What is a “Conflict of Interests” - A conflict of

interests can be of two types:

Pecuniary - an interest that a person has in a matter because of a reasonable

likelihood or expectation of appreciable financial gain or loss to the person

or another person with whom the person is associated.

Non-pecuniary – a private or personal interest that a Council

official has that does not amount to a pecuniary interest as defined in the Code

of Conduct for Councillors (eg. A friendship, membership of an association,

society or trade union or involvement or interest in an activity and may

include an interest of a financial nature).

Remoteness – a person does not have a pecuniary interest in a matter

if the interest is so remote or insignificant that it could not reasonably be

regarded as likely to influence any decision the person might make in relation

to a matter or if the interest is of a kind specified in the Code of Conduct

for Councillors.

Who has a Pecuniary Interest? - a person has a pecuniary interest in a

matter if the pecuniary interest is the interest of the person, or another

person with whom the person is associated (see below).

Relatives, Partners - a person is taken to have a pecuniary interest in a

matter if:

§ The person’s

spouse or de facto partner or a relative of the person has a pecuniary interest

in the matter, or

§ The person, or a

nominee, partners or employer of the person, is a member of a company or other

body that has a pecuniary interest in the matter.

N.B. “Relative”, in relation to a person means any of the

following:

(a) the

parent, grandparent, brother, sister, uncle, aunt, nephew, niece, lineal

descends or adopted child of the person or of the person’s spouse;

(b) the

spouse or de facto partners of the person or of a person referred to in

paragraph (a)

No Interest in the Matter - however, a person is not taken to have a

pecuniary interest in a matter:

§ If the person is

unaware of the relevant pecuniary interest of the spouse, de facto partner,

relative or company or other body, or

§ Just because the

person is a member of, or is employed by, the Council.

§ Just because the

person is a member of, or a delegate of the Council to, a company or other body

that has a pecuniary interest in the matter provided that the person has no

beneficial interest in any shares of the company or body.

Disclosure and participation in meetings

§ A Councillor or a

member of a Council Committee who has a pecuniary interest in any matter with

which the Council is concerned and who is present at a meeting of the Council

or Committee at which the matter is being considered must disclose the nature

of the interest to the meeting as soon as practicable.

§ The Councillor or

member must not be present at, or in sight of, the meeting of the Council or

Committee:

(a) at any

time during which the matter is being considered or discussed by the Council or

Committee, or

(b) at any

time during which the Council or Committee is voting on any question in

relation to the matter.

No Knowledge - a person does not breach this Clause if the person did

not know and could not reasonably be expected to have known that the matter

under consideration at the meeting was a matter in which he or she had a

pecuniary interest.

Non-pecuniary Interests - Must be disclosed in meetings.

There are a broad range of options available for managing conflicts &

the option chosen will depend on an assessment of the circumstances of the

matter, the nature of the interest and the significance of the issue being

dealt with. Non-pecuniary conflicts of interests must be dealt with in at

least one of the following ways:

§ It may be appropriate

that no action be taken where the potential for conflict is minimal.

However, Councillors should consider providing an explanation of why they

consider a conflict does not exist.

§ Limit involvement if

practical (eg. Participate in discussion but not in decision making or vice-versa).

Care needs to be taken when exercising this option.

§ Remove the source of

the conflict (eg. Relinquishing or divesting the personal interest that creates

the conflict)

§ Have no involvement by

absenting yourself from and not taking part in any debate or voting on the

issue as of the provisions in the Code of Conduct (particularly if you have a significant

non-pecuniary interest)

RECORDING OF VOTING ON PLANNING MATTERS

Clause 375A of the Local Government Act 1993

– Recording of voting on planning matters

(1) In this section, planning

decision means a decision made in the exercise of a function of a council

under the Environmental Planning and Assessment Act 1979:

(a) including a decision

relating to a development application, an environmental planning instrument, a

development control plan or a development contribution plan under that Act, but

(b) not including the making of

an order under that Act.

(2) The general manager is

required to keep a register containing, for each planning decision made at a

meeting of the council or a council committee, the names of the councillors who

supported the decision and the names of any councillors who opposed (or are

taken to have opposed) the decision.

(3) For the purpose of

maintaining the register, a division is required to be called whenever a motion

for a planning decision is put at a meeting of the council or a council

committee.

(4) Each decision recorded in

the register is to be described in the register or identified in a manner that

enables the description to be obtained from another publicly available

document, and is to include the information required by the regulations.

(5) This section extends to a

meeting that is closed to the public.

Late Reports 14.1

Late Reports

Report

No. 14.1 Draft

2018/2019 Financial Statements

Directorate: Corporate

and Community Services

Report

Author: James

Brickley, Manager Finance

File No: I2019/1613

Summary:

The Draft 2018/2019 Financial Statements have been prepared

and been subjected to external audit. This report recommends to Council

the adoption of the Draft 2018/2019 Financial Statements and the completion of

the statutory steps outlined in Section 418 to 420 of the Local Government Act

1993.

The External Auditor, being the NSW Auditor General

(represented by a Director of Financial Audit from the NSW Audit Office) or

their representative firm Thomas Noble and Russell have been invited to this

Ordinary Council Meeting, to present on the Draft 2018/2019 Financial

Statements, and answer any questions from Councillors on the Financial

Statements.

|

RECOMMENDATION:

1. That

Council adopts the Draft 2018/2019 Financial Statements incorporating the

General Purpose Financial Statements and Special Purpose Financial

Statements.

2. That

Council approves the signing of the “Statement by Councillors and

Management” in accordance with Section 413(2)(c) of the Local

Government Act 1993 and Clause 215 of the Local Government (General)

Regulation 2005 in relation to the 2018/2019 Draft Financial Statements.

3. That

Council exhibits the Financial Statements and Auditor’s Report and

calls for public submissions on those documents with submissions closing on 5

December 2019 in accordance with Section 420 of the Local Government Act

1993.

4. That the Audited

Financial Statements and Auditors Report be presented to the public at

the Ordinary Meeting of Council scheduled for 28 November 2019 in accordance with

Section 418(1) of the Local Government Act 1993.

|

Attachments:

1 Draft

2018-2019 General Purpose Financial Statements, E2019/76834 , page 12⇩

2 Draft

2018-2019 Special Purpose Financial Reports, E2019/76833

, page 97⇩

3 Draft

Byron Shire Council Conduct of the Audit Report 2019, E2019/76920 , page 110⇩

4 Draft

Byron Shire Council Audit Report 2019, E2019/76966

, page 116⇩

REPORT

The purpose of this report is to recommend the adoption and

exhibition of the Financial Statements for the year ended 30 June 2019. The

Financial Statements presented to Council for the financial year ended 30 June

2019 (refer to Attachments 1 to 4) are the final audited results and include

the Auditor’s Report. Council has received an unmodified audit

opinion for the 2018/2019 financial year.

The Draft 2018/2019 Financial Statements were to be

considered by the Audit, Risk and Improvement Committee on 10 October 2019 but

as the audit was not finalised by this date the Meeting was cancelled. The

Audit, Risk and Improvement Committee is meeting on 14 November 2019 and it

will consider the Financial Statements prior to Council Meeting to be held on

28 November 2019.

The External Auditor, being the Audit Office of NSW or

someone from their representative firm, Thomas Noble and Russell has been

invited to this Ordinary Council Meeting, to present on the Draft 2018/2019

Financial Statements, and answer any questions from Councillors.

The Financial Statements and Auditor’s Reports are a

statutory requirement and provide information on the financial performance of

Council over the previous twelve-month period.

The Draft 2018/2019 Financial Statements provided in the

attachments are broken down into:

- General

Purpose Financial Statements – Attachment 1

- Special

Purpose Financial Statements – Attachment 2

In previous years, Council also produced Special Schedules

that were not audited, however from the 2018/2019 financial year, whilst the

Special Schedules are still produced and submitted to the Office of Local

Government, they are no longer required to be published as part of Council’s

Financial Statements.

Brief explanations for each item follow:

General Purpose Financial

Statements

These Statements provide an overview of the operating result, financial

position, changes in equity and cash flow movement of Council as at 30 June

2019 on a consolidated basis with internal transactions between Council’s

General, Water and Sewerage Funds eliminated. The notes included within these

reports provide details of major items of income and expenditure with

comparisons to the previous financial year. The notes also highlight the cash

position of Council and indicate which funds are externally restricted (i.e.

may be used for a specific purpose only), and those that may be used at

Council’s discretion.

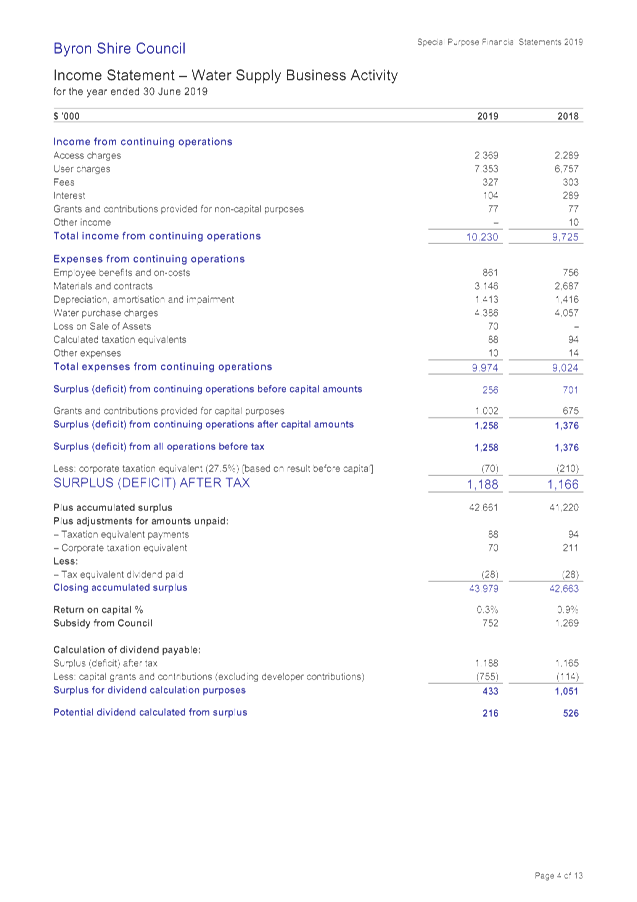

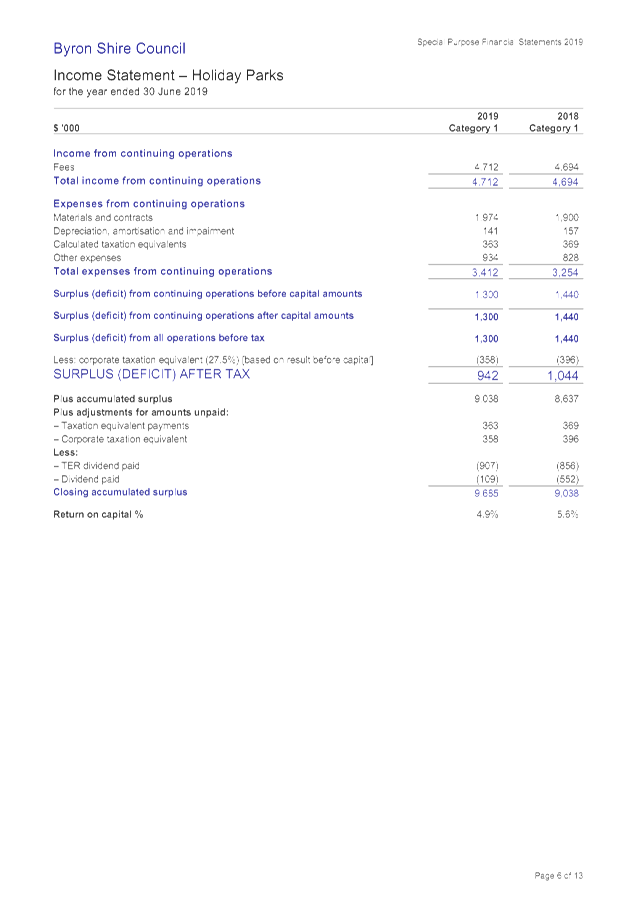

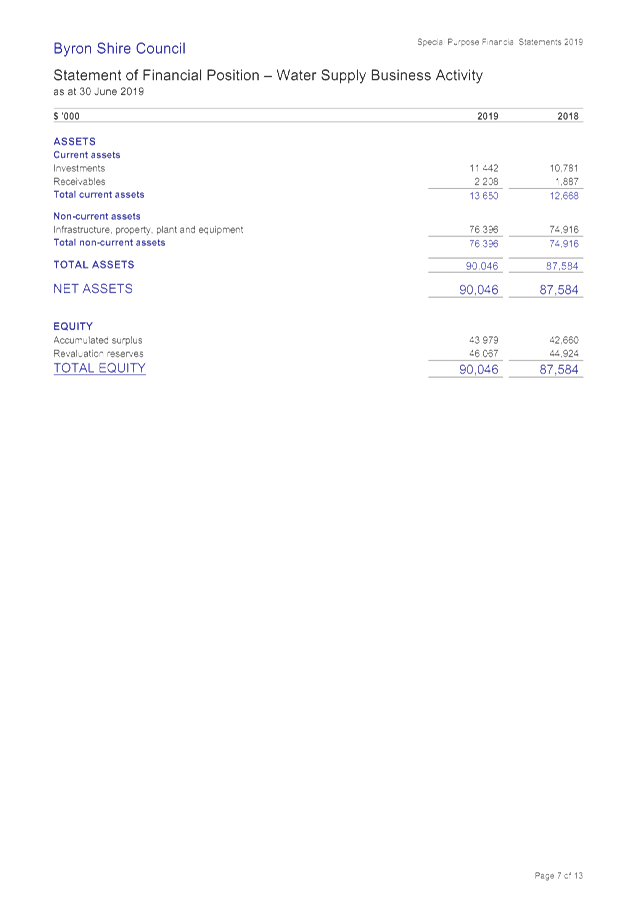

Special Purpose Financial Statements

These Statements are a result of the implementation of the National

Competition Policy and relate to those aspects of Council’s operations

that are business oriented and compete with other businesses with similar

operations.

