What is a “Conflict of Interests” - A conflict of

interests can be of two types:

Pecuniary - an interest that a person has in a matter because of a reasonable

likelihood or expectation of appreciable financial gain or loss to the person

or another person with whom the person is associated.

Non-pecuniary – a private or personal interest that a Council

official has that does not amount to a pecuniary interest as defined in the

Local Government Act (eg. A friendship, membership of an association, society

or trade union or involvement or interest in an activity and may include an

interest of a financial nature).

Remoteness – a person does not have a pecuniary interest in a matter

if the interest is so remote or insignificant that it could not reasonably be

regarded as likely to influence any decision the person might make in relation

to a matter or if the interest is of a kind specified in Section 448 of the

Local Government Act.

Who has a Pecuniary Interest? - a person has a pecuniary interest in a

matter if the pecuniary interest is the interest of the person, or another

person with whom the person is associated (see below).

Relatives, Partners - a person is taken to have a pecuniary interest in a

matter if:

§ The person’s

spouse or de facto partner or a relative of the person has a pecuniary interest

in the matter, or

§ The person, or a

nominee, partners or employer of the person, is a member of a company or other

body that has a pecuniary interest in the matter.

N.B. “Relative”, in relation to a person means any of the

following:

(a) the

parent, grandparent, brother, sister, uncle, aunt, nephew, niece, lineal

descends or adopted child of the person or of the person’s spouse;

(b) the

spouse or de facto partners of the person or of a person referred to in

paragraph (a)

No Interest in the Matter - however, a person is not taken to have a

pecuniary interest in a matter:

§ If the person is

unaware of the relevant pecuniary interest of the spouse, de facto partner,

relative or company or other body, or

§ Just because the

person is a member of, or is employed by, the Council.

§ Just because the

person is a member of, or a delegate of the Council to, a company or other body

that has a pecuniary interest in the matter provided that the person has no

beneficial interest in any shares of the company or body.

Disclosure and participation in meetings

§ A Councillor or a

member of a Council Committee who has a pecuniary interest in any matter with

which the Council is concerned and who is present at a meeting of the Council

or Committee at which the matter is being considered must disclose the nature

of the interest to the meeting as soon as practicable.

§ The Councillor or

member must not be present at, or in sight of, the meeting of the Council or

Committee:

(a) at any

time during which the matter is being considered or discussed by the Council or

Committee, or

(b) at any

time during which the Council or Committee is voting on any question in

relation to the matter.

No Knowledge - a person does not breach this Clause if the person did

not know and could not reasonably be expected to have known that the matter

under consideration at the meeting was a matter in which he or she had a

pecuniary interest.

Participation in Meetings Despite Pecuniary Interest (S 452 Act)

A Councillor is not prevented from taking part in the consideration or

discussion of, or from voting on, any of the matters/questions detailed in

Section 452 of the Local Government Act.

Non-pecuniary Interests - Must be disclosed in meetings.

There are a broad range of options available for managing conflicts &

the option chosen will depend on an assessment of the circumstances of the

matter, the nature of the interest and the significance of the issue being

dealt with. Non-pecuniary conflicts of interests must be dealt with in at

least one of the following ways:

§ It may be appropriate

that no action be taken where the potential for conflict is minimal.

However, Councillors should consider providing an explanation of why they

consider a conflict does not exist.

§ Limit involvement if

practical (eg. Participate in discussion but not in decision making or

vice-versa). Care needs to be taken when exercising this option.

§ Remove the source of

the conflict (eg. Relinquishing or divesting the personal interest that creates

the conflict)

§ Have no involvement by

absenting yourself from and not taking part in any debate or voting on the

issue as if the provisions in S451 of the Local Government Act apply

(particularly if you have a significant non-pecuniary interest)

RECORDING OF VOTING ON PLANNING MATTERS

Clause 375A of the Local Government Act 1993

– Recording of voting on planning matters

(1) In this section, planning

decision means a decision made in the exercise of a function of a council

under the Environmental Planning and Assessment Act 1979:

(a) including a decision

relating to a development application, an environmental planning instrument, a

development control plan or a development contribution plan under that Act, but

(b) not including the making of

an order under Division 2A of Part 6 of that Act.

(2) The general manager is

required to keep a register containing, for each planning decision made at a

meeting of the council or a council committee, the names of the councillors who

supported the decision and the names of any councillors who opposed (or are

taken to have opposed) the decision.

(3) For the purpose of

maintaining the register, a division is required to be called whenever a motion

for a planning decision is put at a meeting of the council or a council committee.

(4) Each decision recorded in

the register is to be described in the register or identified in a manner that

enables the description to be obtained from another publicly available

document, and is to include the information required by the regulations.

(5) This section extends to a

meeting that is closed to the public.

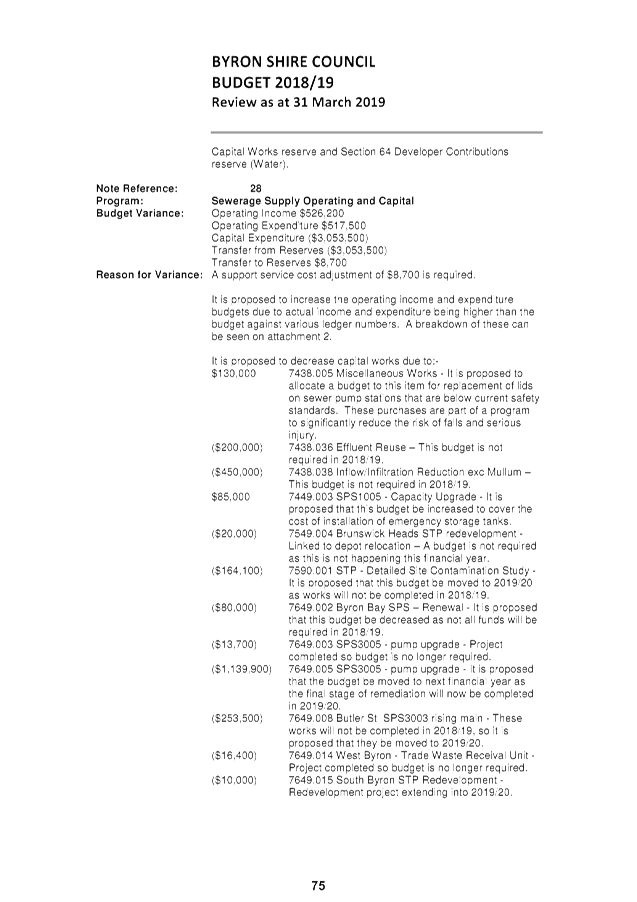

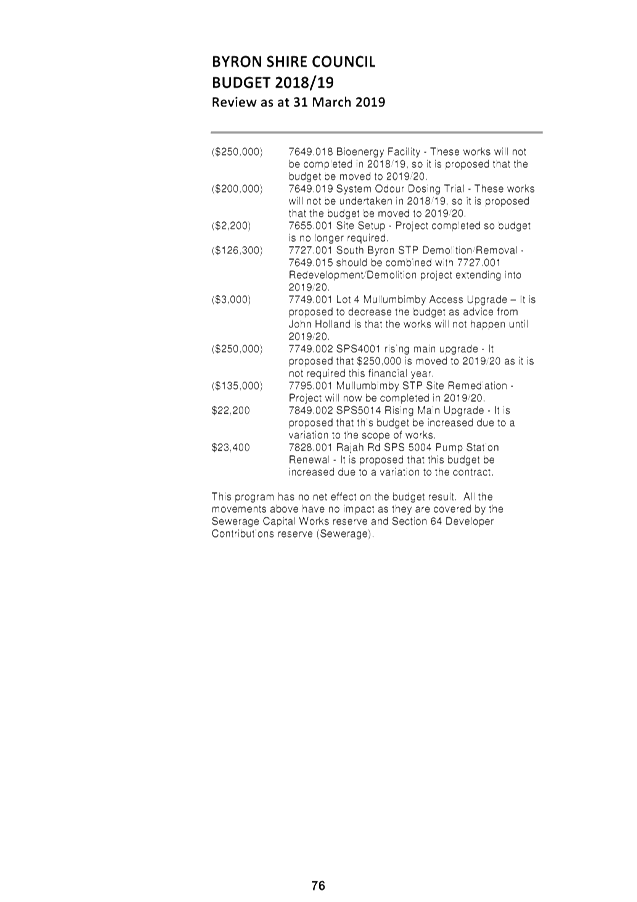

Staff Reports - Corporate and Community Services 4.1

Staff Reports - Corporate and Community

Services

Report No. 4.1 Quarterly

Update - Implementation of Special Rate Variation

Directorate: Corporate

and Community Services

Report

Author: James

Brickley, Manager Finance

File No: I2019/672

Summary:

At

its Ordinary Meeting held on 2 February 2017 Council resolved to apply for a

Special Rate Variation (SRV) of 7.50% per annum for four years commencing from

the 2017/2018 financial year (Resolution 17-020 part 5).

Following

approval of Council’s SRV by the Independent Pricing and Regulatory

Tribunal (IPART) received on 9 May 2017, Council resolved to implement the SRV

at its Ordinary Meeting held 22 June 2017 (Resolution 17-268 part 1).

At

the same Ordinary Meeting Council resolved (Resolution 17-222 part 2) to

incorporate reporting on the Special Rate Variation into the development of the

2017/2018 Financial Sustainability Plan and quarterly updates to Council

through the Finance Advisory Committee on the implementation of the adopted

Financial Sustainability Plan. Whilst Council is no longer developing an annual

Financial Sustainability Plan (from 2018/2019 onwards), it is important to

provide progressive reporting on the implementation of the SRV.

The

purpose of this report is to provide the Finance Advisory Committee with a

quarterly update on implementation of the SRV and expenditure up to 31 March

2019.

|

RECOMMENDATION:

That the Finance Advisory Committee notes the quarterly

update on the Special Rate Variation Implementation as at 31 March 2019.

|

Attachments:

1 2018-19

Special Rate Management Report as at 31 March 2019 reported to Finance Advisory

Committee 9/5/2019, E2019/30628 , page 8⇩

REPORT

At

its Ordinary Meeting held on 2 February 2017 Council resolved to apply for a

Special Rate Variation (SRV) as follows:

Resolution 17-020 part 5:

Lodge a

Section 508A permanent Special Rate Variation application to the Independent

Pricing and Regulatory Tribunal, for increases to the ordinary rate income

(general revenue) of 7.5% (including rate peg) in 2017/18, 7.5% (including rate

peg) in 2018/19, 7.5% (including rate peg) in 2019/20 and 7.5% (including rate

peg) in 2020/21.

After lodging the Special Rate

Variation application with the Independent Pricing and Regulatory Tribunal

(IPART), Council received approval to increase its ordinary rate income as per

resolution 17-020. This approval was granted on 9 May 2017.

Council resolved to implement the SRV through adoption of the 2017/2018

Operational Plan and Revenue Policy at its Ordinary Meeting held on 22 June

2017 (Resolution 17-268 part 1).

At its Ordinary Meeting held on 22

June 2017 Council received Report 13.13 confirming the outcome of the SRV

application and its subsequent approval. Council resolved resolution 17-222

as follows:

1. That

Council note the determination from IPART in relation to its 2017/2018

Special Rate Application including the following conditions imposed by IPART on

Council for the:-

a) use

of the additional income derived from the special variation for the purposes of

reducing its infrastructure backlog and improving financial sustainability;

and

b)

reporting on this use against the forecasts included in the Council’s

application as part the Council’s annual report for each year from

2017-18 to 2026-27.

2. That

Council adopt as a Policy Framework the use and reporting conditions imposed by

IPART in the SRV determination and further incorporate reporting on the Special

Rate Variation into the development of the 2017/2018 Financial Sustainability

Plan and the quarterly updates to Council through the Finance Advisory

Committee on the implementation of the adopted Financial Sustainability Plan.

3. That

Council establish as a policy framework that funding for infrastructure renewal

and maintenance from general revenue sources is not ever lower then the general

revenue baseline indicator established in the 2016/2017 Budget.

4.That

Council establish as a policy framework that any funds generated by the SRV

that remain unexpended at the end of each financial year are to be restricted

and held in a internal reserve, to be carried forward to subsequent financial

year, for expenditure in accordance with the uses imposed in the SRV approval.

5. That

Council incorporate the research of potential non resident revenue sources (if

any) as part of the Revenue Review chapter in the development of the 2017/2018

Financial Sustainability Plan, and provide quarterly updates to Council through

the Finance Advisory Committee.

6.

That Council not proceed with the implementation of part 9 and part 11

of resolution 17-020.

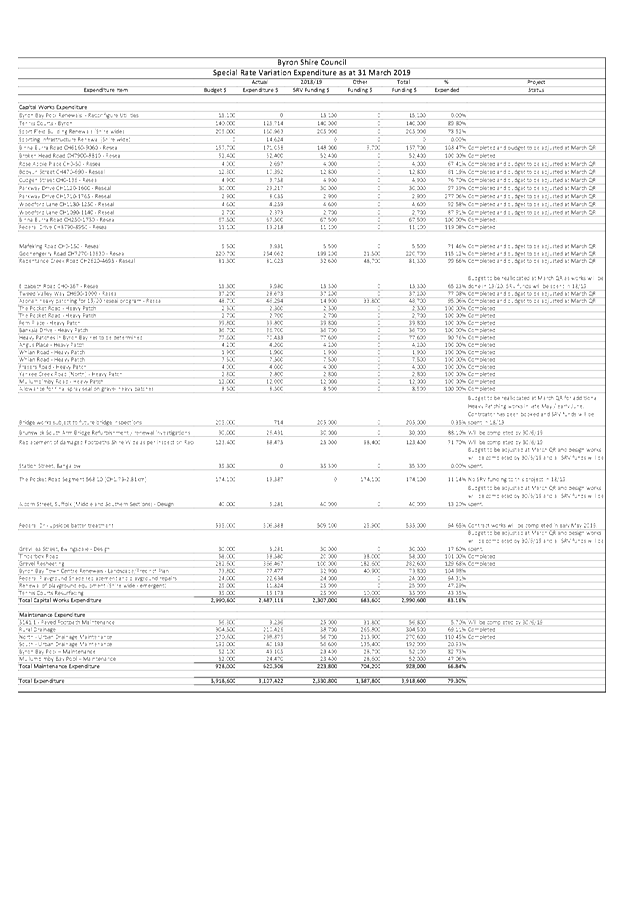

This report is provided to the

Finance Advisory Committee to advise on the implementation of the SRV and the

current status of expenditure from 1 July 2018 to 31 March 2019 which is

detailed in Attachment 1, being the second year of the SRV.

The levy of Council’s annual

rates and charges was completed in accordance with Resolution 18-429

prior to 31 July 2018 and this included applying the second tranche of the 7.5%

ordinary rate increase for 2018/2019, continuing the revised ordinary rating

structure adopted by Council for 2017/2018.

The yield from the SRV for

2017/2018, being the first year of the increase, is $1,185,000 with the yield

from the SRV for 2018/2019, the second year of the increase, estimated at

$2,276,400.

Upon adoption of the 2018/2019

Budget Estimates, Council resolved to undertake the program of capital and

maintenance works, including the additional SRV revenue and other funding,

outlined in Attachment 1. During the course of the 2018/2019 financial

year, there may be adjustments required to the expenditure budgets identified

in the schedule of capital and maintenance works currently funded by the SRV

revenue which will be presented to Council for approval via the Quarterly

Budget Review process.

The expenditure program adopted for

the 2018/2019 financial year is consistent with Council’s SRV application

and approval from IPART to use the funding to improve financial sustainability

and reduce infrastructure backlog.

STRATEGIC CONSIDERATIONS

Community Strategic Plan and Operational Plan

|

CSP Objective

|

L2

|

CSP Strategy

|

L3

|

DP Action

|

L4

|

OP Activity

|

|

Community

Objective 5: We have community led decision making which is open and

inclusive

|

5.2

|

Create a

culture of trust with the community by being open, genuine and transparent

|

5.2.1

|

Provide timely,

accessible and accurate information to the community

|

5.2.1.3

|

Report on

progress of Delivery Program actions

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Legal/Statutory/Policy Considerations

Approval and conditions received from the

Independent Pricing and Regulatory Tribunal (IPART) regarding the Byron Shire

Council Special Rate Application 2017-2018 received 9 May 2017.

Council Resolution 17-268, 18-429 and 17-222.

Financial

Considerations

There

are no direct financial implications associated with this report. The table

included at Attachment 1 provides information to the Finance Advisory Committee

as to the expenditure of the Special Rate Variation Funds up to the end of the

third quarter of the 2018/2019 financial year.

The

total 2017/2018 SRV Allocation for 2018/2019 as indicated in Attachment 1 is

$2,530,800. Whilst the 2018/2019 SRV levy is $2,276,400, the difference

of $254,400 is unexpended funds from 2017/2018 that have been carried forward

to the current financial year.

Consultation

and Engagement

Prior

to the approval of the SRV, Council undertook extensive community consultation.

This report also provides an opportunity for the community to receive a

quarterly update on the implementation of the SRV for the current financial

year. Final outcomes for the 2018/2019 financial year will also be published in

Council’s Annual Report in accordance with the approval conditions set by

IPART.

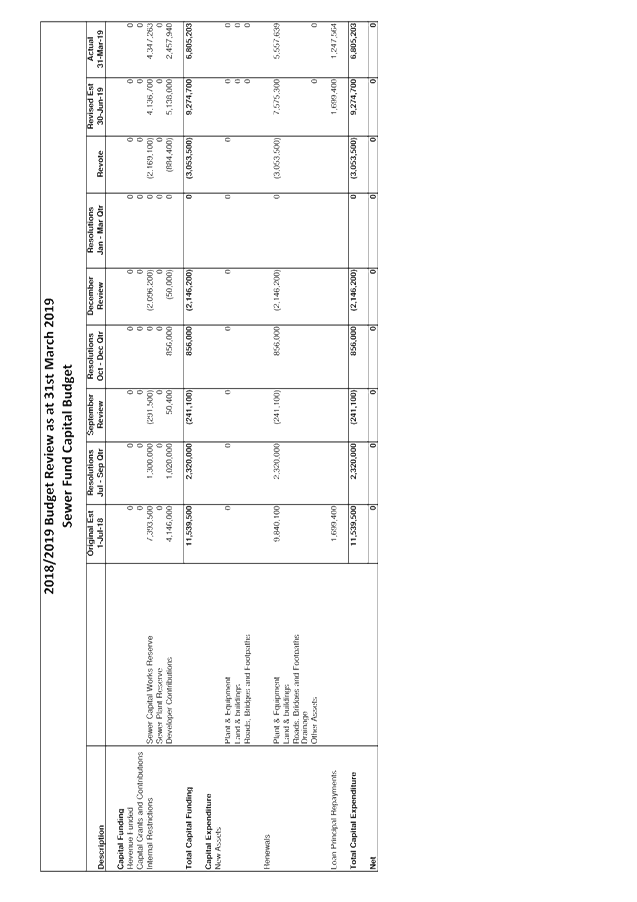

Staff Reports - Corporate and Community Services 4.2

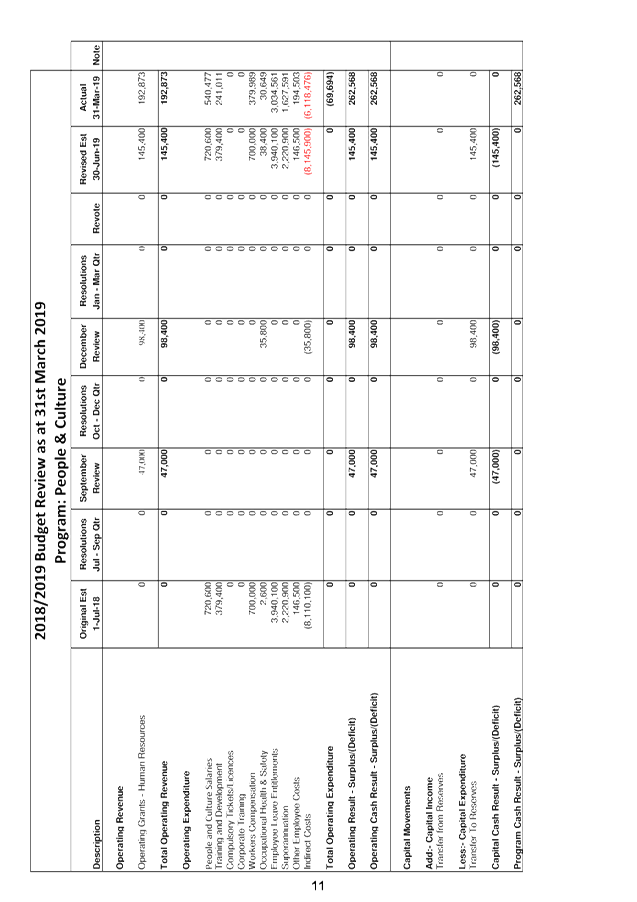

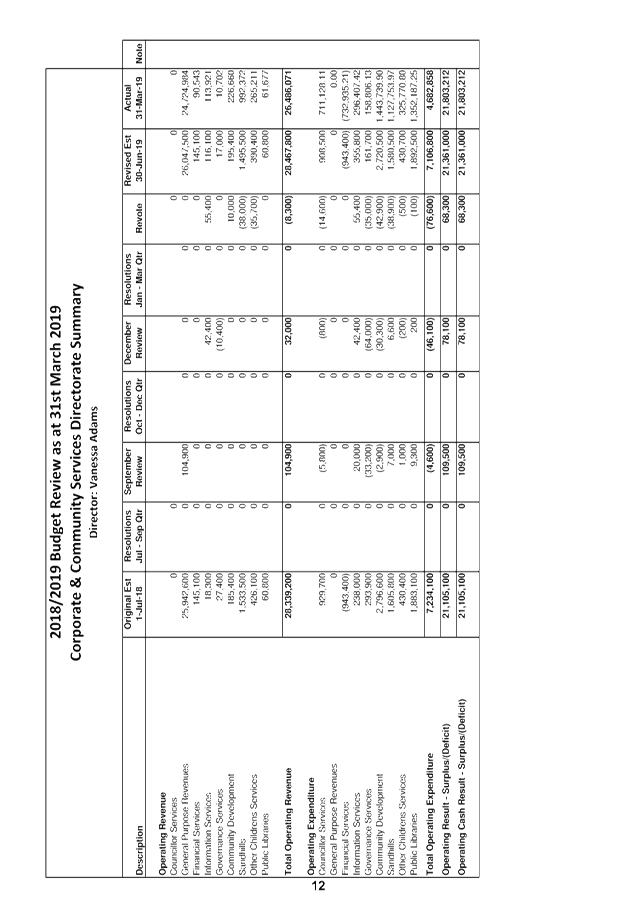

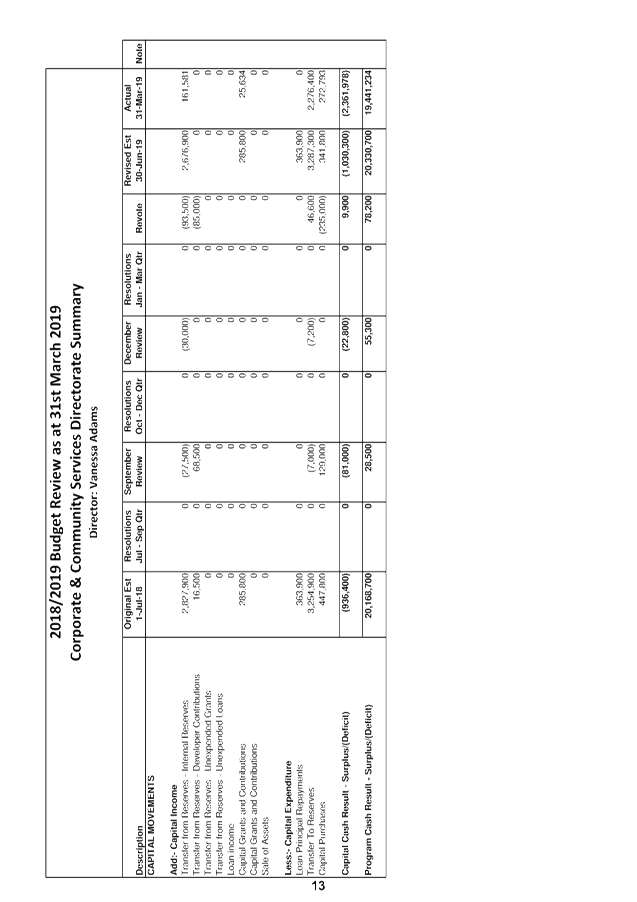

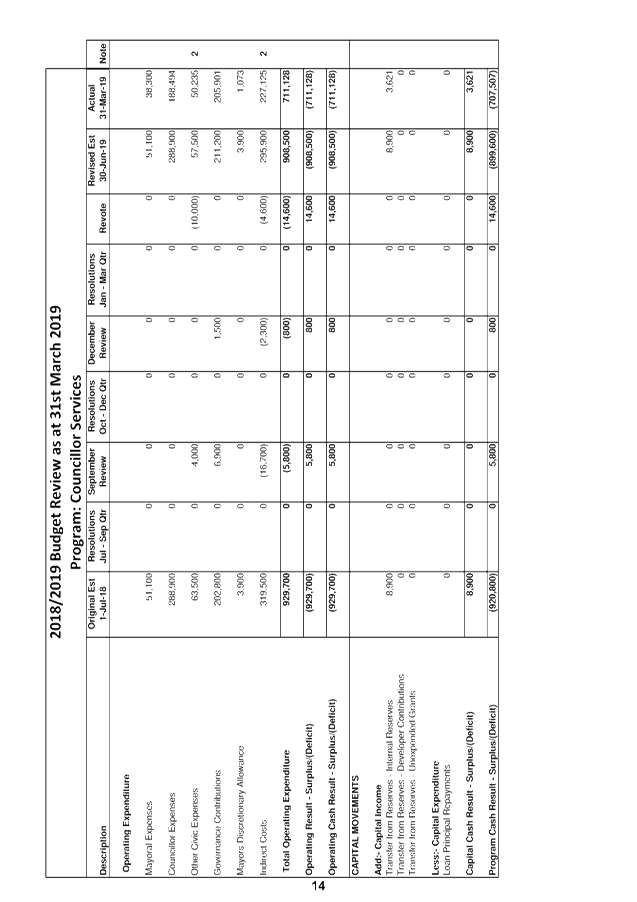

Report No. 4.2 Budget

Review - 1 January 2019 to 31 March 2019

Directorate: Corporate

and Community Services

Report

Author: James

Brickley, Manager Finance

File No: I2019/682

Summary:

This report is prepared to comply with Regulation 203 of the

Local Government (General) Regulation 2005 and to inform Council and the

community of Council’s estimated financial position for the 2018/2019

financial year, reviewed as at 31 March 2019.

