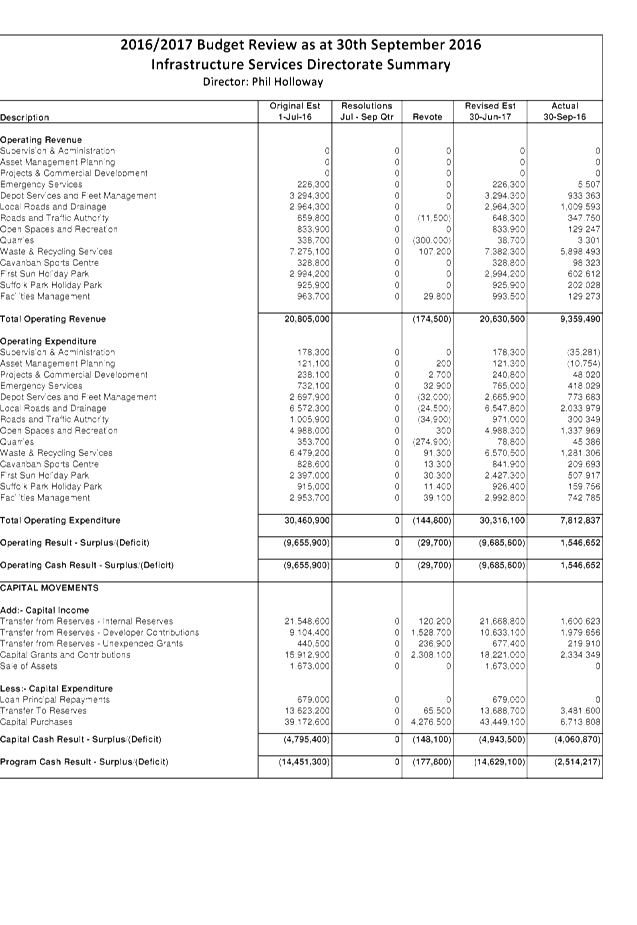

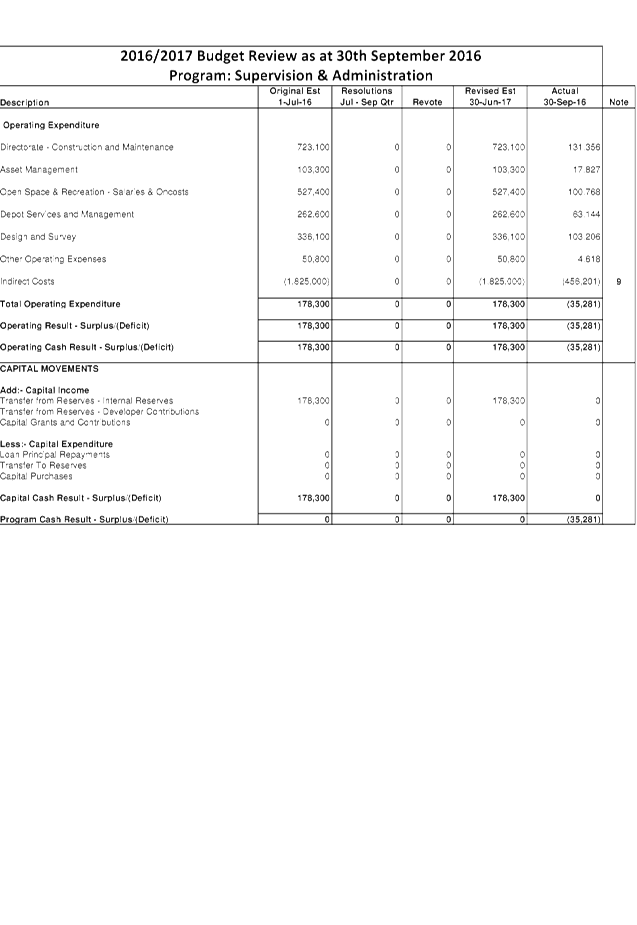

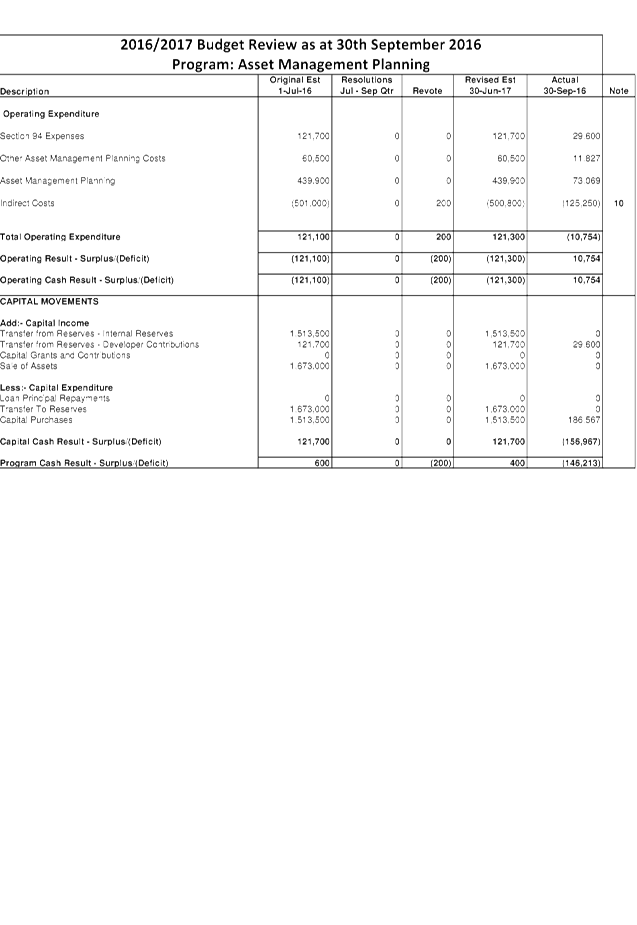

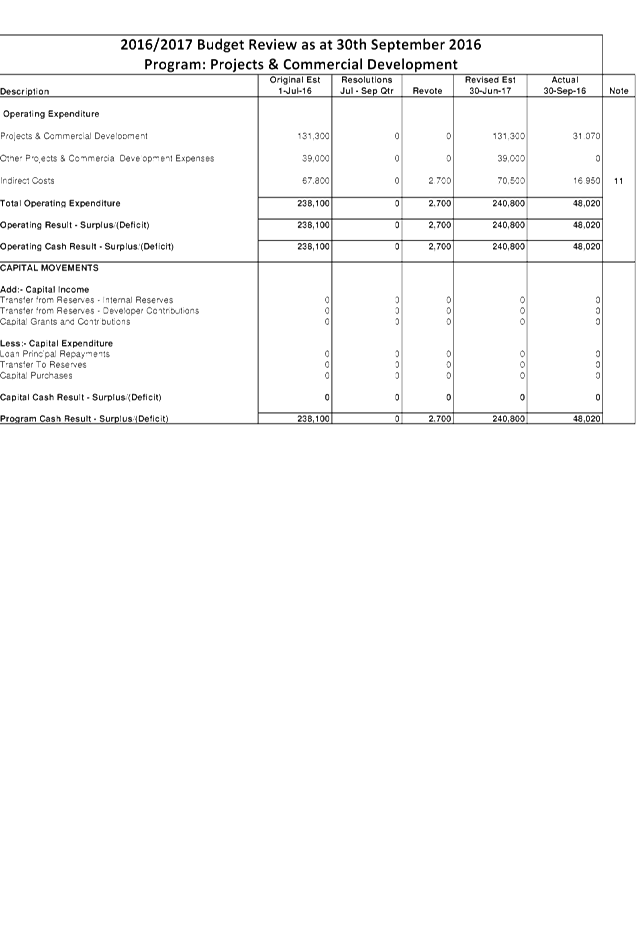

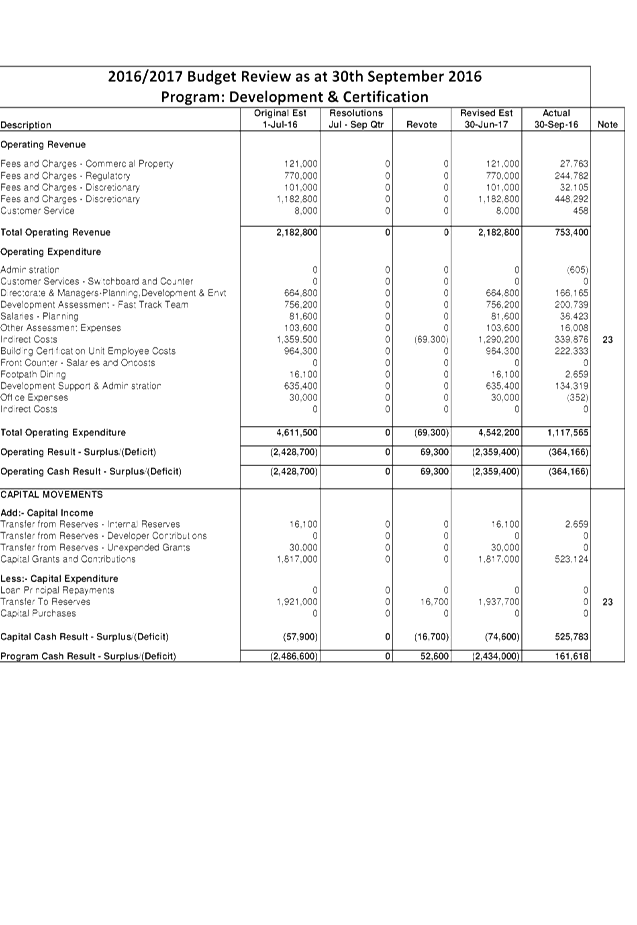

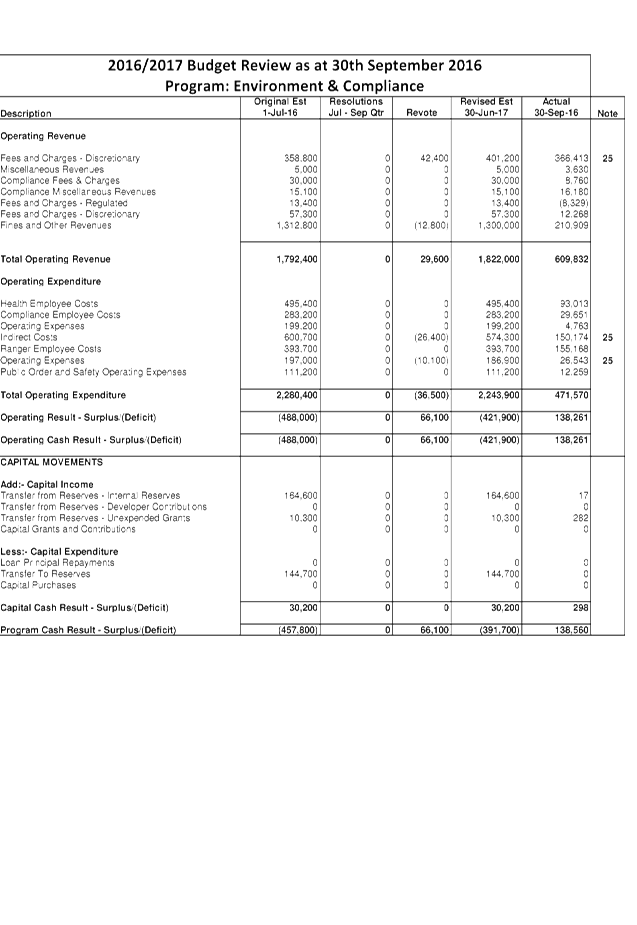

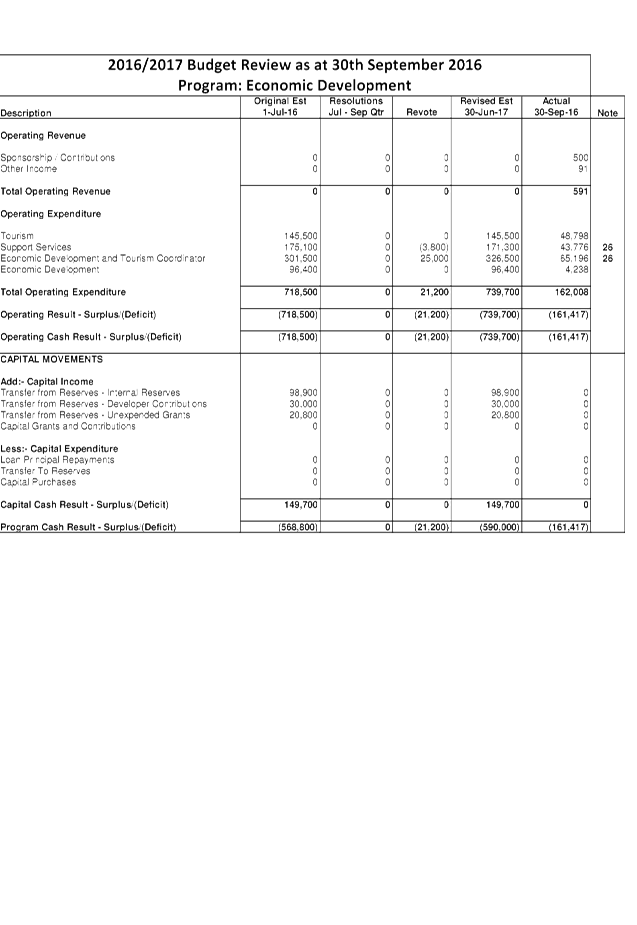

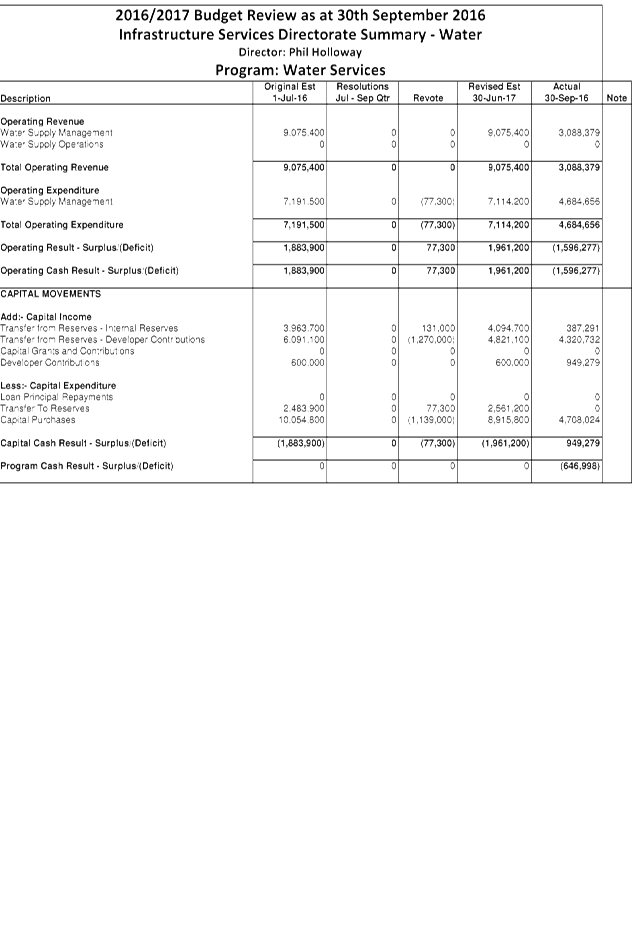

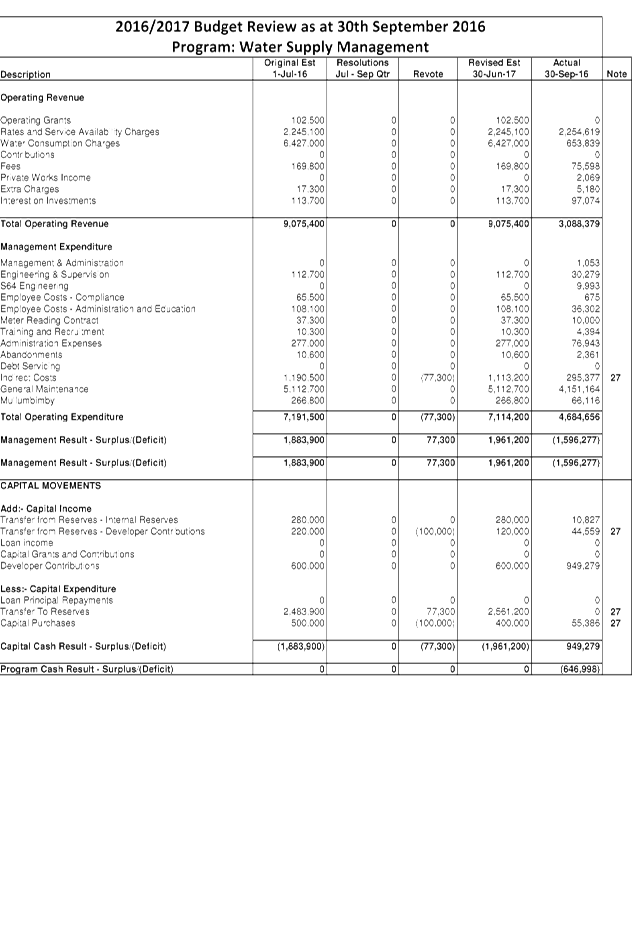

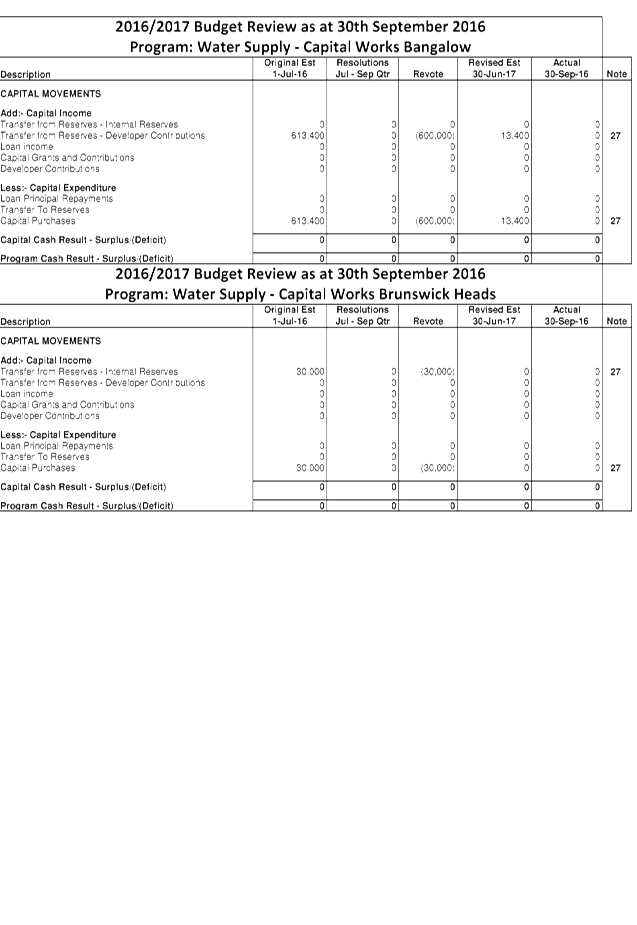

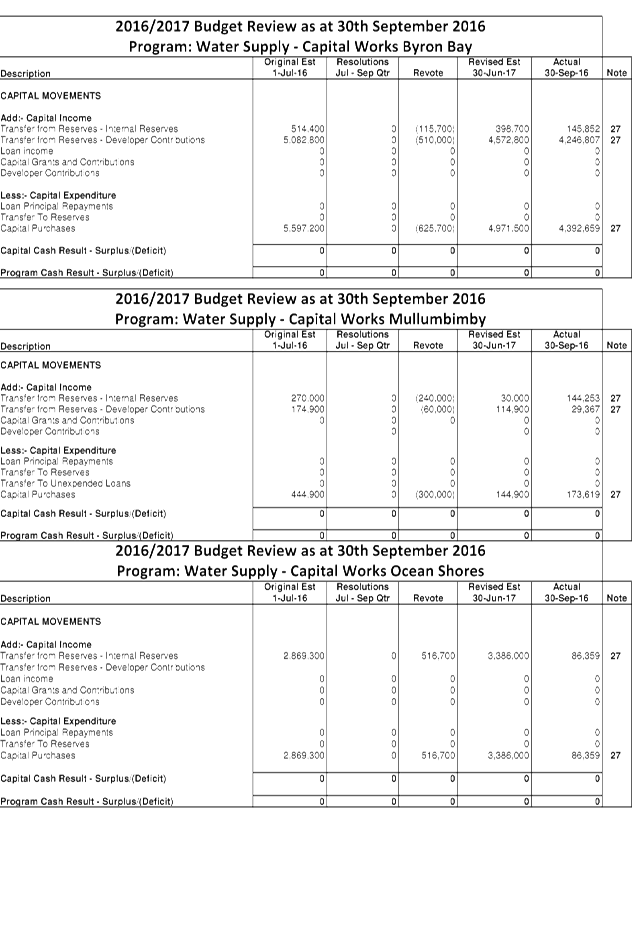

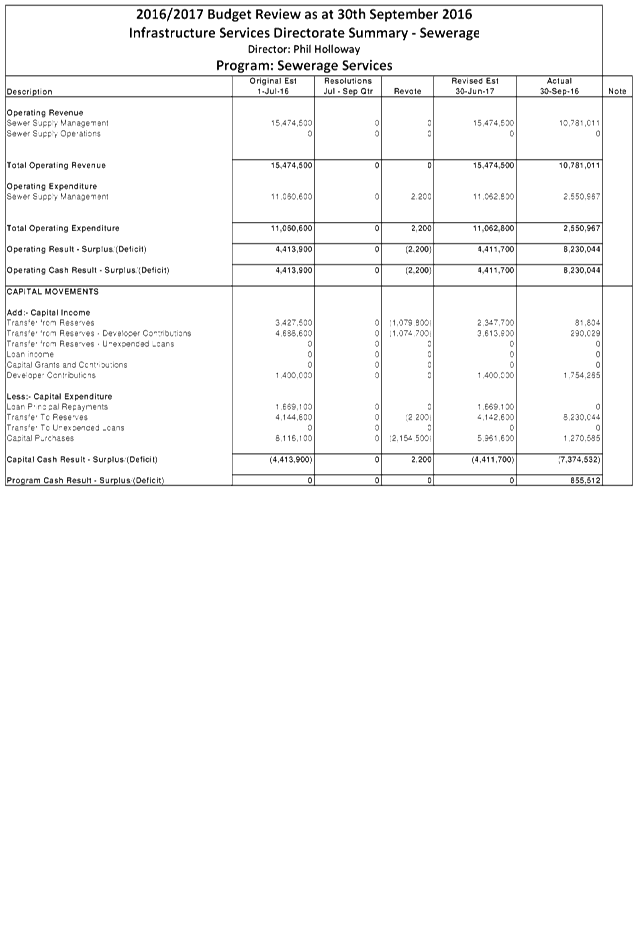

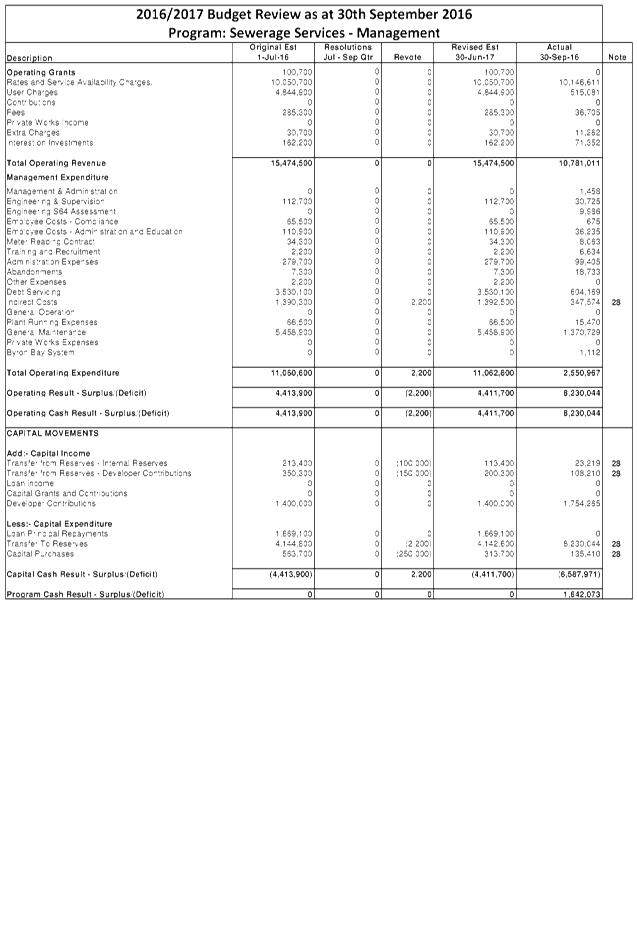

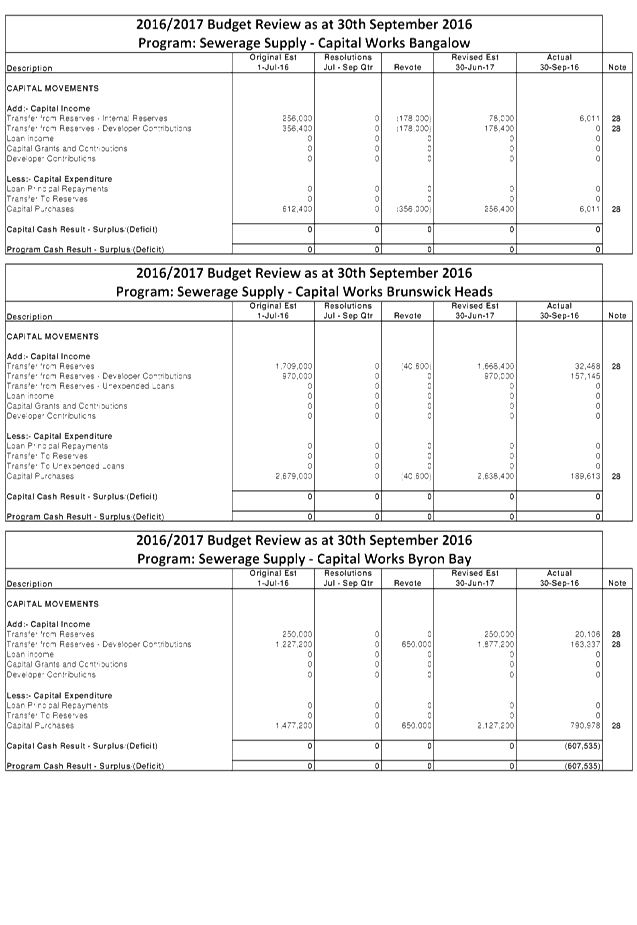

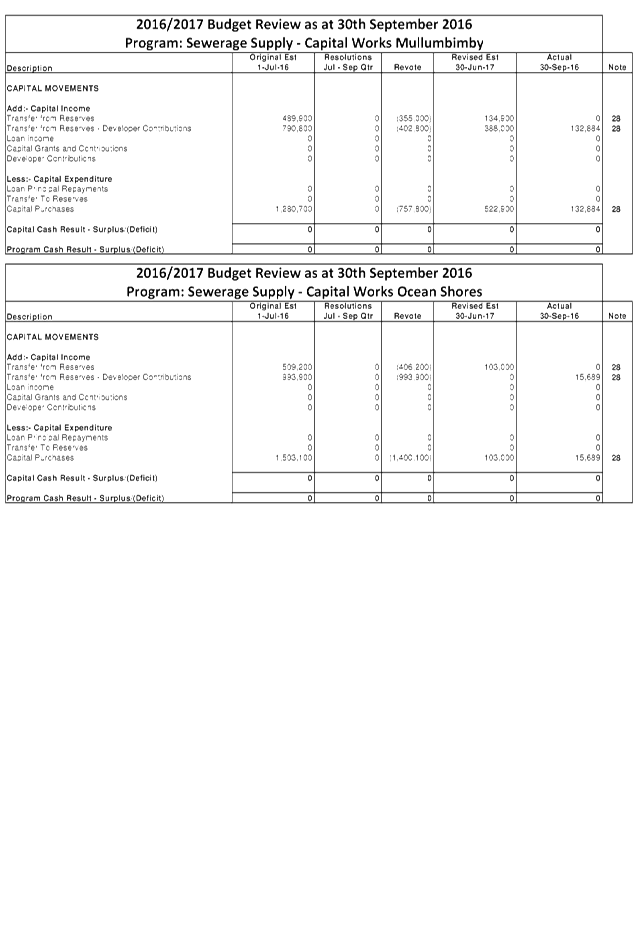

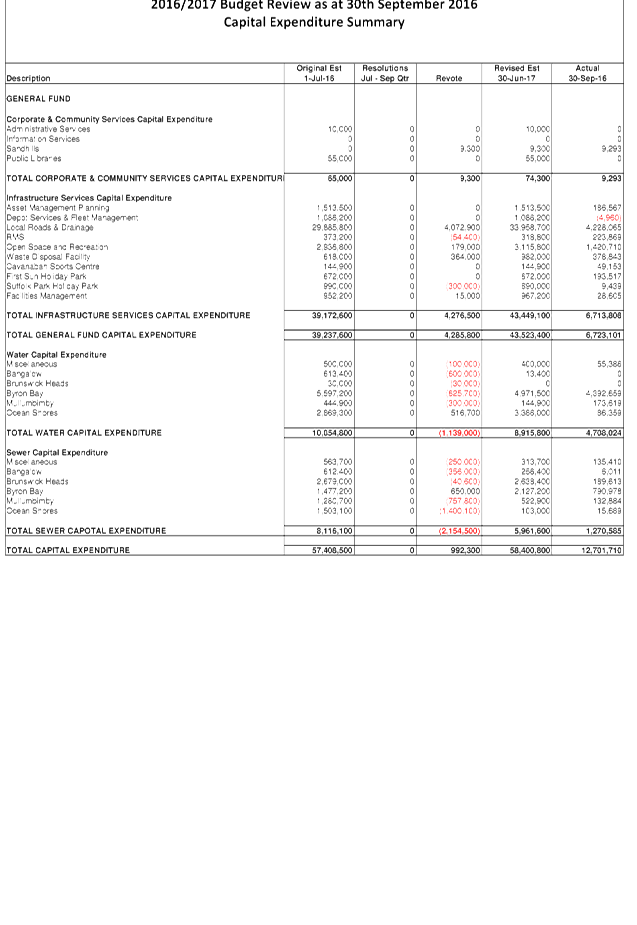

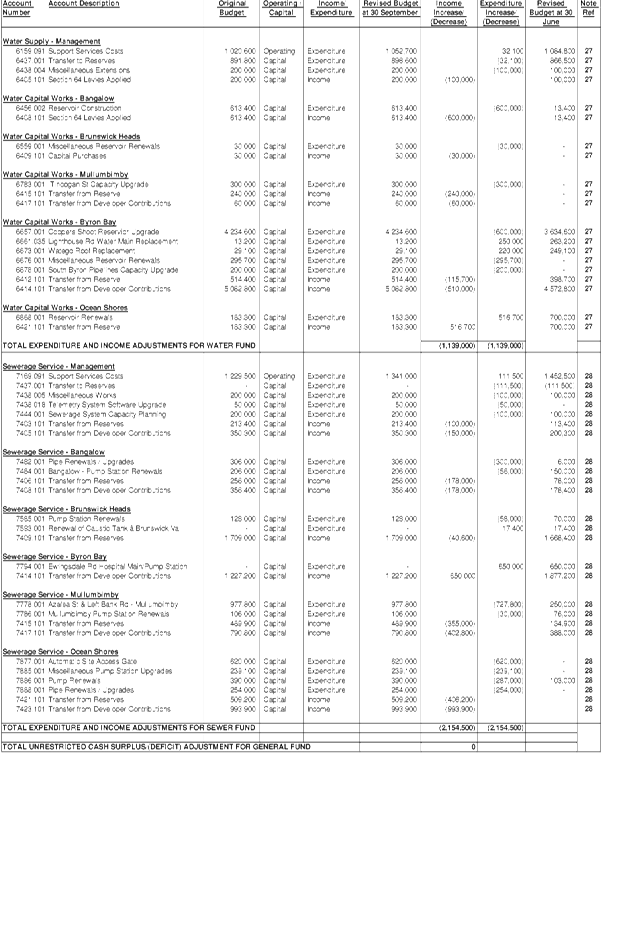

The details of the budget review for the Consolidated,

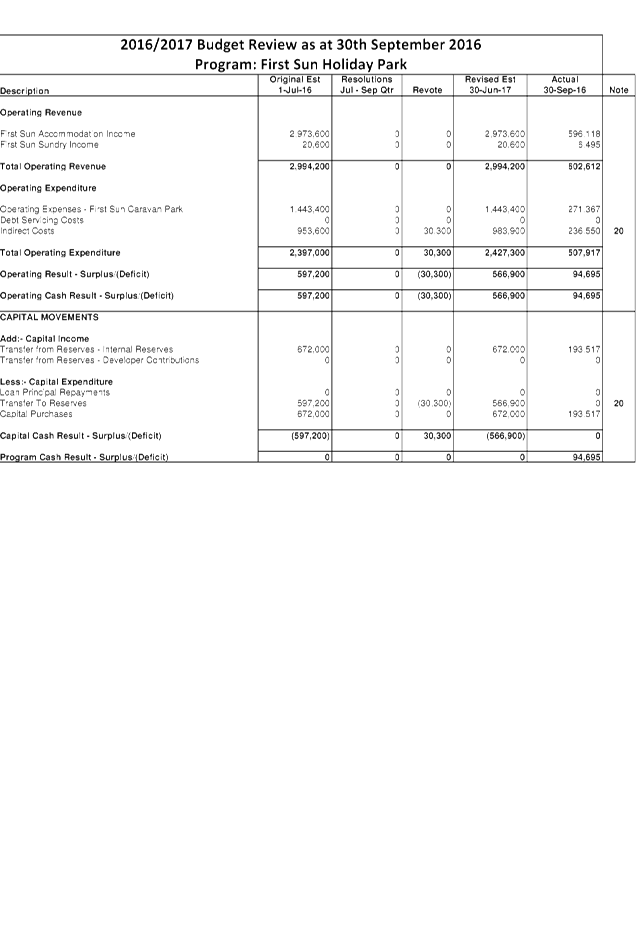

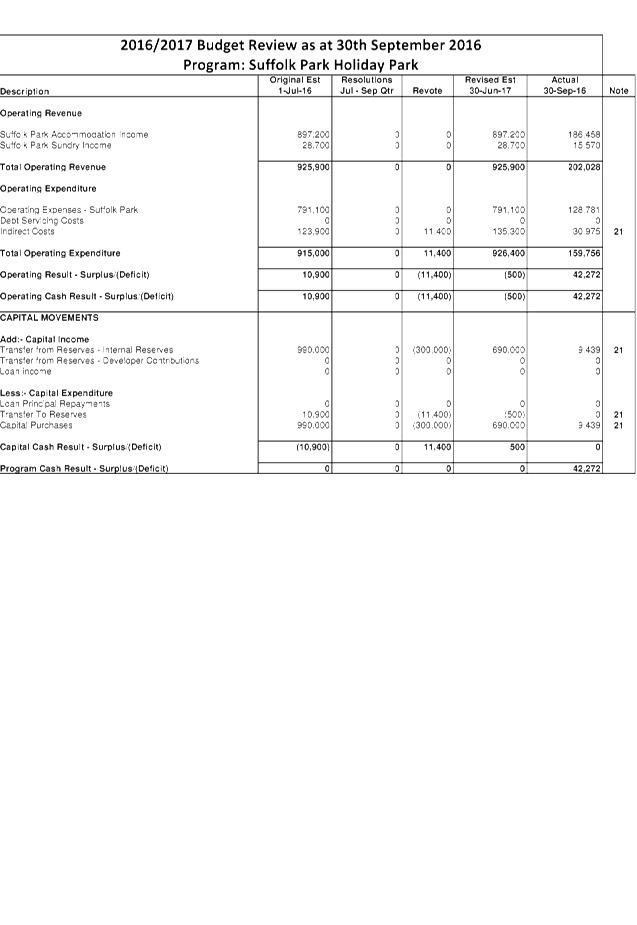

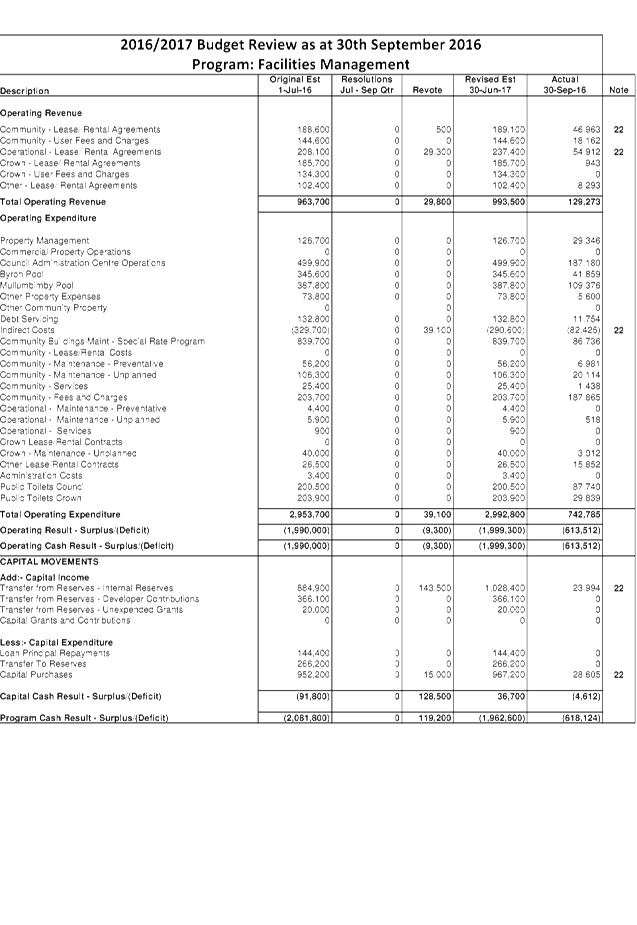

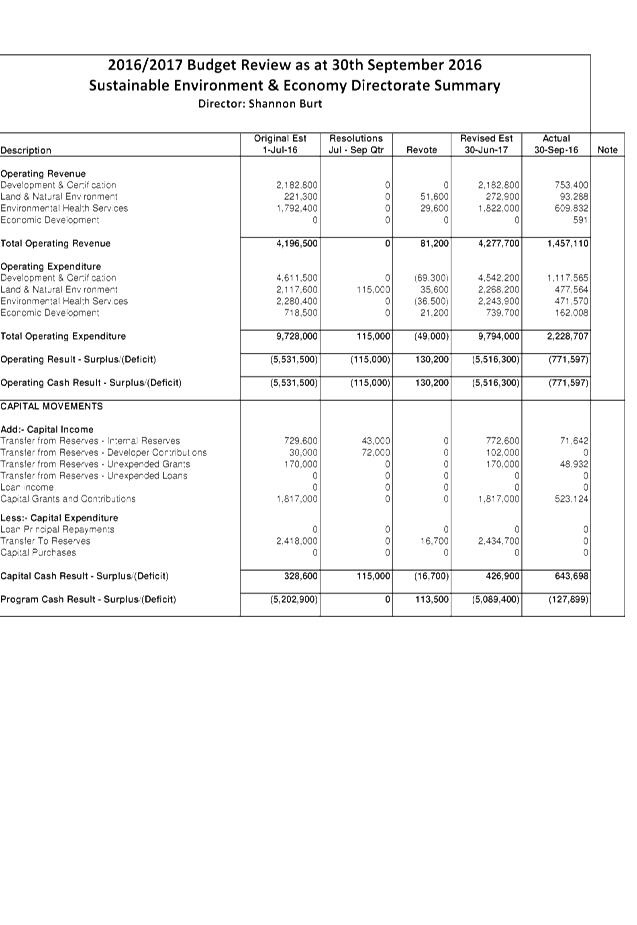

General, Water and Sewer Funds are included in Attachment 1, with an itemised

listing in Attachment 2. This aims to show the consolidated budget

position of Council, as well as a breakdown by Fund and Principal Activity. The

document in Attachment 1 is also effectively a publication outlining a review

of the budget and is intended to provide Councillors with more detailed

information to assist with decision making regarding Council’s finances.

Contained in the document at Attachment 1 is the following

reporting hierarchy:

Consolidated Budget

Cash Result

General Fund Cash

Result Water Fund Cash Result Sewer

Cash Result

Principal Activity Principal

Activity Principal

Activity

Operating Income Operating