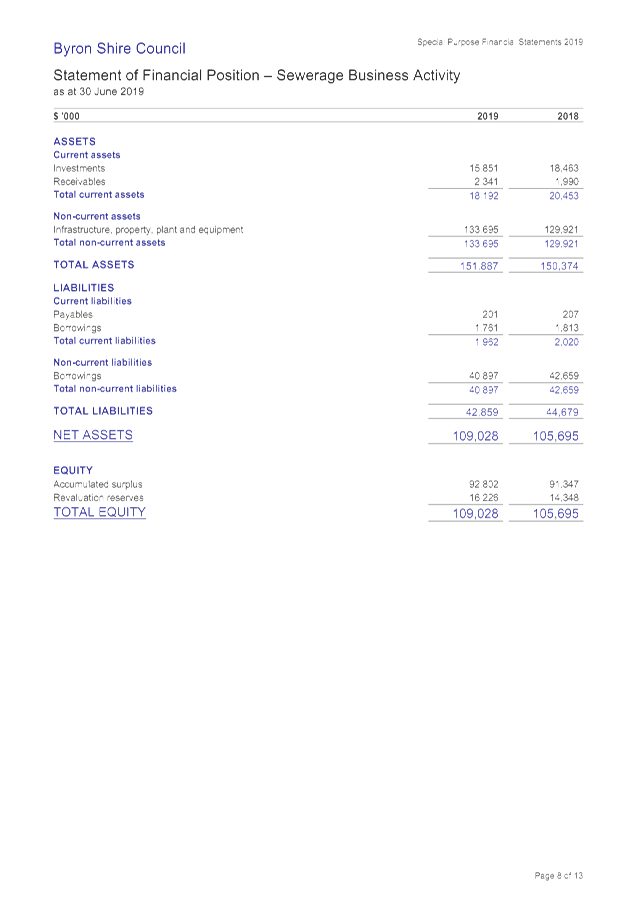

Mandatory disclosures in the Special Purpose Financial

Reports are Water and Sewerage.

Additional disclosure relates to Council business units that

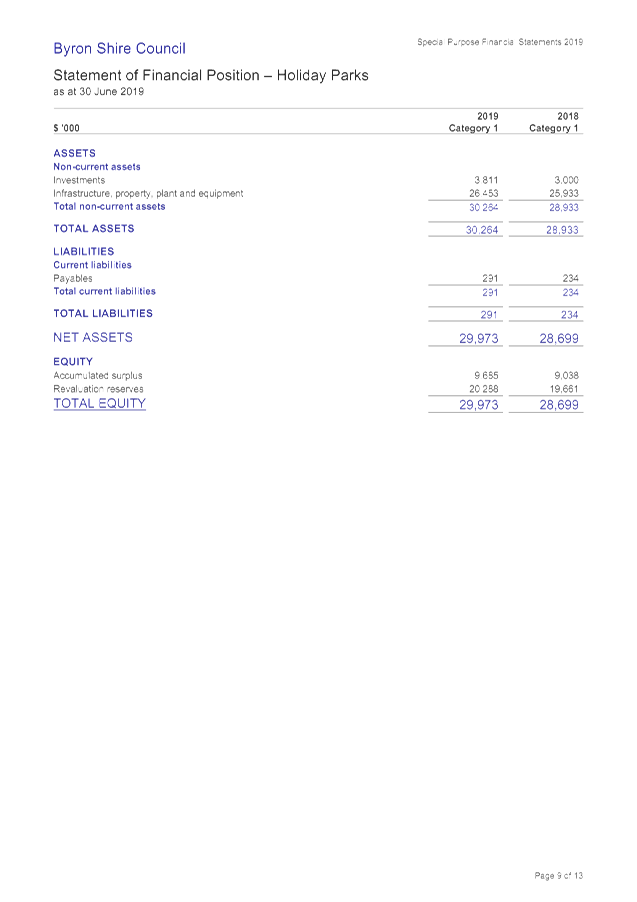

Council deems ‘commercial’. In this regard Council has

traditionally reported its Caravan Park Operations being Suffolk Beachfront

Holiday Park and First Sun Holiday Park on a combined basis. These

financial reports must also classify business units in the following

categories:

· Category 1 –

operating turnover is greater than $2million

· Category 2 –

operating turnover is less than $2million

All of Council’s business units are classed as

Category 1 with all having operating turnover greater than $2 million.

Another feature of the Special Purpose Financial Reports is

to build taxes and charges where not physically incurred into the financial

results in order that the results can be measured on a level playing field with

other organisations operating similar businesses, who are required to

pay these additional taxes and charges. These taxes and charges include:

· Land tax – Council

is normally exempt from this tax so notional land tax is applied.

· Income tax –

Council is exempt from income tax and in regard to these reports, company

tax. Any surplus generated has a notional company tax applied to it.

· Debt guarantee fees

– Generally due to the low credit risk associated with Councils, Councils

can often borrow loan funds at lower interest rates then the private

sector. A debt guarantee fee inflates the borrowing costs by

incorporating a notional cost between interest payable on loans at the interest

rate borrowed by Council and one that would apply commercially.

The Special Purpose Financial Reports are prepared on a

non-consolidated basis - in other words they are grossed up to include any

internal transactions with the General Fund.

Auditor’s Report on

the Financial Statements

Council’s auditor, the Auditor General of NSW (NSW Audit Office) and

their representative firm Thomas Noble and Russell, have completed their audit

of the Draft 2018/2019 Financial Statements. All matters identified during the

audit have been adjusted and included in the Draft 2018/2019 Financial

Statements (if required) included at Attachments 1 and 2. The Auditor’s

Report is to report on the following:

· A report on the

conduct of the audit. This report states the financial statements have been

audited with an opinion. For the year ended 30 June 2019 the opinion is

expected to be unmodified. In addition, this report outlines any

significant audit issues and observations, and includes an analysis of the

major aspects of the financial statements.

The Draft Auditor’s Report is included at Attachments

3 and 4.

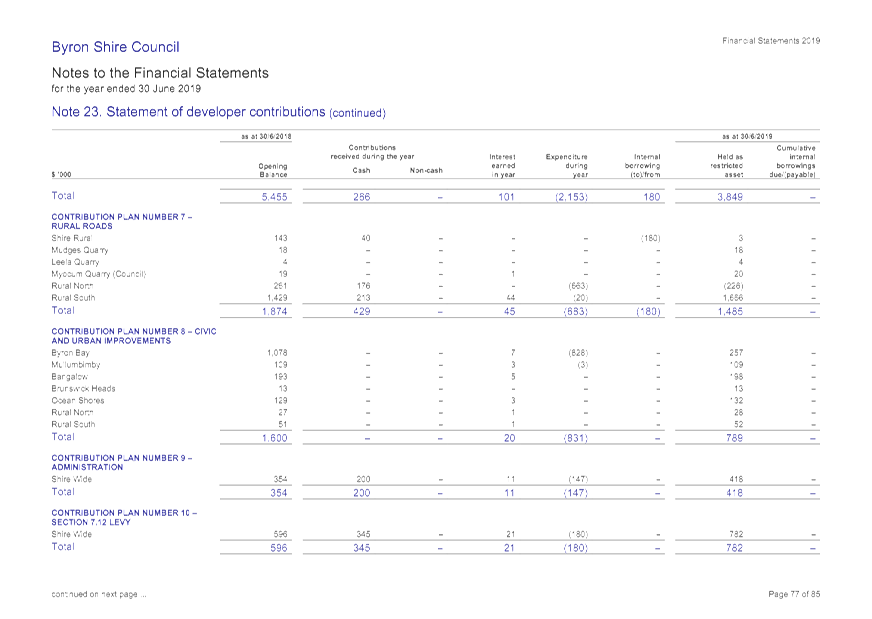

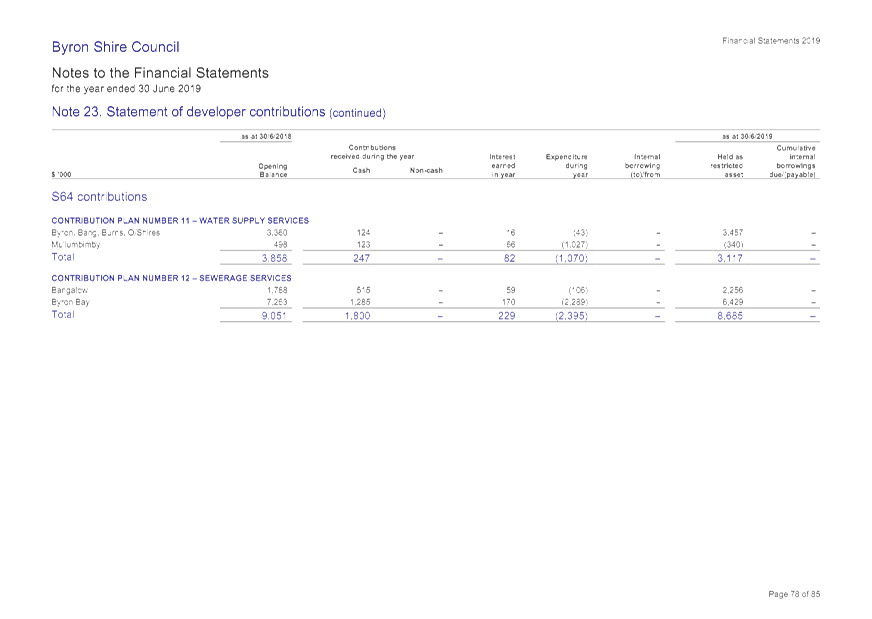

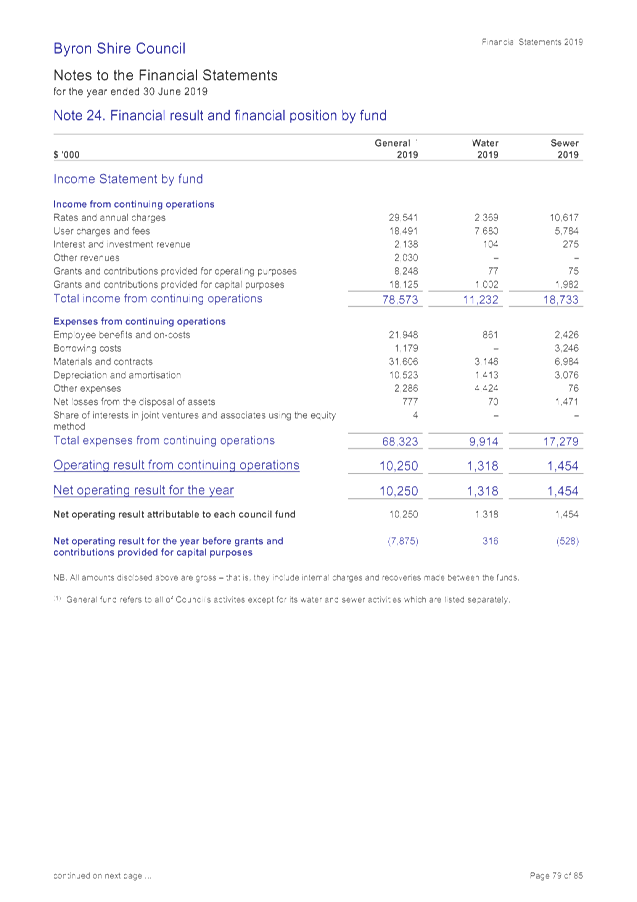

Specific Items relating to 2018/2019 Draft Financial

Statements

The Draft 2018/2019 Financial Statement results have been

impacted by the following items that require explanation to Council:

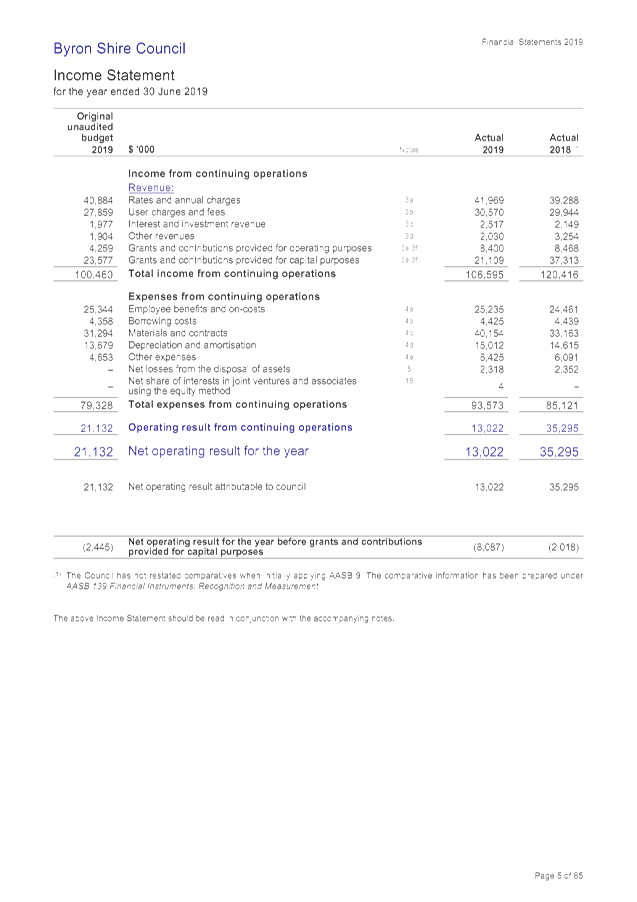

· Operating

Result from Continuing Operations

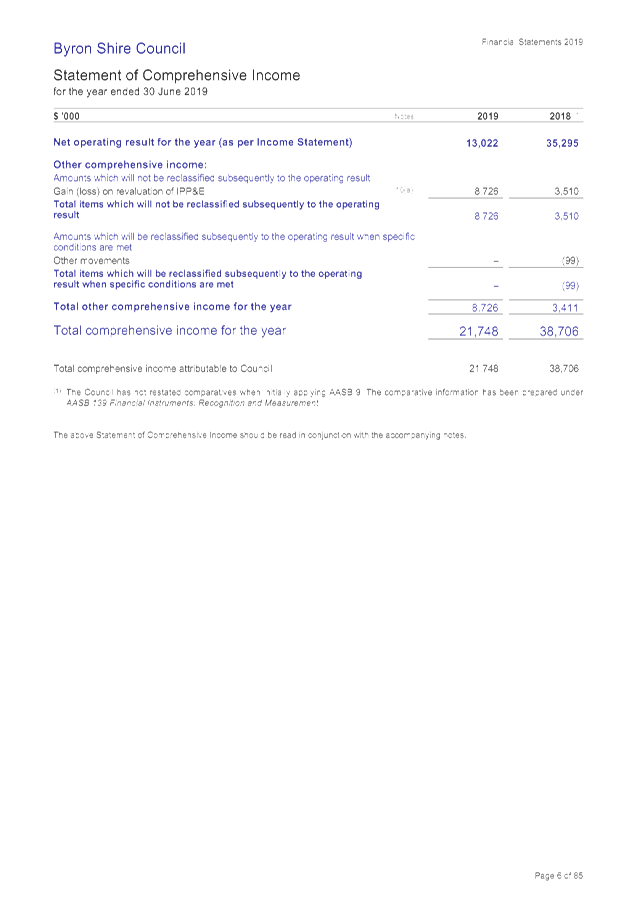

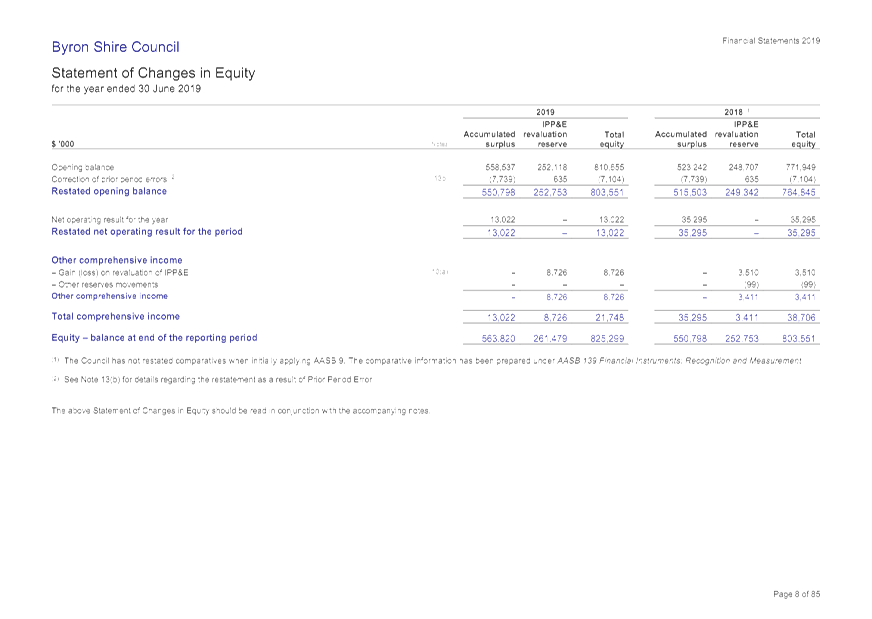

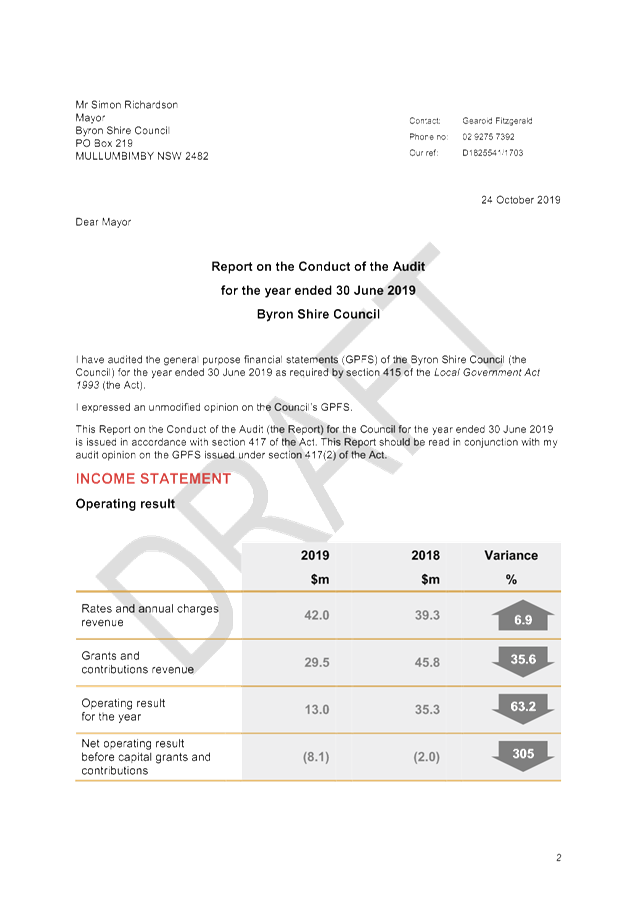

The 2018/2019 financial year has seen a positive overall

financial result. Council recorded a $13.022million surplus which, while less

than the $35.295million surplus in 2017/2018, is still nevertheless a surplus.

This result incorporates the recognition of capital revenues such as capital

grants and contributions for specific purposes and asset dedications amounting

to $21.109 million compared to $37.314million in 2017/2018. Capital grants and

contributions in 2017/2018 were significantly influenced by the transfer of

assets to Council from the Old Pacific Highway that was not repeated in

2018/2019.

A more important indicator is the operating result before capital

grants and contributions. This result was a deficit of $8.087 million in

2018/2019 compared to a deficit of 2.018million in 2017/2018 representing a

decrease of $6.069million between financial years. This indicates

Council’s operating expenditures exceeded its operating revenues. Whilst

operating revenues excluding capital grants and contributions grew by

$2.383million, overall operating expenses grew by $8.452million.

With reference to the Income Statement to the General

Purpose Financial Reports included at Attachment 1, the following table

indicates the major changes between 2018/2019 and 2017/2018 by line item:

|

Item

|

Change between 2018/2019 and 2017/2018 $’000

|

Change

Outcome

|

Comment

|

|

Income

|

|

|

|

|

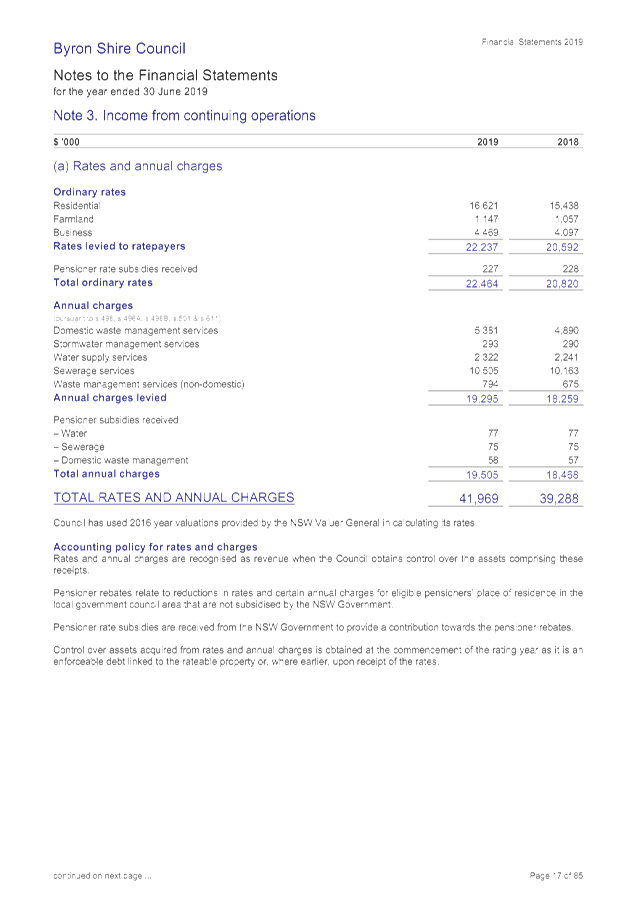

Rates & Annual Charges

|

+$2,681

|

Increase

|

Reflects imposition of the

second year of the 7.50% Special Rate Variation and changes in annual charges

from Council’s adopted 2018/2019 Revenue Policy

|

|

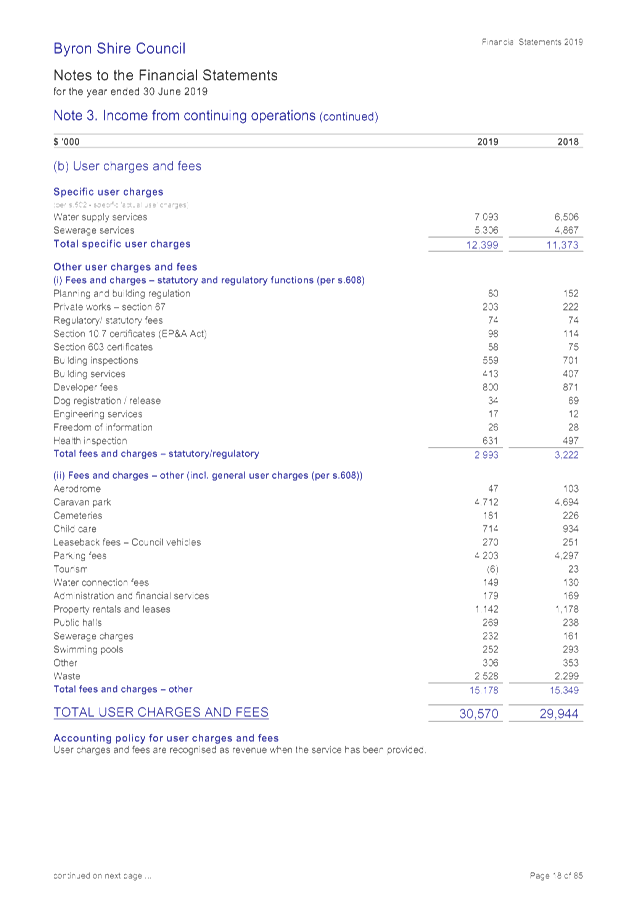

User Charges and Fees

|

+$626

|

Increase

|

Major changes include

additional $1,026k revenue for water and sewer user charges, increase in

waste fees $229K and a decline in statutory/regulatory fees of $229k. Further

information is available in Note 3(b) to Attachment 1.

|

|

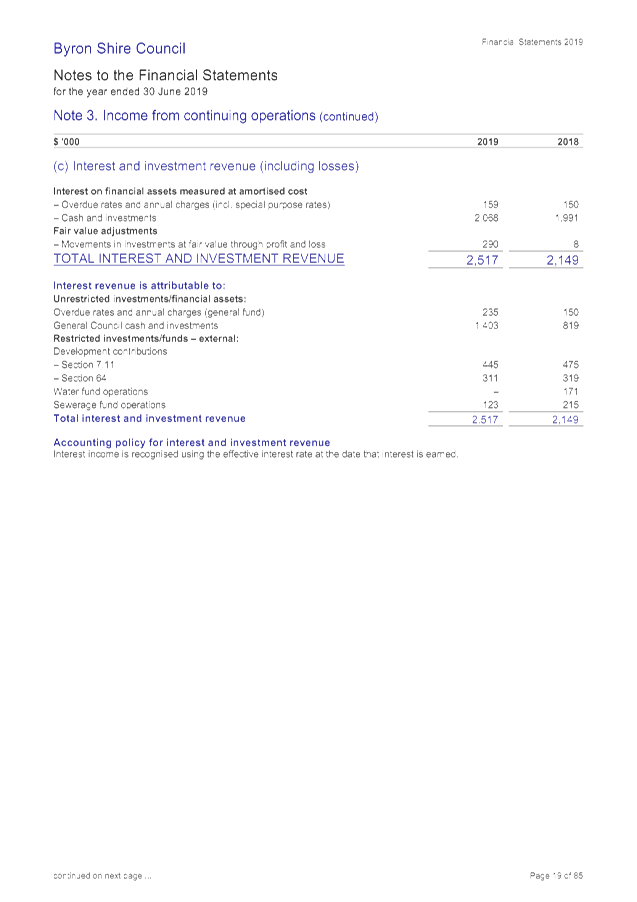

Interest and Investment

Revenue

|

+$368

|

Increase

|

Council’s cash

position did not decline as expected which enabled more funds to be invested

even though interest rates have continued to decline. Council also realised a

$290k fair value gain on its investments.

|

|

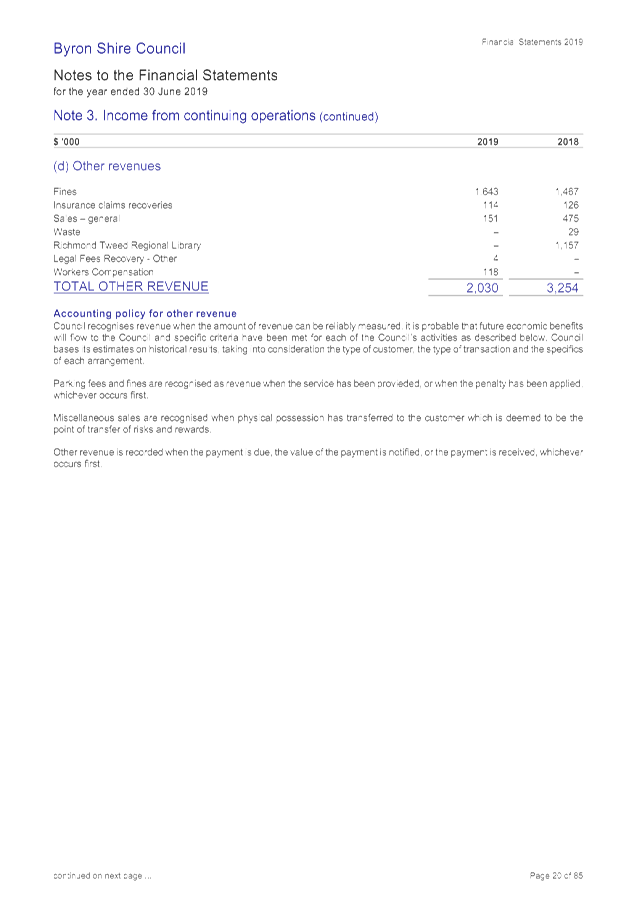

Other Revenues

|

-$1,224

|

Decrease

|

Increase of $176k for

fines, but major change was the once off recognition of share in Richmond

Tweed Regional Library $1,157k in 2017/2018 that was not repeated in

2018/2019.