This report contains an overview of the proposed budget

variations for the General Fund, Water Fund and Sewerage Fund. The specific

details of these proposed variations are included in Attachment 1 and 2 for

Council’s consideration and authorisation.

Attachment 3 contains the Integrated Planning and Reporting

Framework (IP&R) Quarterly Budget Review Statement (QBRS) as outlined by

the Office of Local Government in circular 10-32.

|

RECOMMENDATION:

That the Finance Advisory

Committee recommends to Council:

1. That

Council authorises the itemised budget variations as shown in Attachment 2 (#E2019/31364)

which include the following results in the 31 March 2019 Quarterly Review of

the 2018/2019 Budget:

a) General

Fund – $0 change to the Estimated Unrestricted Cash Result

b) General

Fund - $5,141,900 increase in reserves

c) Water

Fund - $3,003,000 increase in reserves

d) Sewerage

Fund - $3,062,200 increase in reserves

2. That

Council adopts the revised General Fund Estimated Unrestricted Cash Result of

$1,145,200 for the 2018/2019 financial year as at 31 March 2019.

|

Attachments:

1 Budget

Variations for General, Water and Sewerage Funds, E2019/31363 , page 20⇩

2 Itemised

Listing of Budget Variations for General, WWater and Sewerage Funds, E2019/31364 ,

page 98⇩

3 Integrated

Planning and Reporting Framework (IP&R) required Quarterly Review

Statements, E2019/31365 , page 109⇩

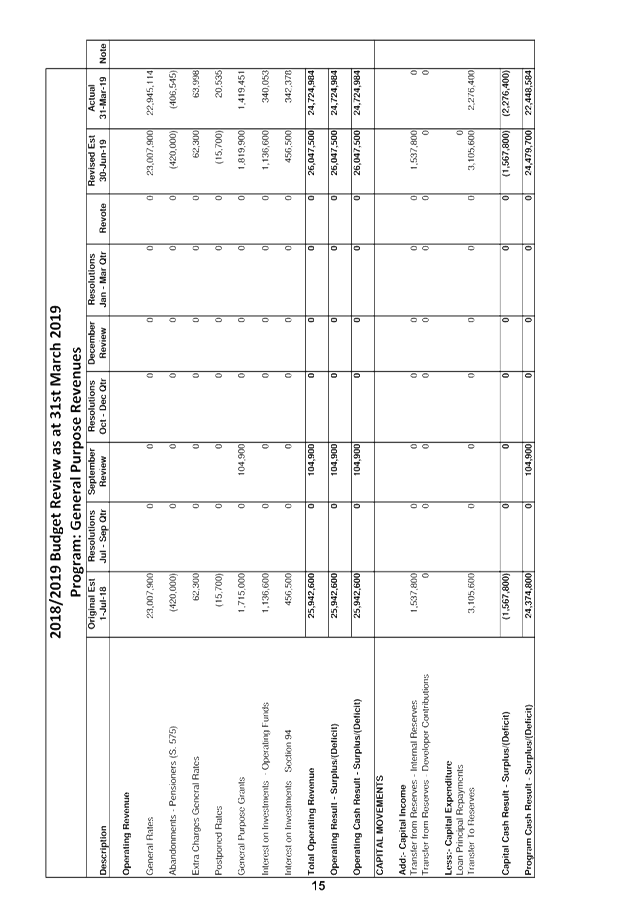

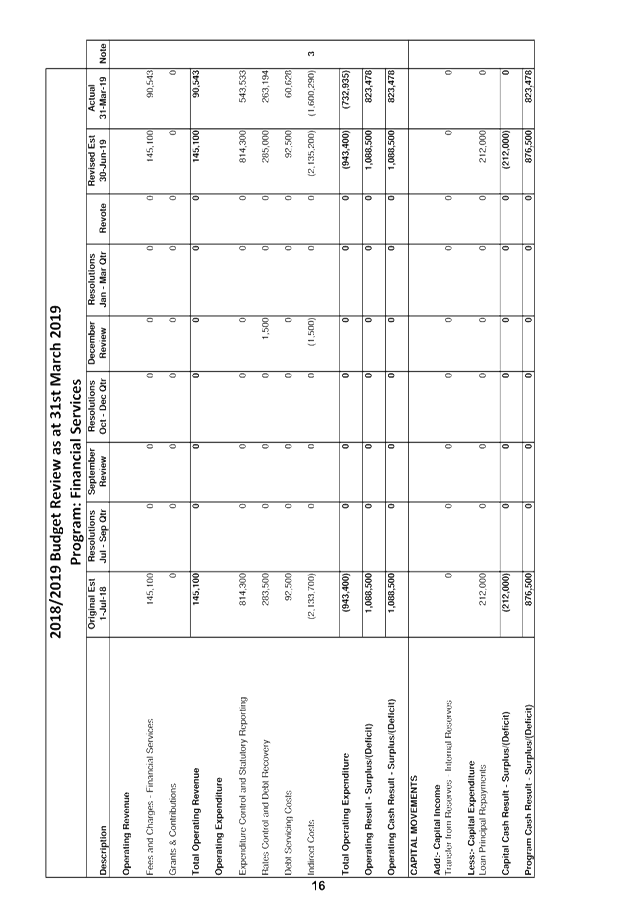

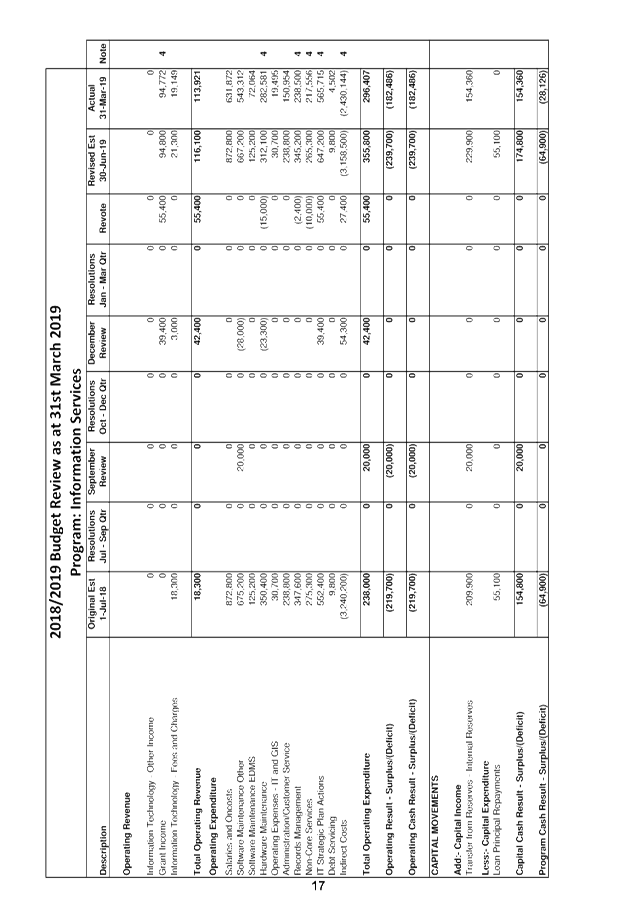

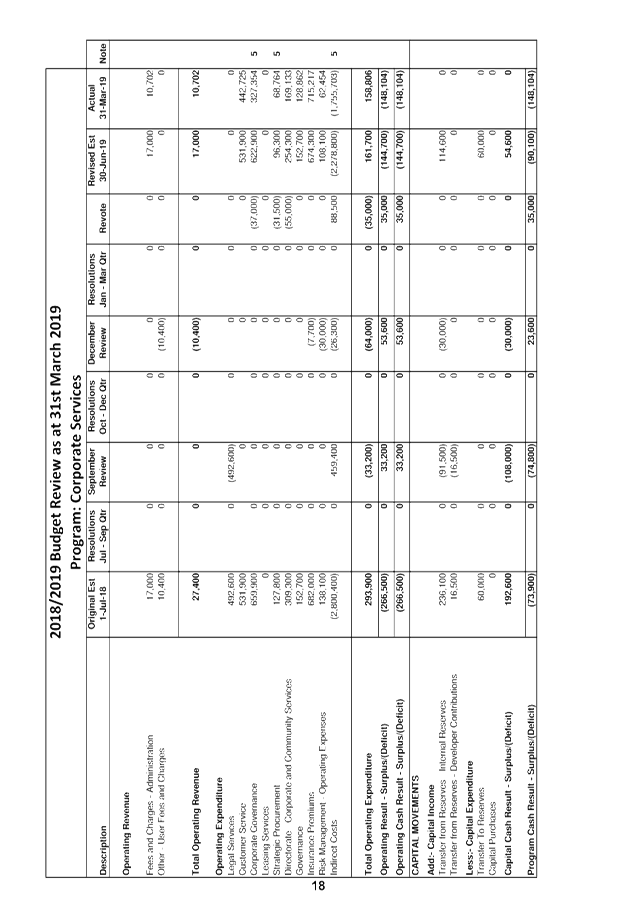

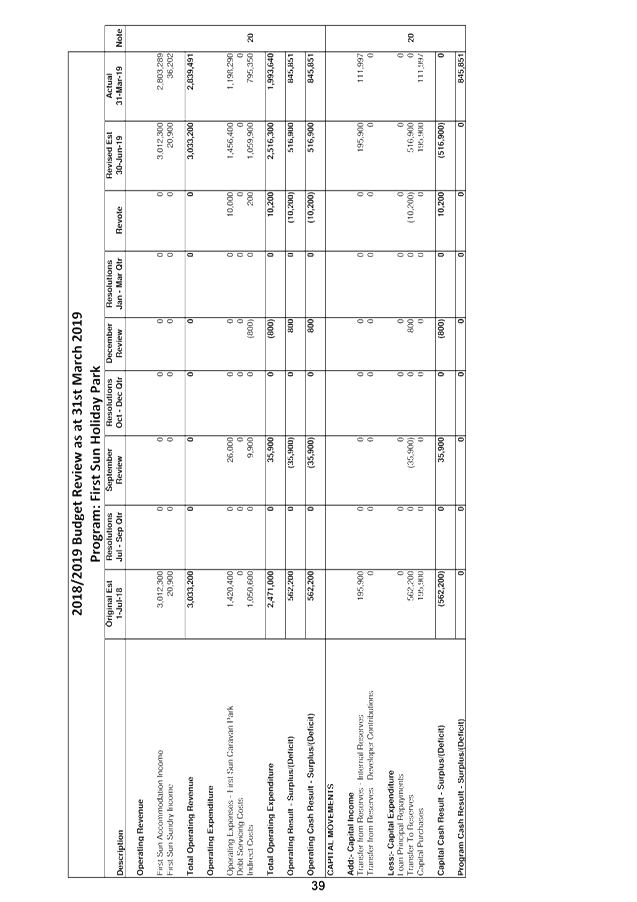

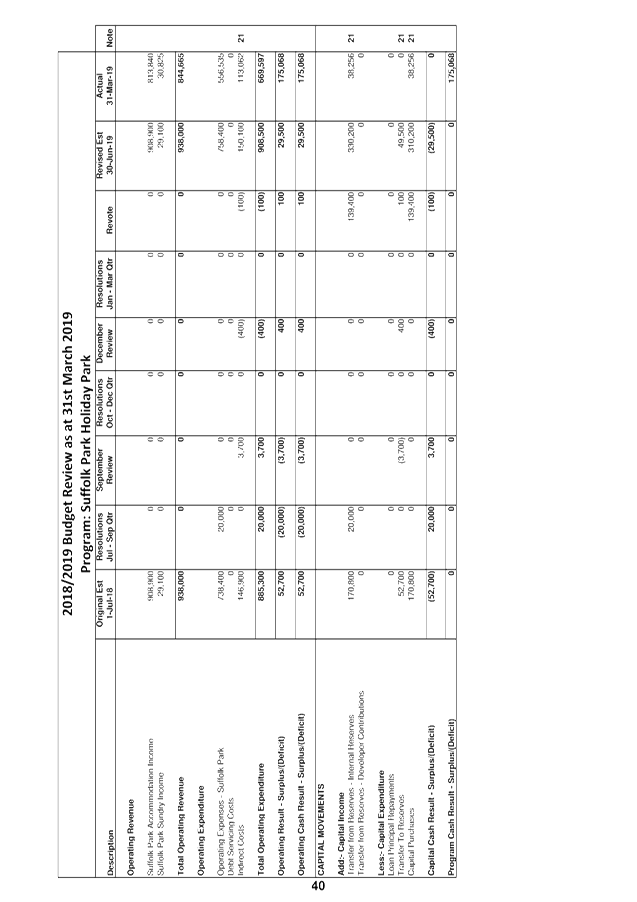

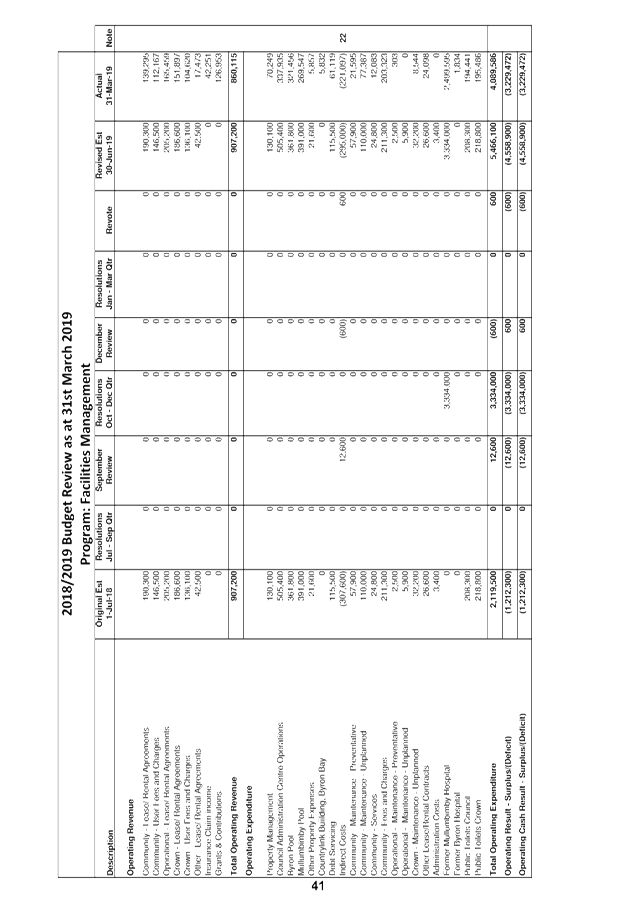

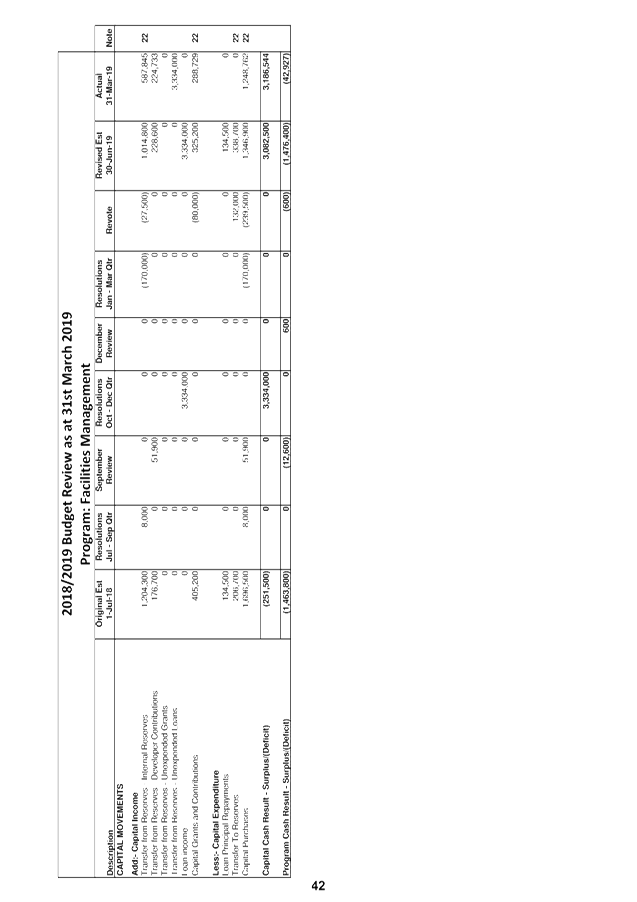

REPORT

Council adopted the 2018/2019 budget on 28 June 2018 via

Resolution 18-429. It also considered and adopted the budget carryovers

from the 2017/2018 financial year, to be incorporated into the 2018/2019 budget

at its Ordinary Meeting held on 23 August 2018 via Resolution 18-522.

Since that date Council has reviewed the budget, taking into consideration the

2017/2018 Financial Statement results and progress through the first half of

the 2018/2019 financial year. This report considers the March 2019

Quarter Budget Review.