Expenditure Capital income Capital

Expenditure

The pages within Attachment 1 are presented (from left to

right) by showing the original budget as adopted by Council on 29 June 2016

plus the adopted carryover budgets from 2015/2016 followed by the resolutions

between July and September and the revote (or adjustment for this review) and

then the revised position projected for 30 June 2017 as at 30 September 2016.

On the far right of the Principal Activity, there is a

column titled “Note”. If this is populated by a number, it

means that there has been an adjustment in the quarterly review. This

number then corresponds to the notes at the end of the Attachment 1 which

provides an explanation of the variation.

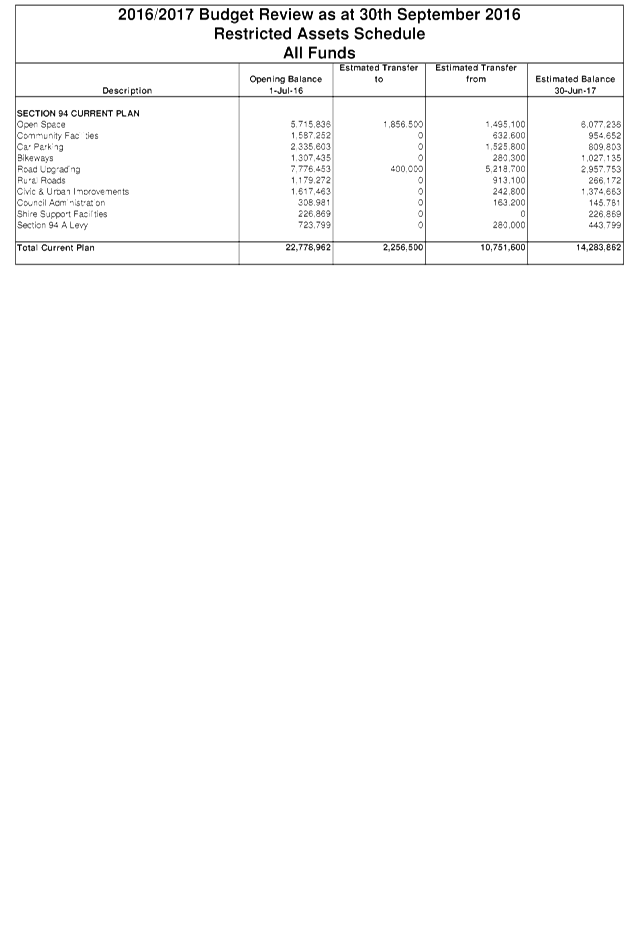

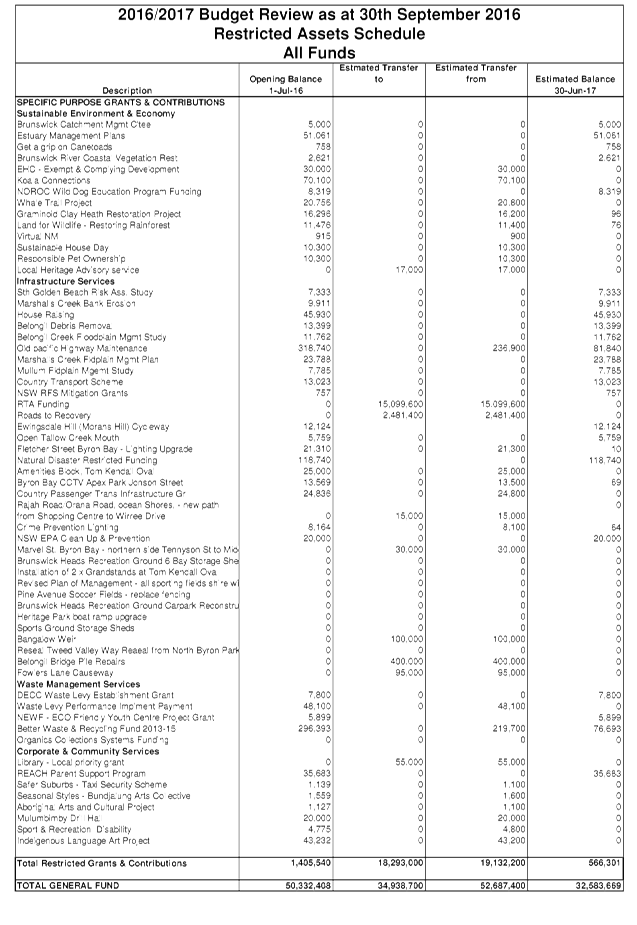

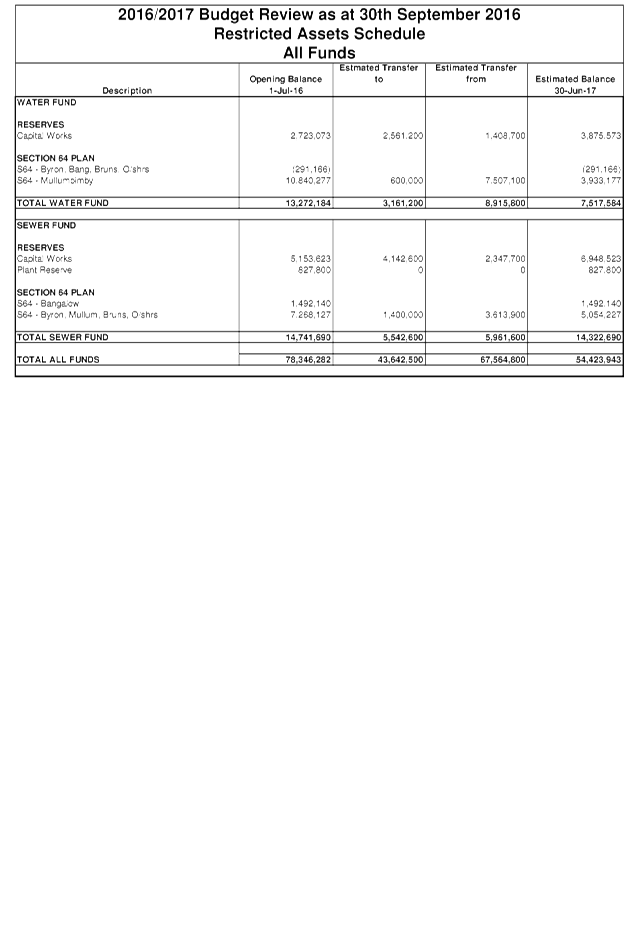

There is also information detailing restricted assets

(reserves) to show Council estimated balances as at 30 June 2017 for all

Council’s reserves.

A summary of Capital Works is also included by Fund and

Principal Activity.

Office of Local Government Budget Review Guidelines:-

The Office of Local Government on 10 December 2010 issued

the new Quarterly Budget Review Guidelines via Circular 10-32, with the

reporting requirements to apply from 1 July 2011. This report includes a

Quarterly Budget Review Statement (refer Attachment 3) prepared by Council in

accordance with the guidelines.

The Quarterly Budget Review Guidelines set a minimum

standard of disclosure, with these standards being included in the Local

Government Code of Accounting Practice and Financial Reporting as mandatory

requirements for Council’s to address.