|

|

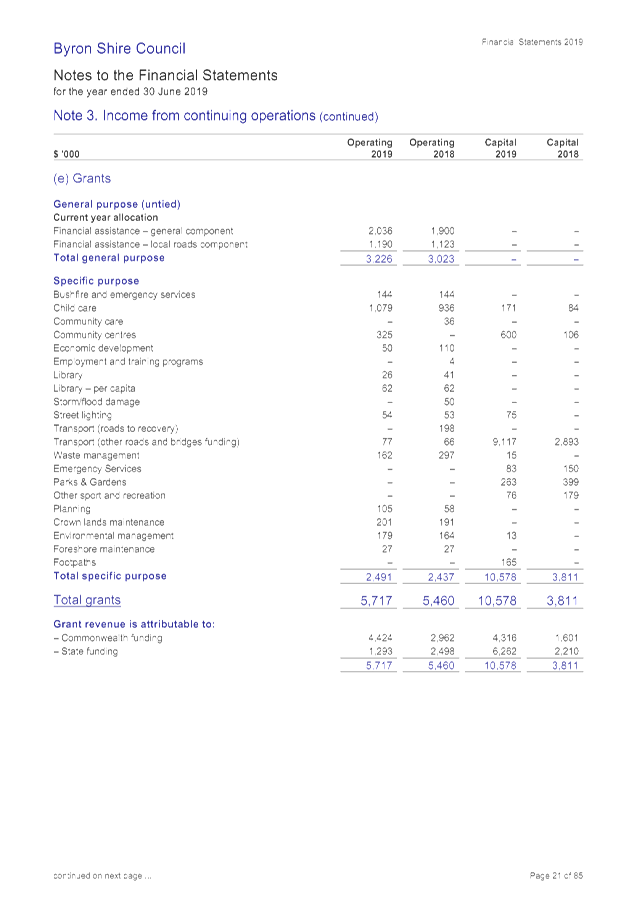

Grants & Contributions

– Operating

|

-$68

|

Decrease

|

Overall operating grants

increased by $257k including 205k increase in the Financial Assistance Grant

but contributions reduced by $325k. Further information is available in

Note 3€ and Note 3(f) to Attachment 1.

|

|

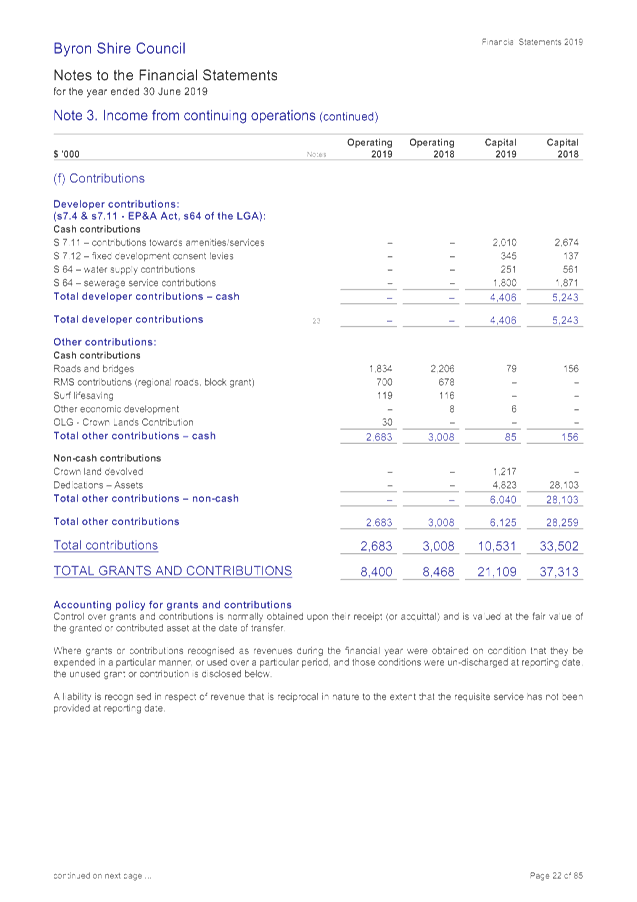

Grants & Contributions

– Capital

|

-$16,204

|

Decrease

|

Capital grants increased

$6,767k mainly for roads and bridges funding but capital contributions

revenue decreased $22,971k. Reduction in capital contributions is due

to reduced asset dedication revenue that was significant in 2017/2018 from

the dedication of former Pacific Highway assets.

|

|

Total Income Change

|

-$13,821

|

Decrease

|

|

|

|

|

|

|

|

Expenditure

|

|

|

|

|

Employee Benefits and

Oncosts

|

+$774

|

Increase

|

Increased leave entitlement

expenses of $959k reflecting emphasis on controlling leave balances and

impact of declining interest rates on present value of liability

calculations. There was a decrease of $371k of employee costs capitalised on

capital works in 2018/2019 compared to 2017/2018 and gross salary and wages

$657k. More information is provided at Note 4(a) to Attachment 1.

|

|

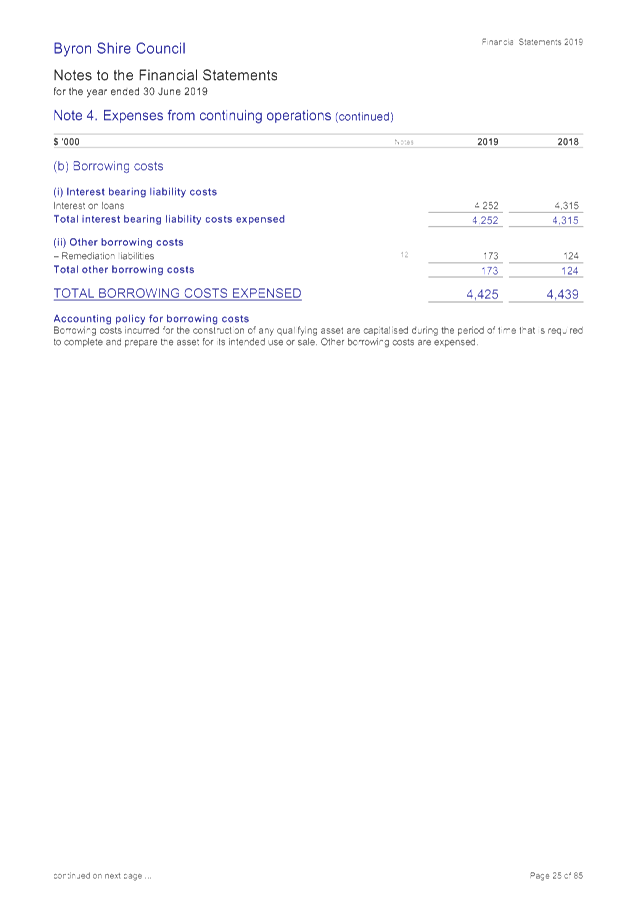

Borrowing Costs

|

-$14

|

Decrease

|

Results from Council

gradually repaying loans and not borrowing significant new loans. New

loans of $7.669million borrowed at end of 2018/2019 financial year.

Interest impact of this loan will be realised commencing in 2019/2020 and

refinancing of significant sewerage loan in December 2019.

|

|

Materials & Contracts

|

+$6,991

|

Increase

|

Raw materials and contracts

increased of $6,414k. Major contributor to this was former Mullumbimby

Hospital demolition $2,025k, natural disaster works $1,886k and capital

expenditure $3,300k not capitalised. Other changes can be found at Note 4(b)

to Attachment 1.

|

|

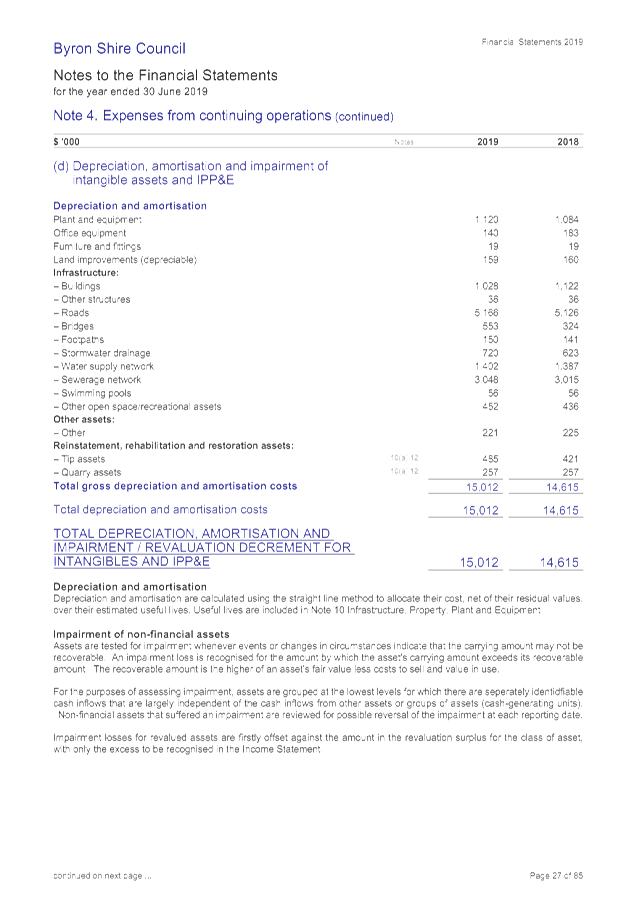

Depreciation

|

+$397

|

Increase

|

Respective changes between

asset classes are outlined at Note 4(d) to Attachment 1. Essentially

small incremental increases in each asset class.

|

|

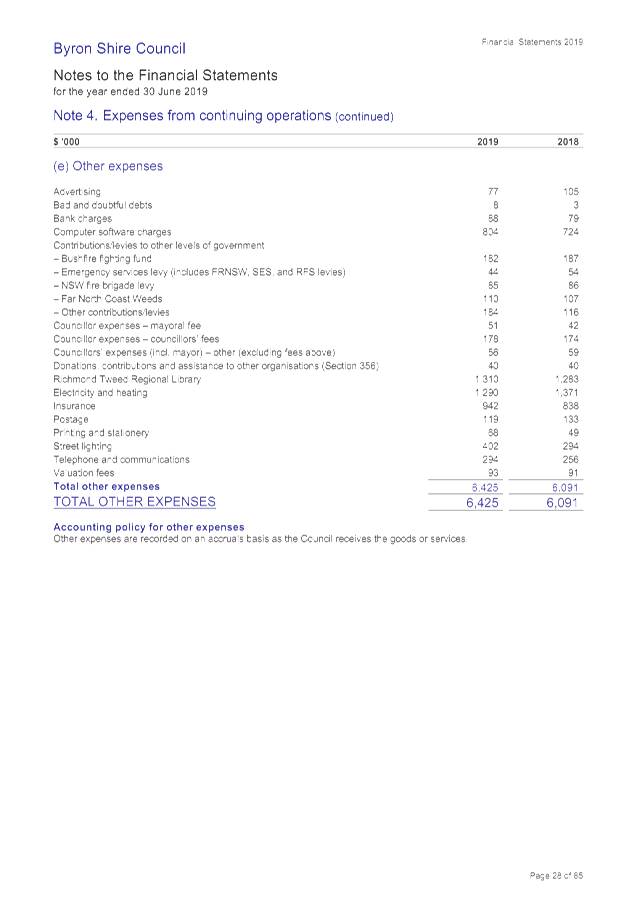

Other Expenses

|

+$334

|

Increase

|

Overall increase but there

were variations in line items as disclosed at Note 4(e) to Attachment 1. Most

significant item was street lighting $108k.

|

|

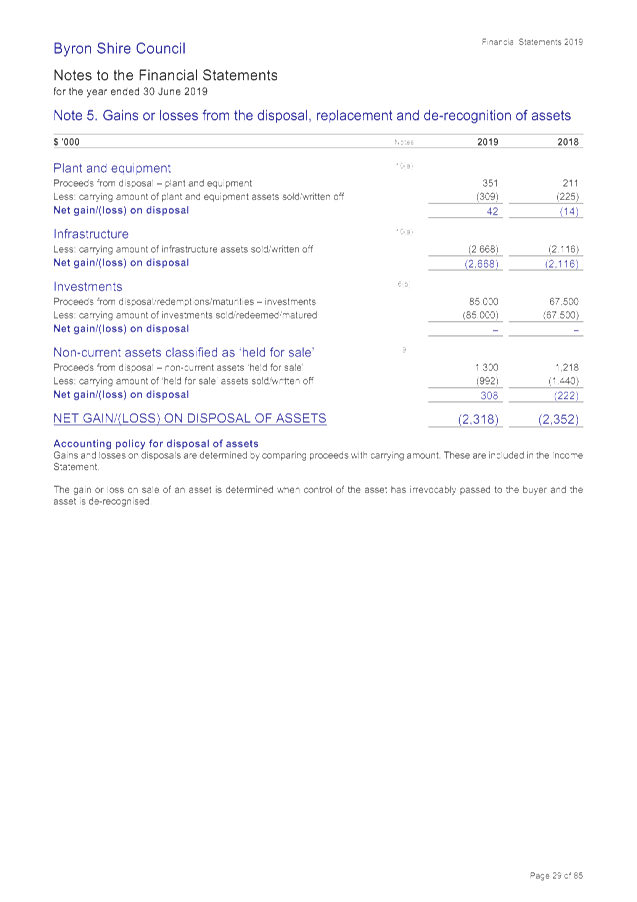

Net Losses from Disposal of

Assets

|

-$34

|

Decrease

|

Reflection of the written

down value of assets disposed at the end of financial year and is contingent

upon the extent of assets disposed and their written down value at the time

of disposal which can vary. For 2018/201, Council has more disposals than

gains including the disposal of infrastructure $2,668k, plant and equipment

$42k gain and gain on sale of land $308k. Further details can be found at

Note 5 to Attachment 1

|

|

Net share of interests in

associates

|

+4

|

Increase

|

Recognition of

Council’s share of the operating result of Richmond Tweed Regional Library

for 2018/2019

|

|

Total Expenditure Change

|

+$8,452

|

Increase

|

|

|

|

|

|

|

|

Change in Result

|

+$22,273

|

Decrease

|

Decrease in overall surplus

between financial years.