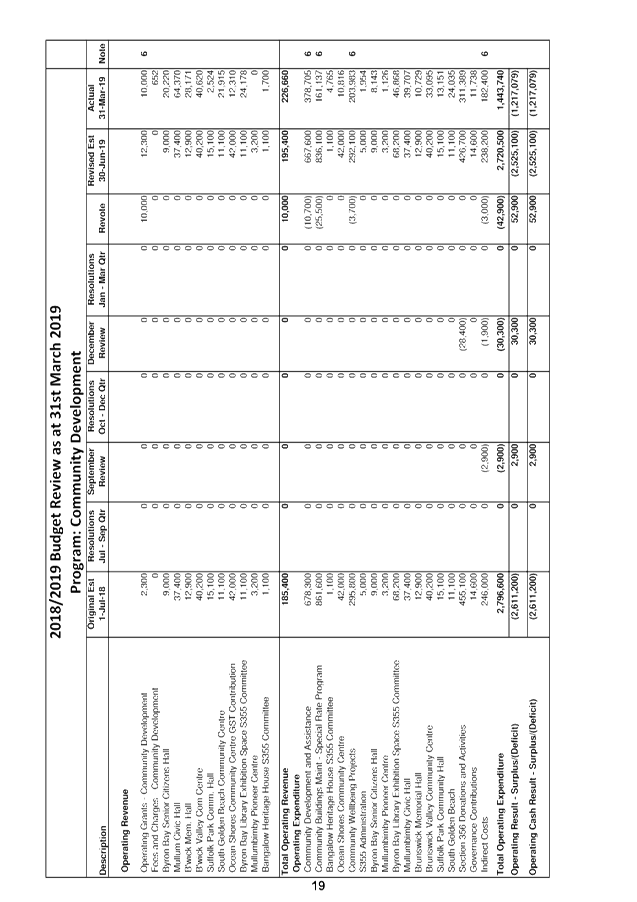

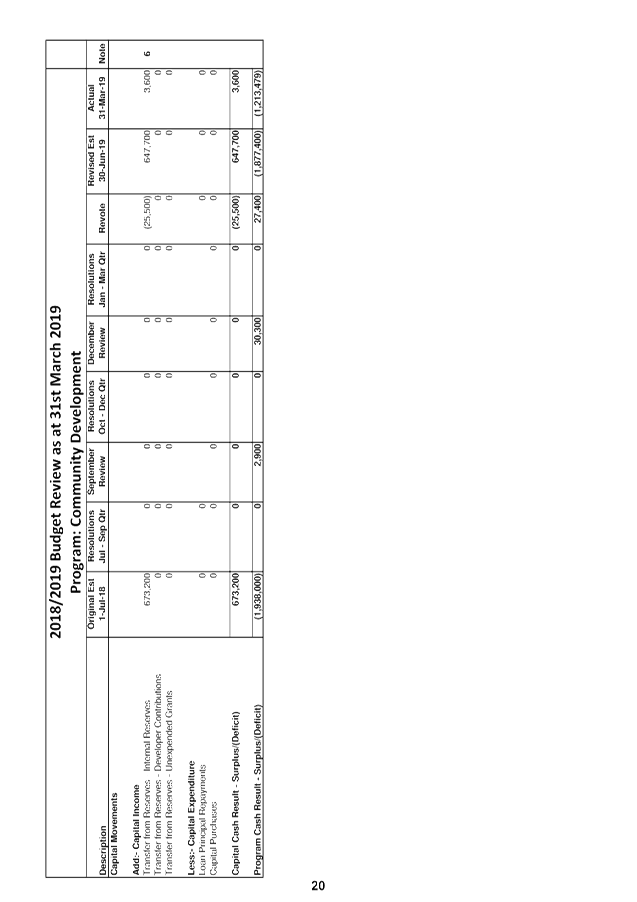

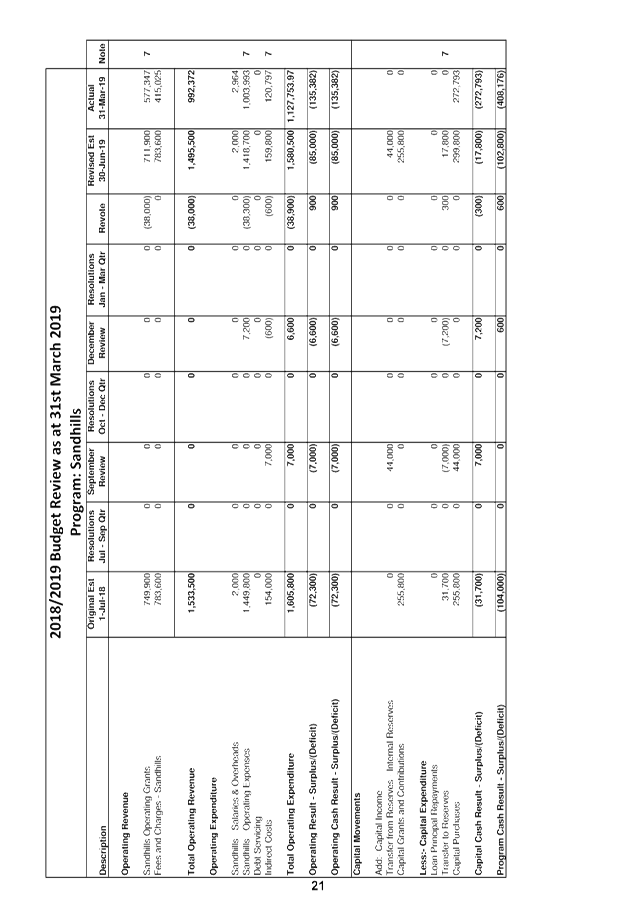

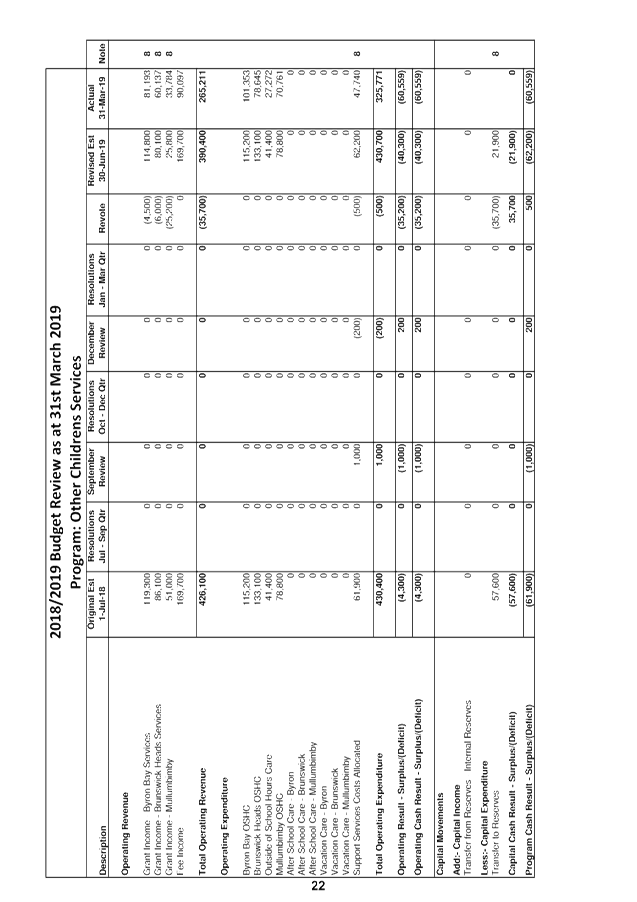

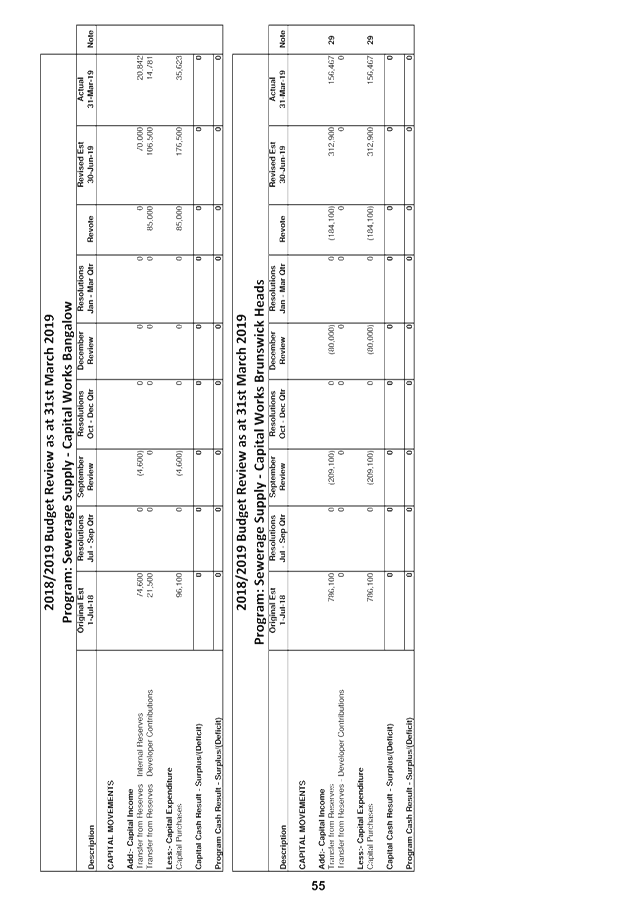

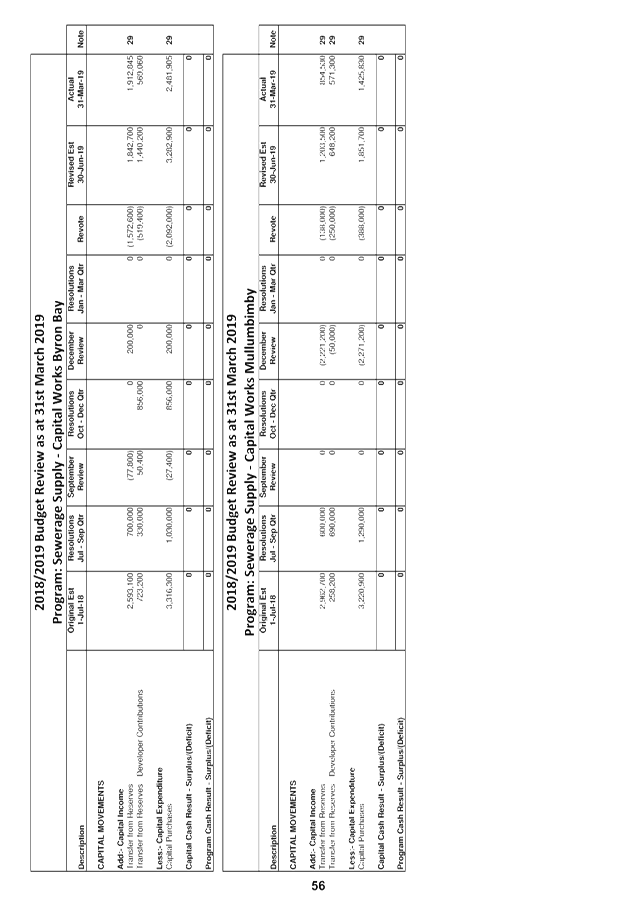

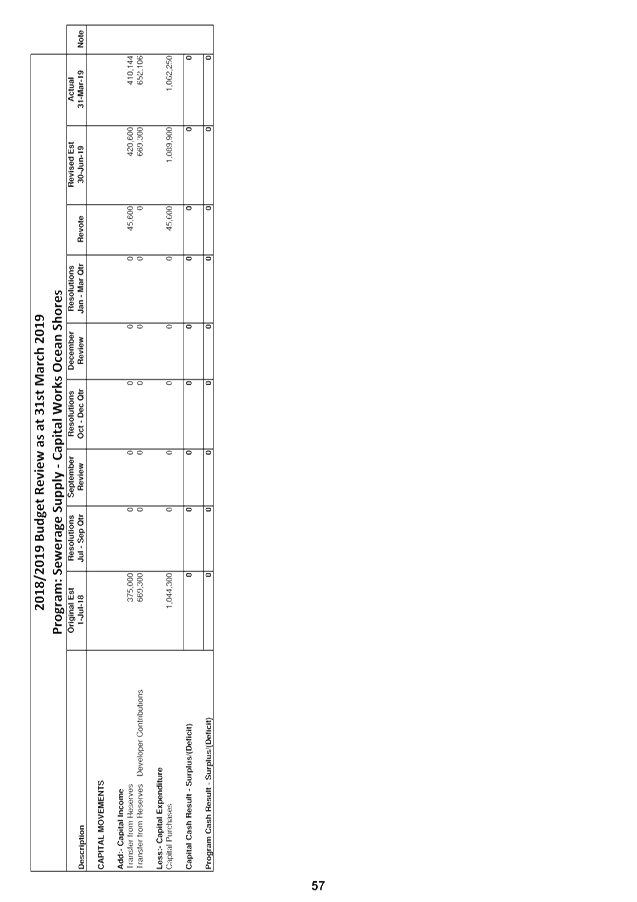

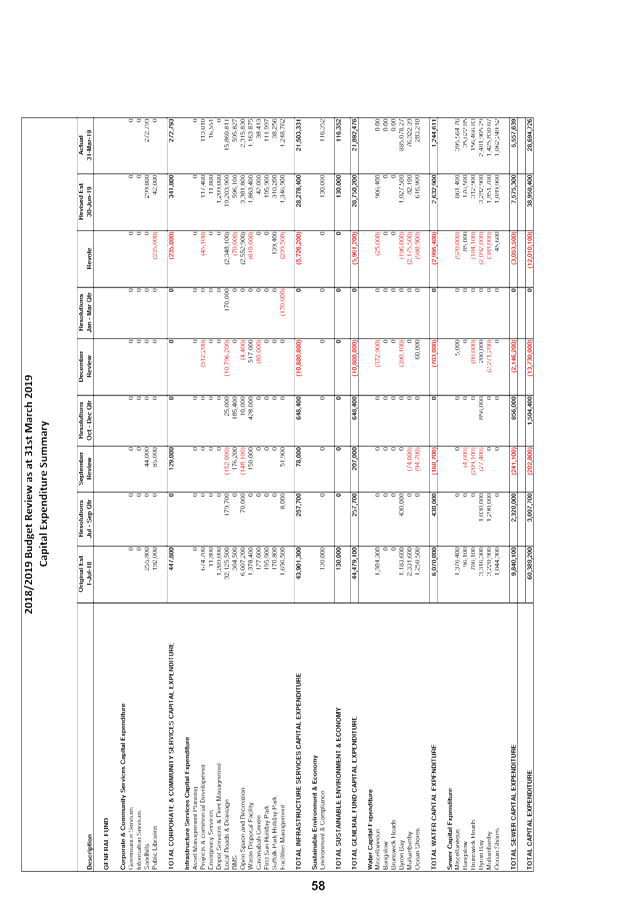

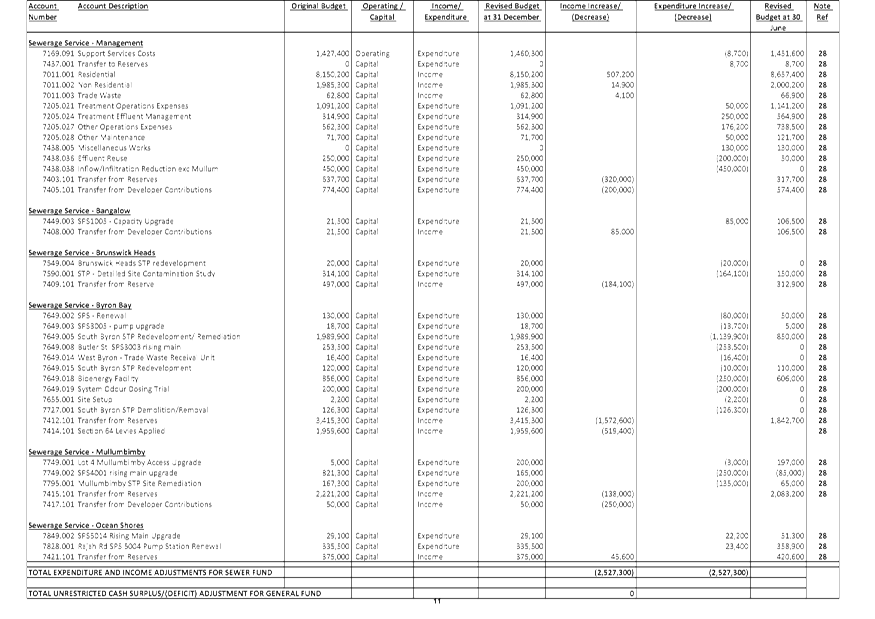

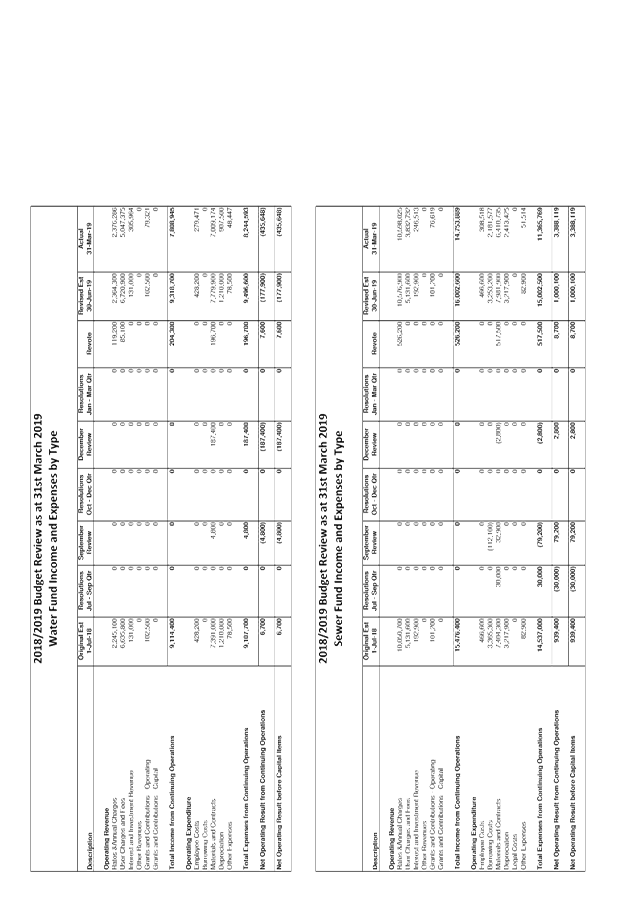

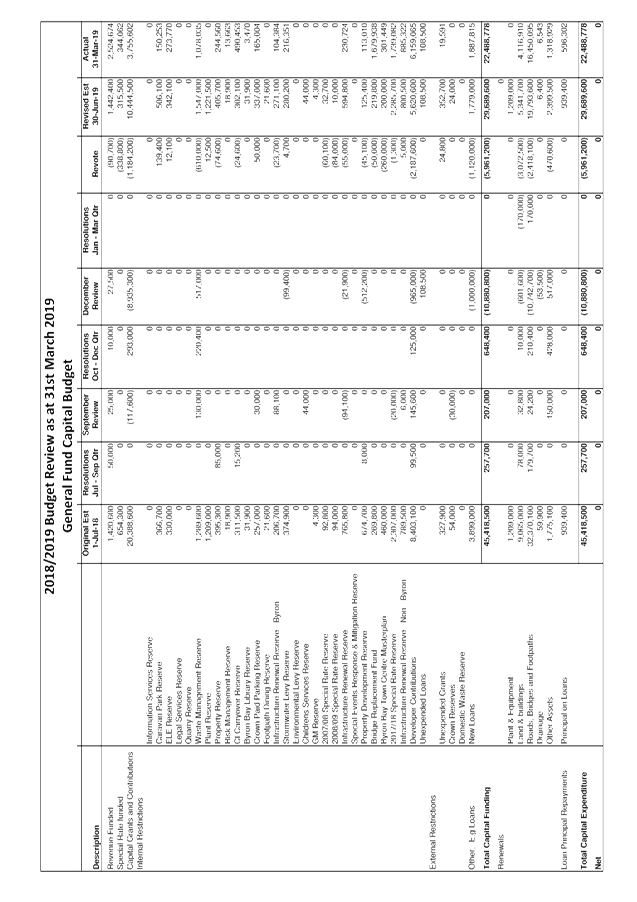

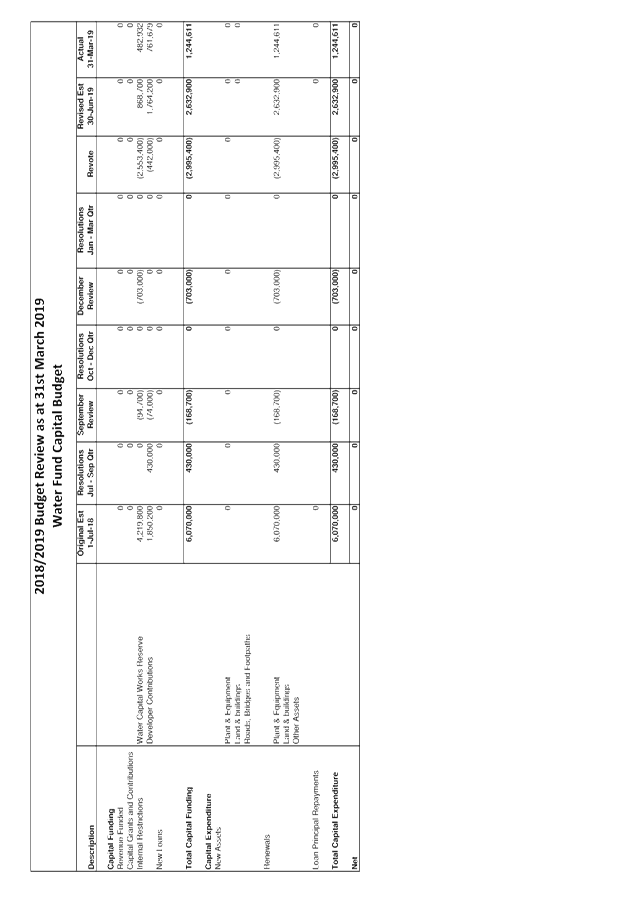

The details of the budget review for the Consolidated, General,

Water and Sewer Funds are included in Attachment 1, with an itemised listing in

Attachment 2. This aims to show the consolidated budget position of

Council, as well as a breakdown by Fund and Principal Activity. The document in

Attachment 1 is intended to provide Councillors with more detailed information

to assist with decision making regarding Council’s finances.

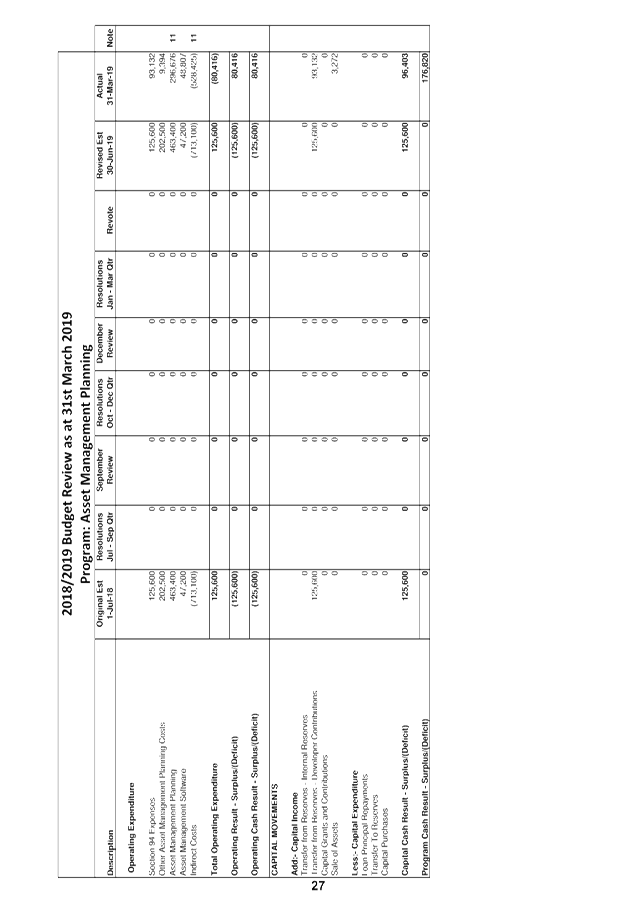

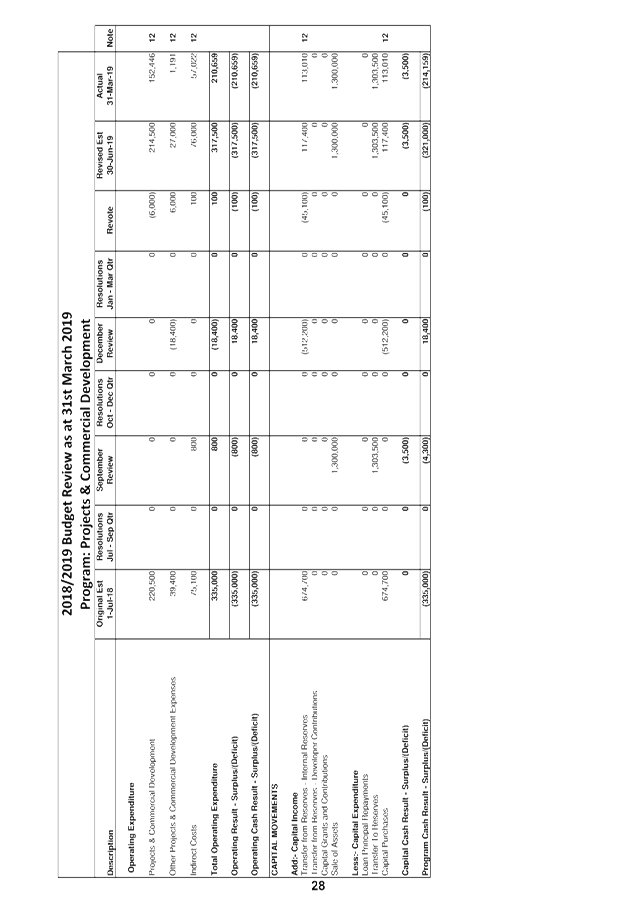

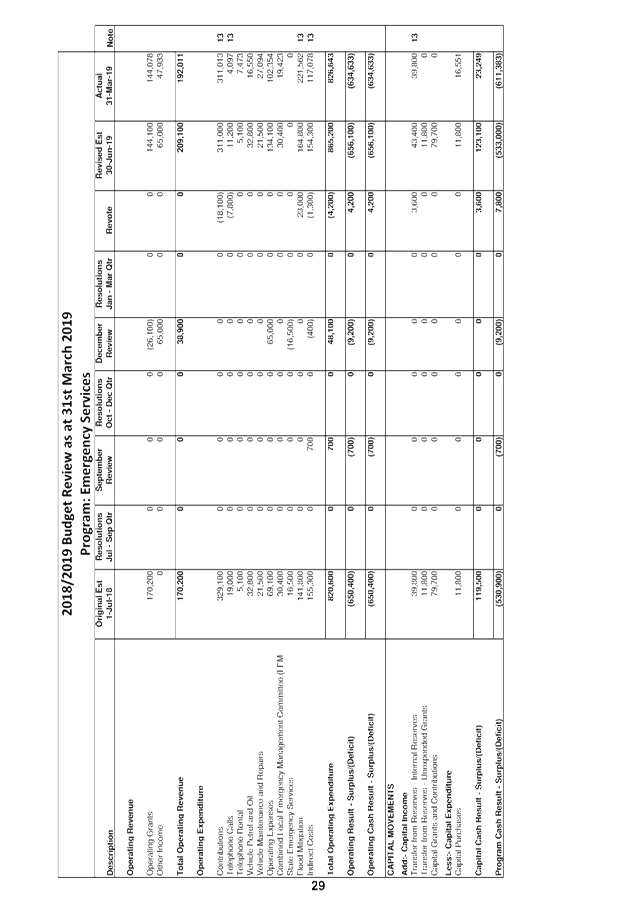

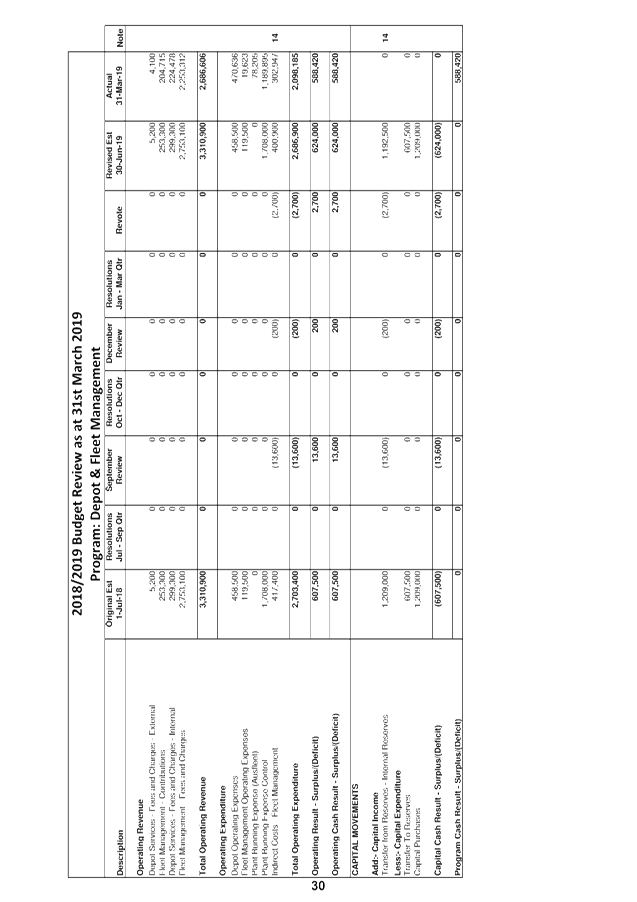

Attachment 1 has the following reporting hierarchy:

Consolidated Budget

Cash Result

General Fund Cash

Result Water Fund Cash Result Sewer

Cash Result

Principal Activity Principal

Activity Principal

Activity

Operating Income Operating

Expenditure Capital income Capital

Expenditure

The pages are presented (from left to right) showing the

original budget as adopted by Council on 28 June 2018 plus the adopted

carryover budgets from 2017/2018, followed by the resolutions between July and

September, the September budget review, resolutions between October and

December, the December review, resolutions between January and March, the

re-vote (or adjustment for this review) and then the revised position projected

for 30 June 2019 as at 31 March 2019.

On the far right of the Principal Activity, there is a

column titled “Note”. If this is populated by a number, it

means that there has been an adjustment in the quarterly review. This number

corresponds to the notes at the end of the Attachment which explain the

variation.