Since the introduction of the new planning and reporting

framework for NSW Local Government, it is now a requirement for Councils to

provide the following components when submitting a Quarterly Budget Review

Statement (QBRS):-

· A signed statement

by the Responsible Accounting Officer on Councils financial position at the end

of the year based on the information in the QBRS

· Budget review

income and expenses statement in one of the following formats:

o Consolidated

o By fund (e.g General, Water,

Sewer)

o By function, activity, program

etc to align with the management plan/operational plan

· Budget Review

Capital Budget

· Budget Review Cash

and Investments Position

· Budget Review Key

performance indicators

· Budget Review

Contracts and Other Expenses

The above components are included in Attachment 3:-

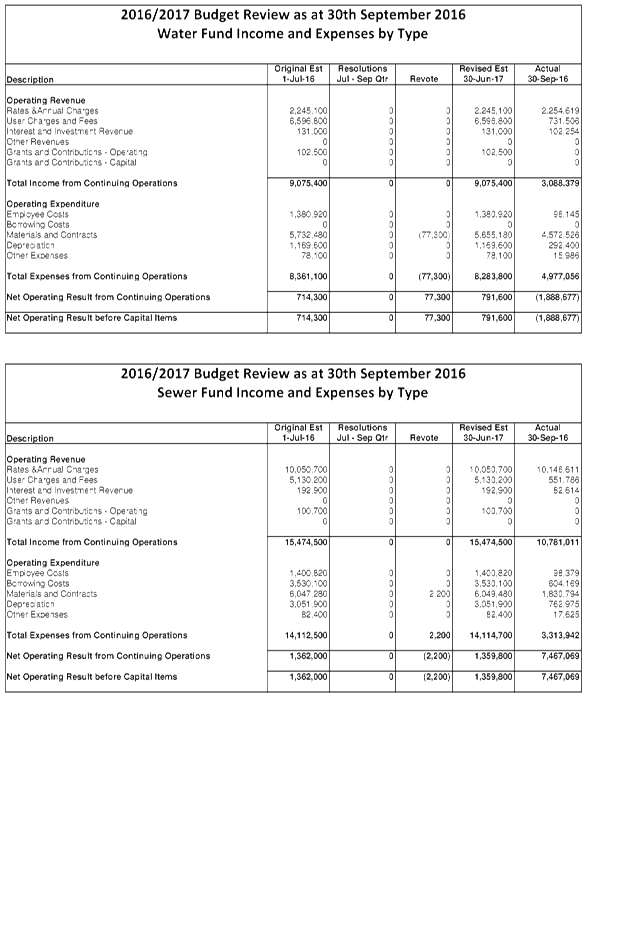

Income and Expenditure Budget

Review Statement by Type – This shows Councils income and Expenditure

by type. This has been split by Fund. Adjustments are shown,

looking from left to right. These adjustments are commented on through

pages 51 to 62 of Attachment 1.

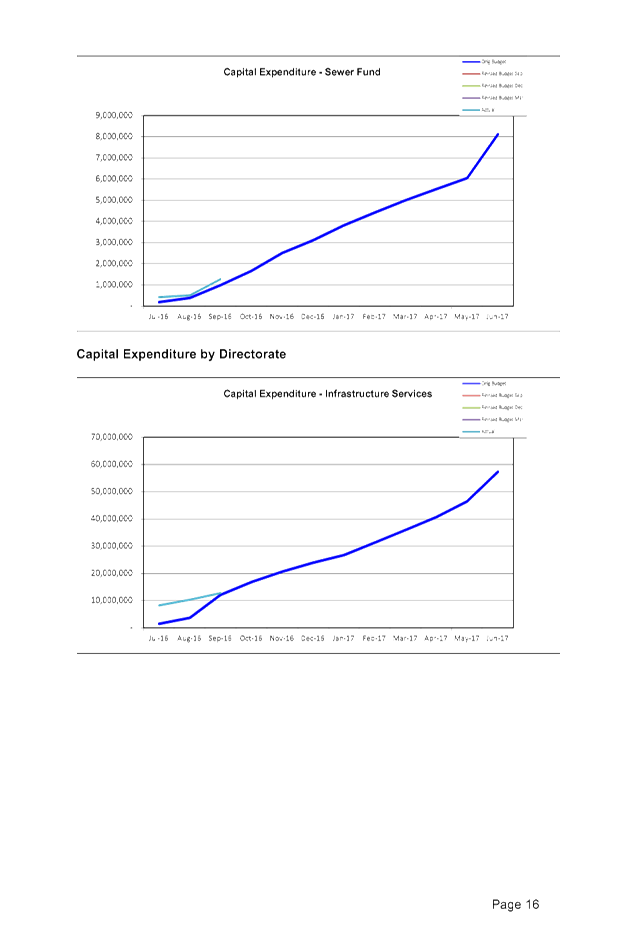

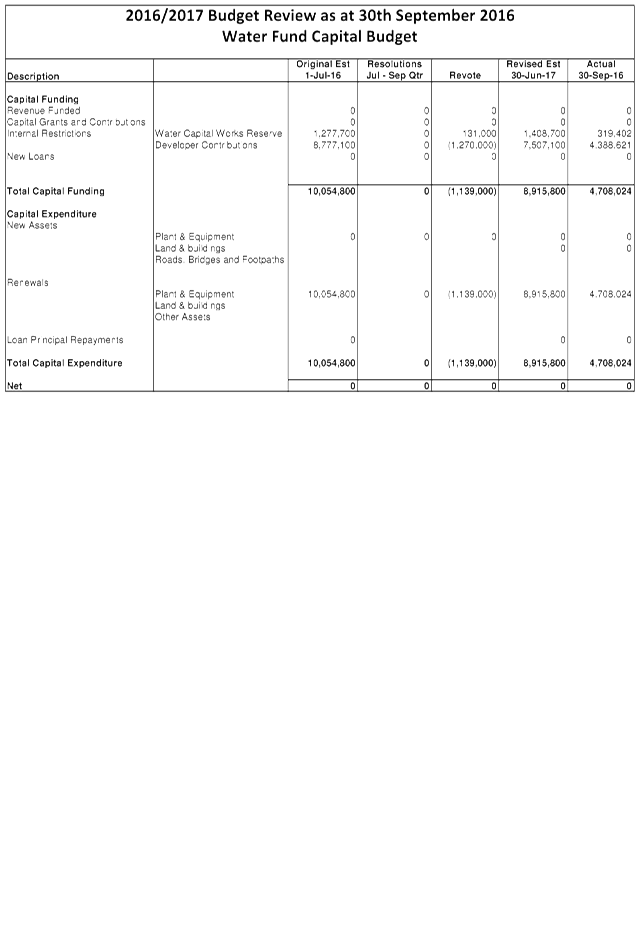

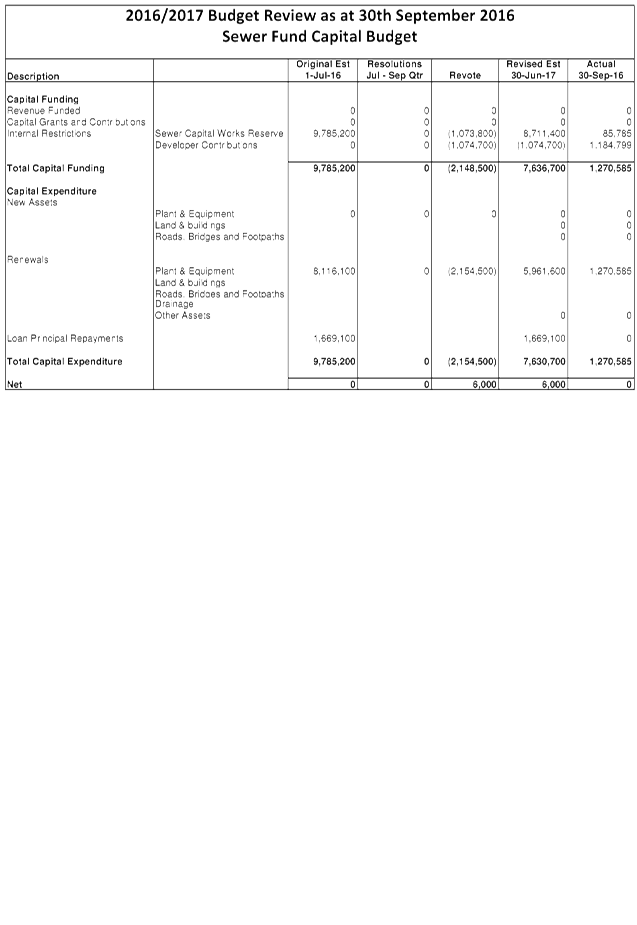

Capital Budget Review Statement

– This statement identifies in summary Council’s capital works

program on a consolidated basis and then split by Fund. It also

identifies how the capital works program is funded. As this is the first

quarterly review for the reporting period, the Statement may not necessarily

indicate the total progress achieved on the delivery of the capital works

program.