|

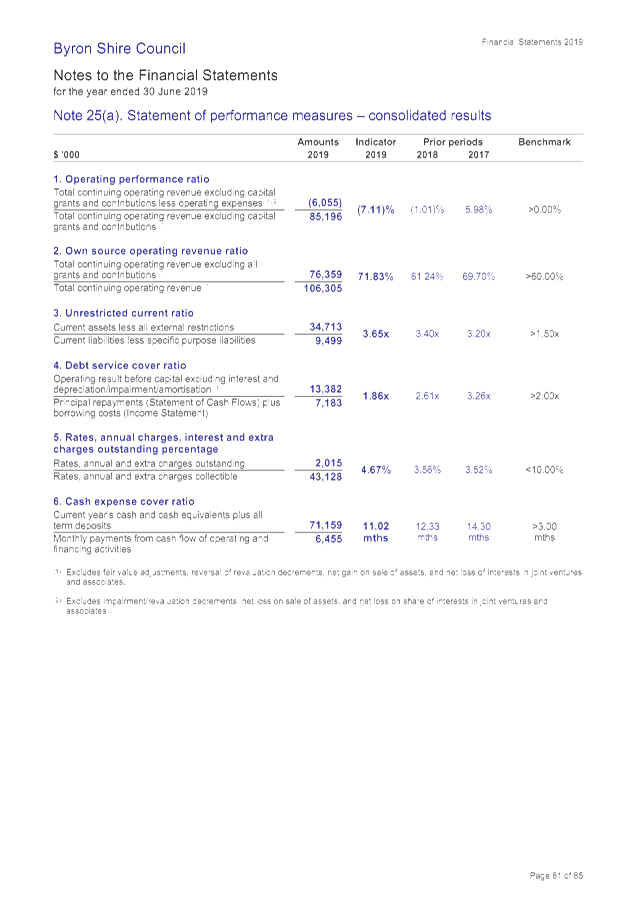

Following from the operating results, are the performance

ratios at Note 25 to the General Purpose Financial Statements. These have

been derived following the financial assessments undertaken by NSW Treasury

Corporation on all NSW Councils in 2012, and are now incorporated into the

latest update to the Code of Accounting Practice and Financial Reporting that

determines the content of Council’s Financial Statements. These

ratios present either a stable or improving result for Council except for the

following:

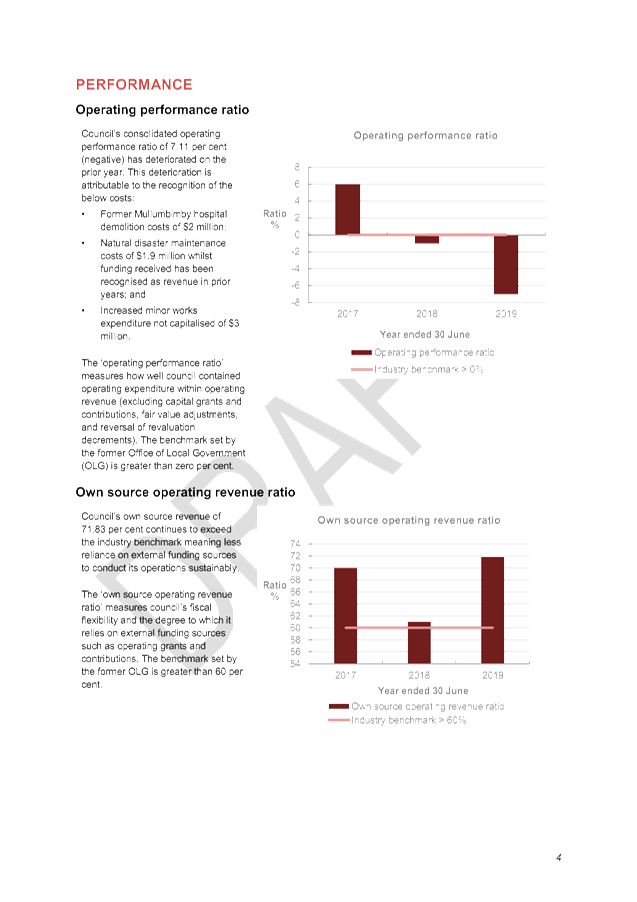

1. Operating

Performance Ratio is a reflection of the operating result of Council. The

benchmark is to be greater than 0% but in 2017/2018 Council’s ratio was

-1.01% and in 2018/2019 it was -7.11%. This ratio was impacted by some

one-off items i.e. demolition costs of the former Mullumbimby Hospital, however

Council will look to improve this result back towards the benchmark.

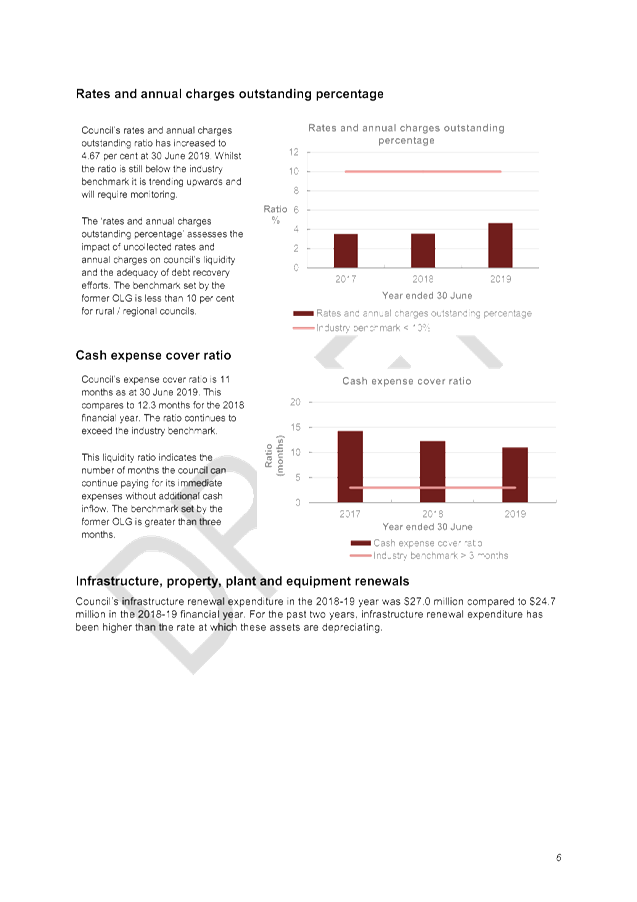

2. Outstanding,

Rates and Annual Charges – Whilst still well within benchmark ,this ratio

has increased given the compounding from the ongoing implementation of the

2017/2018 Special Rate Variation. This means that the increasing annual charges

as well as the current economic climate are impacting the capacity of

ratepayers to pay. Council also changed its Debt Recovery Policy during

the 2018/2019 financial year and this ratio will be closely monitored going forward.

· Asset

Revaluations

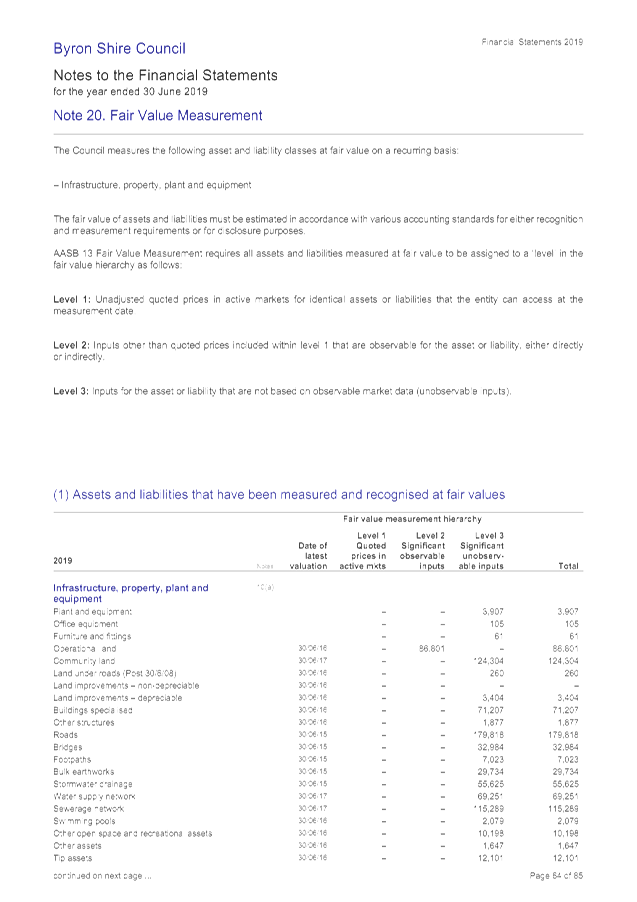

During 2018/2019, there was no revaluation of assets except

for the indexation of Water and Sewerage Assets which is compulsory. Council

also indexed the valuation of its buildings even though this was not

compulsory.

For the upcoming 2019/2020 financial year, Council will need

to consider the revaluation of Roads and Drainage assets given these assets

have not been revalued since 2015 and are due for revaluation.