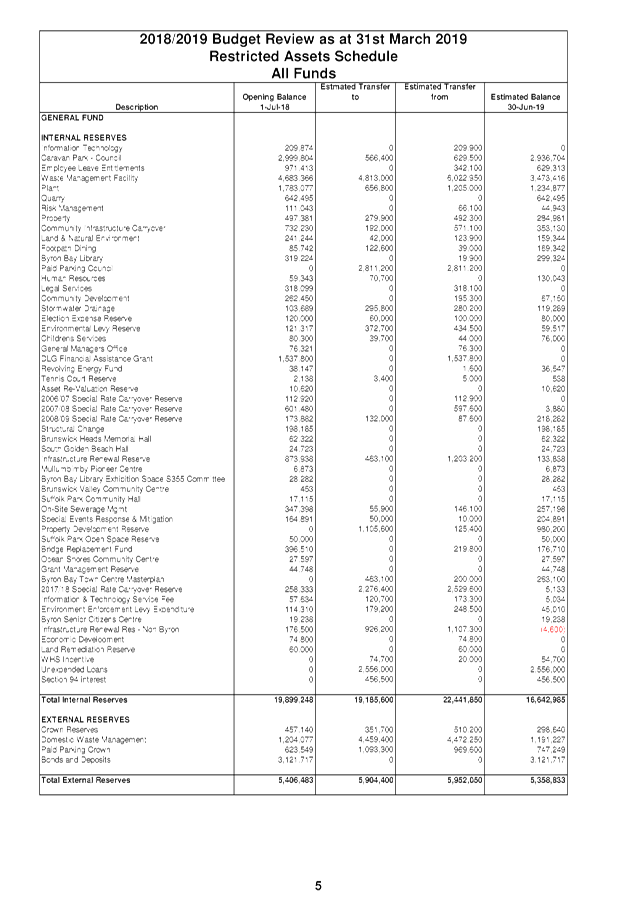

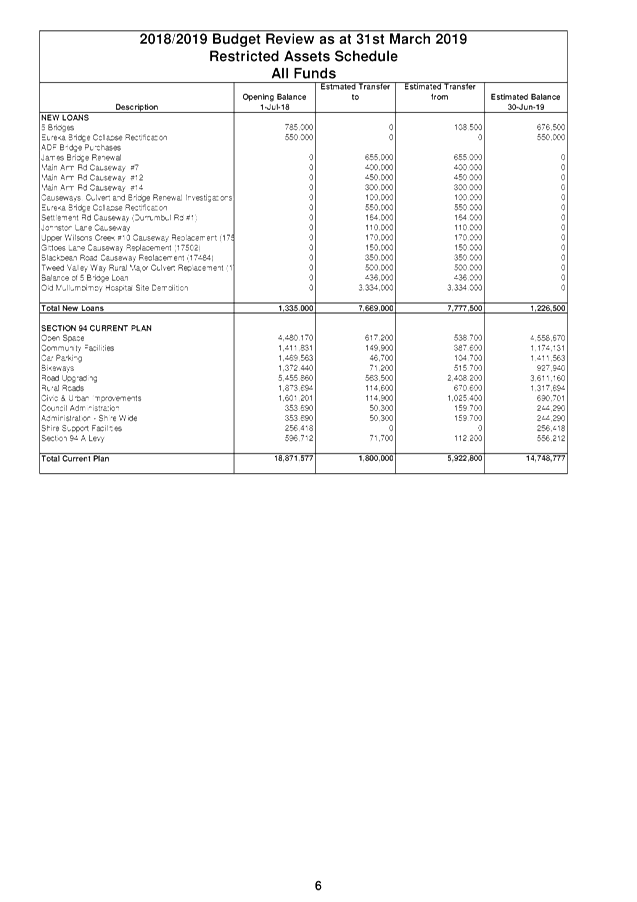

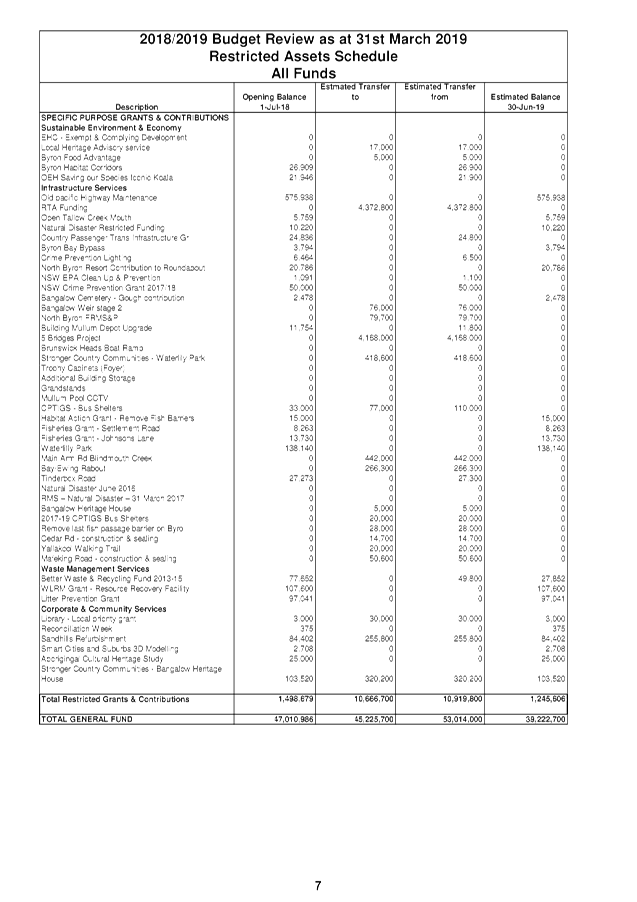

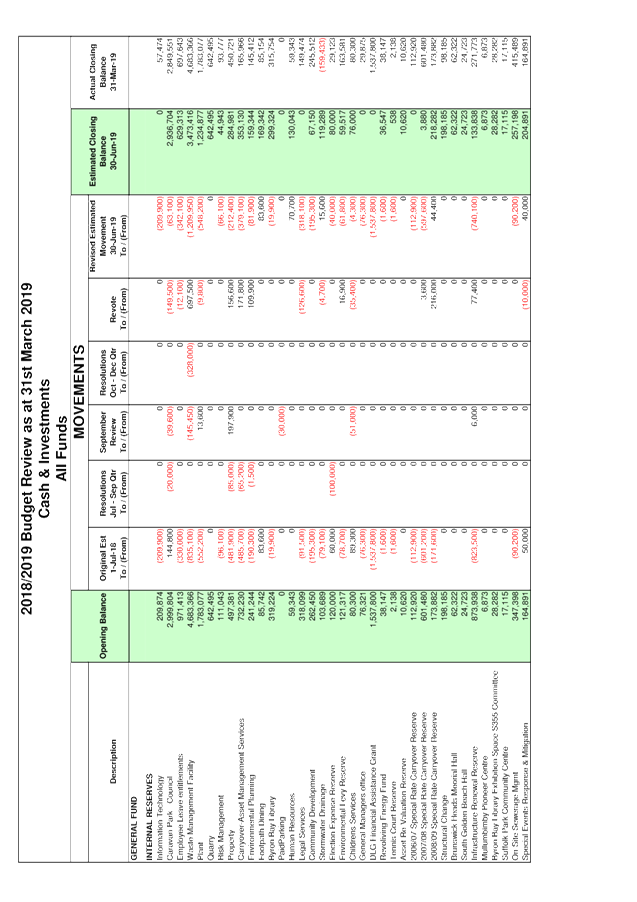

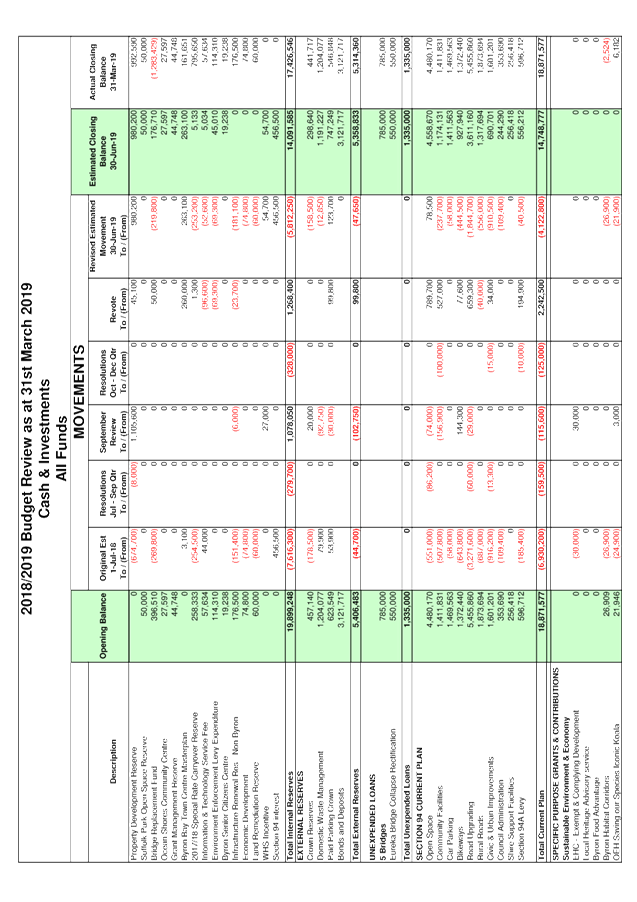

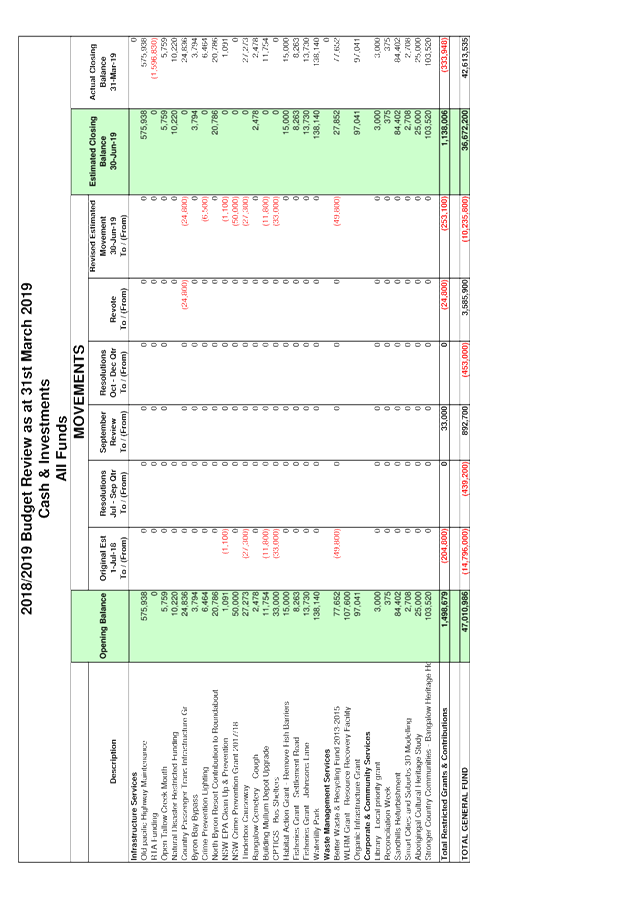

There is also information detailing restricted assets

(reserves) to show estimated balances as at 30 June 2019 for all

Council’s reserves.

A summary of Capital Works is also included by Fund and

Principal Activity.

Office of Local Government Budget Review Guidelines:-

On 10 December 2010 the Office of Local Government issued

new Quarterly Budget Review Guidelines via Circular 10-32, with the reporting

requirements to apply from 1 July 2011. This report includes a Quarterly

Budget Review Statement (refer Attachment 3) prepared by Council in accordance

with the guidelines.

The Quarterly Budget Review Guidelines set a minimum

standard of disclosure, with these standards being included in the Local

Government Code of Accounting Practice and Financial Reporting as mandatory

requirements for Council’s to address.

Since the introduction of the new planning and reporting

framework for NSW Local Government, it is now a requirement for Councils to

provide the following components when submitting a Quarterly Budget Review

Statement (QBRS):-

· A signed statement by

the Responsible Accounting Officer on Council’s financial position at the

end of the year based on the information in the QBRS

· Budget review income and

expenses statement in one of the following formats:

o Consolidated

o By fund (e.g. General, Water, Sewer)

o By function, activity, program etc.,

to align with the management plan/operational plan

· Budget Review Capital

Budget

· Budget Review Cash and

Investments Position

· Budget Review Key

performance indicators

· Budget Review Contracts

and Other Expenses

The above components are included in Attachment 3:-

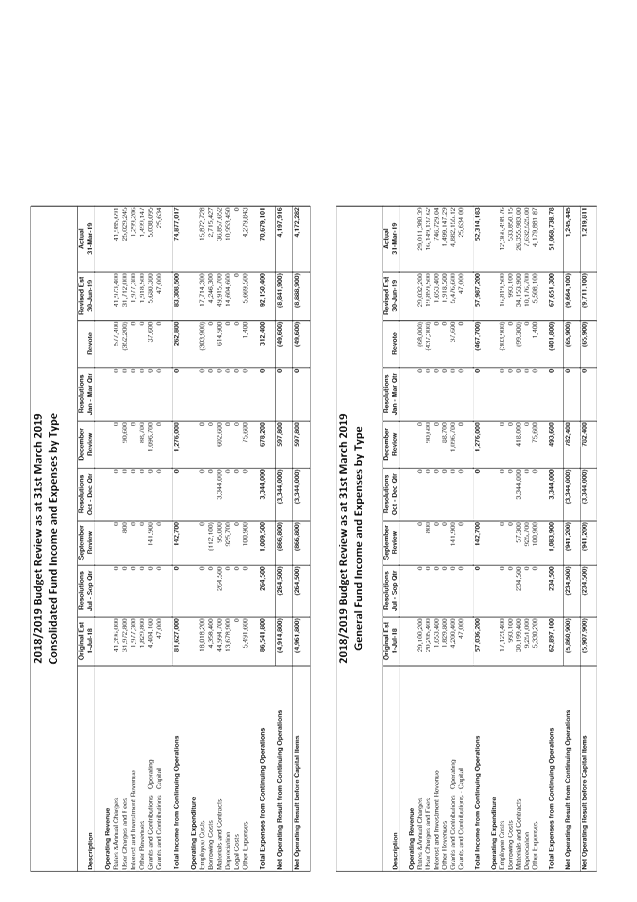

Income and Expenditure Budget Review Statement by Type

– This shows Council’s income and Expenditure by type. This

has been split by Fund. Adjustments are shown, looking from left to

right. These adjustments are commented on through the last 12 pages of

Attachment 1.

Capital Budget Review Statement – This

statement identifies in summary Council’s capital works program on a

consolidated basis and then split by Fund. It also identifies how the

capital works program is funded. As this is the first quarterly review for the

reporting period, the Statement may not necessarily indicate the total progress

achieved on the delivery of the capital works program.

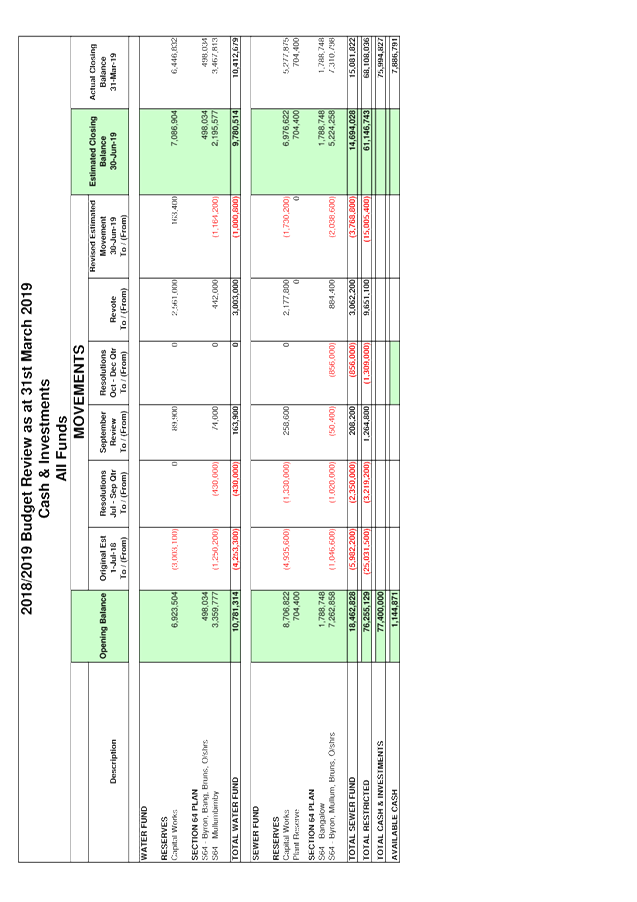

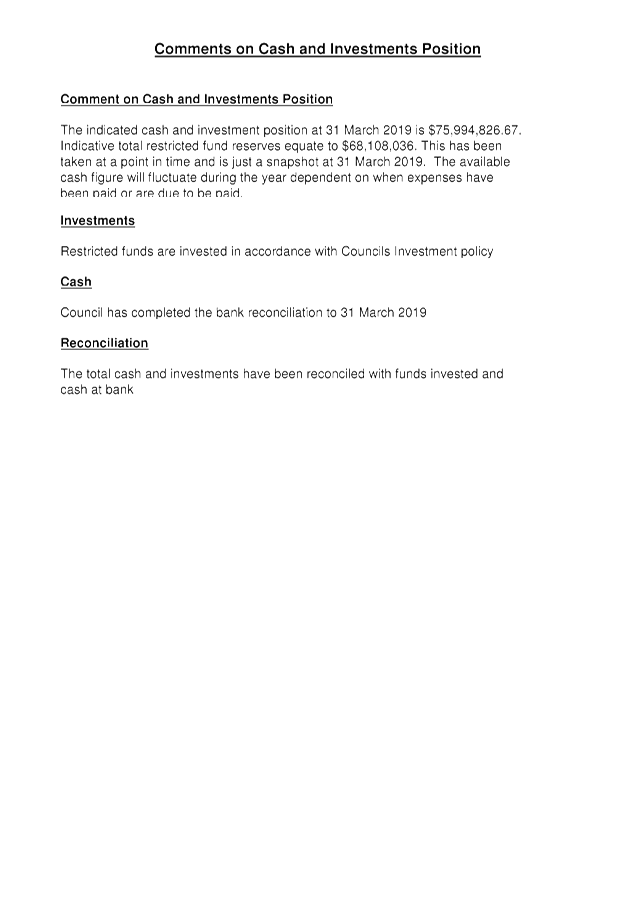

Cash and Investments Budget Review Statement – This

statement reconciles Council’s restricted funds (reserves) against

available cash and investments. Council has attempted to indicate an

actual position as at 31 March 2019 of each reserve to show a total cash

position of reserves with any difference between that position and total cash and

investments held as available cash and investments. It should be

recognised that the figure is at a point in time and may vary greatly in future

quarterly reviews pending on cash flow movements.

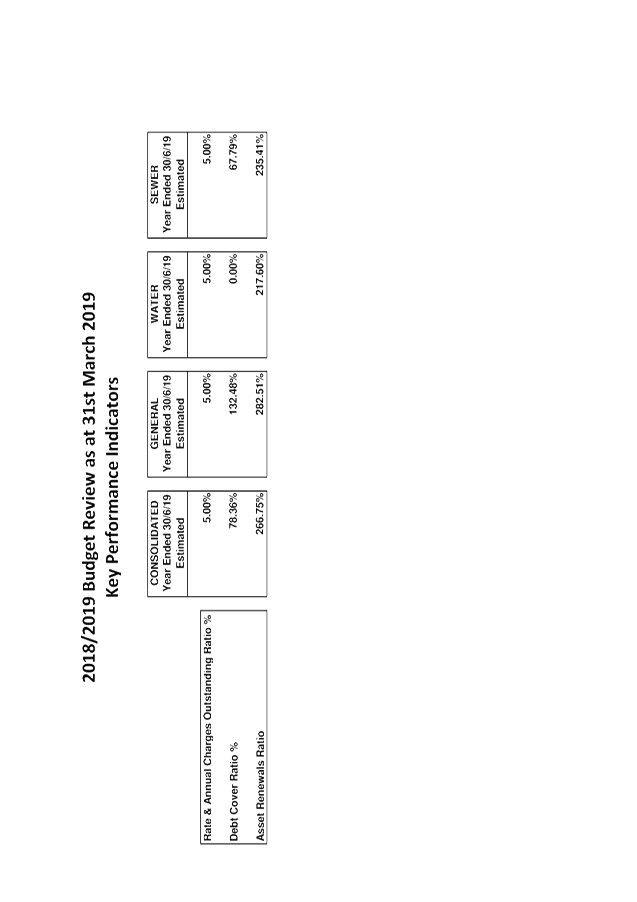

Key Performance Indicators (KPI’s) –

At this stage, the KPI’s within this report are:-

o Debt Service Ratio - This

assesses the impact of loan principal and interest repayments on the

discretionary revenue of Council.

o Rates and Annual Charges

Outstanding Ratio – This assesses the impact of uncollected rates and

annual charges on Councils liquidity and the adequacy of recovery efforts

o Asset Renewals Ratio – This

assesses the rate at which assets are being renewed relative to the rate at

which they are depreciating.

These may be expanded in future to accommodate any

additional KPIs that Council may adopt to use in the Long Term Financial Plan

(LTFP.)

Contracts and Other Expenses - This report highlights

any contracts Council entered into during the October to December quarter that

are greater then $50,000.

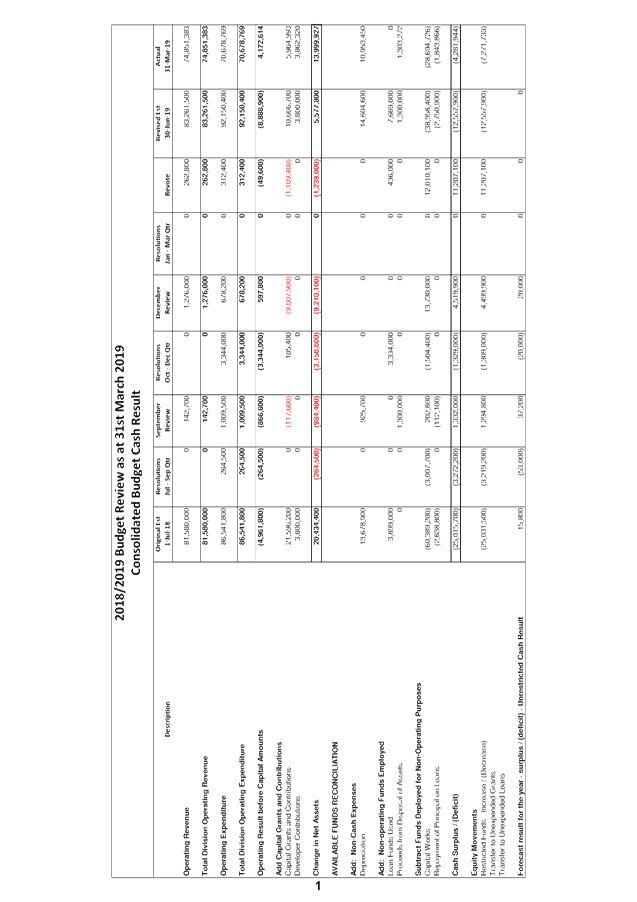

CONSOLIDATED RESULT

The following table provides a summary of the overall

Council budget on a consolidated basis inclusive of all Funds’ budget

movements for the 2018/2019 financial year projected to 30 June 2019 and

revised as at 31 March 2019.

|

2018/2019 Budget Review Statement as at 31 March 2019

|

Original Estimate (Including Carryovers)