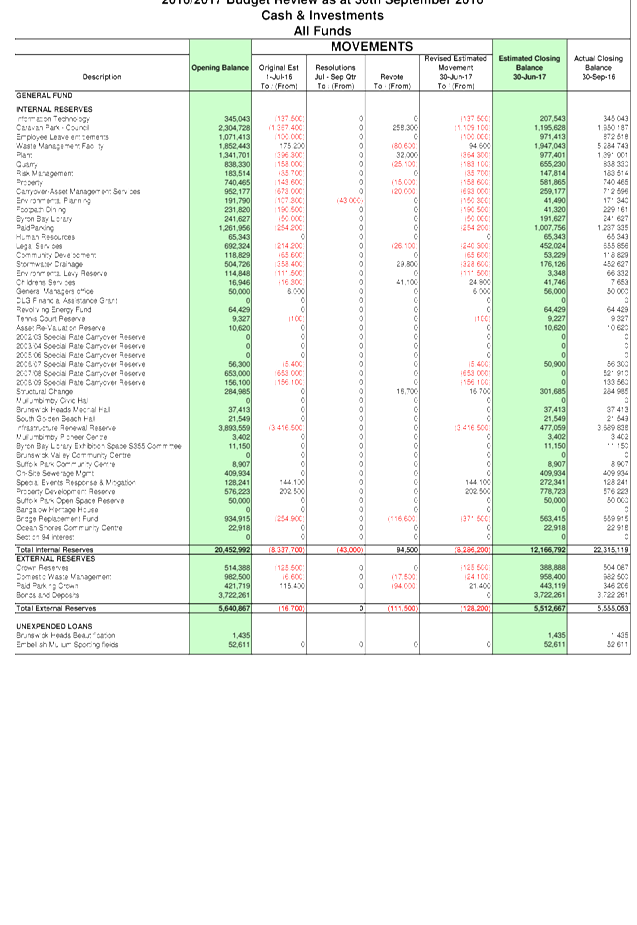

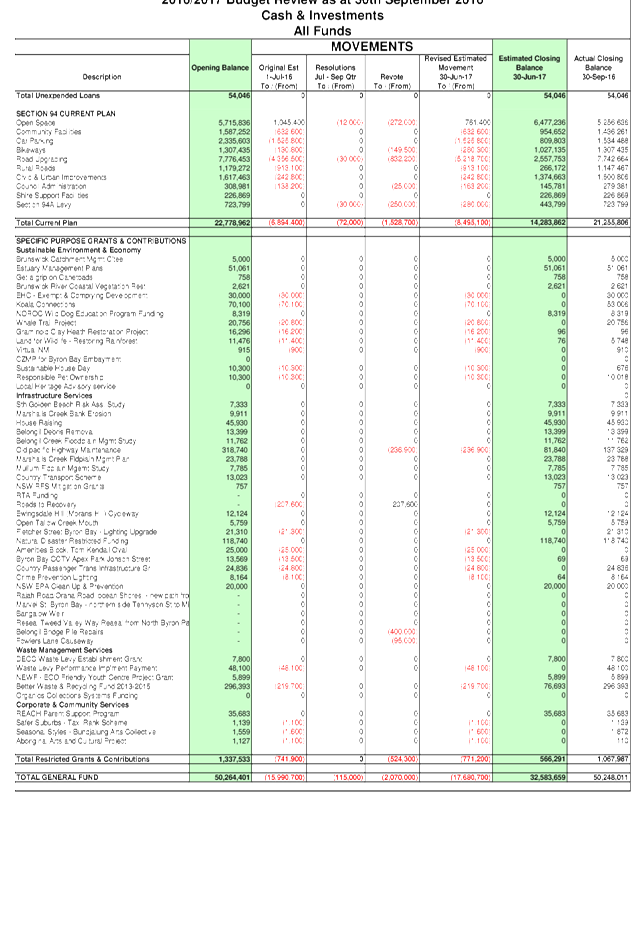

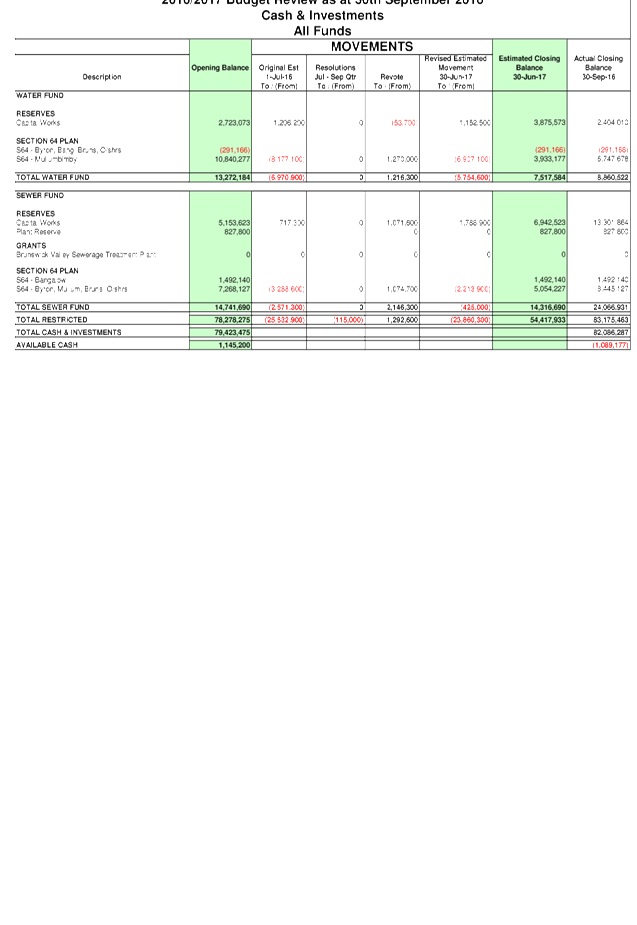

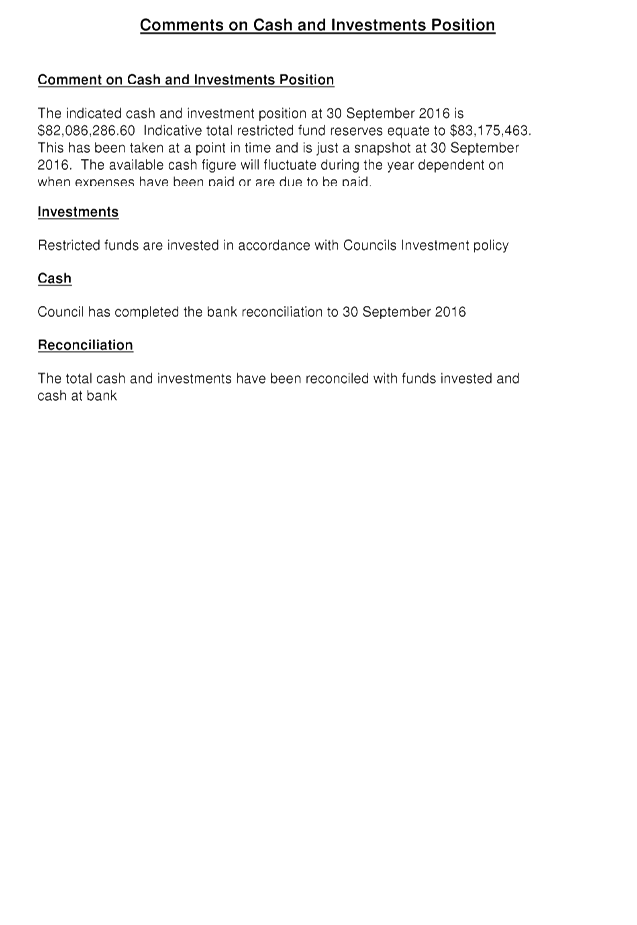

Cash and Investments Budget

Review Statement – This statement reconciles Council’s

restricted funds (reserves) against available cash and investments.

Council has attempted to indicate an actual position as at 30 September 2017 of

each reserve to show a total cash position of reserves with any difference

between that position and total cash and investments held as available cash and

investments. It should be recognised that the figure is at a point in

time and may vary greatly in future quarterly reviews pending on cash flow

movements.

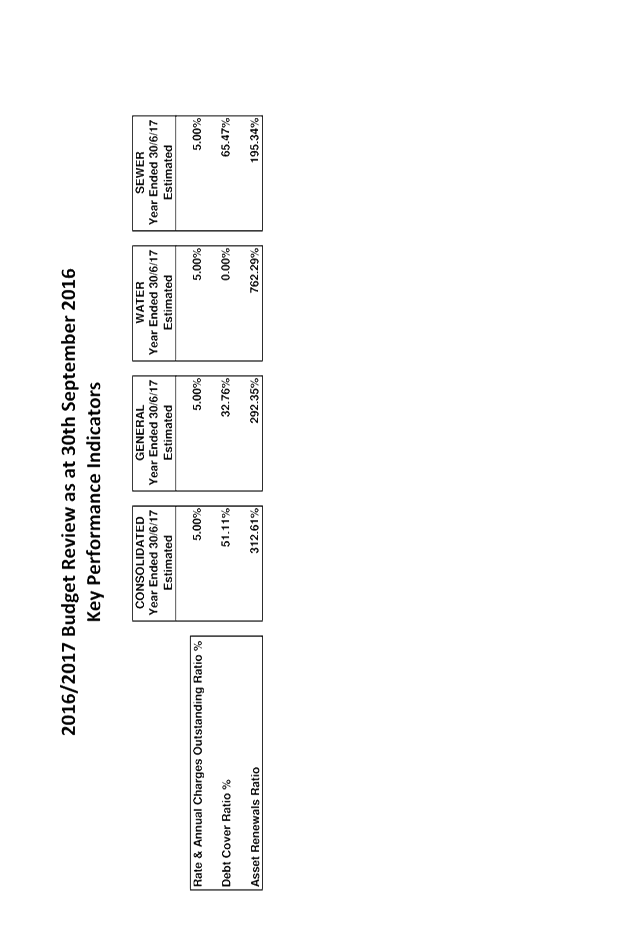

Key Performance Indicators

(KPI’s) – At this stage, the KPI’s within this

report are:-

o Debt Service Ratio -

This assesses the impact of loan principal and interest repayments on the

discretionary revenue of Council.

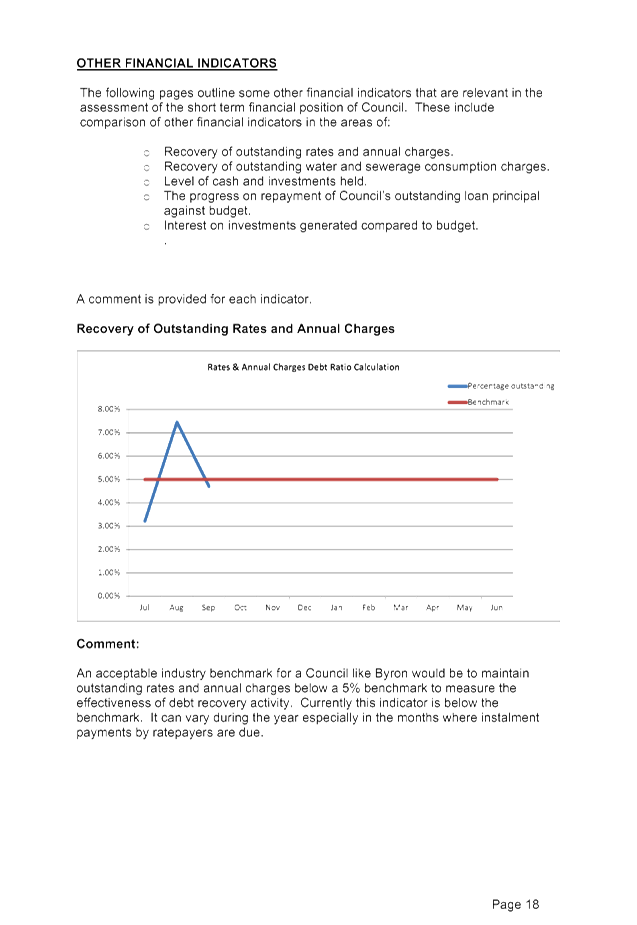

o Rates and Annual Charges

Outstanding Ratio – This assesses the impact of uncollected rates and

annual charges on Councils liquidity and the adequacy of recovery efforts

o Asset Renewals Ratio

– This assesses the rate at which assets are being renewed relative

to the rate at which they are depreciating.

These may be expanded in future

to accommodate any additional KPIs that Council may adopt to use in the Long

Term Financial Plan (LTFP.)

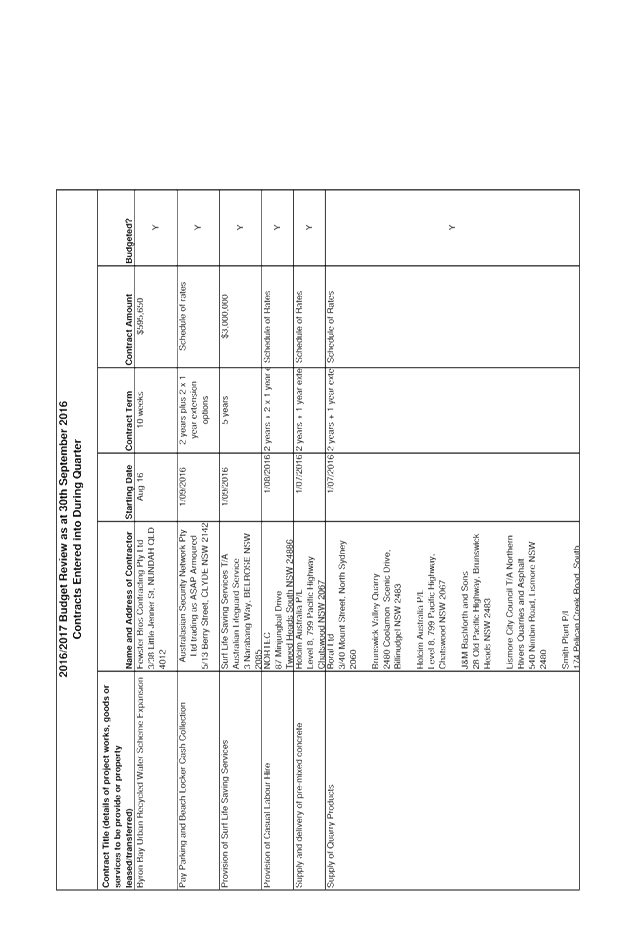

Contracts and

Other Expenses - This report highlights any contracts Council entered into

during the July to September quarter that are greater then $50,000.

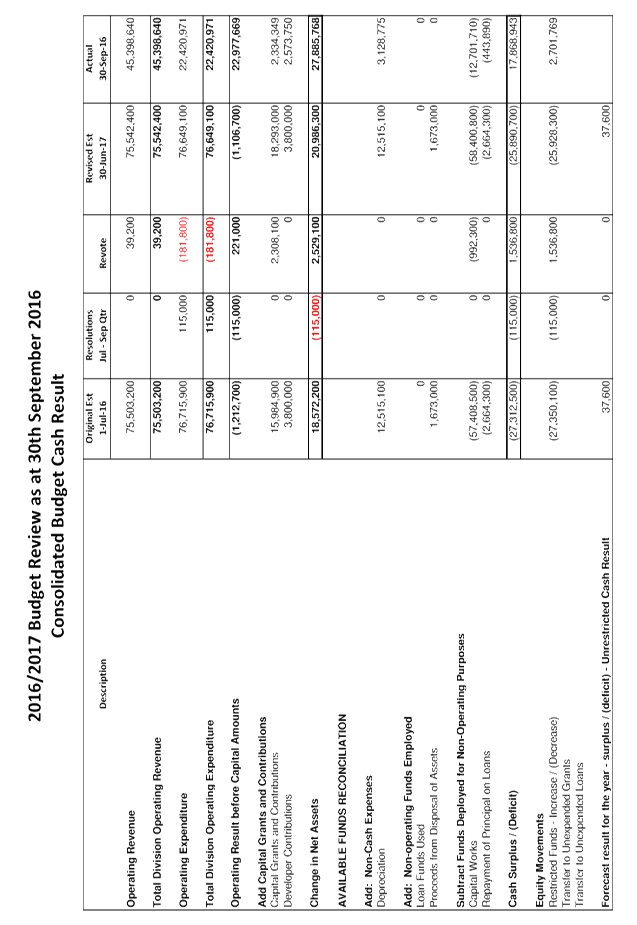

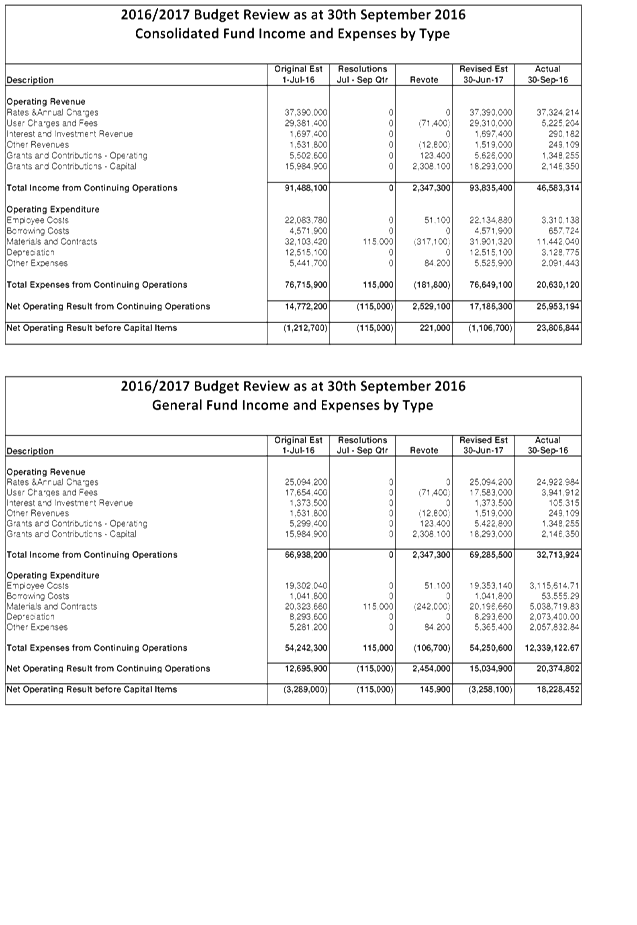

CONSOLIDATED RESULT

The following table provides a summary of the overall

Council budget on a consolidated basis inclusive of all Funds budget movements

for the 2016/2017 financial year projected to 30 June 2017 but revised as at 30

September 2016.