· Asset

Recognition

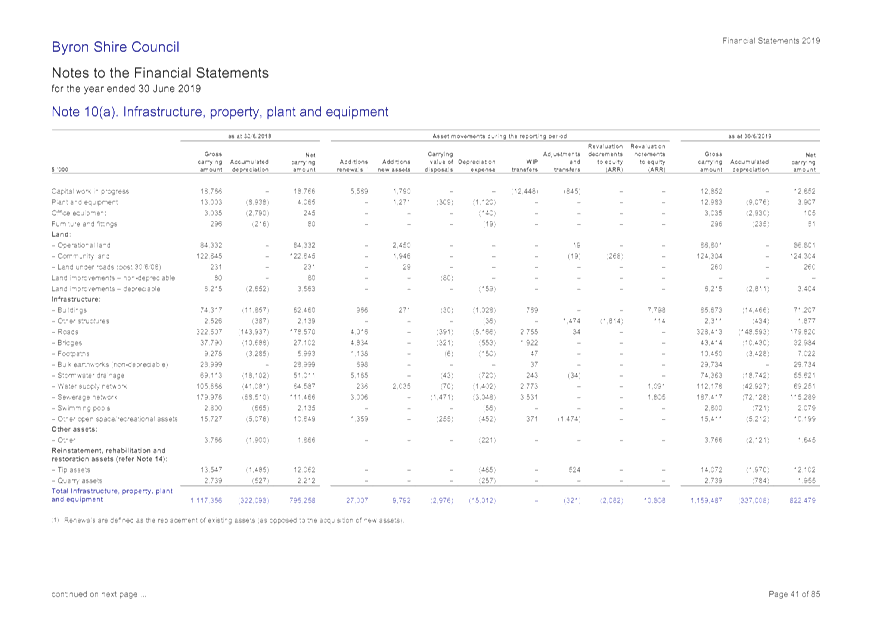

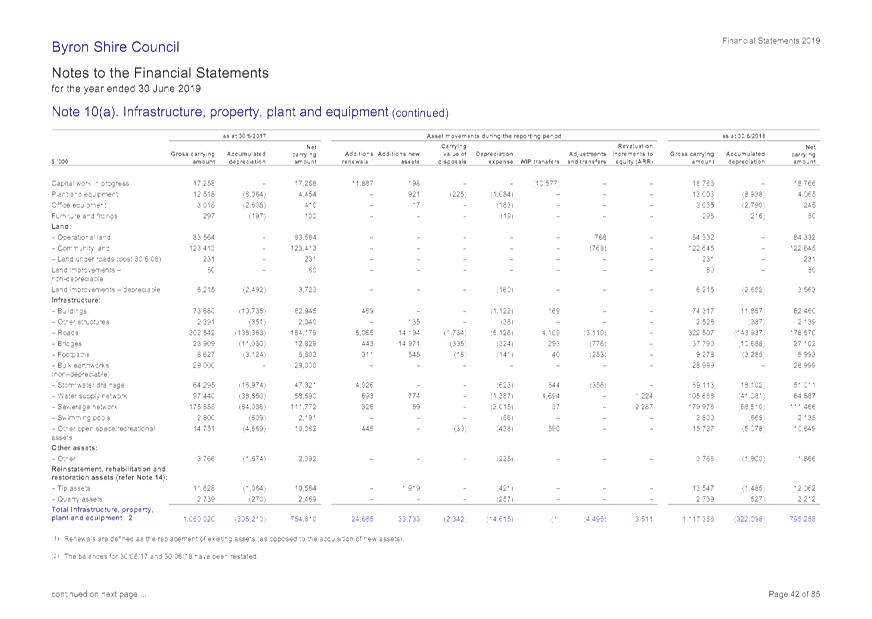

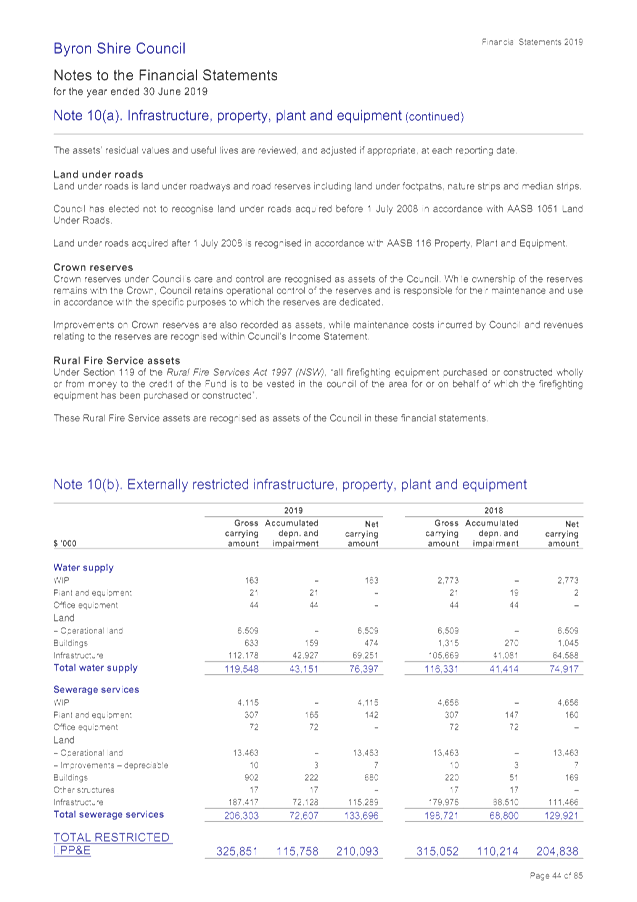

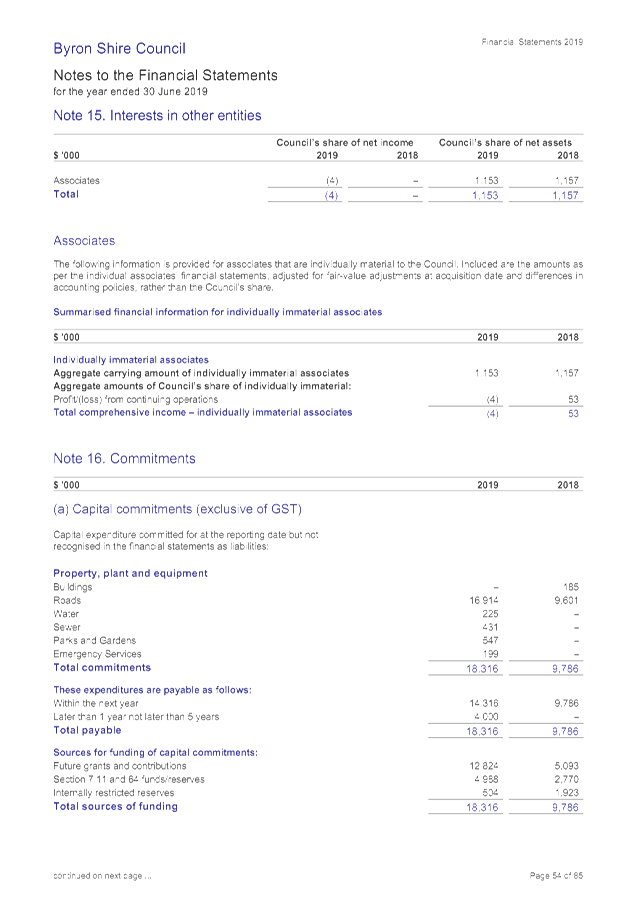

As indicated at Note 10 to the Council’s financial

statements, Council expended $27.007million on asset renewals and $9.792million

on new assets. The extent of asset renewals is significant and demonstrates

ongoing commitment in that area. The depreciation expense of Council’s

assets for 2018/2019 was $15.012million so it is pleasing to see the extent of

asset renewal recognised was significantly more then the financial realisation

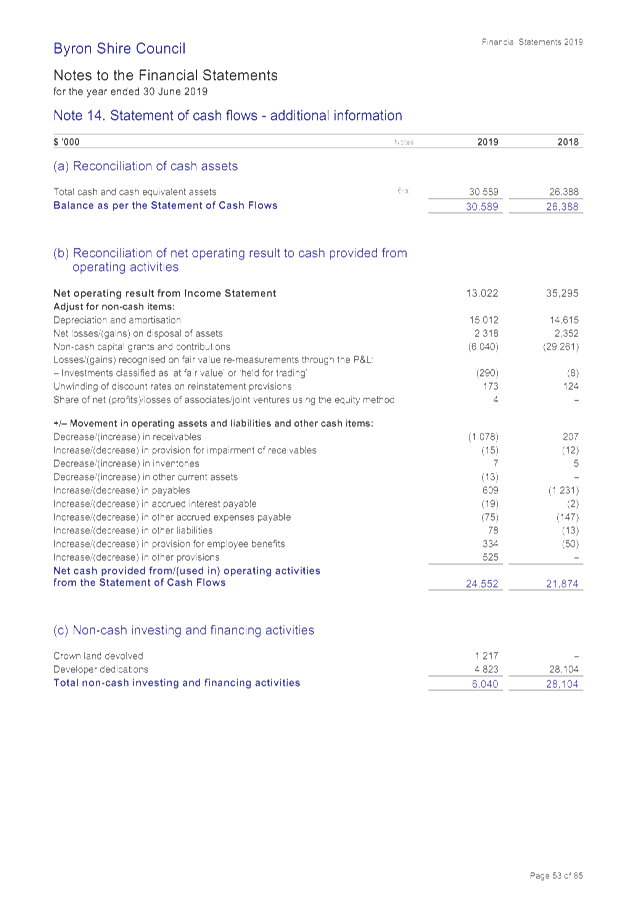

via depreciation of the consumption of Council’s assets.