1/7/2018

|

Adjustments to 31 Mar 2019 including Resolutions*

|

Proposed 31 Mar 2019 Review Revotes

|

Revised Estimate 30/6/2019 at 31/03/2019

|

|

Operating Revenue

|

81,580,000

|

1,418,700

|

262,800

|

83,261,500

|

|

Operating Expenditure

|

86,541,800

|

5,296,200

|

312,400

|

92,150,400

|

|

Operating Result –

Surplus/Deficit

|

(4,961,800)

|

(3,877,500)

|

(49,600)

|

(8,888,900)

|

|

Add: Capital Revenue

|

25,396,200

|

(9,740,100)

|

(1,189,400)

|

14,466,700

|

|

Change in Net Assets

|

20,434,400

|

(13,617,600)

|

(1,239,000)

|

5,577,800

|

|

Add: Non Cash Expenses

|

13,678,900

|

925,700

|

0

|

14,604,600

|

|

Add: Non-Operating Funds

Employed

|

3,899,000

|

4,634,000

|

436,000

|

8,969,000

|

|

Subtract: Funds Deployed for

Non-Operating Purposes

|

(63,028,000)

|

9,308,600

|

12,010,100

|

(41,709,300)

|

|

Cash Surplus/(Deficit)

|

(25,015,700)

|

1,250,700

|

11,207,100

|

(12,557,900)

|

|

Restricted Funds –

Increase / (Decrease)

|

(25,031,500)

|

1,266,500

|

11,207,100

|

(12,557,900)

|

|

Forecast Result for the

Year – Surplus/(Deficit) – Unrestricted Cash Result

|

15,800

|

(15,800)

|

0

|

0

|

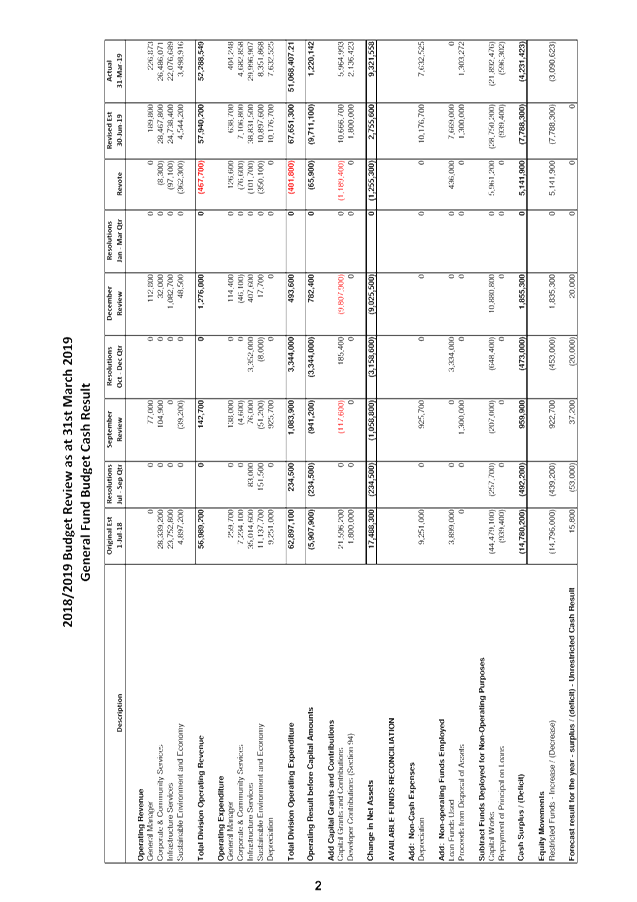

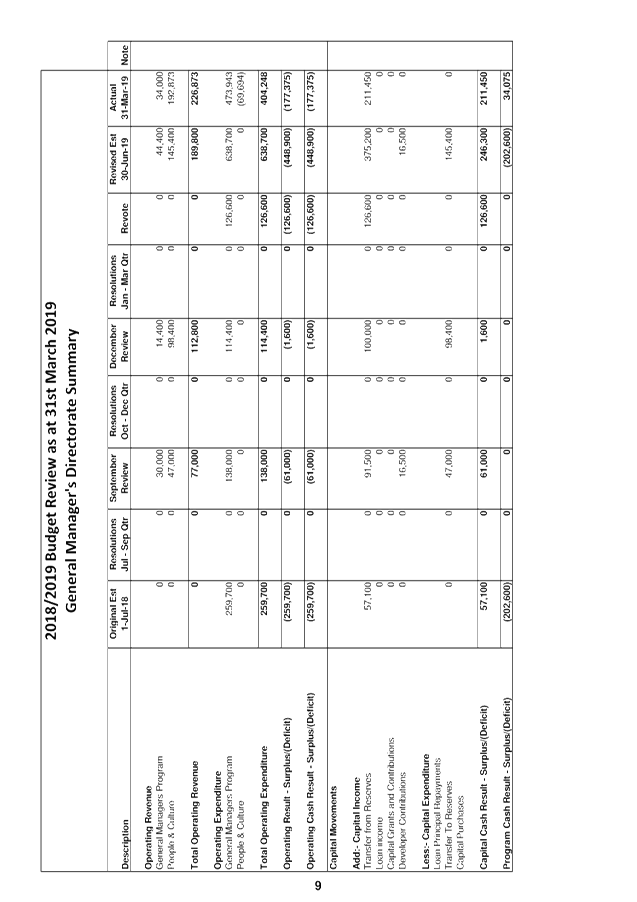

GENERAL FUND

In terms of the General Fund projected Unrestricted Cash

Result, the following table provides a reconciliation of the estimated position

as at 31 March 2019:

|

Opening Balance – 1

July 2018

|

$1,145,200

|

|

Plus original budget

movement and carryovers

|

15,800

|

|

Council Resolutions July

– September Quarter

|

(53,000)

|

|

Recommendations September

Budget Review – increase/(decrease)

|

37,200

|

|

Council Resolutions October

– December Quarter

|

($20,000)

|

|

Recommendations December

Budget Review – increase/(decrease)

|

20,000

|

|

Council Resolutions January

– March Quarter

|

0

|

|

Recommendations within this

Review – increase/(decrease)

|

0

|

|

Forecast Unrestricted

Cash Result – Surplus/(Deficit) – 30 June 2019

|

0

|

|

Estimated Unrestricted

Cash Result Closing Balance – 30 June 2019

|

$1,145,200

|

Overall, the General Fund financial position has remained

balanced as a result of this budget review, leaving the forecast cash result

for 2018/2019 also balanced.

Council Resolutions

There were no Council resolutions during the January to

March quarter that affected the forecast cash result.

Budget Adjustments

The budget adjustments identified in Attachments 1 and 2 for

the General Fund have been summarised by Budget Directorate in the following

table:

|

Budget Directorate

|

Revenue

Increase/

(Decrease) $

|

Expenditure

Increase/

(Decrease) $

|

Accumulated

Surplus (Working Funds) Increase/ (Decrease) $

|

|

General Manager

|

126,600

|

126,600

|

0

|

|

Corporate & Community Services

|

(186,800)

|

(265,000)

|

78,200

|

|

Infrastructure Services

|

(5,361,100)

|

(5,420,700)

|

59,600

|

|

Sustainable Environment & Economy

|

(425,200)

|

(287,400)

|

(137,800)

|

|

Total Budget Movements

|

(5,846,500)

|

(5,846,500)

|

0

|

Budget Adjustment Comments

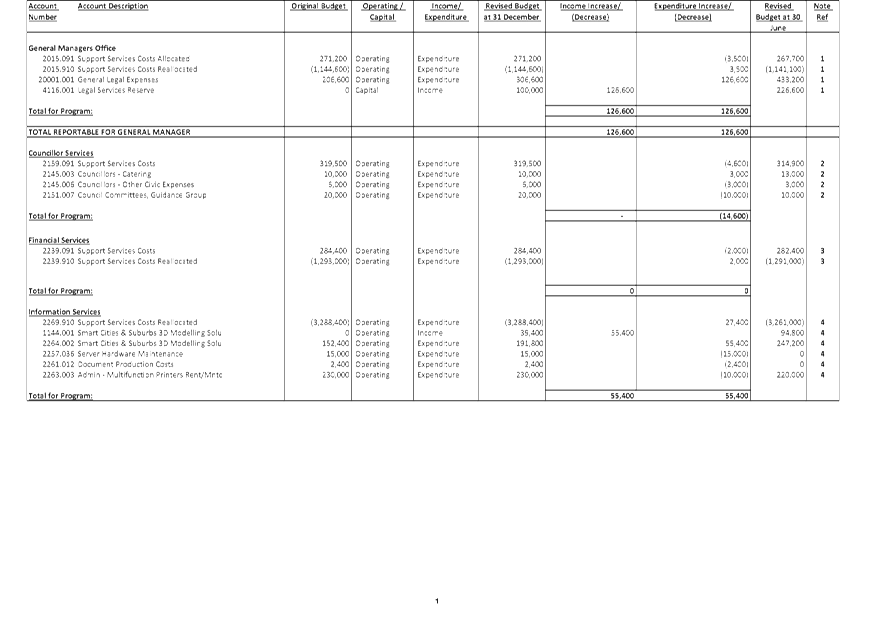

Within each of the Budget Directorates of the General Fund,

are a series of budget adjustments identified in detail at Attachment 1 and

2. More detailed notes on these are provided in Attachment 1 but the

major additional items included are summarised below by Directorate and are

included in the overall budget adjustments table above:

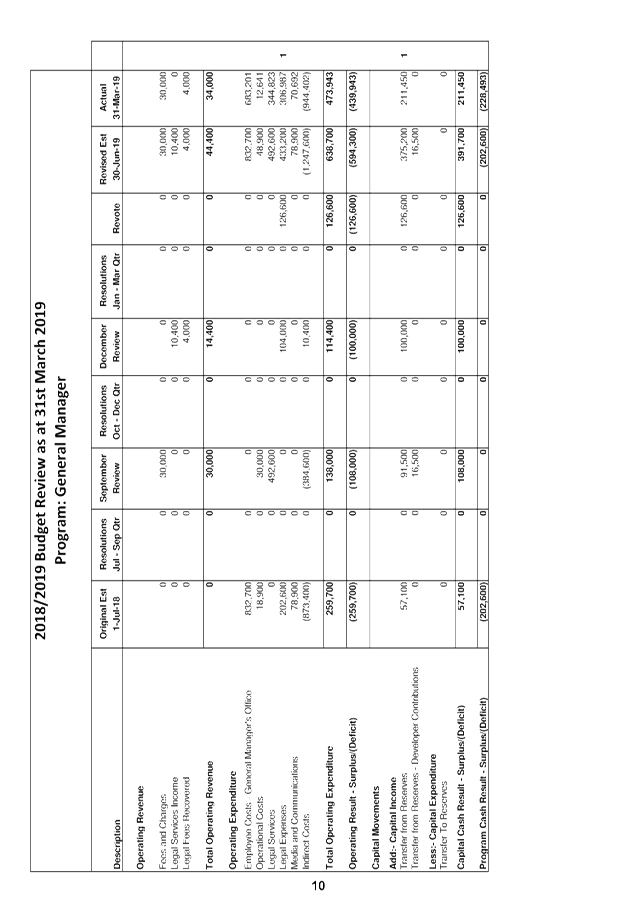

General Manager

· In the General

Manager’s program, it is proposed to increase the Legal Services budget

by $126,600 to allow for the anticipated increase in legal costs prior to the

end of the financial year. This can be funded from the Legal Services

reserve and legal fees recovered. This increase in expenditure will fully

deplete the legal services reserve. Council will need to address the

funding for the legal services reserve.

Corporate and Community Services

· In the Information

Services program, it is proposed to increase revenue and expenditure by $55,400

due to the final instalment of the grant for the Smart Cities & Suburbs 3D

Modelling Solutions project. It is proposed to decrease operating expenditure

for Server Hardware Maintenance ($15,000), Document Production Costs ($2,400),

and Multi Function Printer rent and maintenance ($10,000), as actual

expenditure will be under the current allocated budgets. These adjustments

against expenditure are offset through support services costs allocated to

other budget programs.

· In the Corporate

Services Program, it is proposed to decrease expenditure due to Delegations

Management ($2,000), Grants Management, ($35,000) and Procurement Expenses

($6,000) expected to remain unexpended in 2018/19. There are also savings

of $80,500 that can be recognised against salaries due to vacancies that have

occurred to different positions during the year. The decrease in the Corporate

Services program is offset by a support service cost adjustment of the same

amount so no budget change is realised in the program. However, the

decrease in support service costs are realised in other programs of Council

through a decrease in their support service costs.

· In the Community

Development program, it is proposed to increase operating income by $10,000 due

to the final instalment of the Love Byron Halls project being received and

decrease operating expenditure by $42,900 for Schoolies Approvals being less

than the budget ($3,700) and budgets no longer required for the Social

Innovation/Entrepreneurship Projects ($5,000) and the Youth Small Changes

Grants ($5,500). It is also proposed to remove $25,500 of the

Urgent/Unplanned Community Building maintenance budget and place back in the

2007/08 Special Rate reserve. This can then be used to fund part of the

Solar Panel Installation in the Facilities Management program. It is

proposed to decrease support service costs by $3,000.

· In the Sandhills

program, it is proposed to decrease operating income and expenditure by

$38,000. Sandhills does not currently have any children with special needs, so

the Special Needs funding grant will not be received. This is offset by a

decrease in inclusion support workers’ employee costs for staff that

would normally assist any special needs children.

· In the Other Children’s

Service program, it is proposed to decrease operating income by $35,700 as

grants for special needs will not be received. None of Council’s

OOSH services currently has any students with special needs.

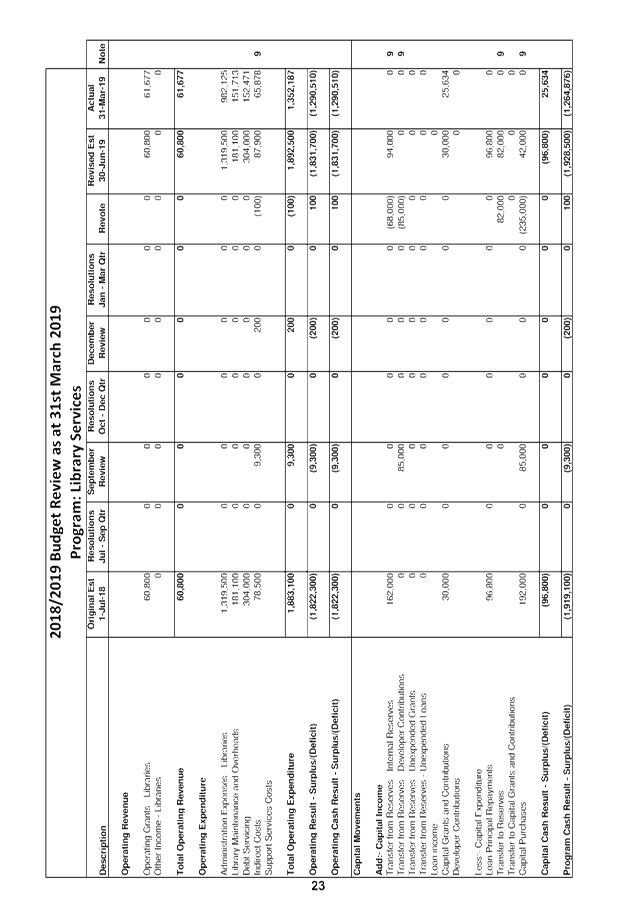

· In the Public Libraries

program, it is proposed to decrease capital expenditure by removing the

Brunswick Heads Library Upgrade ($235,000) (Council funding) from the budget,

as a grant needed to complete the project has not been approved.

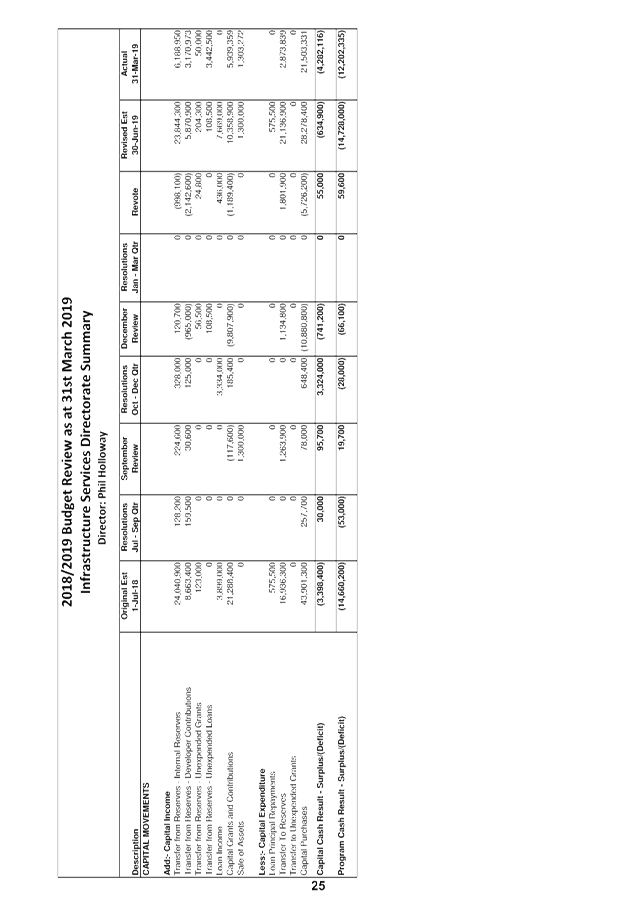

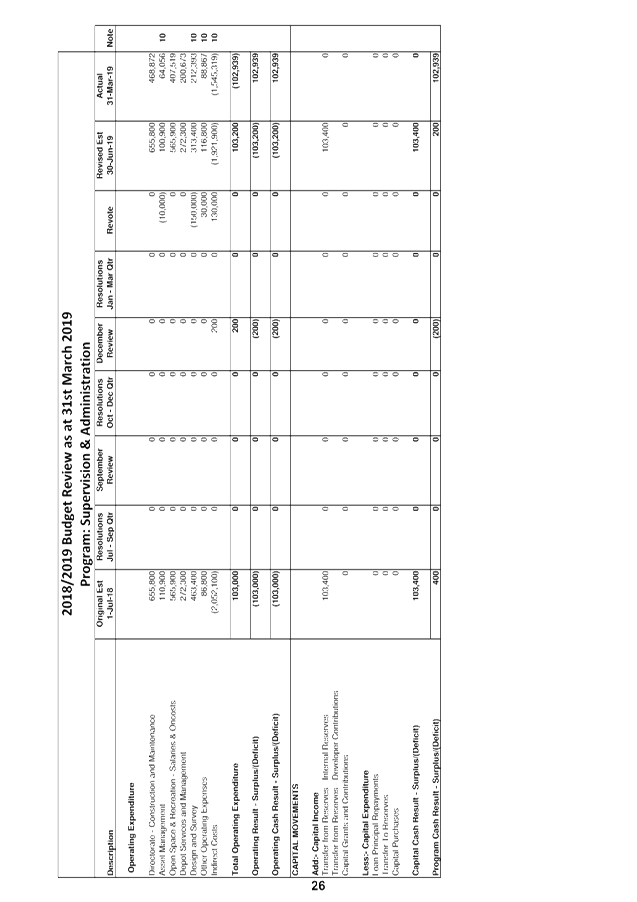

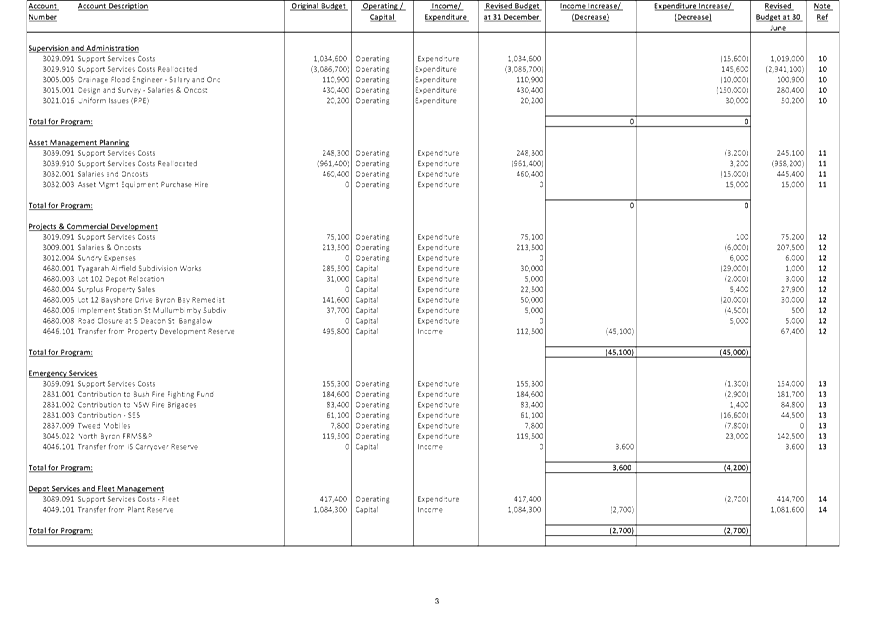

Infrastructure Services

· In the

Supervision & Administration program, it is proposed to decrease the

salaries budget by $160,000. In the Infrastructure Services directorate, the

majority of salaries are costed against the Supervision & Administration

program. These costs are then dispersed across the other Infrastructure

Services programs dependent on the position’s estimated time spent

working within that program. These percentages are determined when the

budget is created. During the year, some costs that have been budgeted

for in this program have been costed against different projects and

maintenance, therefore creating savings in these ledger accounts. An

increase in the costs associated with uniform issues is also required ($30,000).

The overall decrease expenditure within the Supervision & Administration

program is offset by a support service cost adjustment of the same amount so no

budget change is realised in the program. However, the decrease in

support service costs is realised in other Infrastructure Services programs

through a decrease in their support service costs.

· In the

Projects & Commercial Development program, it is proposed to decrease

capital expenditure due to various works that will not be completed in the 2018/2019

financial year.

· In the

Emergency Services program, it is proposed to decrease operating expenditure by

$4,200 due to actual expenditure for emergency services contributions (RFS, NSW

Fire and SES) being less than the budget ($18,100), a decrease against Tweed

RFS mobile charges ($7,800), an increase against the North Byron Flood Risk

Management Study & Plan to match grant funding to assist a consultant in

completing additional work ($23,000) and a support service cost decrease

($1,300).