|

2016/2017 Budget Review Statement as at 30 September 2016

|

Original Estimate (Including Carryovers)

1/7/2016

|

Adjustments to Sept 2016 including Resolutions*

|

Proposed Sept 2016 Review Revotes

|

Revised Estimate 30/6/2017 at 30/9/2016

|

|

Operating Revenue

|

75,503,200

|

0

|

39,200

|

75,542,400

|

|

Operating Expenditure

|

76,715,900

|

115,000

|

(181,800)

|

76,649,100

|

|

Operating Result –

Surplus/Deficit

|

(1,212,700)

|

(115,000)

|

221,000

|

(1,106,700)

|

|

Add: Capital Revenue

|

19,784,900

|

0

|

2,308,100

|

22,093,000

|

|

Change in Net Assets

|

18,574,200

|

(115,000)

|

2,529,100

|

20,986,300

|

|

Add: Non Cash Expenses

|

12,515,100

|

0

|

0

|

12,515,100

|

|

Add: Non-Operating Funds

Employed

|

1,673,000

|

0

|

0

|

1,673,000

|

|

Subtract: Funds Deployed for

Non-Operating Purposes

|

(60,072,800)

|

0

|

(992,300)

|

(61,065,100)

|

|

Cash Surplus/(Deficit)

|

(27,312,500)

|

(115,000)

|

1,536,800

|

(25,890,700)

|

|

Restricted Funds –

Increase / (Decrease)

|

(27,350,100)

|

(115,000)

|

1,536,800

|

(25,928,300)

|

|

Forecast Result for the

Year – Surplus/(Deficit) – Unrestricted Cash Result

|

37,600

|

0

|

0

|

37,600

|

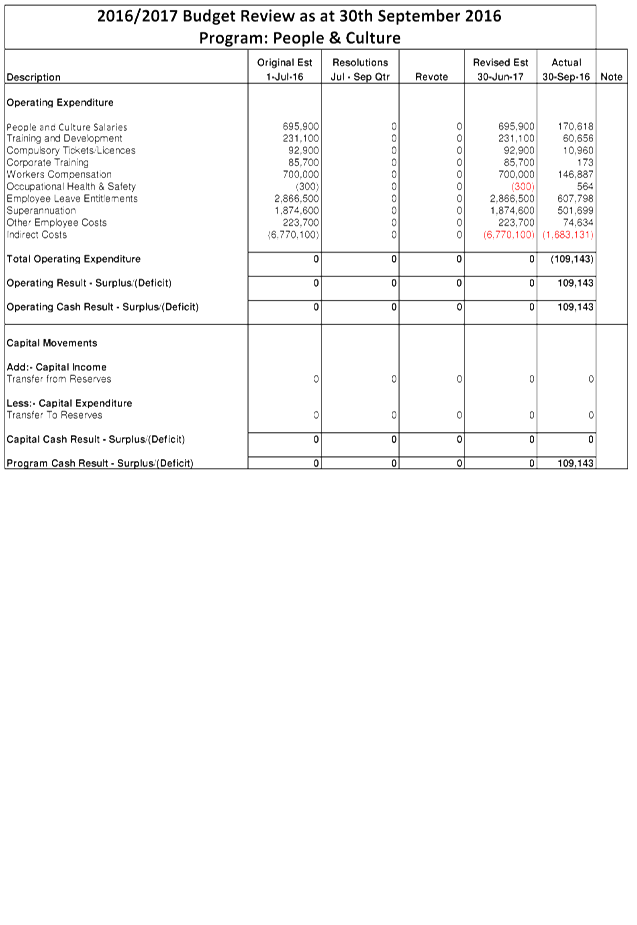

As part of this budget review, there has been a reassessment

of the distribution support costs following implementation of the organisational

restructure. Support costs are distributed across the primary activities

of Council to reflect actual costs of those services. Budget programs

such as People and Culture, Finance, Information Technology and Governance are

examples of Council activities that provide support and where costs

are distributed to the primary activities of Council or

output service areas. In this review, the costs of the General Manager

Directorate which contains Organisation Development, Media/Communications,

Customer Service and Organisation Development were revised to be allocated

based on budgeted expenditure as opposed to the previous method of full time

staff to reflect a more appropriate allocation of these costs. This has

had an effect across most programs with a comment against the relevant budget

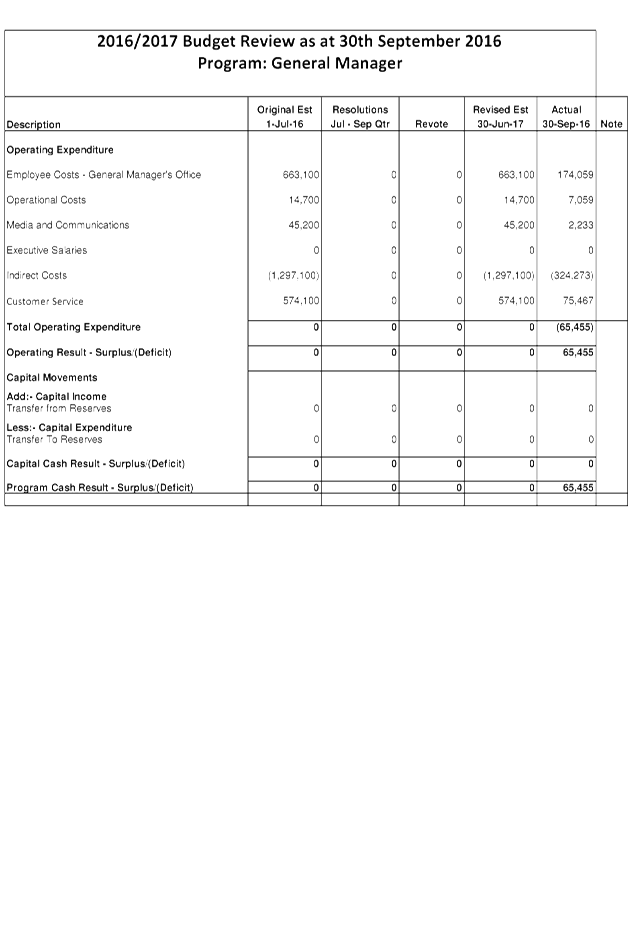

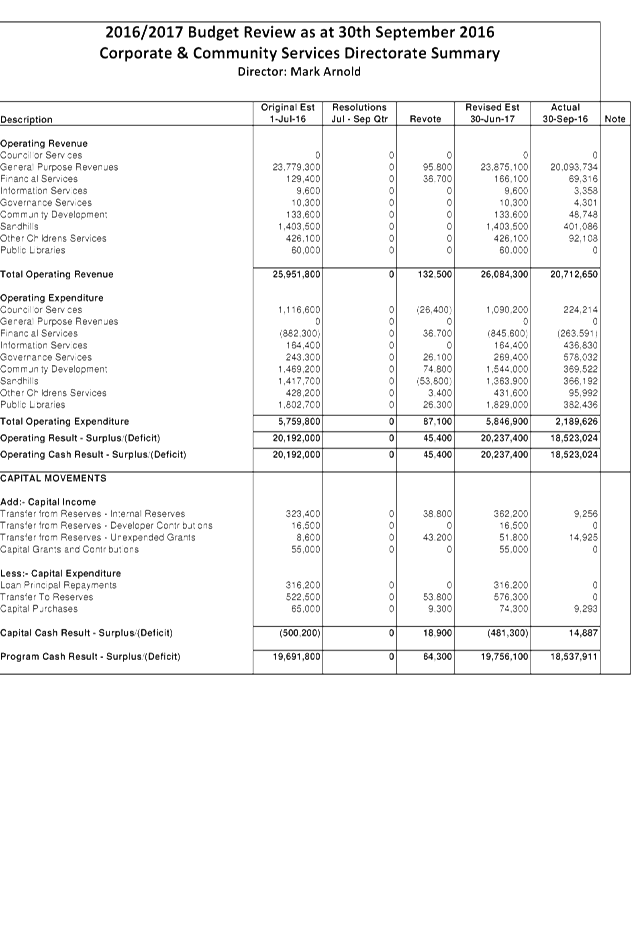

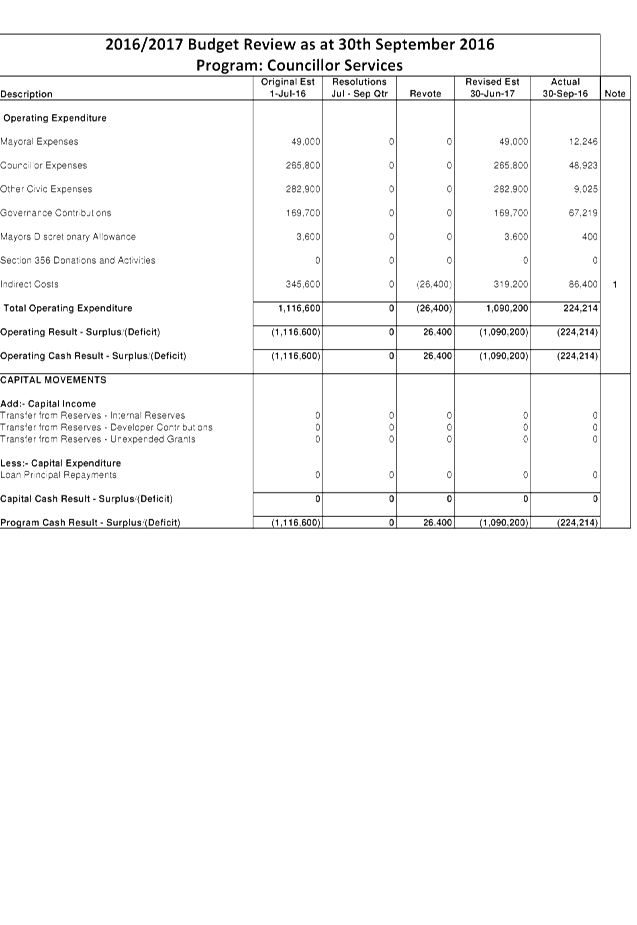

program impacted in attachment 1.

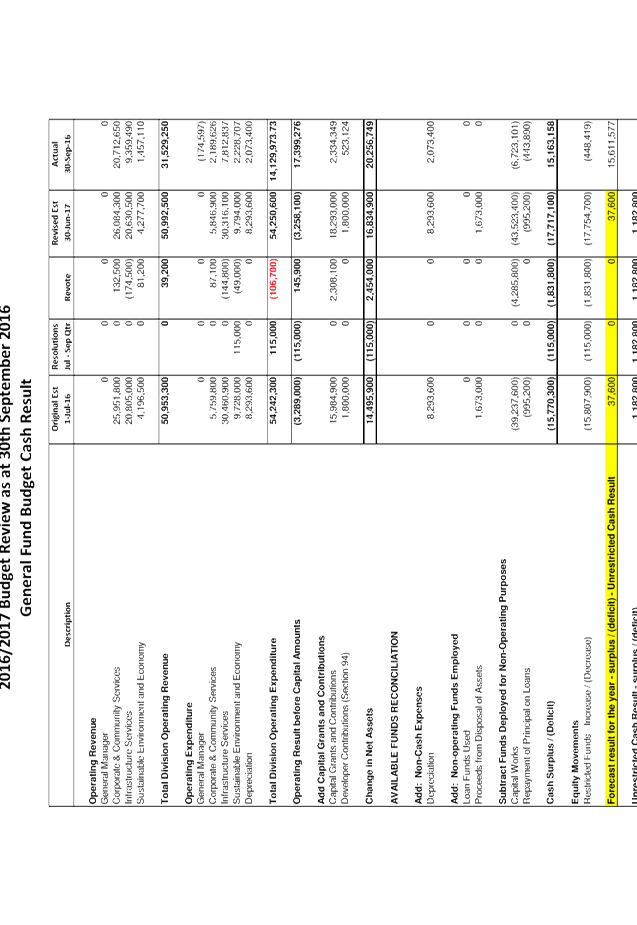

GENERAL FUND

In terms of the General Fund projected Unrestricted Cash

Result the following table provides a reconciliation of the estimated position

as at 30 September 2016:

|

Opening Balance – 1

July 2016

|

$1,145,200

|

|

Plus original budget

movement and carryovers

|

$37,600

|

|

Council Resolutions July

– September Quarter

|

0

|

|

Recommendations within this

Review – increase/(decrease)

|

$0

|

|

Forecast Unrestricted

Cash Result – Surplus/(Deficit) – 30 June 2017

|

$37,600

|

|

Estimated Unrestricted

Cash Result Closing Balance – 30 June 2017

|

$1,182,800

|

The General Fund financial position overall has not changed

as a result of this budget review. However there are proposed changes to

the budget as a result of this review. The proposed budget changes are detailed

in Attachment 1 and summarised further in this report below.

Council Resolutions

There were no Council resolutions during the July to

September 2016 quarter that impacted the overall 2016/2017 budget result.

Budget Adjustments

The budget adjustments identified in Attachments 1 and 2 for

the General Fund have been summarised by Budget Directorate in the following

table:

|

Budget Directorate

|

Revenue

Increase/

(Decrease) $

|

Expenditure

Increase/

(Decrease) $

|

Accumulated

Surplus (Working Funds) Increase/ (Decrease) $

|

|

General Manager

|

0

|

0

|

0

|

|

Corporate & Community Services

|

215,000

|

150,200

|

64,800

|

|

Infrastructure Services

|

3,927,600

|

4,105,900

|

(178,300)

|

|

Sustainable Environment & Economy

|

81,200

|

(32,300)

|

113,500

|

|

Total Budget Movements

|

4,223,800

|

4,223,800

|

0

|

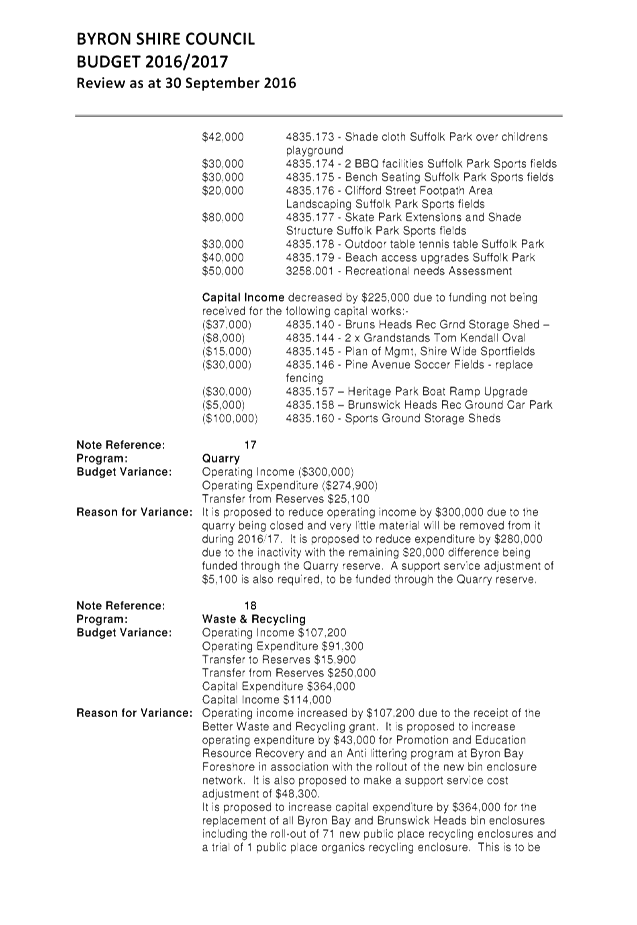

Budget Adjustment Comments

Within each of the Budget Directorates of the General Fund,

are a series of budget adjustments identified in detail at Attachment 1 and

2. More detailed notes on these are provided in Attachment 1 but in

summary the major additional items included are summarised below by Directorate

and are included in the overall budget adjustments table above:

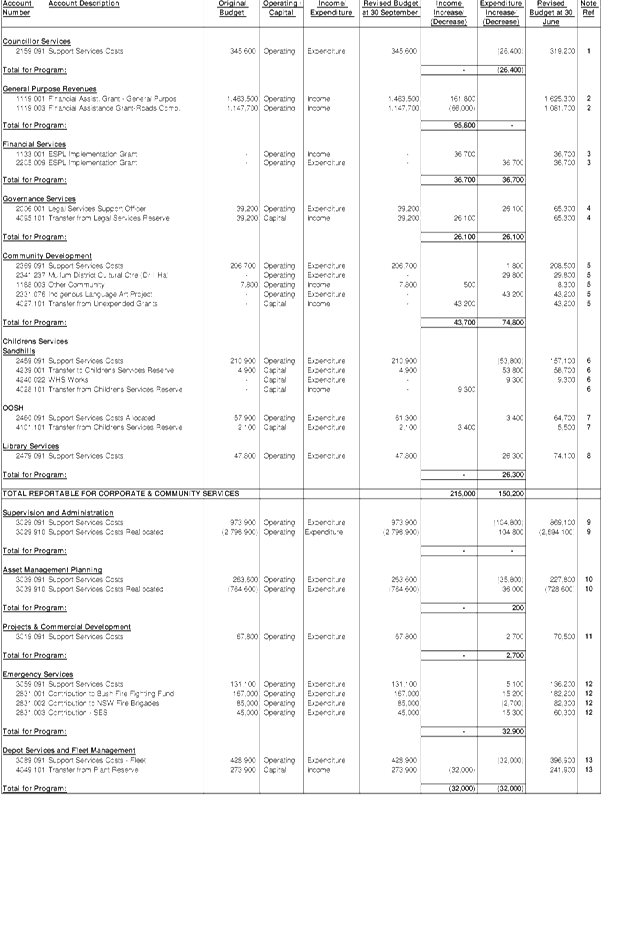

Corporate and Community Services

· In the General

Purpose Revenues Program an additional $95,800 in revenue has been recognised

as the allocation for Council’s 2016/2017 Financial Assistance Grant is

$95,800 more then budgeted. The original budget for this grant replicated

the 2015/16 amount as Councils were advised that the Financial Assistance Grant

would be frozen for four years from the 2014 Federal Budget. Council though has

received an increased allocation following determination from the NSW Local

Government Grants Commission as to the distribution of the Financial Assistance

Grant allocated to NSW.