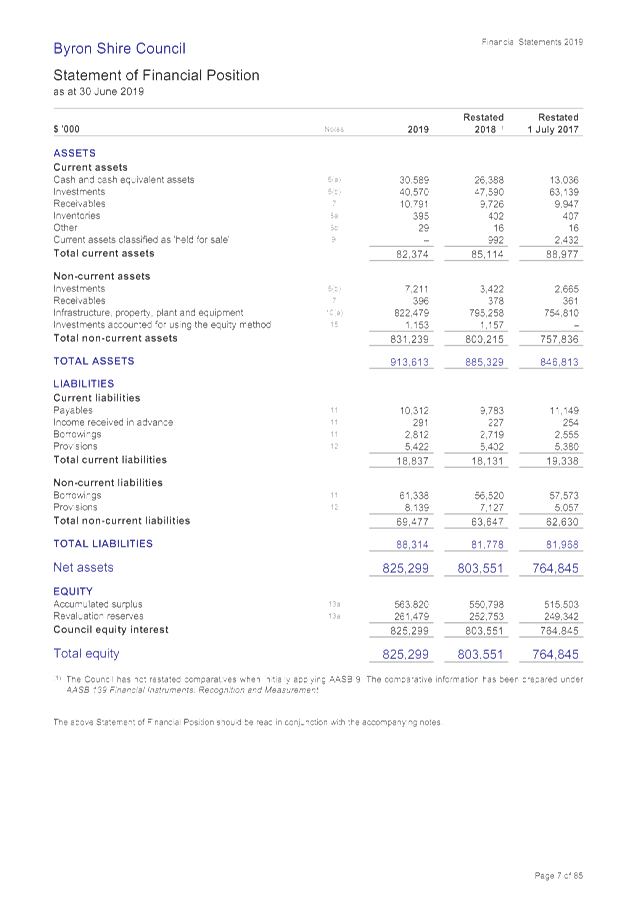

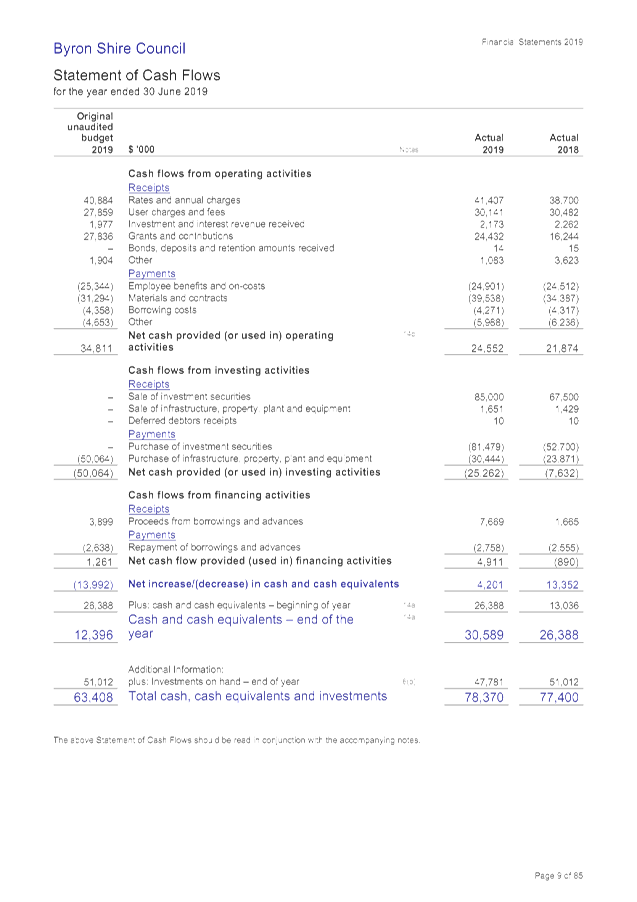

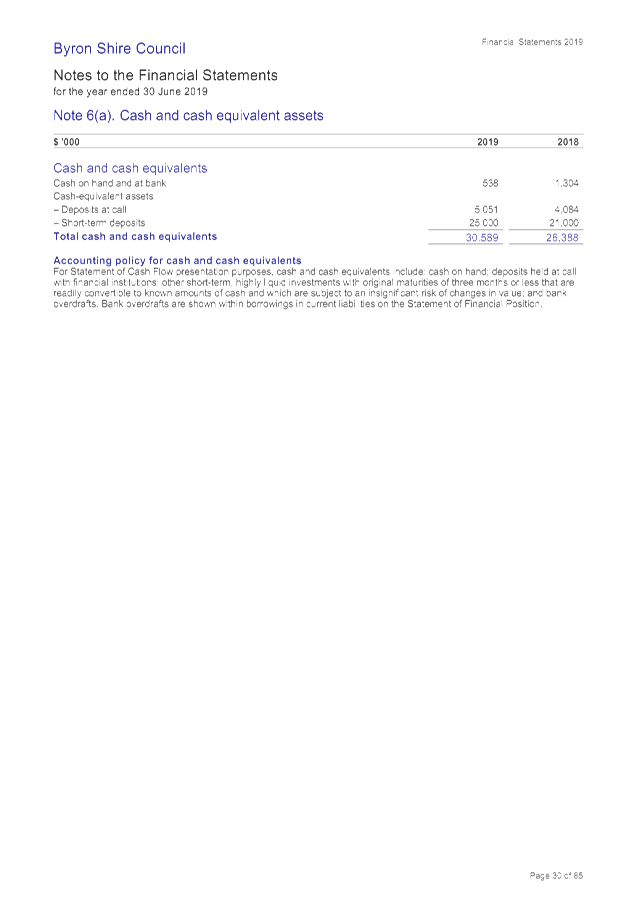

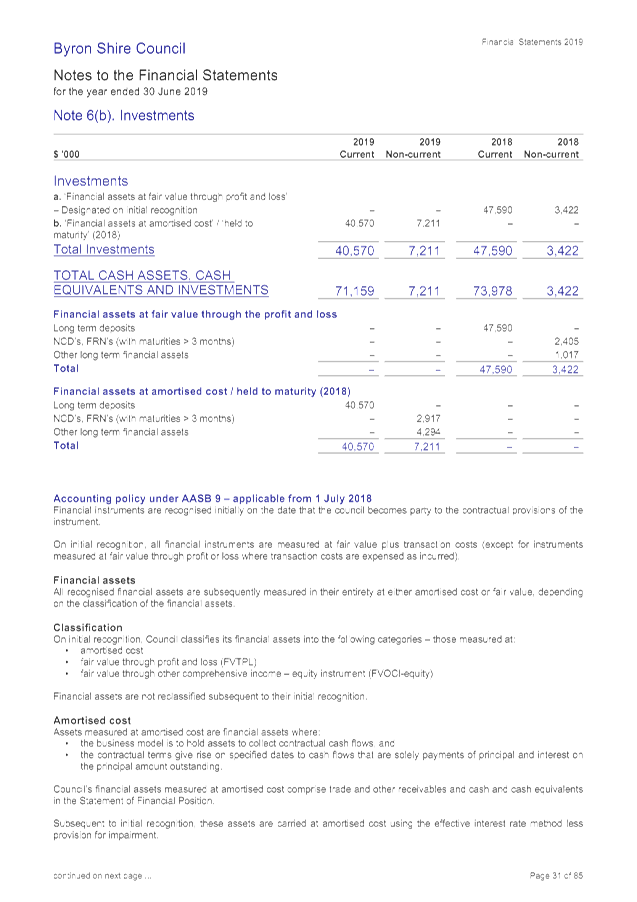

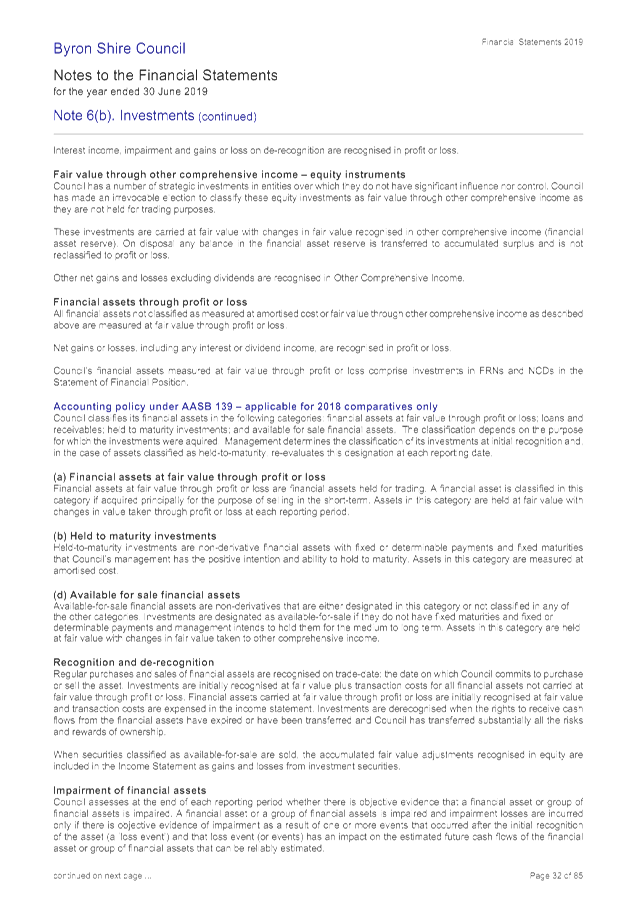

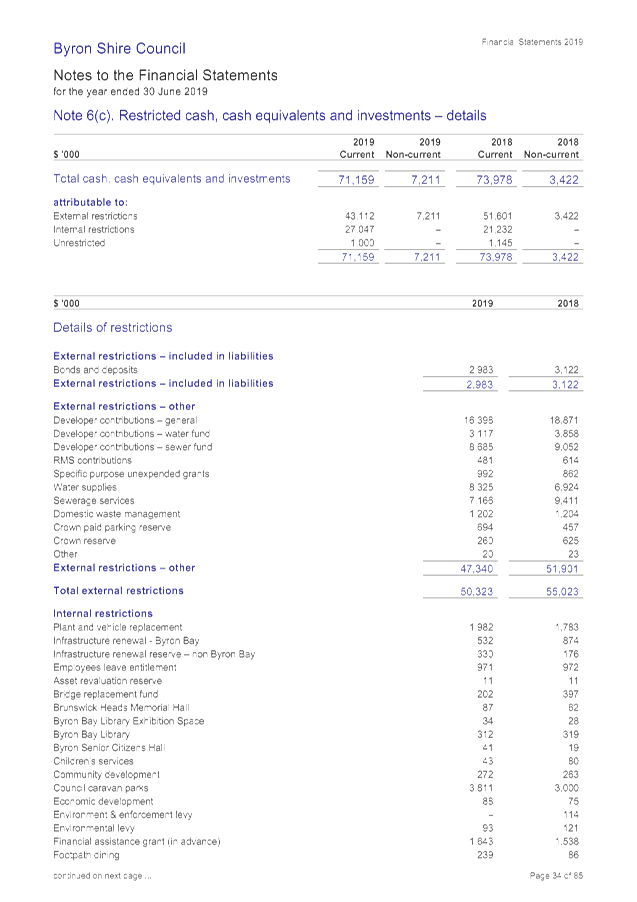

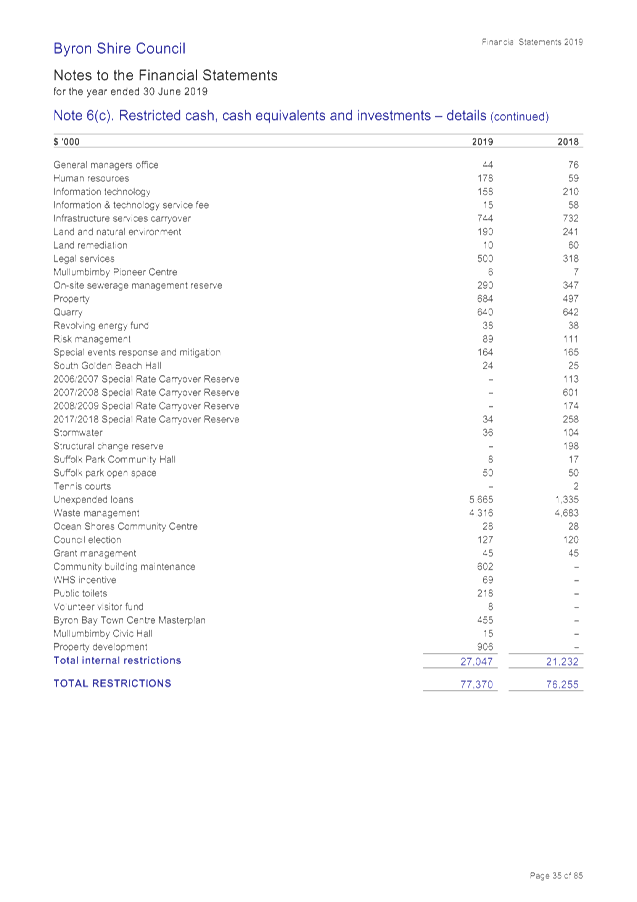

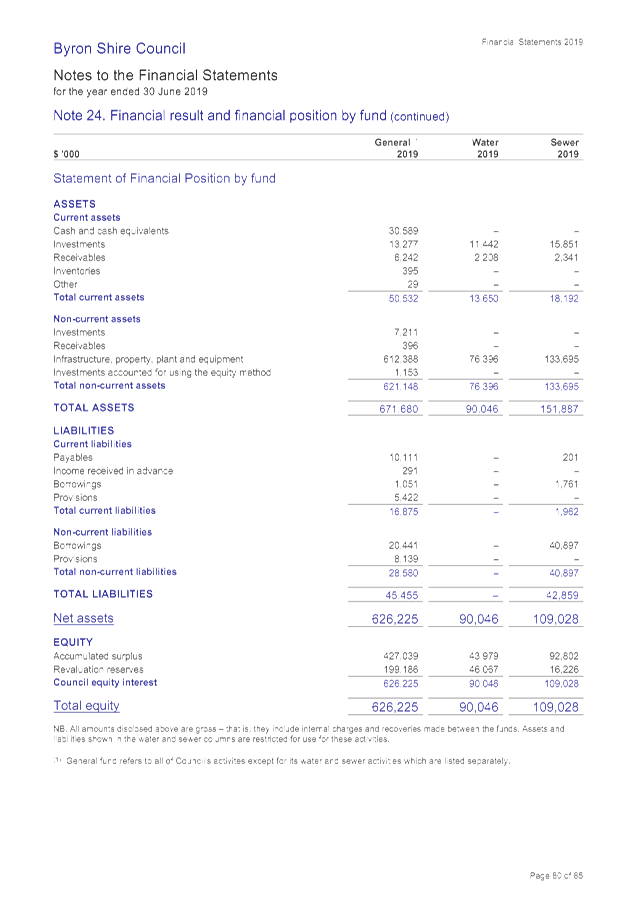

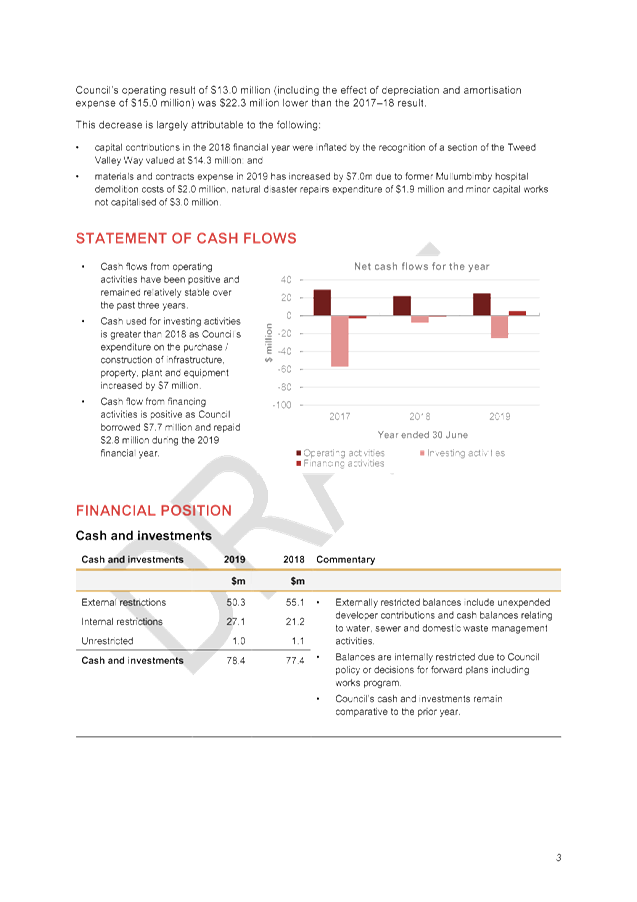

· Cash and

Investments

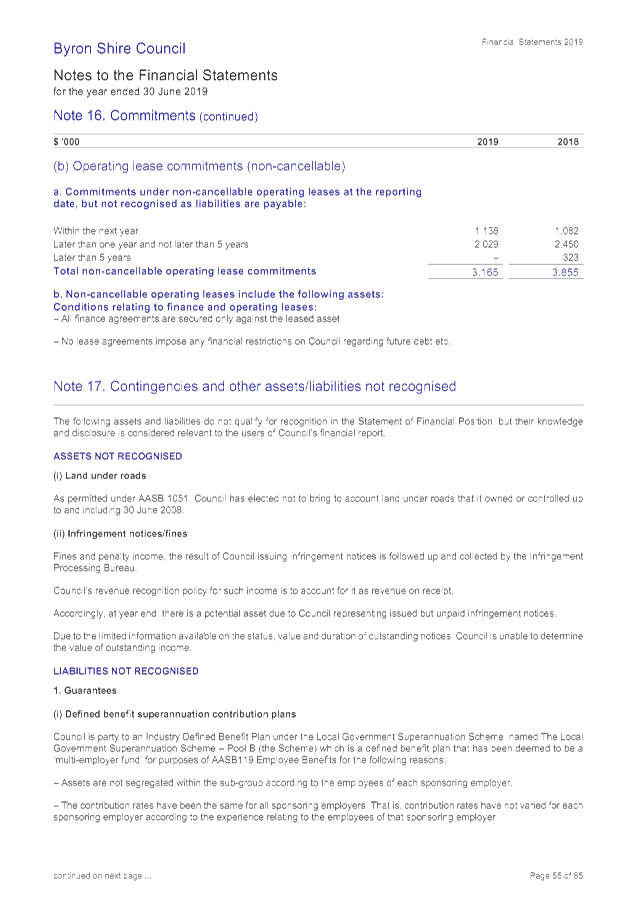

As at 30 June 2019 (detailed at Note 6 to the financial

statements) Council has maintained $1.000million in unrestricted cash and

investments being a reduction of $0.145million compared to 2017/2018.

This is an ongoing pleasing result and Council has been able to maintain another

one of its short term financial goals of reaching an unrestricted cash balance

of $1million. All other cash and investments totalling $77.370million are

restricted for specific purposes. Overall the cash and investment position of

Council increased by $0.970million during the year.

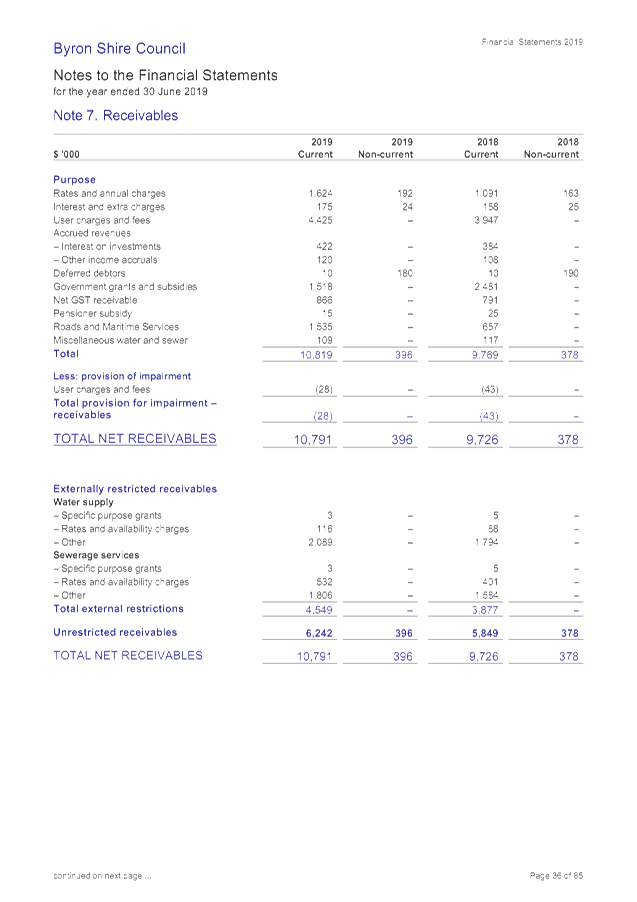

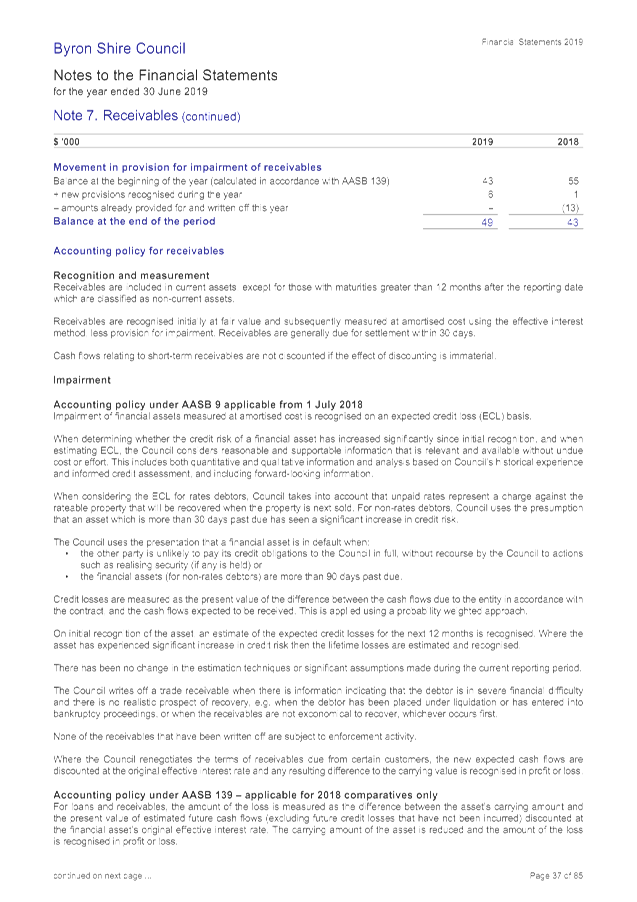

· Receivables

As at 30 June 2019 (detailed at Note 7 to the financial

statements) Council was due $11.187million in receivables. Of this amount

$1.535million was due from Roads and Maritime Services for expenditure claims,

$0.866million from the Commonwealth Government for Goods and Services Tax and

$1.581million in Government grants and subsidies. Overall receivables increased

by $1.083million compared to the 2017/2018 financial year.