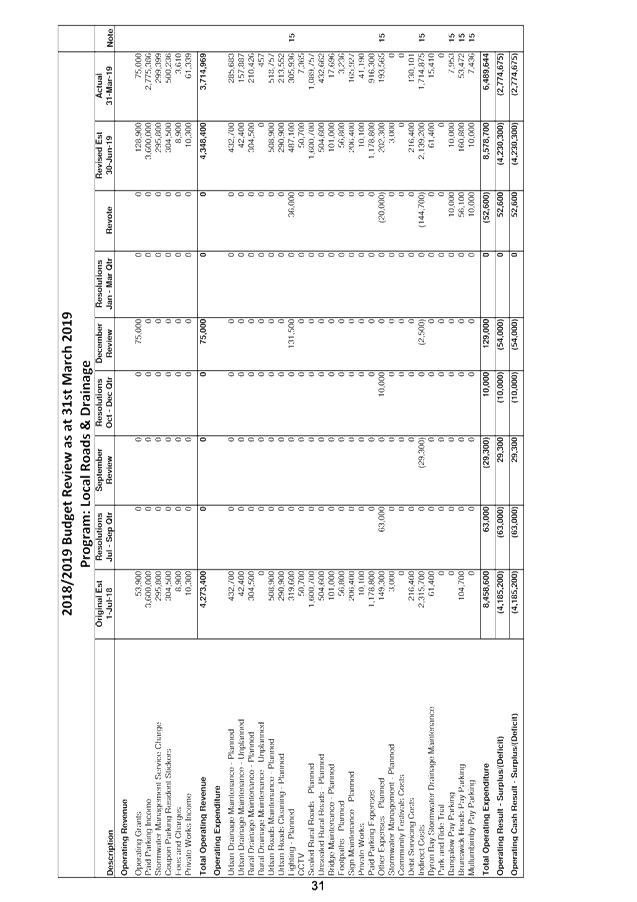

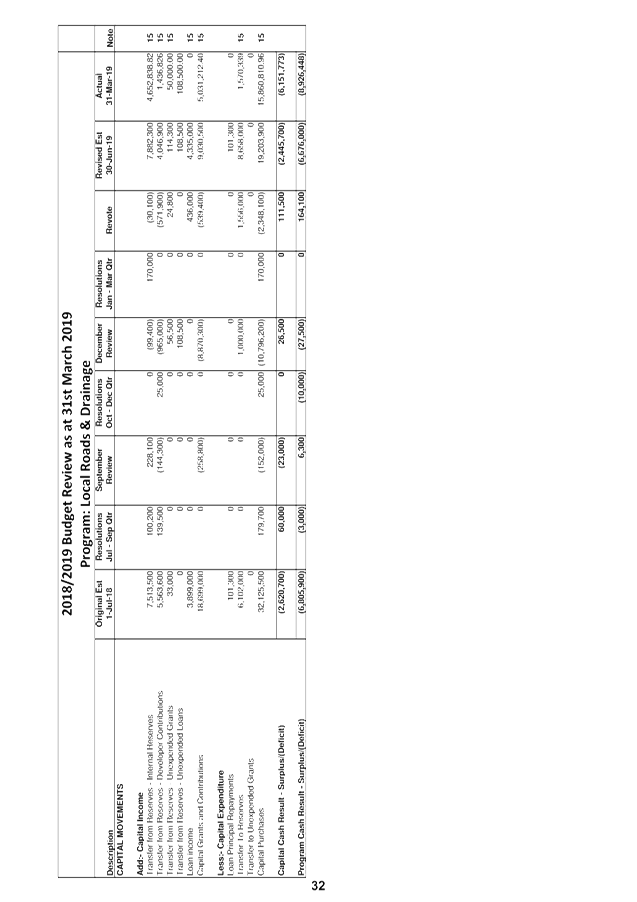

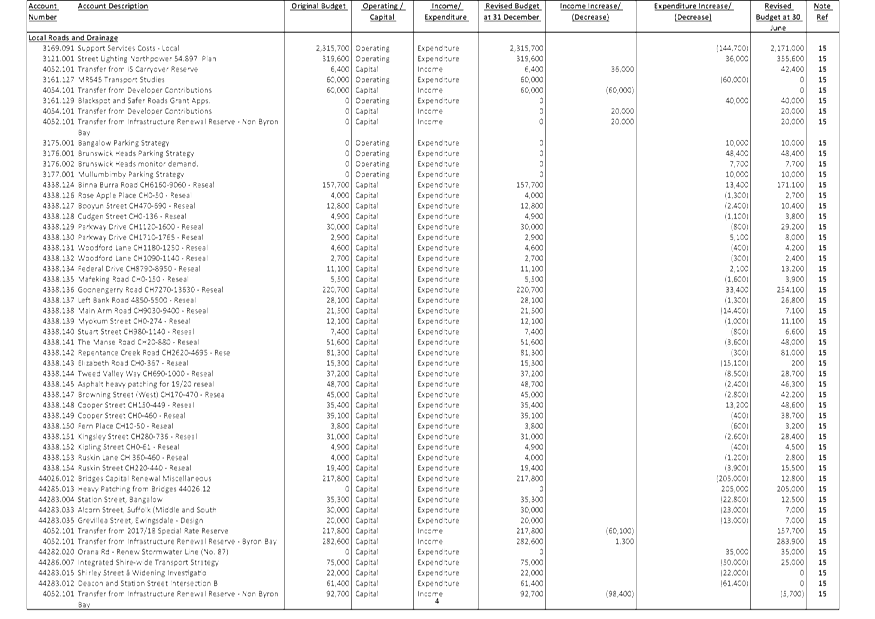

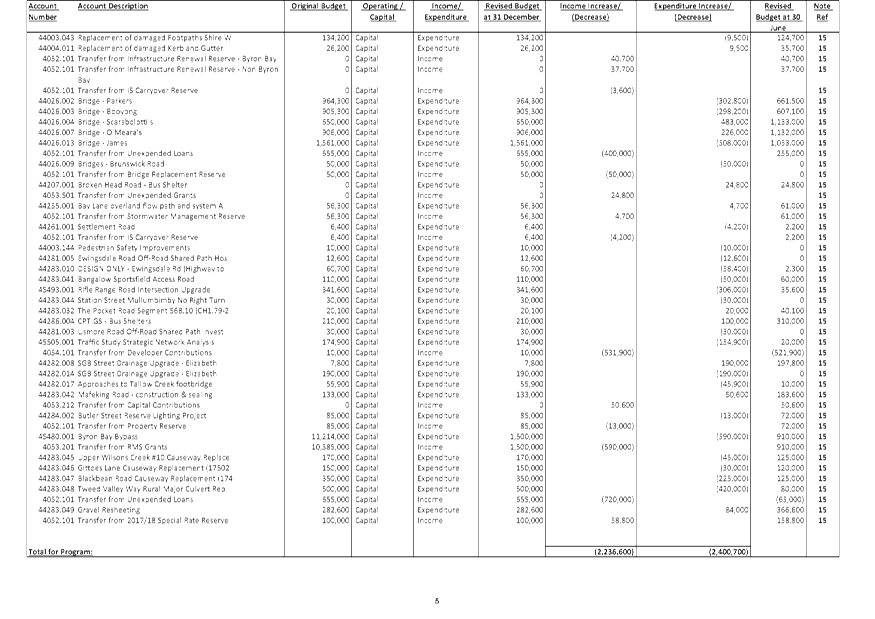

· In the Local Roads and

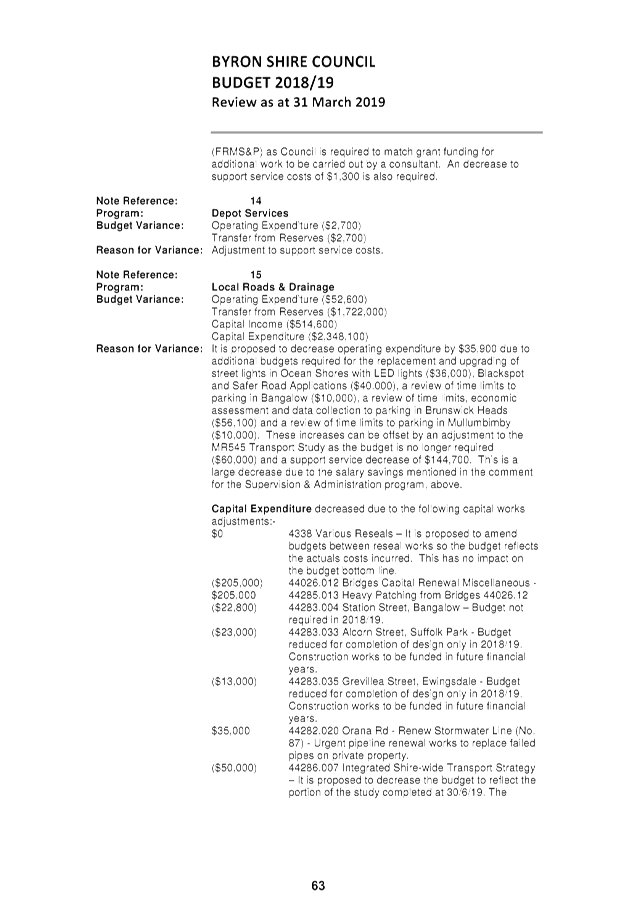

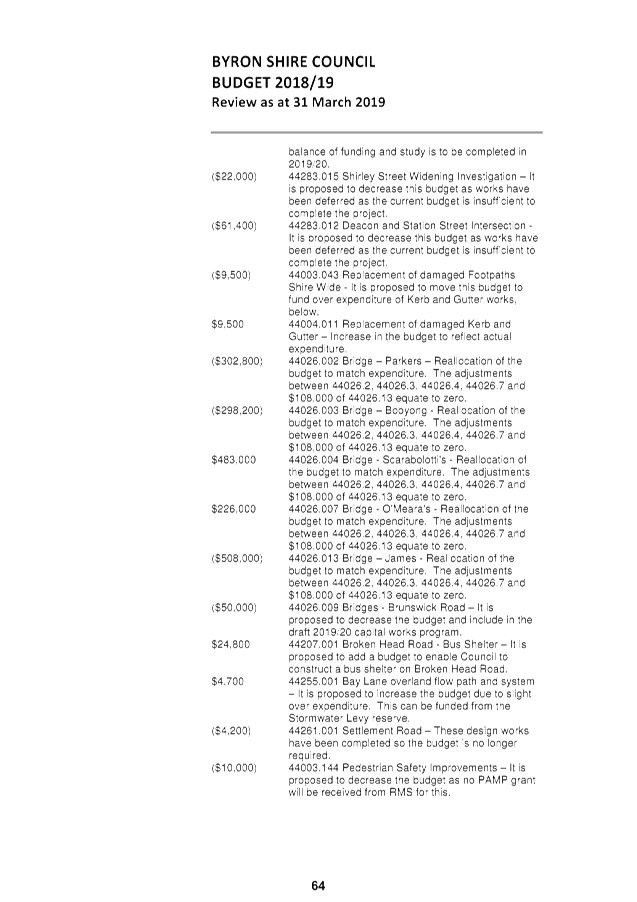

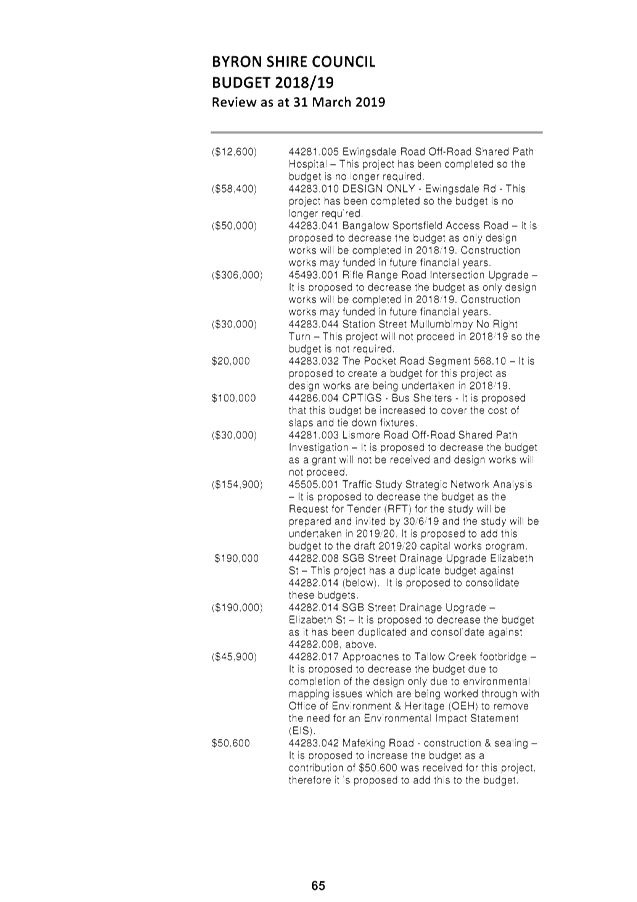

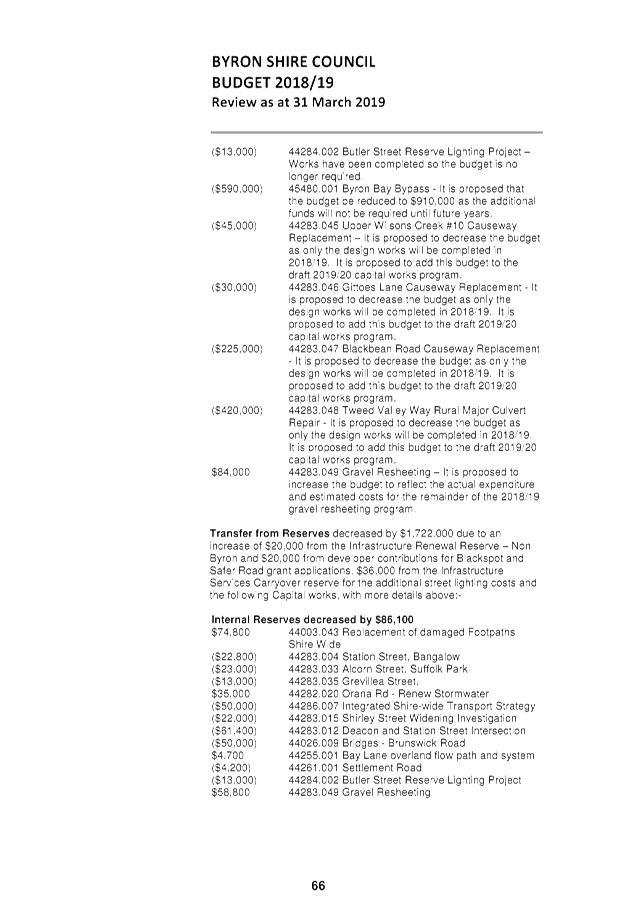

Drainage program, there are a number of adjustments outlined under Note 15 in

the Budget Variations explanations section of Attachment 1. Further

disclosure is included in the fifth and sixth pages of Attachment 2 under the

budget program heading Local Roads and Drainage.

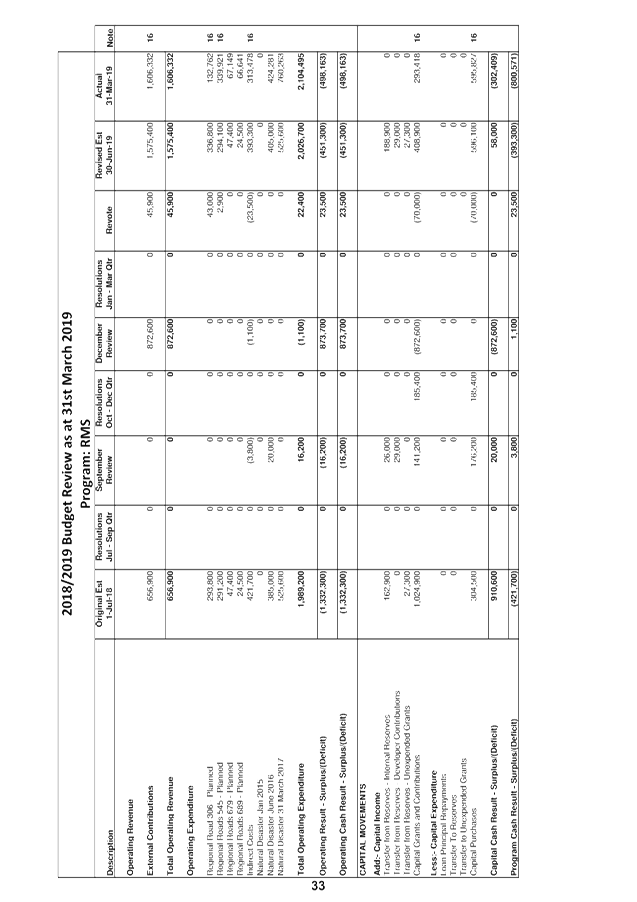

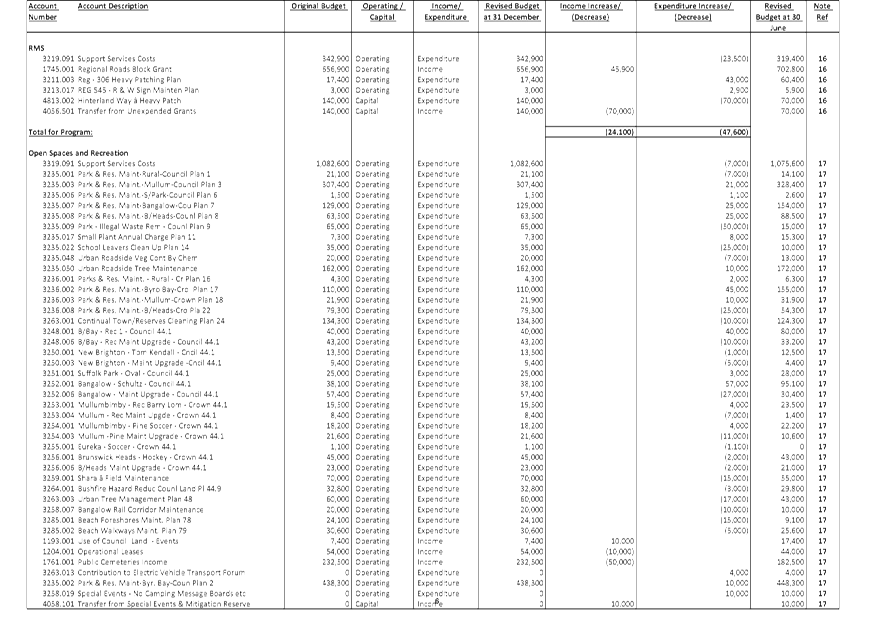

· In the Roads and

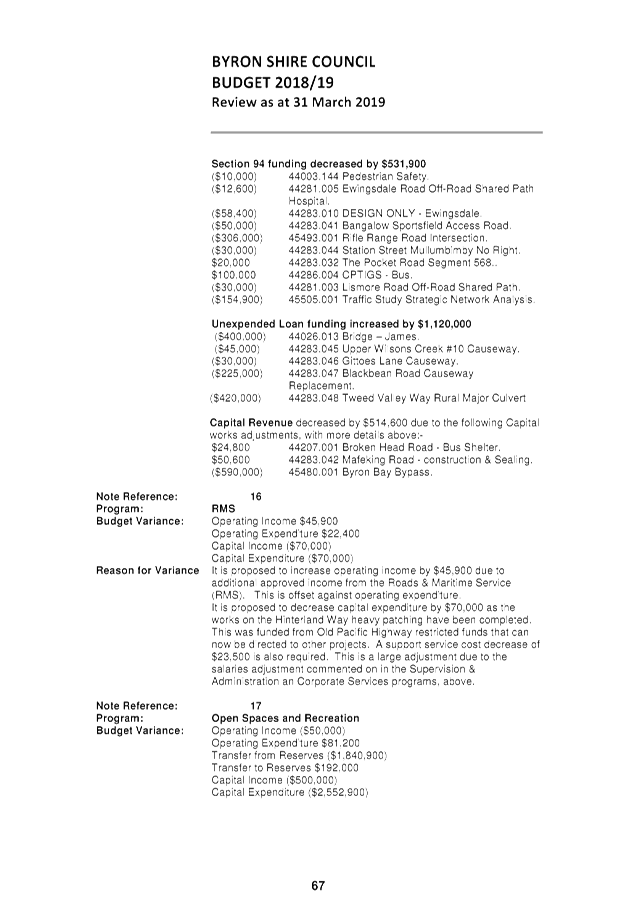

Maritime Services program (RMS), it is proposed to increase operating income

and expenditure by $45,900 to reflect the actual amount approved by the RMS for

the block grant and decrease the capital budget by $70,000 for the Hinterland

Way project that has been completed.

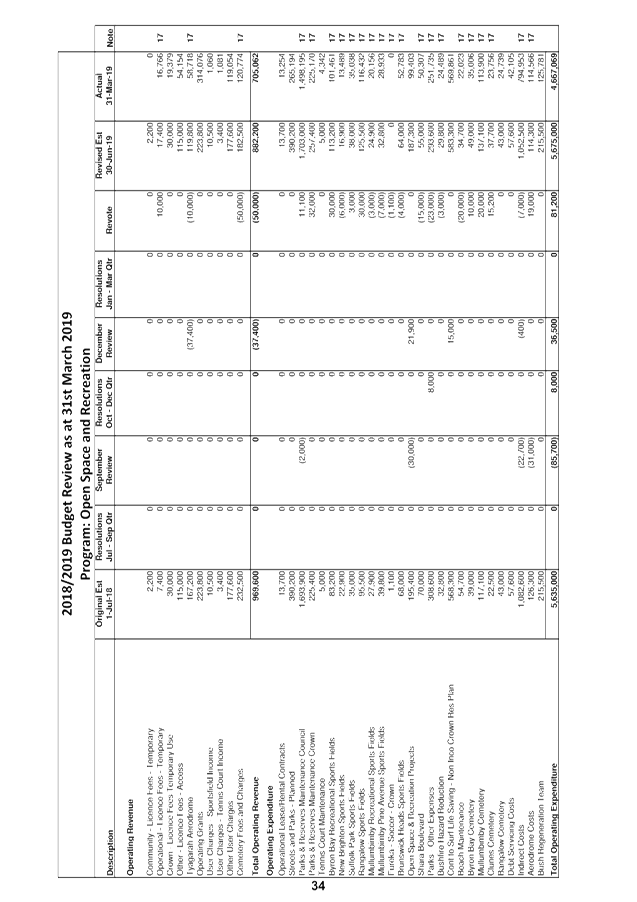

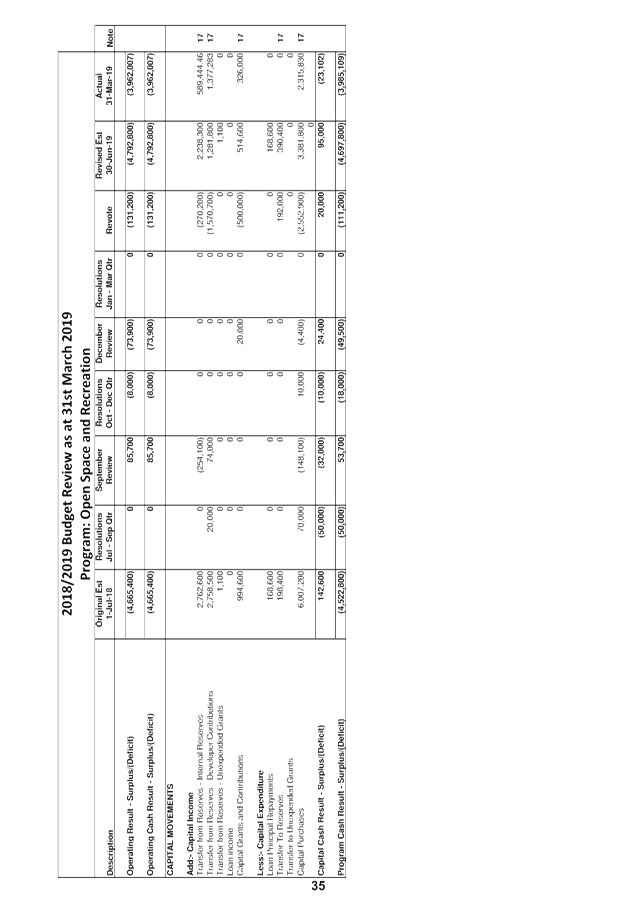

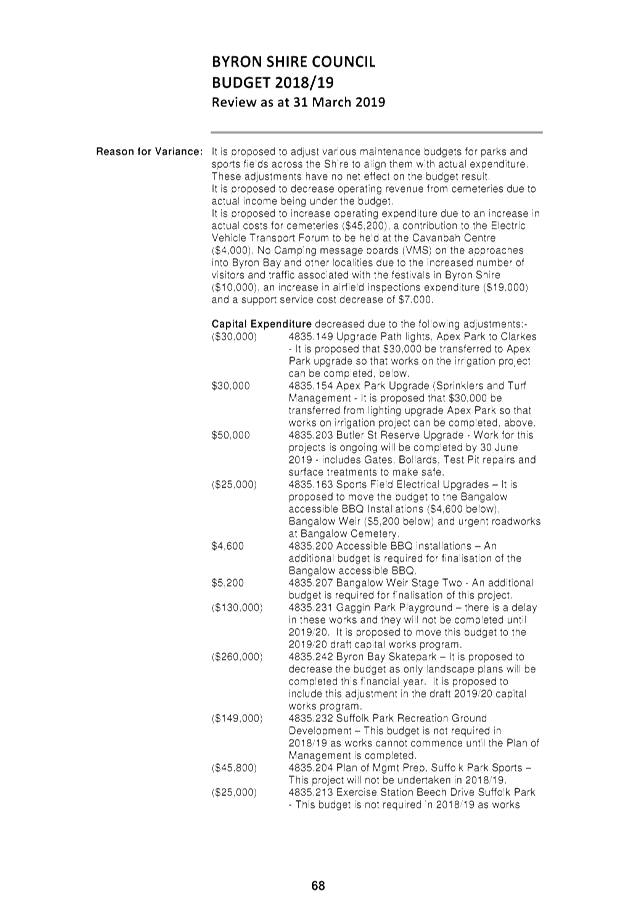

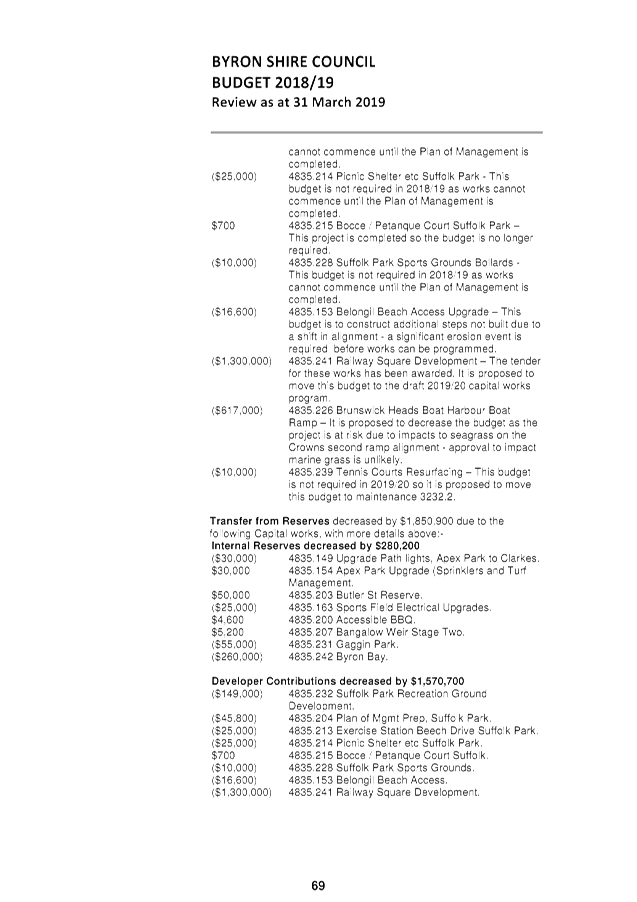

· In the Open Space and

Recreation program, there are a number of adjustments outlined under Note 17 in

the Budget Variations explanations section of Attachment 1. Further

disclosure is included in the eighth and ninth pages of Attachment 2 under the

budget program heading Open Space & Recreation.