· In the Financial

Services Program there is a proposed budget adjustment for additional income

and expenditure of $36,700 due to a grant that was received from the NSW

Treasury for the implementation of the Emergency Services Property Levy

(ESPL). The ESPL will replace the Emergency Services Levy (ESL) that is

currently collected as part of all property-based insurance policies and will

be paid by all property owners alongside Council rates. This grant will

assist with the implementation of this new charge.

· In the Governance

Services Program it is proposed to increase expenditure by $26,100 to increase

the number of days per week from 3 to 5 for the position of Legal Services

Support Officer to provide additional resource to Legal Services to assist with

work volumes. Funding for this is to be provided by the Legal Services

Reserve.

· In the Community

Development Program, expenditure has increased due to the Indigenous Language

Arts project ($43,200 – funded from an unexpended grant) and a new 5 year

licence agreement with the Mullumbimby District Cultural Centre for the

Mullumbimby Drill hall ($29,800). This is funded from a rent subsidy by

Council of $29,300 (The corresponding income adjustment is in the Facilities

management program) and Licensee rent of $500.

· In the Sandhills

program, it is proposed to reduce the support service costs by $53,800 as

mentioned previously in this report and to increase the budget for required WHS

works on the building and its grounds ($9,300). These movements have no

net effect on the result as all movements are taken up through the

Childrens’ Service reserve.

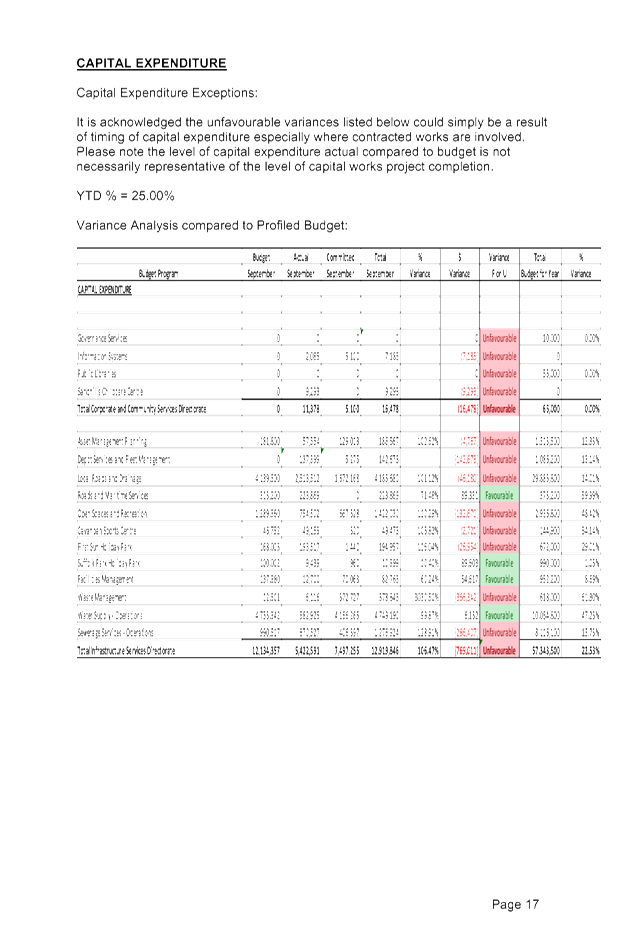

Infrastructure Services

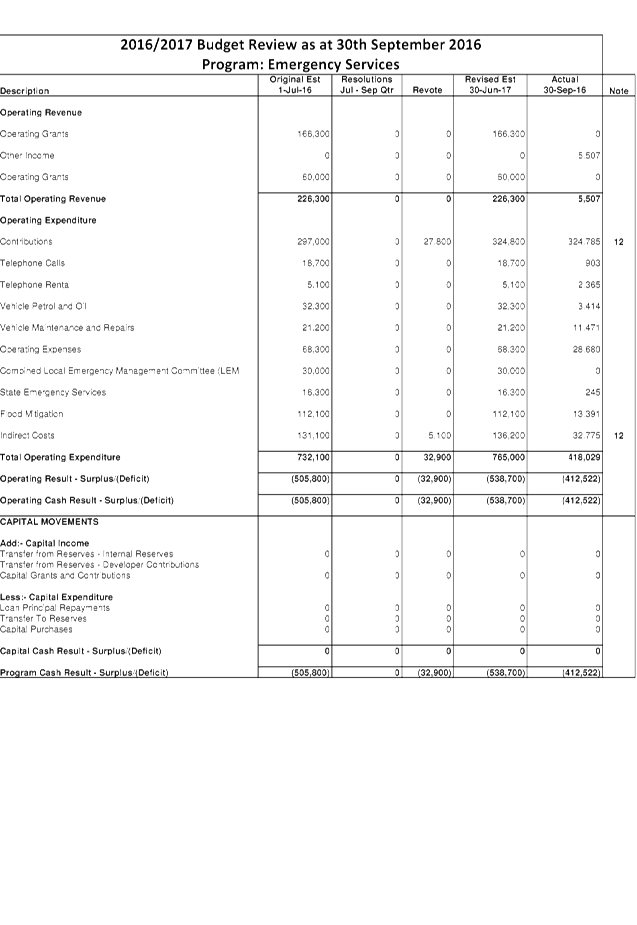

· In the Emergency

Services program, it is proposed to increase the expenditure budget to allow

for the increase in contributions to the Rural Fire Service, NSW Fire Brigade

and the SES. This is to reflect the actual cost to be incurred by Council

as advised by the NSW Government.

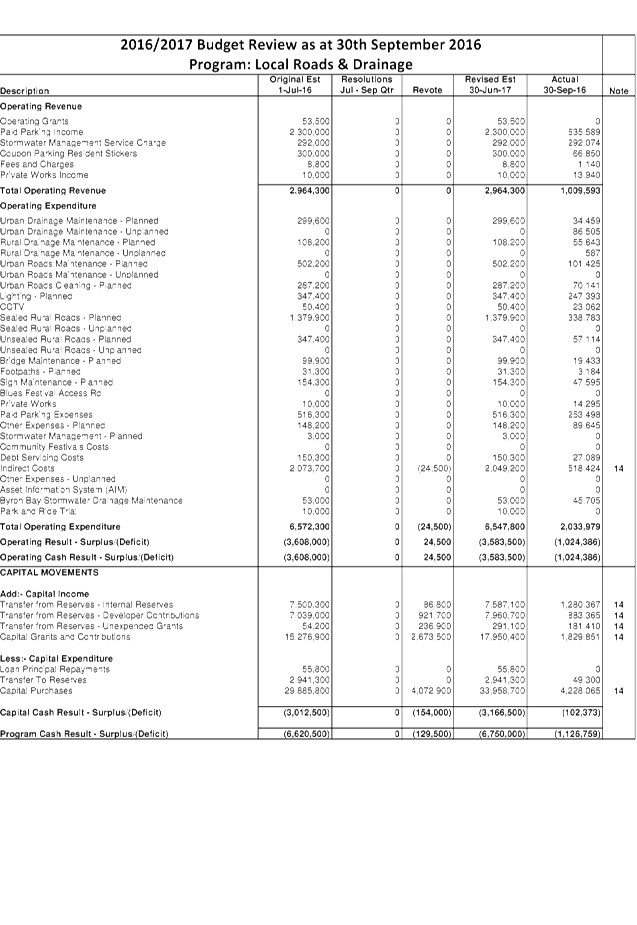

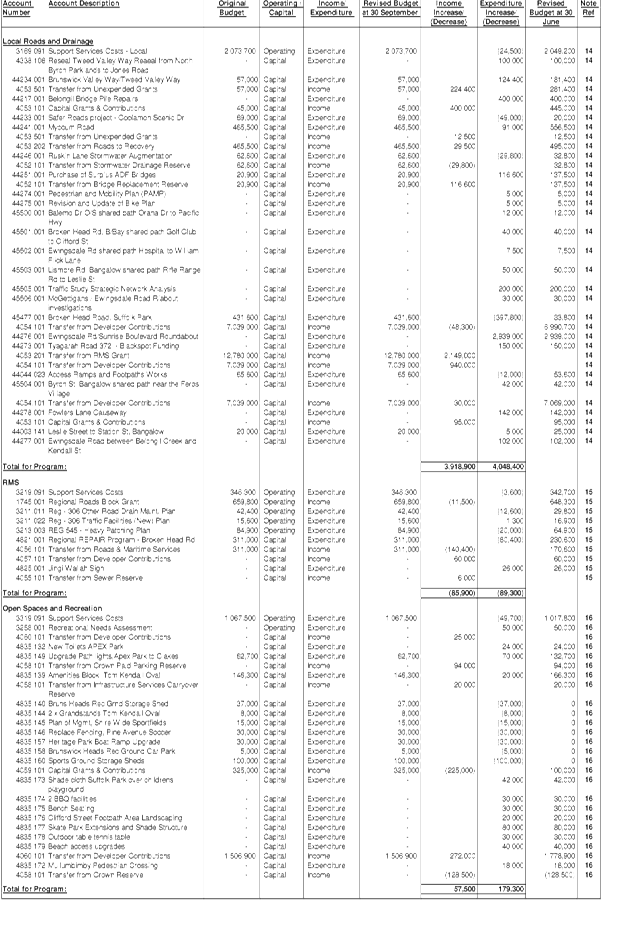

· In the Local Roads

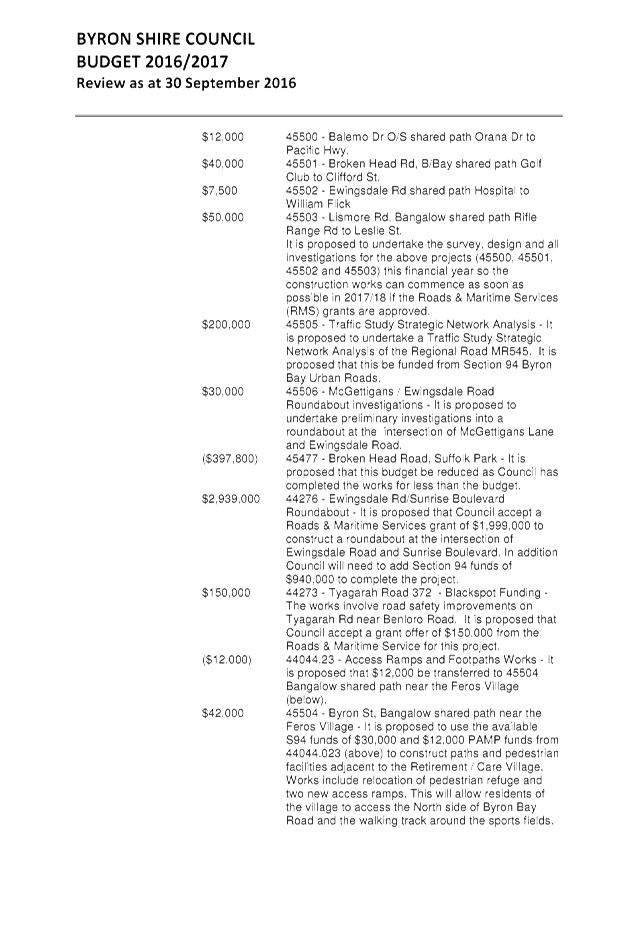

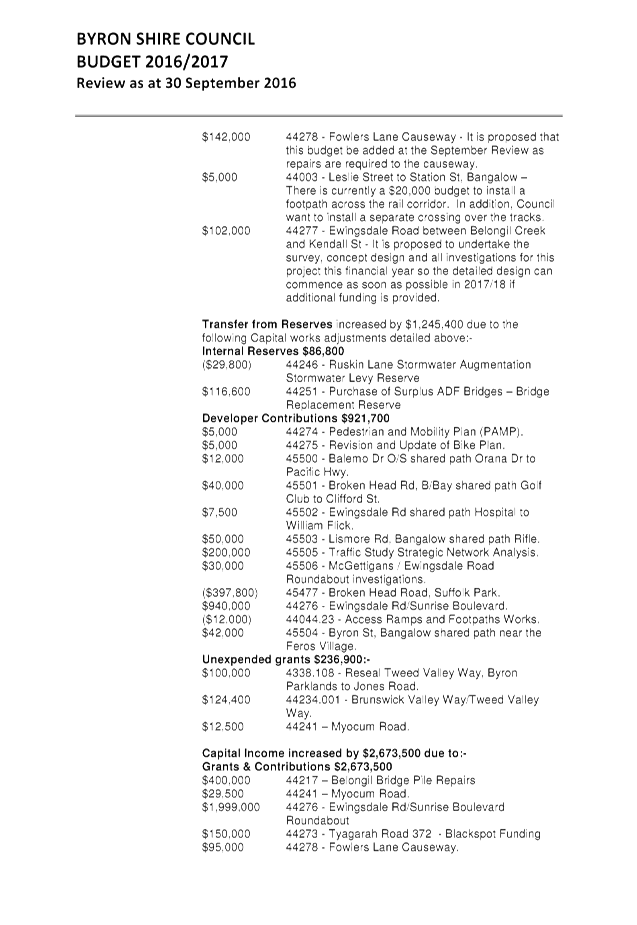

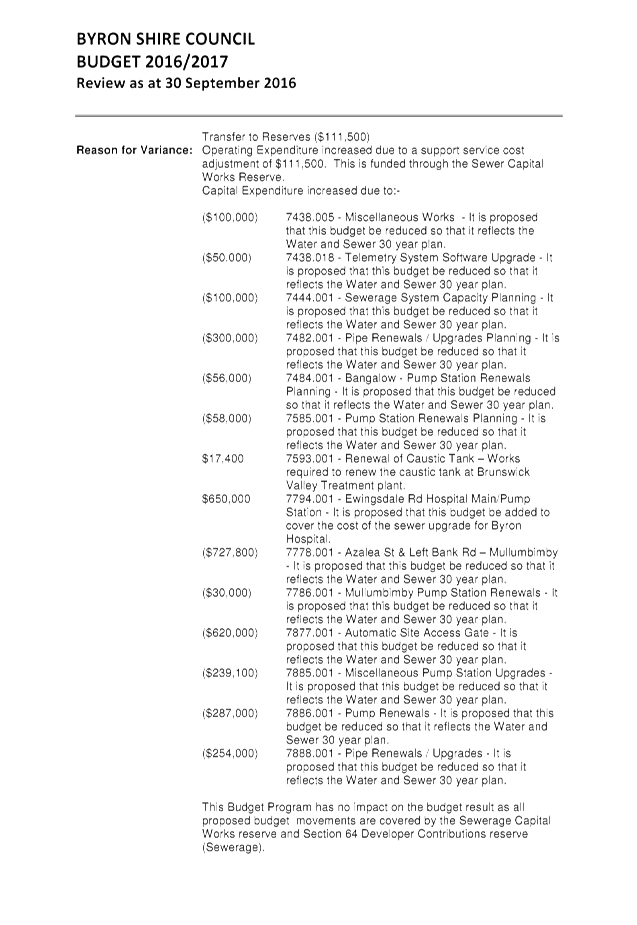

and Drainage program, there are a number of adjustments outlined under Note 14

in the Budget Variations explanations section of Attachment 1. Further

disclosure is included in the second page of Attachment 2 under the budget

program heading Local Roads and Drainage.

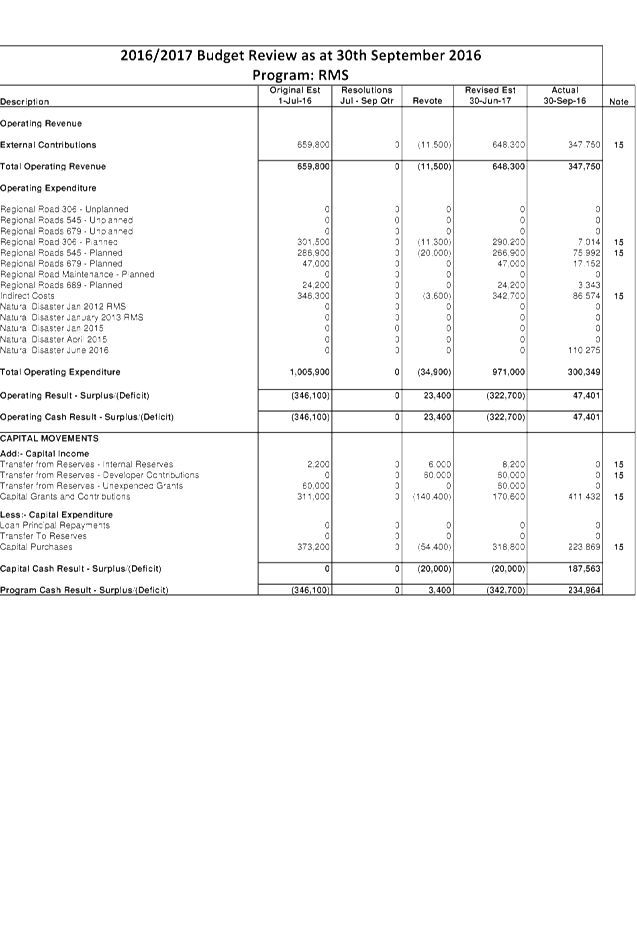

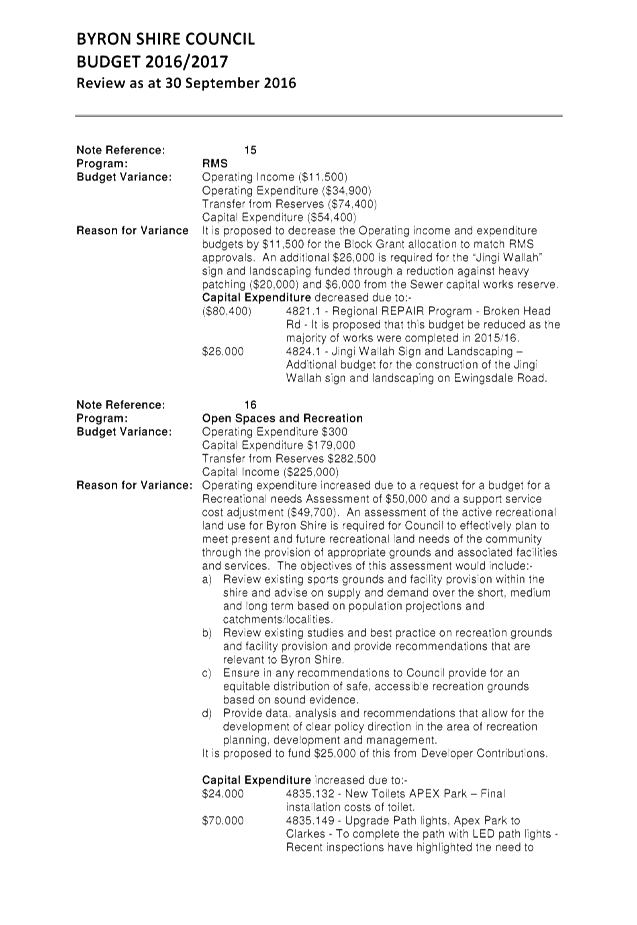

· In the Roads and

Maritime Services program (RMS) it is proposed to decrease operating income and

expenditure by $11,500 from the block grant to match RMS approvals. It is also

proposed to decrease capital expenditure by $54,400 due to the completion of

the Broken Head road works being under budget ($80,400) and additional works

for the creation and installation of the Jingi Wallah sign ($26,000).

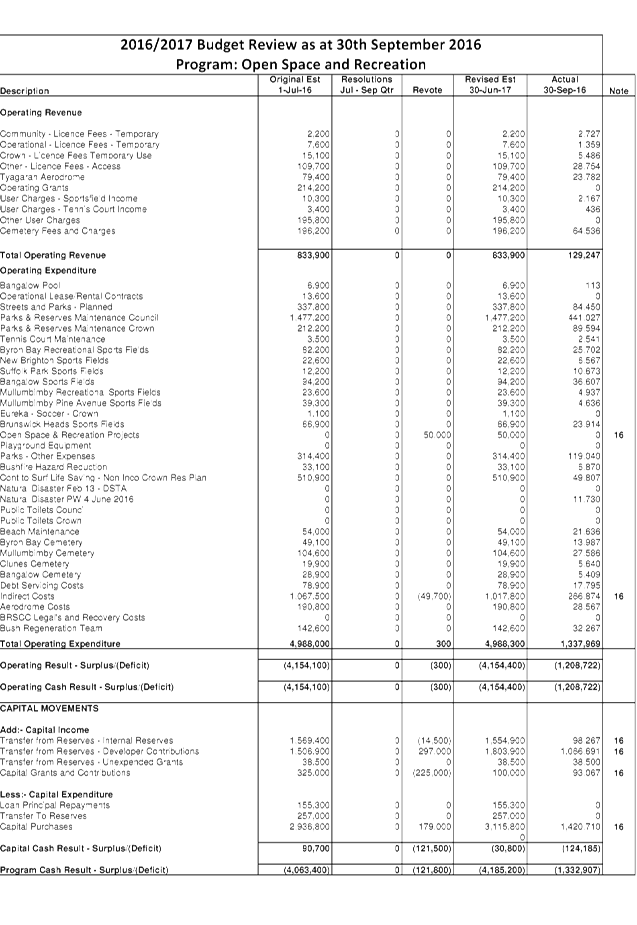

· In the Open Space

and Recreation program, operating expenditure increased by $300 due to a

request for a budget for a Recreational needs Assessment of $50,000 and a

support service cost adjustment ($49,700). An assessment of the active

recreational land use for Byron Shire is required for Council to effectively

plan to meet present and future recreational land needs of the community

through the provision of appropriate grounds and associated facilities and

services. There are a number of capital expenditure adjustments outlined

under Note 16 in the Budget Variations explanations section of Attachment

1. Further disclosure is included in the third page of Attachment 2 under

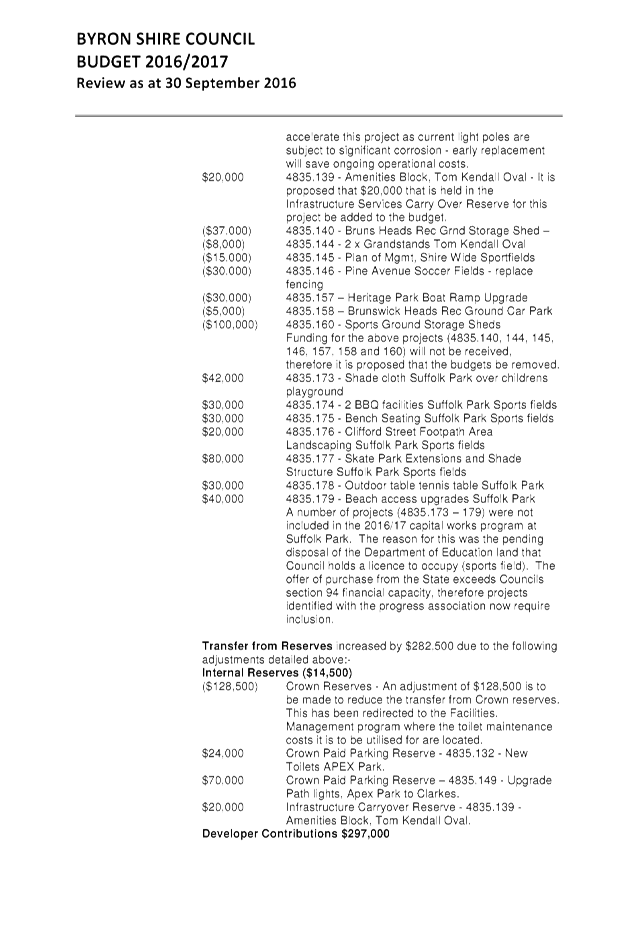

the budget program heading Open Space & Recreation.

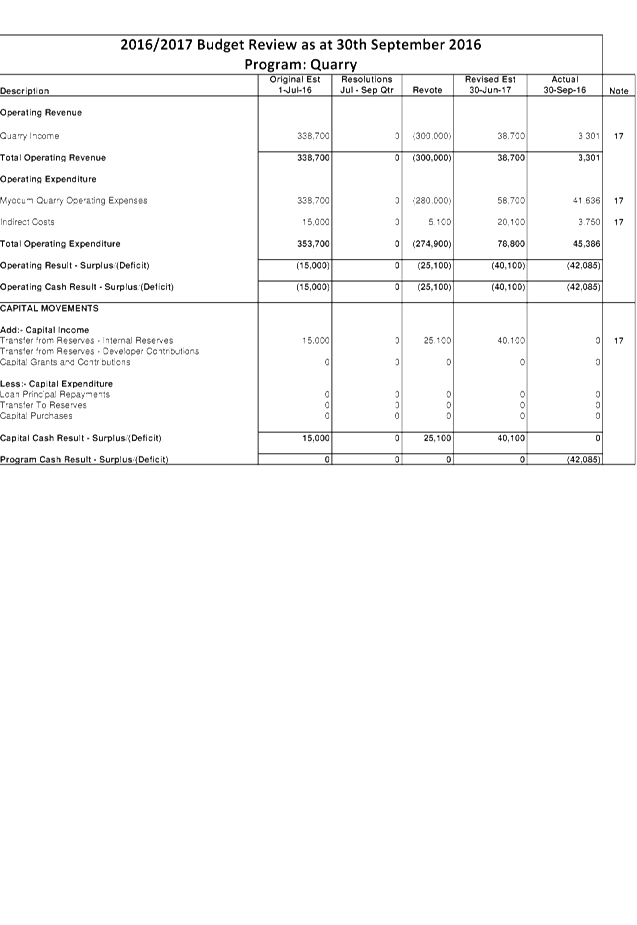

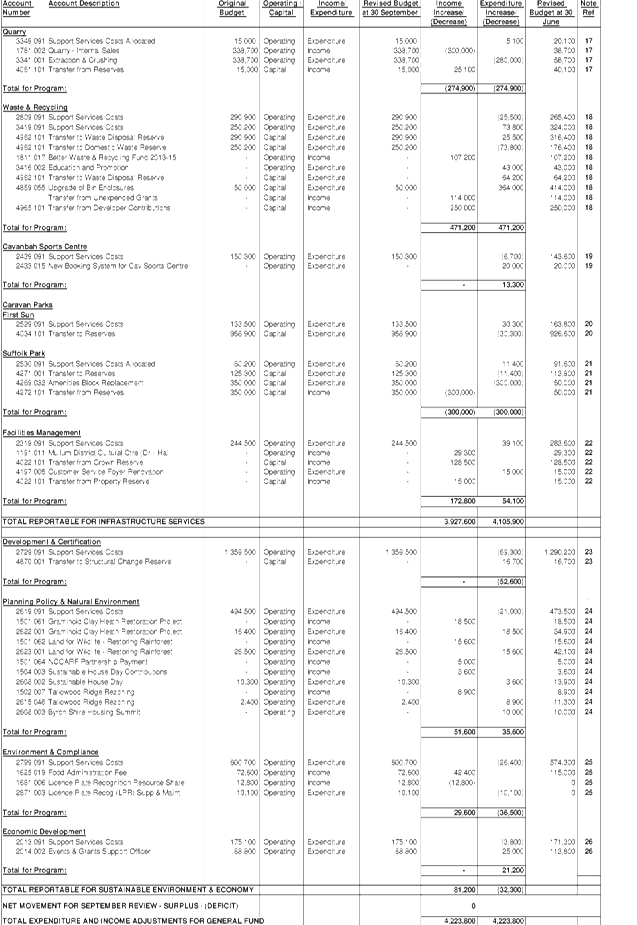

· In the Quarry

program it is proposed to reduce income and expenditure due to the inactivity

of the Quarry.

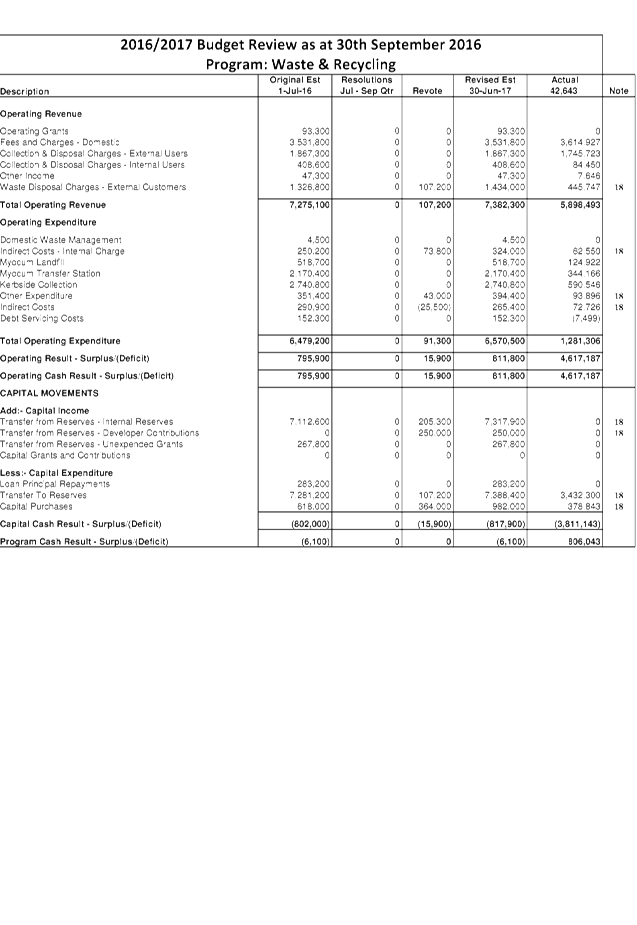

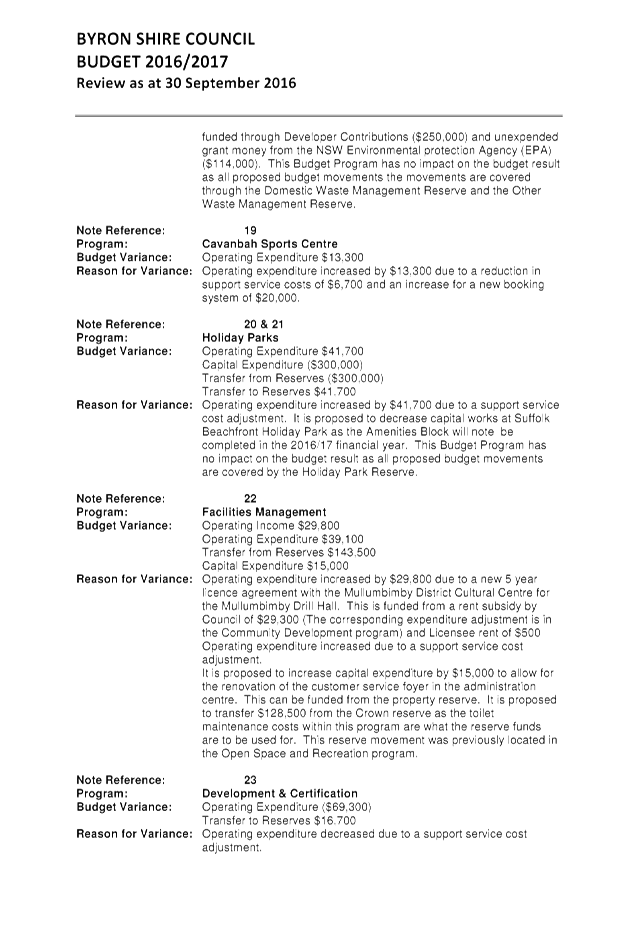

· In the Waste &

Recycling program It is proposed to increase operating income by $107,200 due

to the receipt of the Better Waste and Recycling grant. It is proposed to

increase operating expenditure by $43,000 for Promotion and Education Resource

Recovery and an Anti littering program at Byron Bay Foreshore in association

with the rollout of the new bin enclosure network. It is also proposed to

make a support service adjustment of $48,300. It is proposed to increase

capital expenditure by $364,000 for the replacement of all Byron Bay and

Brunswick Heads bin enclosures including the roll-out of 71 new public place

recycling enclosures and a trial of 1 public place organics recycling

enclosure. This is to be funded through Developer Contributions

($250,000) and unexpended grant money from the NSW Environmental protection

Agency (EPA) ($114,000).

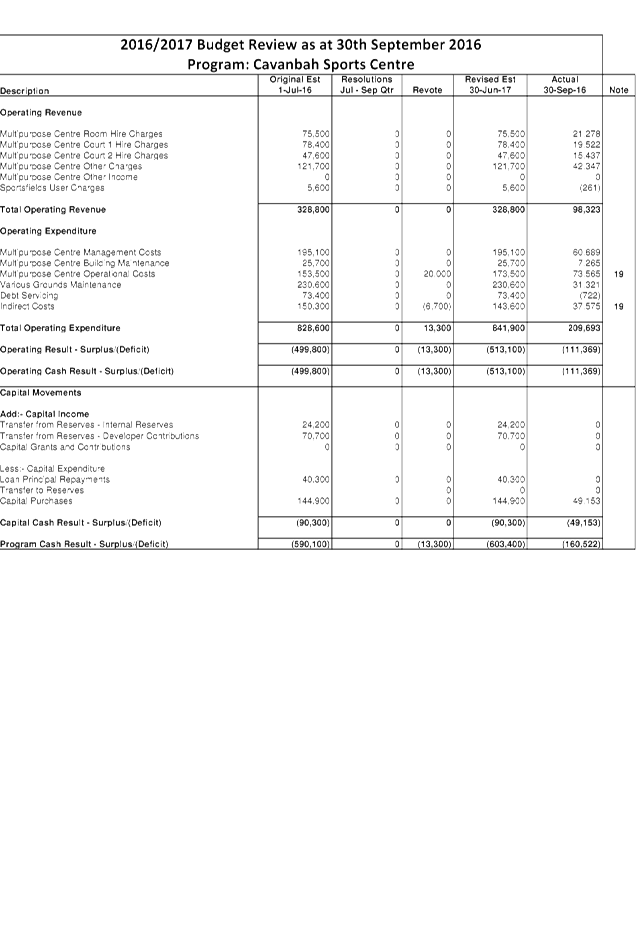

· In the Cavanbah

Centre program, it is proposed to increase expenditure to allow for the cost of

installing a new booking system ($20,000)

· In the Suffolk

Beachfront Holiday Park program, it is proposed to decrease the budget by

$300,000 for the replacement of the Amenities block. It is anticipated

that the majority of these works will now be carried out in the 2017/18

financial year.

· In the Facilities

Management program it is proposed to increase operating expenditure by $39,100

due to a support service cost adjustment and increase capital expenditure to

fund the administration centre foyer renovation ($15,000).

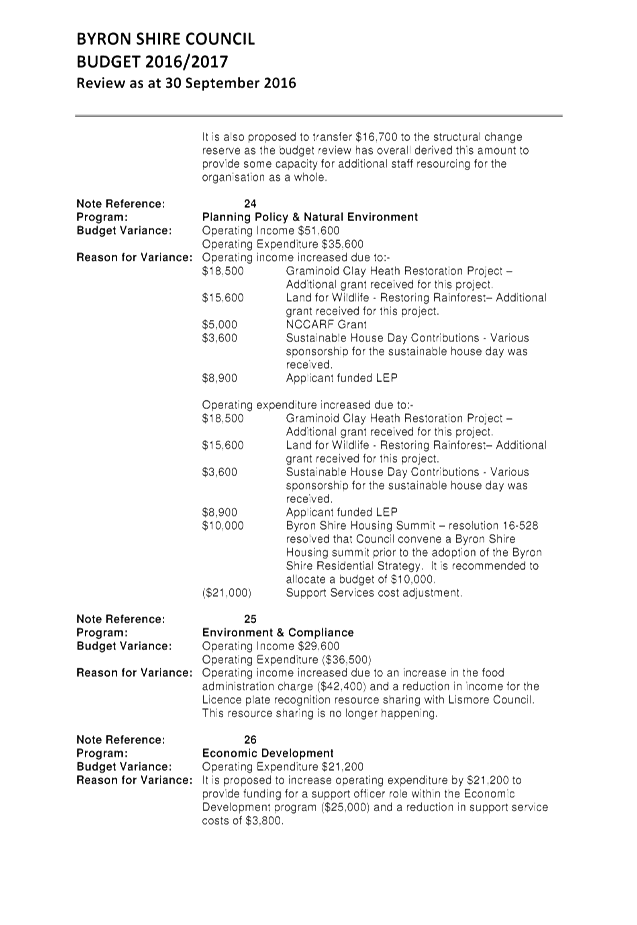

Sustainable Environment and Economy

· In the Planning Policy

and Natural Environment Program, It is proposed to adjust the budget to cater

for three new grants received (Graminoid Clay Heath Restoration $18,500, Land

for Wildlife $15,600 and NCCARF Partnership program $5,000), income received

from sponsorship at the sustainable house day ($3,600) and an applicant funded

LEP contribution ($8,900). It is proposed to increase expenditure by the

same grant monies and an additional $10,000 for the Byron Shire Housing Summit,

as outlined in Council resolution 16-528.