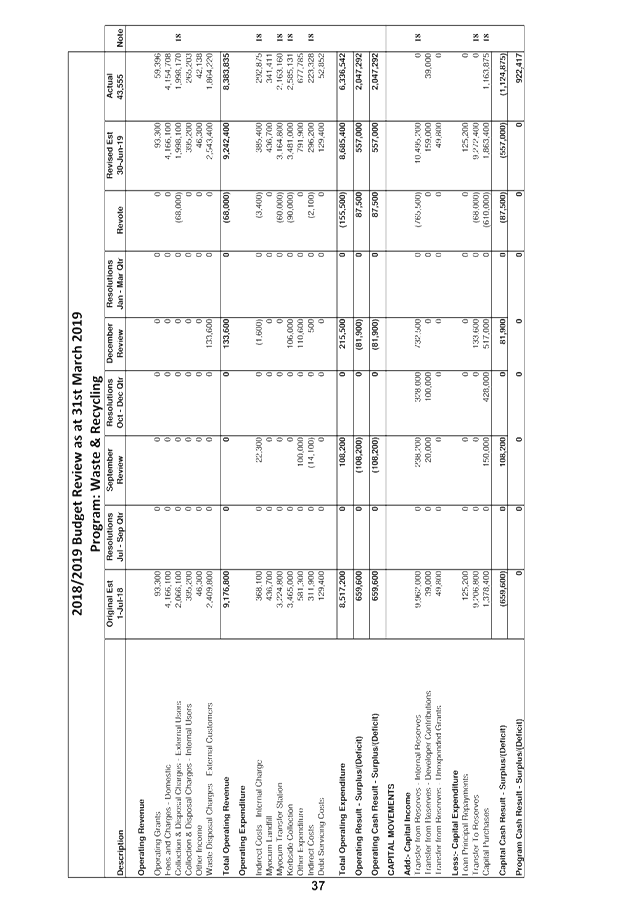

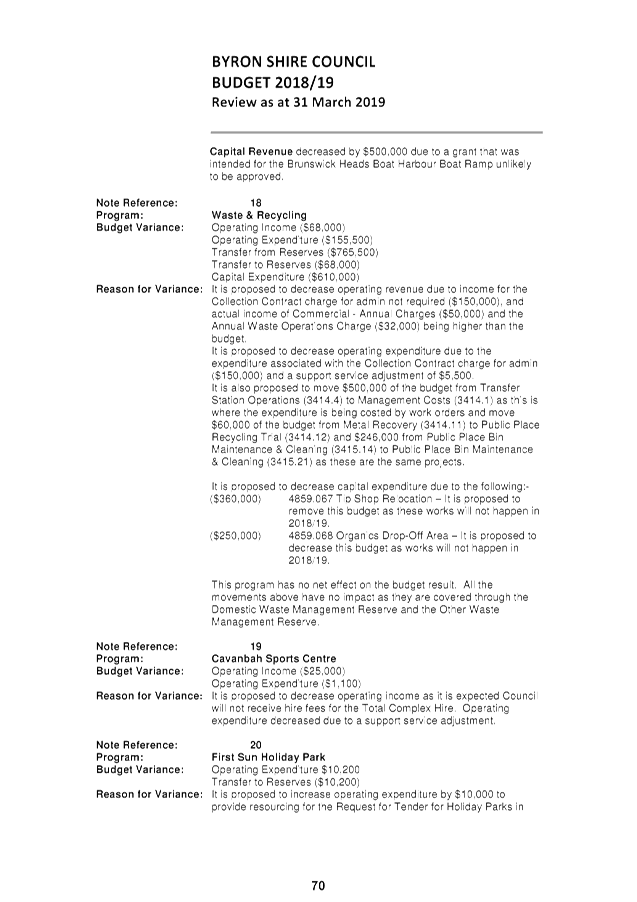

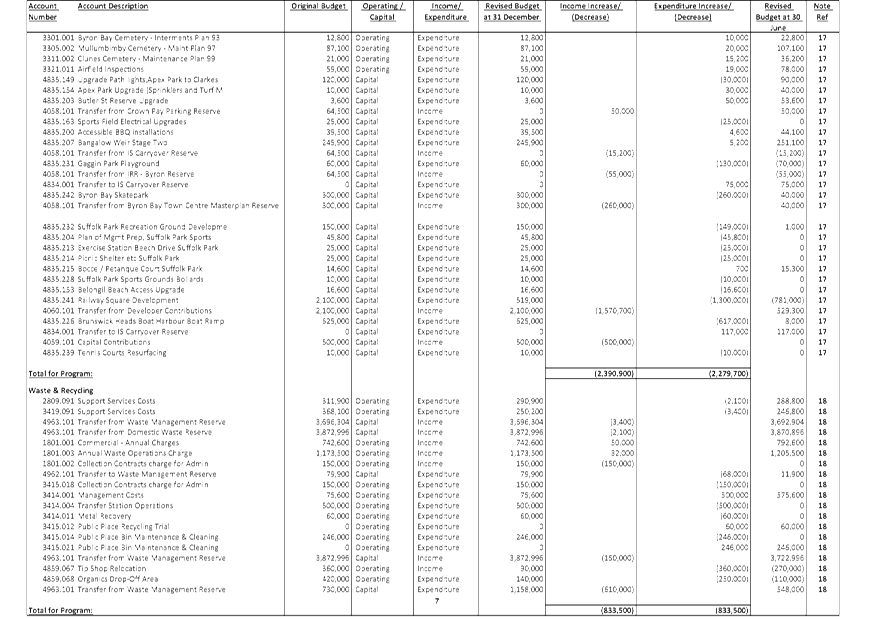

· In the Waste &

Recycling program, it is proposed to decrease operating revenue due to income

for the Collection Contract charge for administration not required ($150,000),

and actual income of Commercial - Annual Charges ($50,000) and the Annual Waste

Operations Charge ($32,000) being higher than the budget. It is proposed

to decrease operating expenditure due to the expenditure associated with the

Collection Contract charge for admin ($150,000) and a support service

adjustment of $5,500. It is proposed to decrease capital expenditure due to the

removal of the budget for the Tip Shop Relocation ($360,000) and the Organics

Drop-Off Area ($250,000) as these projects will not be completed in 2018/19.

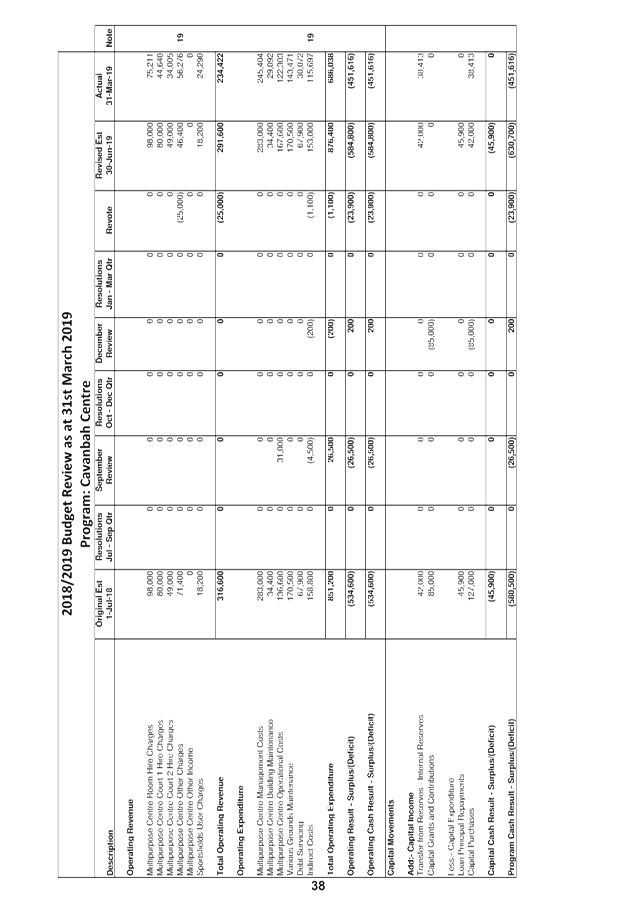

· In the Cavanbah Centre

program, it is proposed to decrease operating income by $25,000 for the Total

Complex Hire as this will not be received in 2018/19.

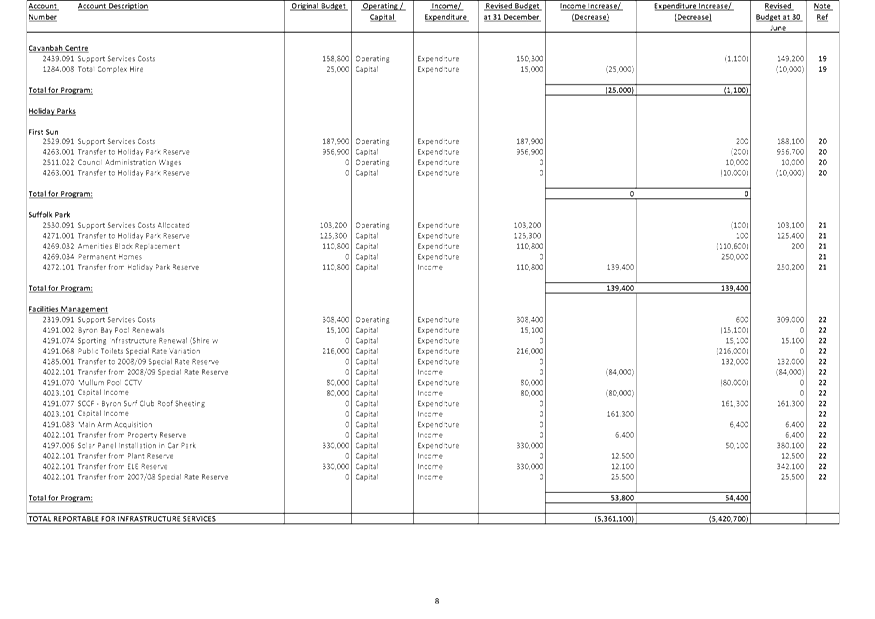

· In the Holiday Park

programs, it is proposed to create a budget of $10,000 to assist in the

upcoming tender for the Holiday Parks, remove the budget for the Amenities

Block replacement at Suffolk Park Holiday Park ($110,600), moving the budget to

2019/20 and creating a budget for the purchase of permanent sites at Suffolk

Park Holiday Park ($250,000) subject to a report to Council on 16 May 2019.

In the Facilities Management

program, it is proposed to decrease capital expenditure due to removing the

budget for Public Toilets ($216,000) as works are still in the planning stage

and the location of toilets is still to be determined, a decrease against the

Mullumbimby Pool CCTV project ($80,000) as the grant will not be received to

fund this project, an increase to the budget for the Byron Surf Club Roof

Sheeting ($161,300), a budget created for land acquired at Main Arm ($6,400)

and a budget increase for additional works related to the Solar Panel

Installation in the Council car park ($50,100).

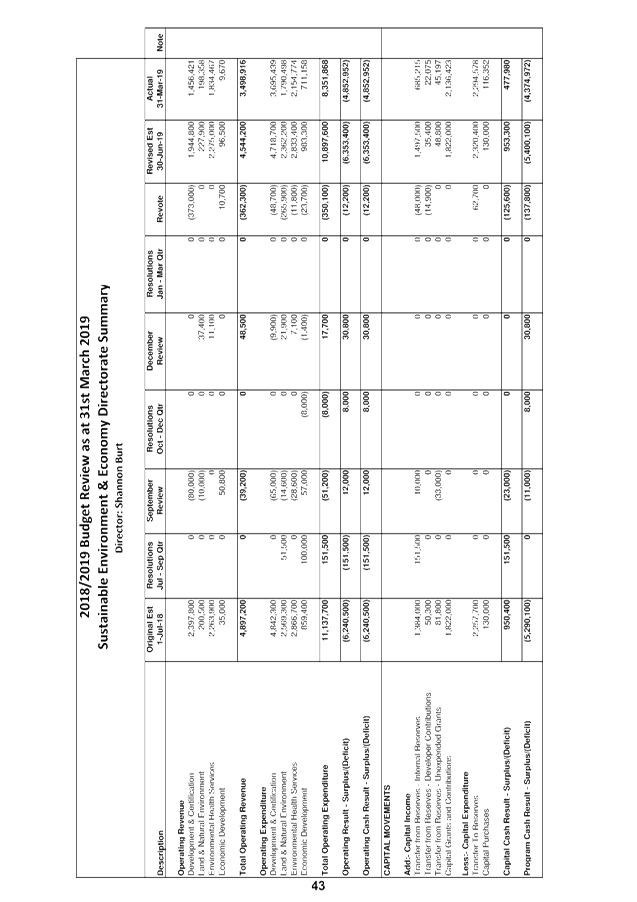

Sustainable Environment and Economy

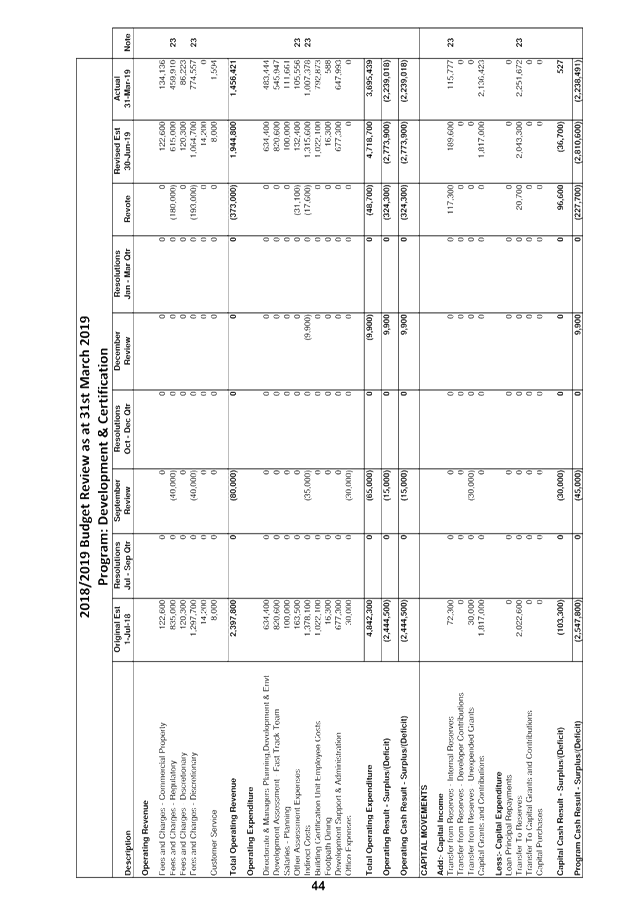

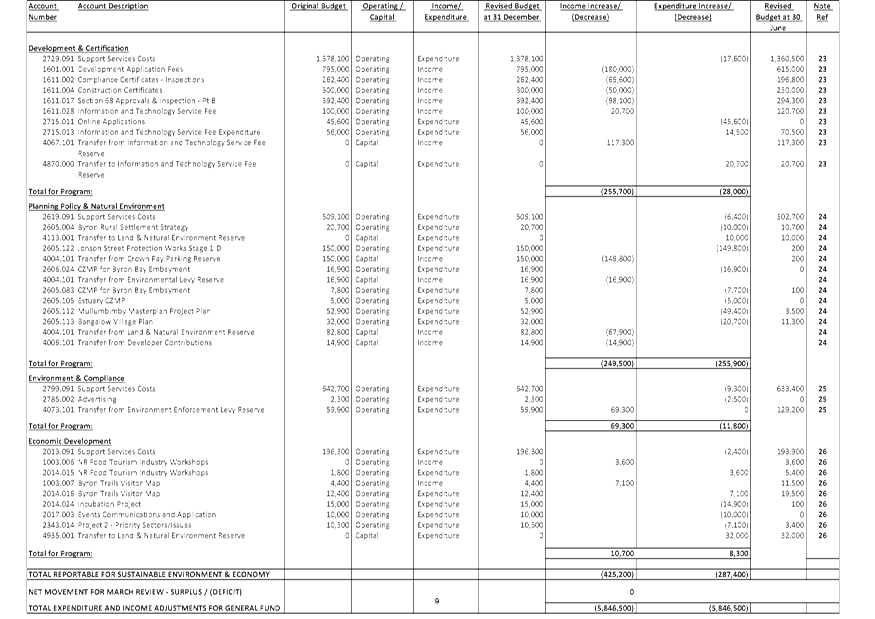

· In the Development and

Certification program, it is proposed to decrease income by $373,000 due to a

decline in income received for DA Fees ($180,000), Compliance Certificates

– Inspections ($65,600), Construction Certificates ($50,000), and Section

68 Approvals & Inspection - Pt B ($98,100) and an increase against actual

income received for the Information & Technology Service Fee. This is

largely due to a decrease in the number of Development Applications received

and the market share for Construction Certificates dropping with additional

providers offering this service. Some of the decrease to income can be

offset by a transfer from the Information & Technology Service Fee reserve

($117,300).

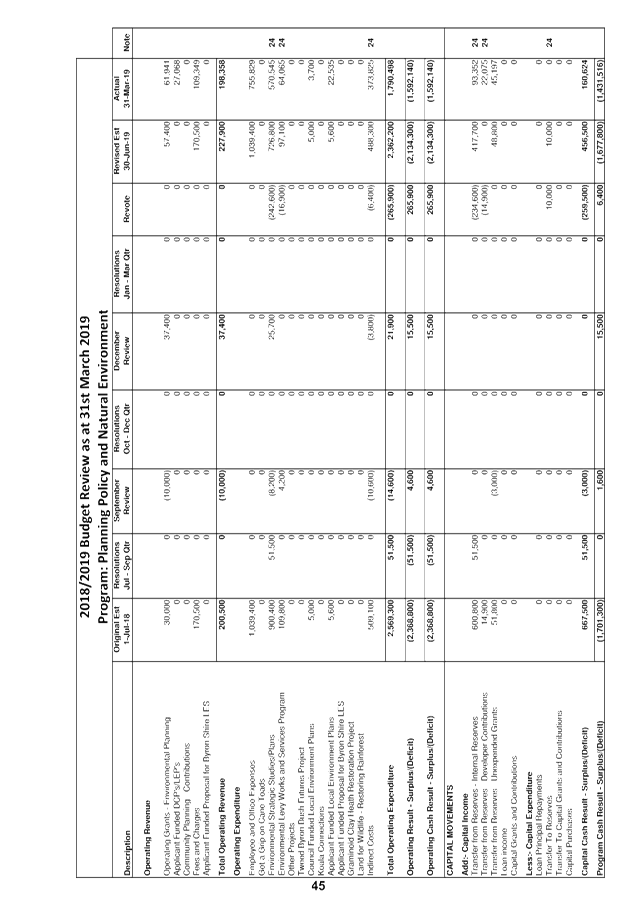

· In the Planning Policy

& Natural Environment program, it is proposed to decrease operating

expenditure due to the Jonson Street Protection Works Stage 1 ($149,800) and

the Bangalow Village Plan ($20,700) being moved to the draft 2019/20 budget and

the Byron Rural Settlement Strategy ($10,000), CZMP for Byron Bay Embayment

($24,600), Estuary CZMP ($5,000) and Mullumbimby Masterplan Project Plan

($49,400) being returned to reserves as the budgets are not required in

2018/19.

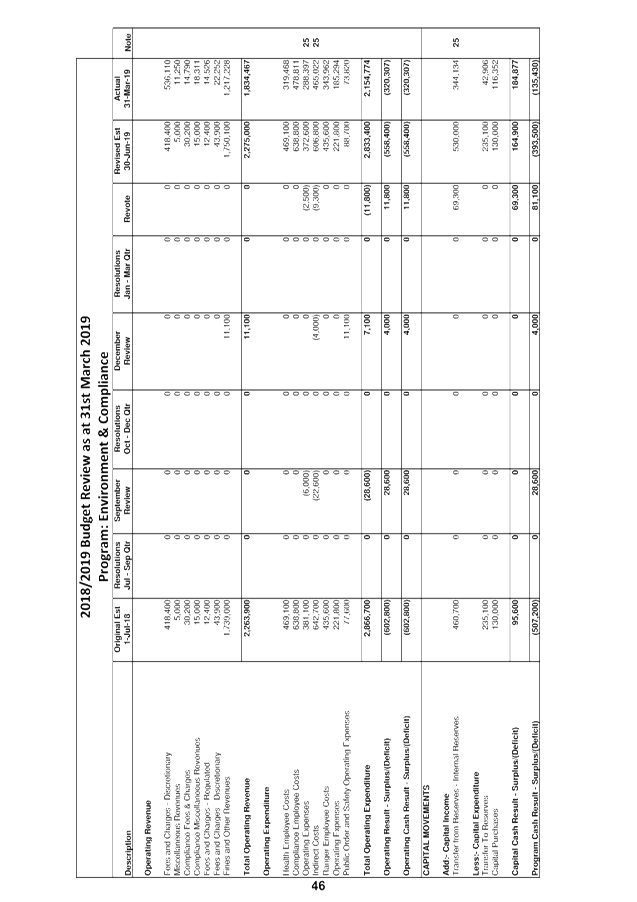

· In the Environment &

Compliance program, it is proposed to transfer $69,300 from the Environment

Enforcement Levy reserve to cover the decrease in income in the Development

& Certification program.

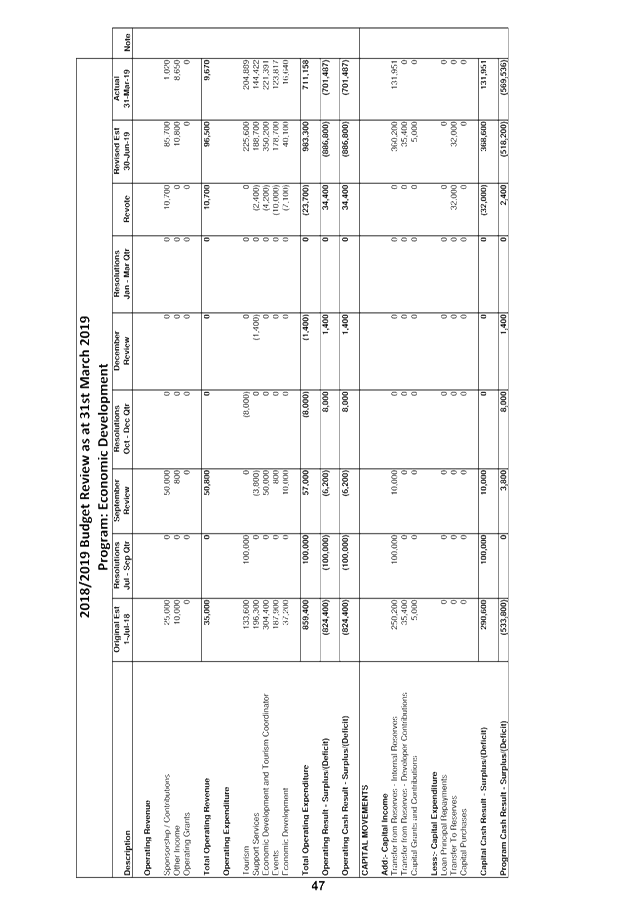

· In the Economic

Development program, it is proposed to increase operating income and

expenditure by $10,700 due to income received for NR Food Tourism Industry

Workshops ($3,600) and Byron Trails Visitor Map ($7,100). It is proposed to

decrease expenditure budgets for the Incubation Project ($14,900), Events

Communications and Applications ($10,000) and Project 2 - Priority

Sectors/Issues ($7,100) as these budgets are not required in 2018/19.