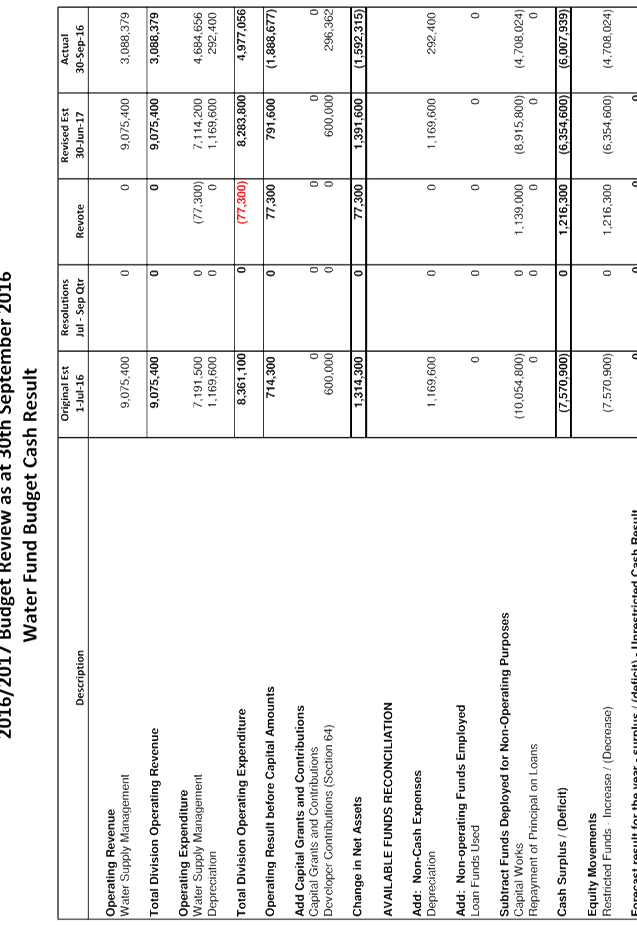

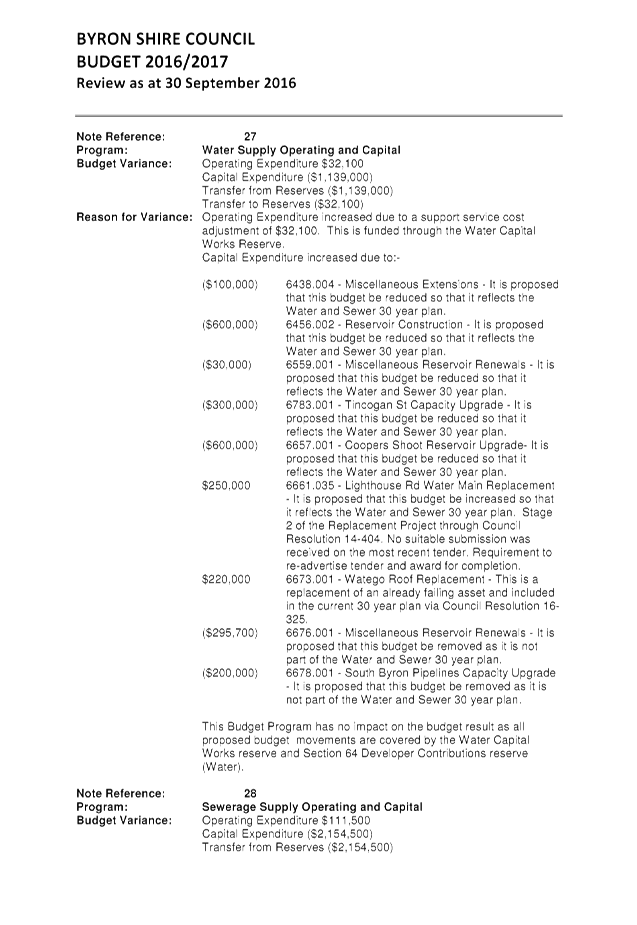

WATER FUND

After completion of the 2015/2016

Financial Statements the Water Fund as at 30 June 2016 has a capital works

reserve of $2,723,000 and held $10,549,100 in section 64 developer

contributions.

The estimated Water Fund reserve

balances as at 30 June 2017, and forecast in this Quarter Budget Review, are

derived as follows:

Capital Works Reserve

|

Opening Reserve Balance at 1

July 2016

|

$2,723,000

|

|

Plus original budget reserve

movement

|

1,553,000

|

|

Less reserve funded carryovers

from 2015/2016

|

(346,800)

|

|

Resolutions July -

September Quarter – increase / (decrease)

|

0

|

|

September Quarterly Review

Adjustments – increase / (decrease)

|

(53,700)

|

|

Forecast Reserve Movement for

2016/2017 – Increase / (Decrease)

|

1,152,500

|

|

Estimated Reserve Balance at

30 June 2017

|

$3,875,500

|

Section 64 Developer

Contributions

|

Opening Reserve Balance at 1

July 2016

|

$10,549,100

|

|

Plus original budget reserve

movement

|

(7,794,000)

|

|

Less reserve funded carryovers

from 2015/2016

|

(383,100)

|

|

Resolutions July -

September Quarter – increase / (decrease)

|

0

|

|

September Quarterly Review

Adjustments – increase / (decrease)

|

1,270,000

|

|

Forecast Reserve Movement for

2016/2017 – Increase / (Decrease)

|

(6,907,100)

|

|

Estimated Reserve Balance at

30 June 2017

|

$3,642,000

|

Movements for Water Fund can be seen in Attachment 1 with a

proposed estimated increase to reserves (including S64 Contributions) overall

of $1,216,300 from the 30 September 2016 Quarter Budget Review.

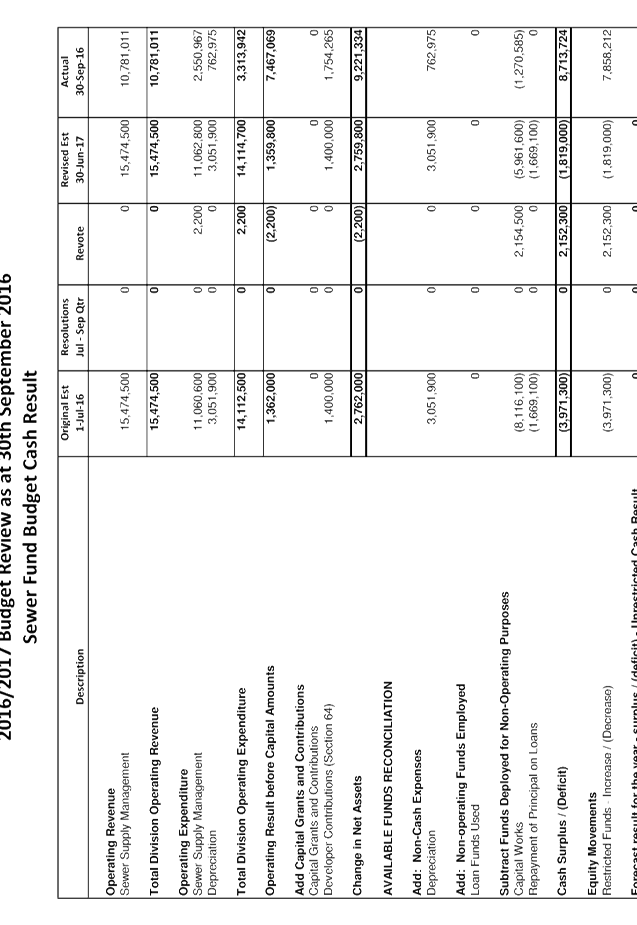

SEWERAGE FUND

After completion of the 2015/2016

Financial Statements the Sewerage Fund held a capital works reserve of

$5,153,600 and a plant reserve of $827,800. It also held $8,760,300 in section

64 developer contributions.

Capital Works Reserve

|

Opening Reserve Balance at 1

July 2017

|

$5,153,600

|

|

Plus original budget reserve

movement

|

814,200

|

|

Less reserve funded carryovers

from 2015/2016

|

(96,900)

|

|

Resolutions July -

September Quarter – increase / (decrease)

|

0

|

|

September Quarterly Review

Adjustments – increase / (decrease)

|

1,071,600

|

|

Forecast Reserve Movement for

2016/2017 – Increase / (Decrease)

|

1,788,900

|

|

Estimated Reserve Balance at

30 June 2017

|

$6,942,500

|

Plant Reserve

|

Opening Reserve Balance at 1

July 2016

|

$827,800

|

|

Plus original budget reserve

movement

|

0

|

|

Less reserve funded carryovers

from 2015/2016

|

0

|

|

Resolutions July -

September Quarter – increase / (decrease)

|

0

|

|

September Quarterly Review

Adjustments – increase / (decrease)

|

0

|

|

Forecast Reserve Movement for

2016/2017 – Increase / (Decrease)

|

0

|

|

Estimated Reserve Balance at

30 June 2017

|

$827,800

|

Section 64 Developer

Contributions

|

Opening Reserve Balance at 1

July 2016

|

$8,760,300

|

|

Plus original budget reserve

movement

|

(2,785,400)

|

|

Less reserve funded carryovers

from 2015/2016

|

(503,200)

|

|

Resolutions July -

September Quarter – increase / (decrease)

|

0

|

|

September Quarterly Review

Adjustments – increase / (decrease)

|

1,074,700

|

|

Forecast Reserve Movement for

2016/2017 – Increase / (Decrease)

|

(2,213,900)

|

|

Estimated Reserve Balance at

30 June 2017

|

$6,546,400

|

Movements for the Sewerage Fund can be seen in Attachment 1

with a proposed estimated overall increase to reserves (including S64

Contributions) of $2,146,300 from the 30 September 2016 Quarter Budget Review.

Legal Expenses

One of the major financial concerns for Council over

previous years has been legal expenses. Not only does this item represent a

large expenditure item funded by general revenue, but can also be susceptible

to large fluctuations.

The table that follows indicates the allocated budget and

actual legal expenditure within Council on

a fund basis as at 30 September 2016.

Total Legal Income & Expenditure as at 30 September

2016

|

Program

|

2016/2017

Budget ($)

|

Actual ($)

|

Percentage To

Revised Budget

|

|

Income

|

|

|

|

|

Legal Expenses Recovered

|

0

|

0

|

0%

|

|

Total Income

|

0

|

0

|

0%

|

|

|

|

|

|

|

Expenditure

|

|

|

|

|

General Legal Expenses

|

200,000

|

7,681

|

3.8%

|

|

Total Expenditure General Fund

|

200,000

|

7,681

|

3.8%

|

Note: The above table does not include costs incurred

by Council in proceedings after 30 September 2016 or billed after this date.

Financial Implications

The 30 September 2016 Quarter Budget Review of the 2016/2017

Budget has not changed the overall budget result. As a result there is no

expected change to the estimated unrestricted cash balance attributable to the

General Fund, with this remaining an estimated $1,182,800 at 30 June 2017.

Statutory and Policy

Compliance Implications

In accordance with Regulation 203

of the Local Government (General) Regulation 2005 the Responsible Accounting

Officer of a Council must:-

(1) Not later than 2 months after the end of each quarter

(except the June quarter), the responsible accounting officer of a council must prepare and submit to the council a budget review statement that shows, by

reference to the estimate of income and expenditure set out in the statement of

the council’s revenue policy included in the operational plan for the

relevant year, a revised estimate of the income and expenditure for that year.

(2) A budget review statement must include or be

accompanied by:

(a) a report as to whether or not the responsible

accounting officer believes that the statement indicates that the financial

position of the council is satisfactory, having regard to the original estimate

of income and expenditure, and

(b) if that position is unsatisfactory, recommendations

for remedial action.

(3) A budget review statement must also include any

information required by the Code to be included in such a statement.

Statement by Responsible Accounting Officer

This report indicates that the short term financial position

of the Council is satisfactory for the 2016/2017 financial year, having

consideration of the original estimate of income and expenditure at the 30

September 2016 Quarter Budget Review.

This opinion is based on the estimated General Fund

Unrestricted Cash Result position and that the current indicative budget

position for 2016/2017 is maintained in this Budget Review.

Notwithstanding this, Council will need to continue to carefully monitor the

2016/2017 budget over the remainder of the financial year.

Staff Reports - Corporate and Community Services 4.3 - Attachment 1

Staff Reports - Corporate and Community Services 4.3 - Attachment 2

Staff Reports - Corporate and Community Services 4.3 - Attachment 3

Staff Reports - Corporate and Community Services 4.4

Report No. 4.4 Financial

Sustainability Plan 2016/2017

Directorate: Corporate

and Community Services

Report

Author: Mark

Arnold, Director Corporate and Community Services

File No: I2016/1121

Theme: Corporate Management

Financial Services

Summary:

Council at its Ordinary meeting held on 9 May

2013 adopted a Financial Sustainability Plan (“FSP”) for the

2013/2014 financial period (refer Resolution 13-238).

This was the initial FSP developed and adopted

by Council, and was prepared in accordance with part 3 of Council Resolution

13-148, to provide a strategic approach to the management of the Financial

Sustainability of Council.

Resolution 13-148, adopted by the

Strategic Planning Committee Resolution at its meeting held on 28 March 2013,

provided the framework for the development the FSP.

The FSP provides a means for Council to

communicate with the community on proposed reforms and actions to manage the financial sustainability of the organisation in the

short, medium and long term.

This report has been prepared to allow the Finance Advisory

Committee to consider the fourth version of the Financial

Sustainability Plan for the 2016/2017 financial period.

A copy of the draft Financial

Sustainability Plan 2016/17 will be distributed to Committee Members prior to

the meeting.

|

RECOMMENDATION:

That the Finance Advisory

Committee recommend to Council:

That Council adopt the Draft Financial Sustainability

Plan 2016/2017 (#E2016/26998).

|

Report

This report has been prepared to allow the Finance Advisory

Committee to consider the draft “Financial

Sustainability Plan 2016/2017” (“FSP 2016/2017”).

The FSP 2016/2017 is the fourth version of

the FSP prepared for consideration by Council.

The first version of the FSP, FSP 2013/2014

was adopted by Council on 9 May 2013 via Resolution 13-238.

The second version of the FSP, FSP

2014/2015 was adopted by Council on 7 August 2014 via Resolution 14-326.

The third version of the FSP, FSP 2015/2016

was adopted by Council on 15 December 2015 via Resolution 15-606.

During the course of the 2015/2016

financial year, work on the implementation of the actions detailed in the

individual chapters of the 2015/2016 FSP was undertaken, with the outcomes

progressively reported to the Finance Advisory Committee on a quarterly basis

on 18 February 2016 and 12 May 2016, with the final report for the 2015/2016

financial year submitted to the FAC meeting held 18 August 2016.

The FSP 2016/2017 has been developed using

a similar format to that of FSP 2015/2016 but has been amended to reflect the

actions undertaken and the impact of the outcomes from these actions on the

future strategic management of Council’s financial sustainability.

The relevant chapters in the FSP 2016/2017

have been prepared to capture the outcomes from the 2015/2016 financial year as

well detail what is proposed for the 2016/2017 financial year.

The Action Plan is a summary of the actions

detailed in the FSPP for the following chapter areas:

· Expenditure

Review

· Revenue

Review

· Land Review

and Property Development

· Strategic

Procurement

· Policy and

Decision Making

· Potential

Commercial Opportunities

· Volunteerism

· Collaborations

and Partnerships

· Asset

Management

· Long Term

Financial Planning

· Performance

Indicators

· Environmental

Projects

The Action Plan will be completed and included in the

2016/2017 FSP when adopted by Council and will be developed from the Actions

included in each Chapter. The Action Plan will then be reported to the FAC each

quarter starting with the December quarter.

A copy of the draft “Financial

Sustainability Plan 2016/2017” will be distributed to Committee

Members prior to the meeting.

Financial Implications

The draft “Financial

Sustainability Plan 2016/2017” forms part of the strategic approach

adopted by Council in managing the short, medium long term sustainability of

Council. The Plan needs to be considered in context with the adopted annual Operational

Plan, the Quarterly Budget Reviews and the Long Term Financial Plan when

Council is considering the financial impacts of specific activities, projects

and Services.

Part 2 of Resolution 13-148 requires

the General Manager to prepare reports on specific elements of sustainability reform package detailed in the FSP, including any rationalisation

of Council's property portfolio and the associated establishment of an

Infrastructure Renewal Fund. The Infrastructure Renewal Fund was established by

Council by Resolution 13-170 and the terms of operation for this Reserve

were adopted by Council on 9 May 2013 via Resolution 13-239.

In accordance with Part 4 of Resolution 13-148

the General Manager will continue to prepare and submit progress reports on the

implementation of the draft “Financial

Sustainability Plan 2016/2017” to the Council's Finance Committee on

a quarterly basis.

Statutory and Policy Compliance Implications

The FSP has been developed as a tool to assist Council in

its ongoing obligations as defined in Chapter 3 (Principles for local

government) of the Local Government Act 1993.

Section 8A of the Local Government 1993 provides that

Council as part of its Guiding Principles consider the following:

(1) Exercise of functions

generally

The following general principles apply to the exercise of functions by

councils:

(a) Councils should

provide strong and effective representation, leadership, planning and

decision-making.

(b) Councils should

carry out functions in a way that provides the best possible value for

residents and ratepayers.

(c) Councils should

plan strategically, using the integrated planning and reporting framework, for

the provision of effective and efficient services and regulation to meet the

diverse needs of the local community.

(d) Councils should

apply the integrated planning and reporting framework in carrying out their

functions so as to achieve desired outcomes and continuous improvements.

(e) Councils should

work co-operatively with other councils and the State government to achieve

desired outcomes for the local community.

(f) Councils should

manage lands and other assets so that current and future local community needs

can be met in an affordable way.

(g) Councils should

work with others to secure appropriate services for local community needs.

(h) Councils should act

fairly, ethically and without bias in the interests of the local community.

(i) Councils should be

responsible employers and provide a consultative and supportive working

environment for staff.

(2) Decision-making

The following principles apply to decision-making by councils (subject to any

other applicable law):

(a) Councils should

recognise diverse local community needs and interests.

(b) Councils should

consider social justice principles.

(c) Councils should

consider the long term and cumulative effects of actions on future generations.

(d) Councils should

consider the principles of ecologically sustainable development.

(e) Council

decision-making should be transparent and decision-makers are to be accountable

for decisions and omissions.

(3) Community participation

Councils should actively engage with their local communities, through the use

of the integrated planning and reporting framework and other measures.