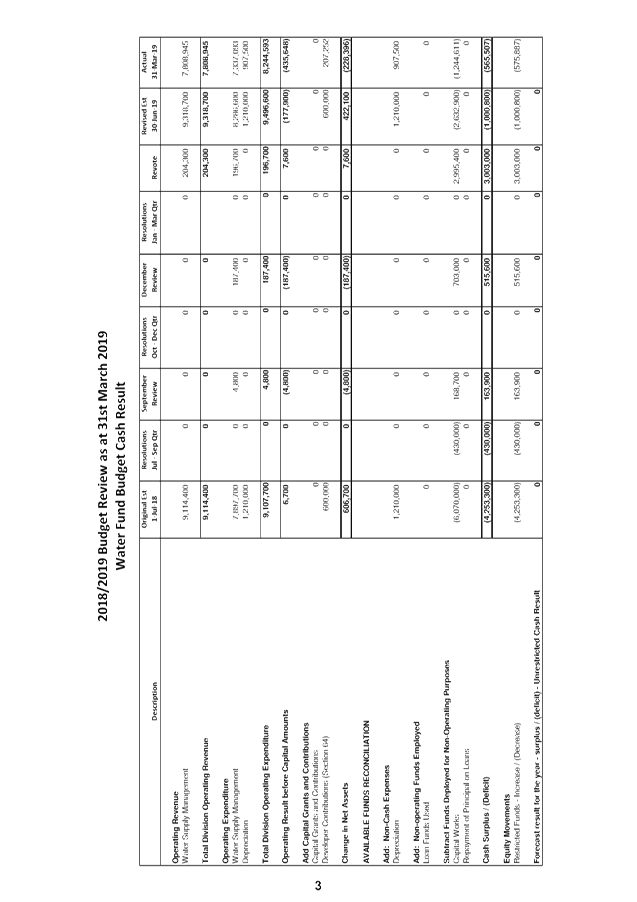

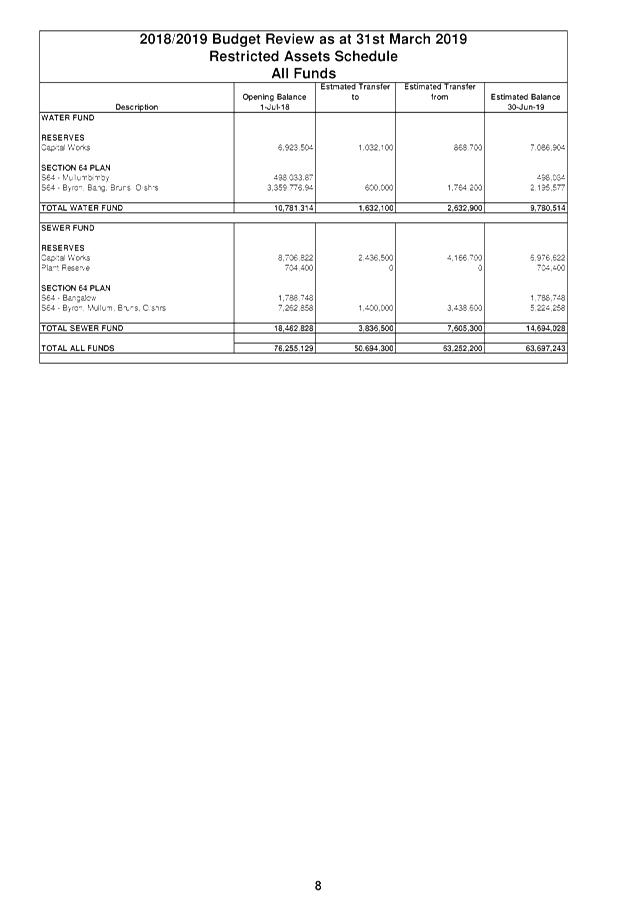

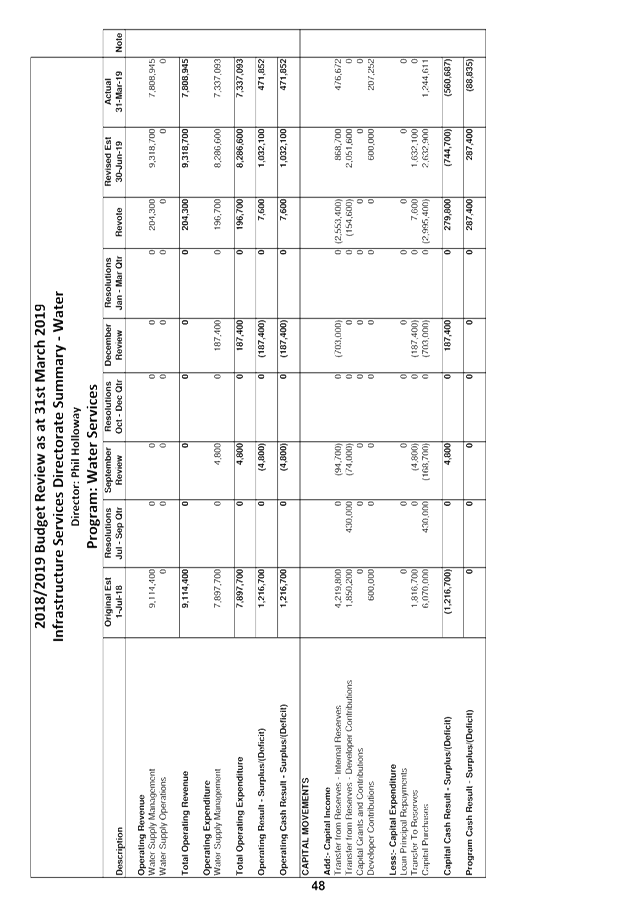

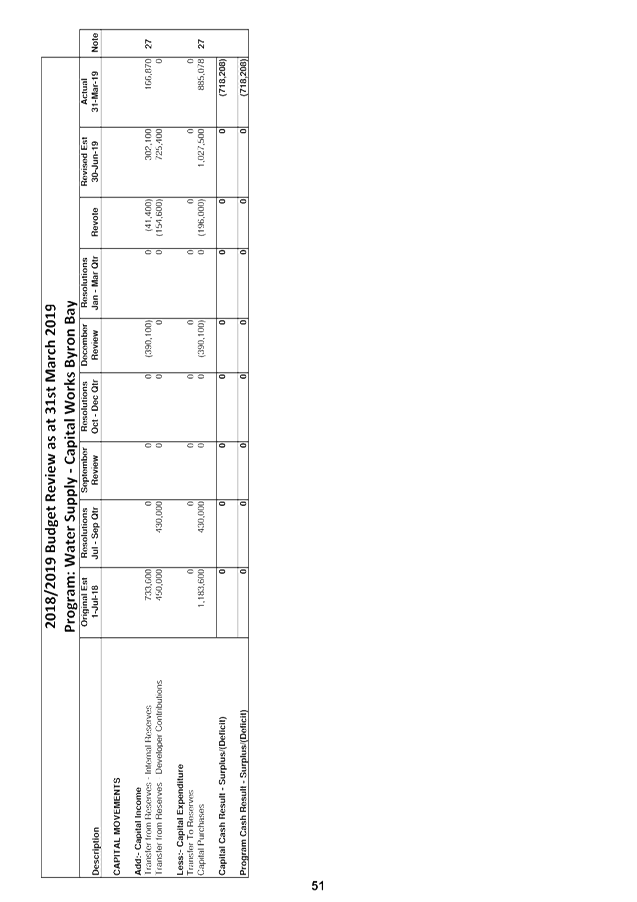

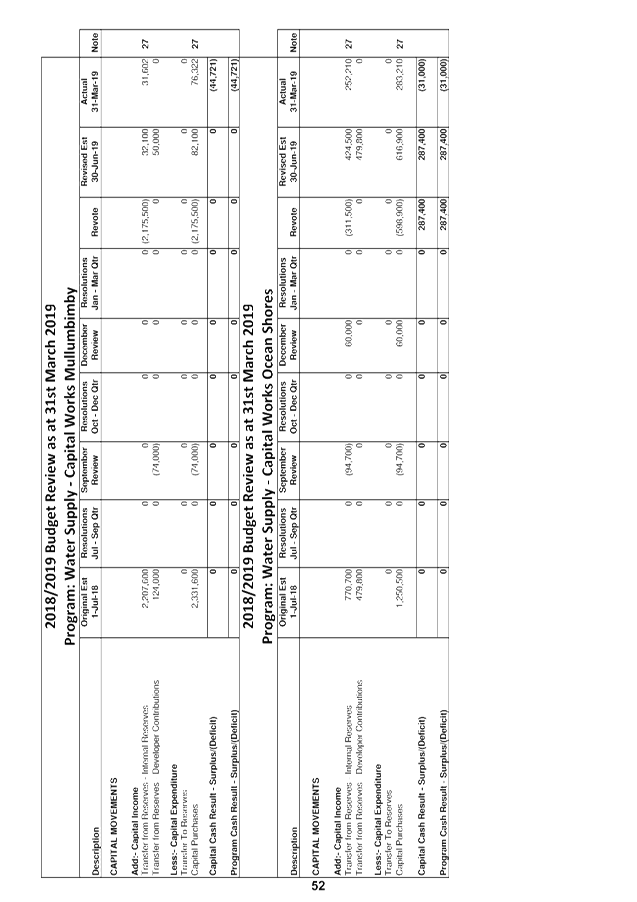

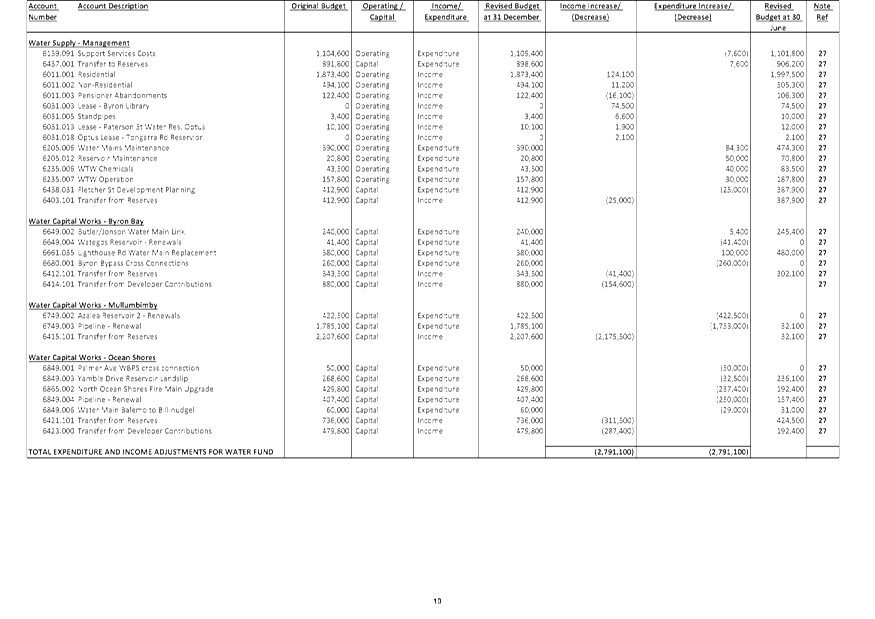

WATER FUND

After completion of the 2017/2018

Financial Statements the Water Fund as at 30 June 2018 had a capital works

reserve of $6,923,500 and held $3,857,800 in Section 64 developer

contributions.

The estimated Water Fund reserve

balances as at 30 June 2019, and forecast in this Quarter Budget Review, are

derived as follows:

Capital Works Reserve

|

Opening Reserve Balance at 1

July 2018

|

$6,923,500

|

|

Plus original budget reserve

movement

|

(2,627,400)

|

|

Less reserve funded carryovers

from 2017/2018

|

(375,700)

|

|

Resolutions July -

September Quarter – increase / (decrease)

|

0

|

|

September Quarterly Review

Adjustments – increase / (decrease)

|

89,900

|

|

Resolutions October -

December Quarter – increase / (decrease)

|

0

|

|

December Quarterly Review

Adjustments – increase / (decrease)

|

515,600

|

|

Resolutions January -

March Quarter – increase / (decrease)

|

0

|

|

March Quarterly Review

Adjustments – increase / (decrease)

|

2,561,000

|

|

Forecast Reserve Movement for

2018/2019 – Increase / (Decrease)

|

163,400

|

|

Estimated Reserve Balance at

30 June 2019

|

$7,086,900

|

Section 64 Developer

Contributions

|

Opening Reserve Balance at 1

July 2018

|

$3,857,800

|

|

Plus original budget reserve

movement

|

(746,400)

|

|

Less reserve funded carryovers

from 2017/2018

|

(503,800)

|

|

Resolutions July -

September Quarter – increase / (decrease)

|

(430,000)

|

|

September Quarterly Review

Adjustments – increase / (decrease)

|

74,000

|

|

Resolutions October -

December Quarter – increase / (decrease)

|

0

|

|

December Quarterly Review

Adjustments – increase / (decrease)

|

0

|

|

Resolutions January -

March Quarter – increase / (decrease)

|

0

|

|

March Quarterly Review

Adjustments – increase / (decrease)

|

442,000

|

|

Forecast Reserve Movement for

2018/2019 – Increase / (Decrease)

|

(1,164,200)

|

|

Estimated Reserve Balance at

30 June 2019

|

$2,693,600

|

Movements for Water Fund can be seen in Attachment 1 with a

proposed estimated increase to reserves (including S64 Contributions) overall

of $3,003,000 from the 31 March 2019 Quarter Budget Review.

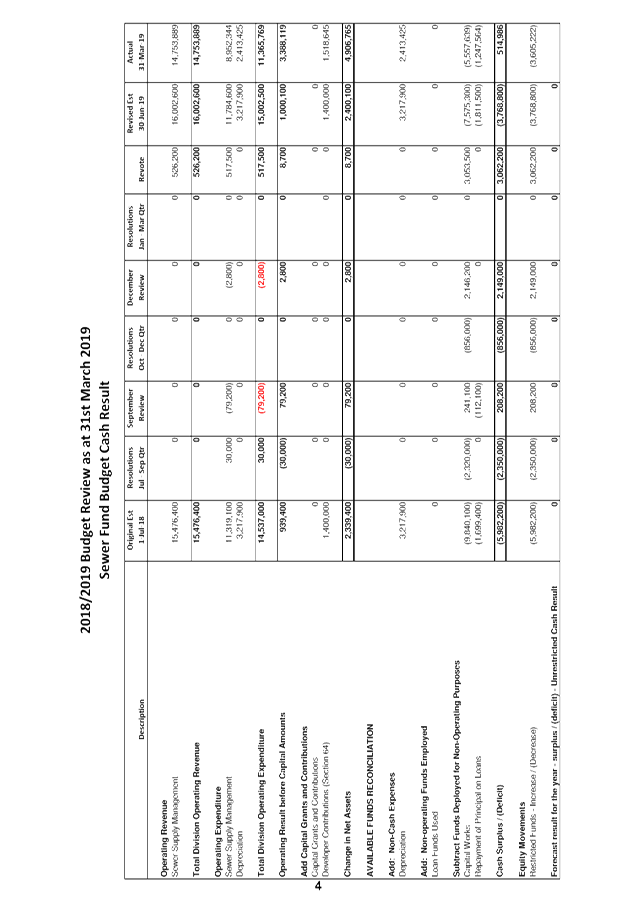

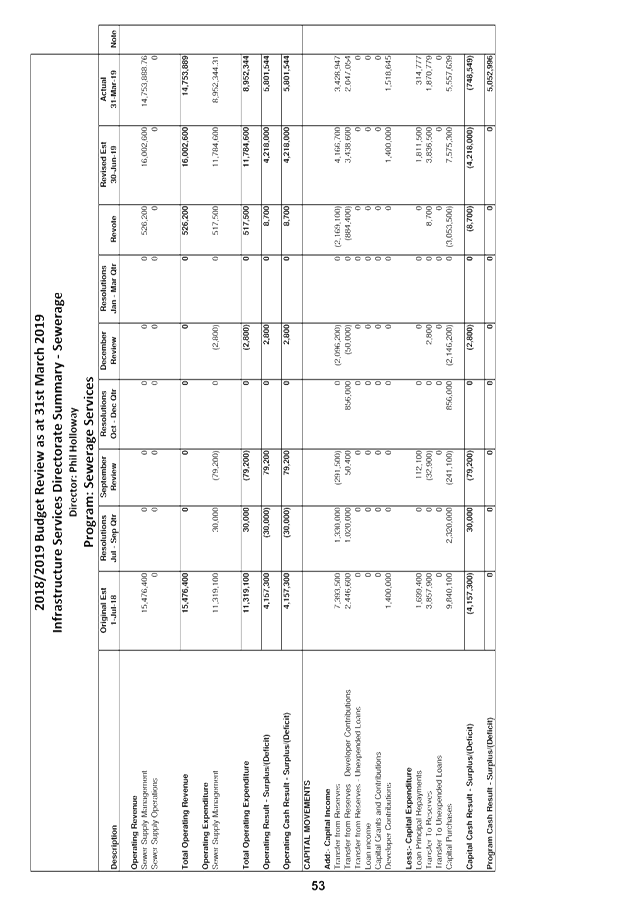

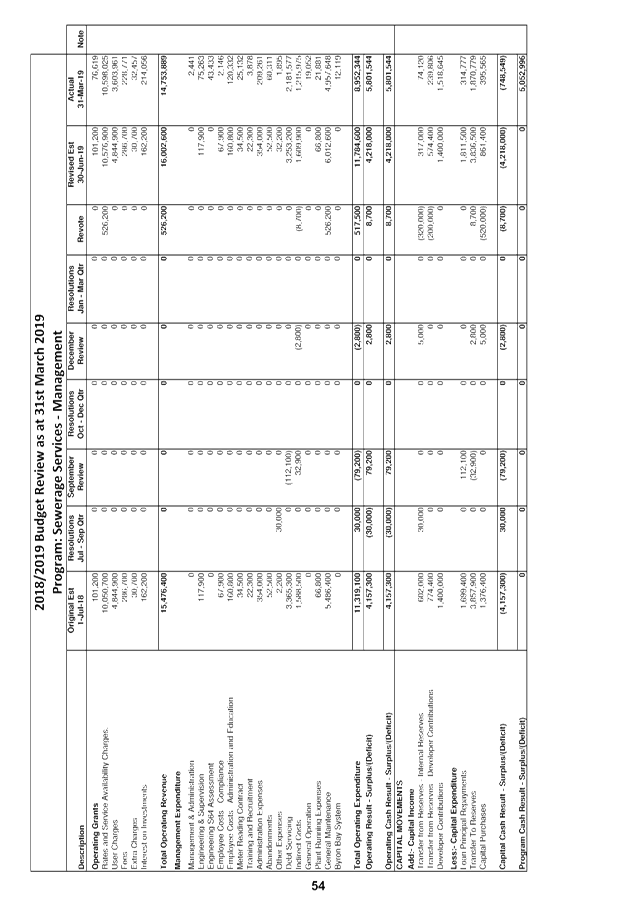

SEWERAGE FUND

After completion of the 2017/2018

Financial Statements the Sewer Fund as at 30 June 2018 had a capital works

reserve of $8,706,800 and plant reserve of $704,400. It also held

$9,051,600 in section 64 developer contributions.

Capital Works Reserve

|

Opening Reserve Balance at 1

July 2018

|

$8,706,800

|

|

Plus original budget reserve

movement

|

(3,480,800)

|

|

Less reserve funded carryovers

from 2017/2018

|

(1,454,800)

|

|

Resolutions July -

September Quarter – increase / (decrease)

|

(1,330,000)

|

|

September Quarterly Review

Adjustments – increase / (decrease)

|

258,600

|

|

Resolutions October -

December Quarter – increase / (decrease)

|

0

|

|

December Quarterly Review

Adjustments – increase / (decrease)

|

2,099,000

|

|

Resolutions January -

March Quarter – increase / (decrease)

|

0

|

|

March Quarterly Review

Adjustments – increase / (decrease)

|

2,177,800

|

|

Forecast Reserve Movement for

2018/2019 – Increase / (Decrease)

|

(1,730,200)

|

|

Estimated Reserve Balance at

30 June 2019

|

$6,976,600

|

Plant Reserve

|

Opening Reserve Balance at 1 July

2018

|

$704,400

|

|

Plus original budget reserve

movement

|

0

|

|

Less reserve funded carryovers

from 2017/2018

|

0

|

|

Resolutions July -

September Quarter – increase / (decrease)

|

0

|

|

September Quarterly Review

Adjustments – increase / (decrease)

|

0

|

|

Resolutions October -

December Quarter – increase / (decrease)

|

0

|

|

December Quarterly Review

Adjustments – increase / (decrease)

|

0

|

|

Resolutions January -

March Quarter – increase / (decrease)

|

0

|

|

March Quarterly Review

Adjustments – increase / (decrease)

|

0

|

|

Forecast Reserve Movement for

2018/2019 – Increase / (Decrease)

|

0

|

|

Estimated Reserve Balance at

30 June 2019

|

$704,400

|

Section 64 Developer

Contributions

|

Opening Reserve Balance at 1

July 2018

|

$9,051,600

|

|

Plus original budget reserve

movement

|

(27,900)

|

|

Less reserve funded carryovers

from 2017/2018

|

(1,018,700)

|

|

Resolutions July -

September Quarter – increase / (decrease)

|

(1,020,000)

|

|

September Quarterly Review

Adjustments – increase / (decrease)

|

(50,400)

|

|

Resolutions October -

December Quarter – increase / (decrease)

|

(856,000)

|

|

December Quarterly Review

Adjustments – increase / (decrease)

|

50,000

|

|

Resolutions January -

March Quarter – increase / (decrease)

|

0

|

|

March Quarterly Review

Adjustments – increase / (decrease)

|

884,400

|

|

Forecast Reserve Movement for

2018/2019 – Increase / (Decrease)

|

(2,038,600)

|

|

Estimated Reserve Balance at

30 June 2019

|

$7,013,000

|

Movements for the Sewerage Fund can be seen in Attachment 1

with a proposed estimated overall increase to reserves (including S64

Contributions) of $3,062,200 from the 31 March 2019 Quarter Budget Review.

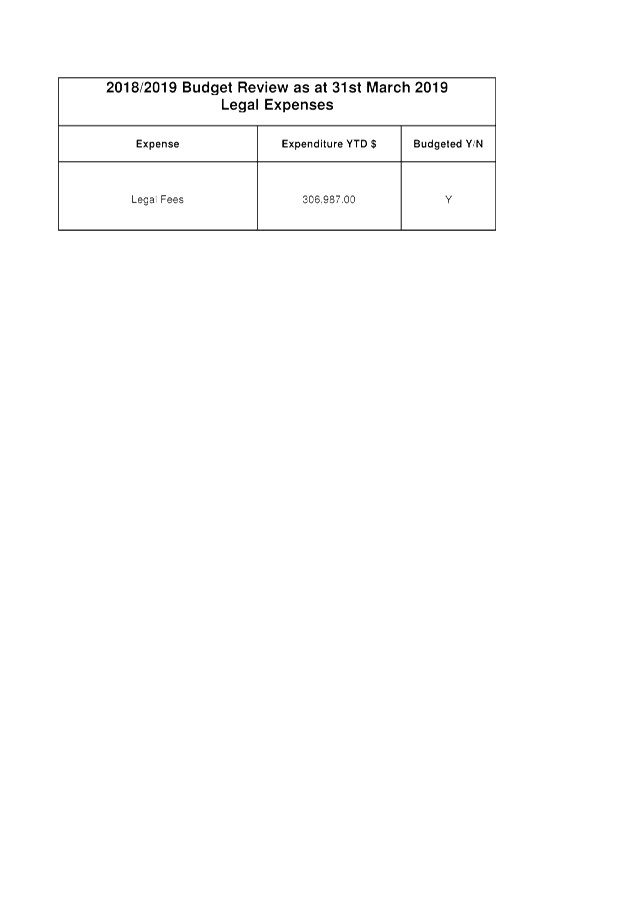

Legal Expenses

One of the major financial concerns for Council over

previous years has been legal expenses. Not only does this item represent a

large expenditure item funded by general revenue, but it can also be

susceptible to large fluctuations.

The table that follows indicates the allocated budget and

actual legal expenditure within Council on

a fund basis as at 31 March 2019.

Total Legal Income & Expenditure as at 31 March 2019

|

Program

|

2018/2019

Budget ($)

|

Actual ($)

|

Percentage To

Revised Budget

|

|

Income

|

|

|

|

|

Legal Expenses Recovered

|

4,000

|

4,000

|

100%

|

|

Total Income

|

4,000

|

4,000

|

100%

|

|

|

|

|

|

|

Expenditure

|

|

|

|

|

General Legal Expenses

|

306,600

|

306,987

|

100.13%

|

|

Total Expenditure General Fund

|

306,600

|

306,987

|

100.13%

|

Note: The above table does not include costs incurred

by Council in proceedings after 31 March 2019 or billed after this date. At the

time of writing this report, Council has incurred an additional $35,804 of

expenditure in April 2019 with a further commitment of $9,124. It is proposed

to transfer an additional $126,600 from the Legal Services Reserve within this

review to cover additional legal expenses expected this financial year. This

increase in expenditure will fully deplete the legal services reserve. Council

will need to address the funding for the legal services reserve.

STRATEGIC CONSIDERATIONS

Community Strategic Plan and Operational Plan

|

CSP Objective

|

L2

|

CSP Strategy

|

L3

|

DP Action

|

L4

|

OP Activity

|

|

Community

Objective 5: We have community led decision making which is open and

inclusive

|

5.5

|

Manage

Council’s finances sustainably

|

5.5.1

|

Enhance the

financial capability and acumen of Council

|

5.5.1.1

|

Financial

reporting as required provided to Council and Management

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Legal/Statutory/Policy Considerations

In accordance with Regulation 203

of the Local Government (General) Regulation 2005 the Responsible Accounting

Officer of a Council must:-

(1) Not later than 2 months after the end of each quarter

(except the June quarter), the responsible accounting officer of a council must prepare and submit to the council a budget review statement that shows, by

reference to the estimate of income and expenditure set out in the statement of

the council’s revenue policy included in the operational plan for the

relevant year, a revised estimate of the income and expenditure for that year.

(2) A budget review statement must include or be

accompanied by:

(a) a report as to whether or not the responsible

accounting officer believes that the statement indicates that the financial

position of the council is satisfactory, having regard to the original estimate

of income and expenditure, and

(b) if that position is unsatisfactory, recommendations

for remedial action.

(3) A budget review statement must also include any

information required by the Code to be included in such a statement.

Financial

Considerations

This report indicates that the short term financial position

of the Council is still satisfactory for the 2018/2019 financial year, having

consideration of the original estimate of income and expenditure at the 31

March 2019 Quarter Budget Review.

This opinion is based on the estimated General Fund

Unrestricted Cash Result position and that the current indicative budget

position for 2018/2019 outlined in this Budget Review remains for the remainder

of the 2018/2019 financial year.

It is also again noted that Council will need to address the

current level of the Legal Services Reserve which will be fully depleted if

adjustments within this review are actioned.