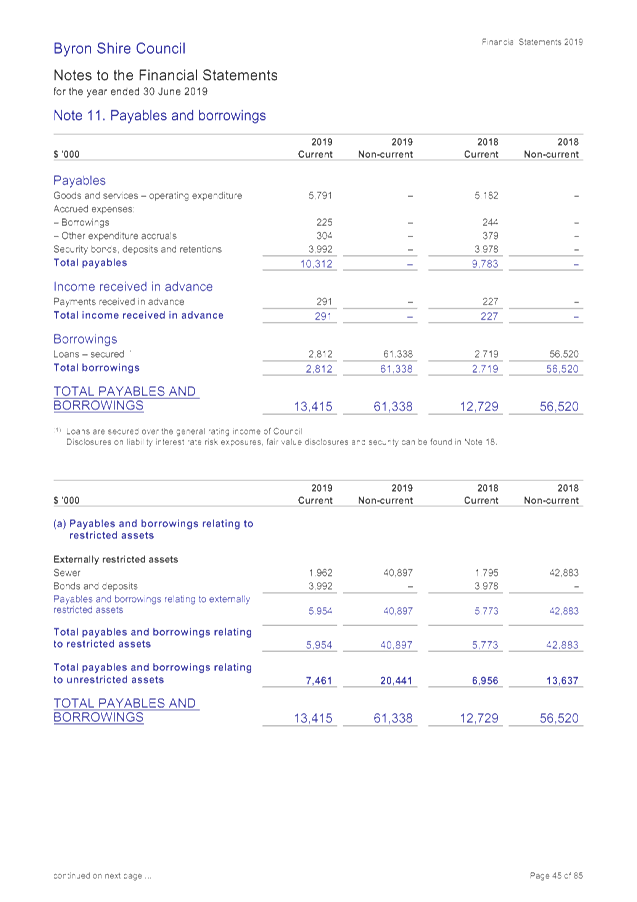

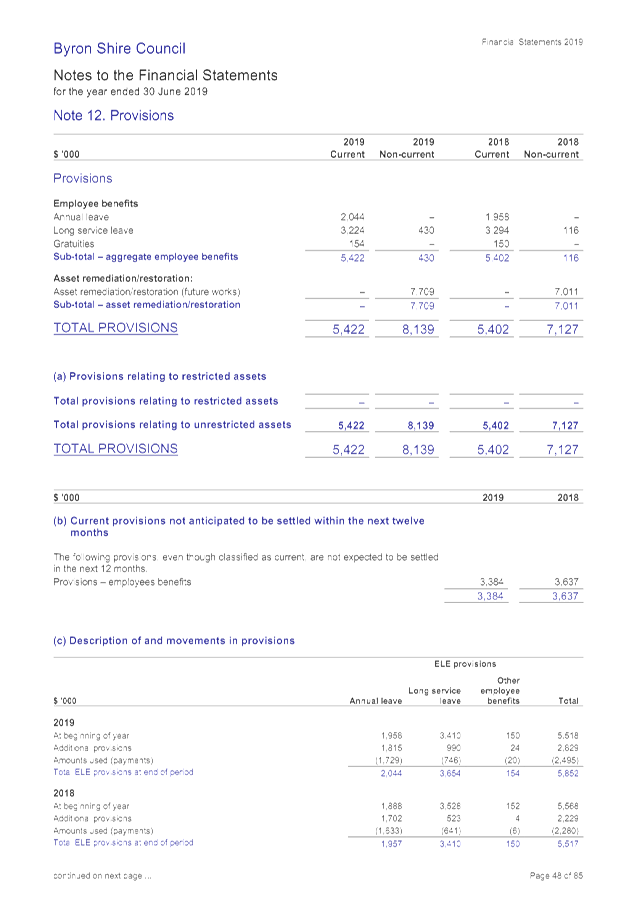

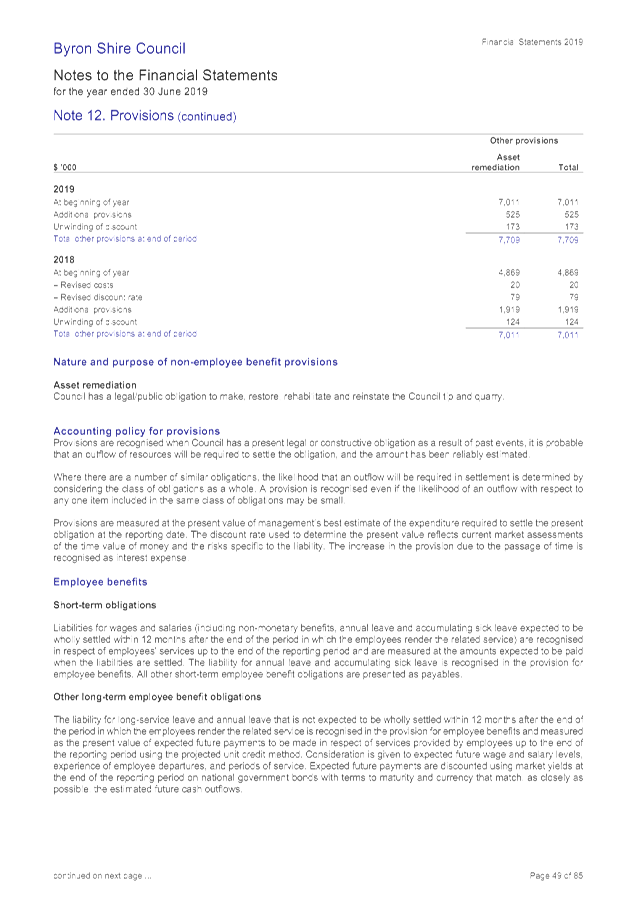

· Payables and

Provisions

At 30 June 2019 (detailed at Note 11 for payables and Note

12 for provisions) total payables by Council were $10.603million including

$4.283million held in security bonds, deposits, retentions, payments received

in advance, $0.529million in accrued expenses and $5.791million payable to

suppliers. In addition at 30 June 2019, Council has accrued employee leave

entitlements valued at $5.852million. Specific employee leave entitlements

include $2.044million for annual leave, $3.654million for long service leave

and $0.154million for gratuities. In comparison to 2017/2018, total payables

increased $0.593million whereas total provisions for employee leave

entitlements increased $0.334million.

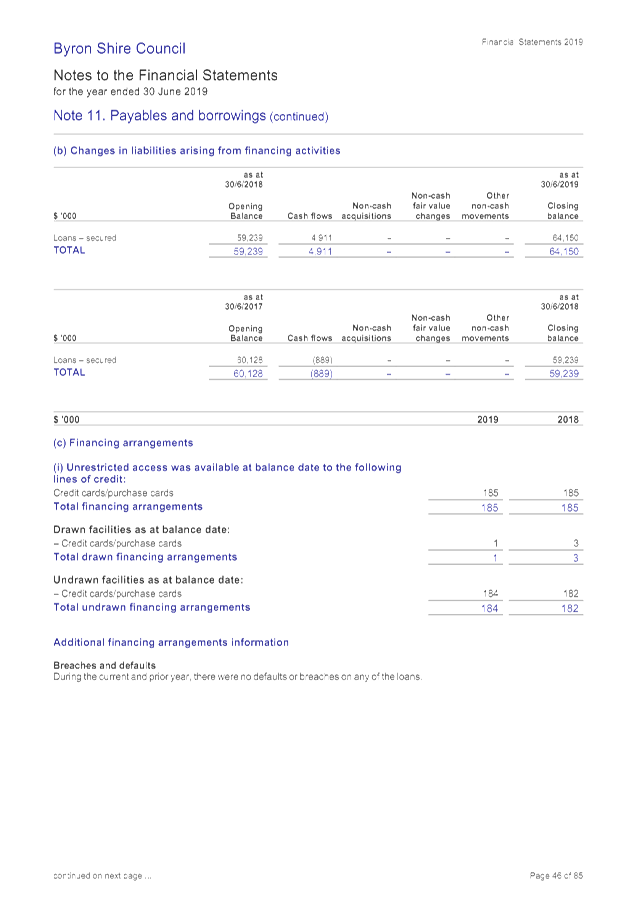

· Loan

Borrowings

During 2018/2019 Council

borrowed new loans of $7.669million and continued to make normal loan

repayments.

Council’s outstanding loans as at 30 June 2019 are

$64.15million. Total loan expenditure for 2018/2019 included interest of

$4.252million and principal payments of $2.758million. Total expenditure in

2018/2019 related to loan repayments was $7.010million or 8.20% of

Council’s revenue, excluding all grants and contributions.

The outstanding loans by Fund totalling $64.150million are

as follows:

· General Fund $21.492million

· Water Fund $0

– Water Fund is debt free

· Sewerage Fund $42.658million

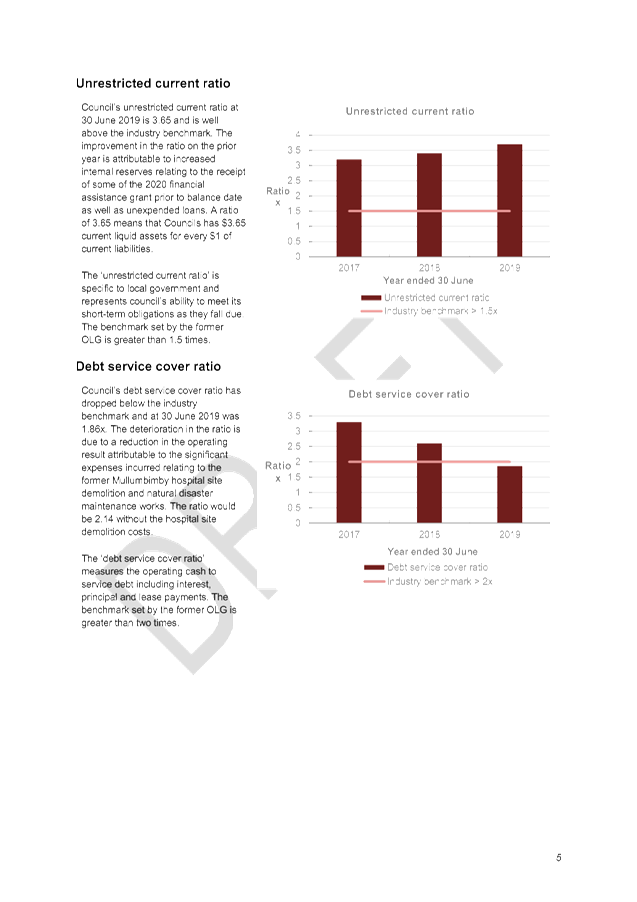

Liquidity

Council’s Statement of Financial Position (balance

sheet) indicates net current assets of $63.537million. It is on this basis, in

the opinion of the Responsible Accounting Officer, that the short term

financial position of Council remains in a satisfactory position and that

Council can be confident it can meet its payment obligations as and when they

fall due. That is, there is no uncertainty as to Council being considered a

‘going concern’. In addition, Council’s cash expense

cover ratio is at 11.02 months whereas the minimum benchmark is 3 months.

Council exceeds this benchmark by nearly four times.

Council’s Unrestricted Current Ratio has improved to

3.65 demonstrating Council has $3.65 in unrestricted current assets compared to

every $1.00 of unrestricted current liabilities.

On a longer term basis Council will need to consider its

financial position carefully. Nevertheless in isolation, the financial results

for 2018/2019 continue to present a ‘stable’ financial position.

Every effort will be made to manage the trend towards operational deficits

before capital grants and contributions.

STRATEGIC CONSIDERATIONS

Community Strategic Plan and

Operational Plan

|

CSP Objective

|

L2

|

CSP Strategy

|

L3

|

DP Action

|

L4

|

OP Activity

|

|

Community

Objective 5: We have community led decision making which is open and

inclusive

|

5.5

|

Manage

Council’s finances sustainably

|

5.5.2

|

Ensure the

financial integrity and sustainability of Council through effective planning

and reporting systems (SP)

|

5.5.2.2

|

Complete annual

statutory financial reports

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Legal/Statutory/Policy

Considerations

Section 413(2)(c) of the Local Government Act 1993 and

Regulation 215 of the Local Government (General) Regulation 2005 requires

Council to specifically form an opinion on the financial statements.

Specifically Council needs to sign off an opinion on the Financial Statements

regarding their preparation and content as follows:

In this regard the Financial Statements have been prepared

in accordance with:

· The Local Government Act

1993 (as amended) and the Regulations made thereunder.

· The Australian

Accounting Standards and professional pronouncements.

· The Local Government

Code of Accounting Practice and Financial Reporting.

And the content to the best of knowledge and belief:

· Presents fairly the

Council’s operating result and financial position for the year.

· Accords with

Council’s accounting and other records.

· Management is not aware

of any matter that would render the Financial Statements false or misleading in

any way.

Section 416(1) of the Local Government Act 1993, requires a

Council’s annual Financial Statements to be prepared and audited within

four (4) months of the end of that financial year i.e. on or before 31 October

2019.

Section 417(4) of the Local

Government Act 1993 requires, as soon as practicable after completing the

audit, the Auditor must send a copy of the Auditor’s Reports to the

Departmental Chief Executive and to the Council.

Section 417(5) of the Local

Government Act 1993 requires Council, as soon as practicable after receiving

the Auditor’s Reports, to send a copy of the Auditor’s Reports on

the Council’s Financial Statements, together with a copy of the

Council’s audited Financial Statements, to the Departmental Chief

Executive before 7 November 2019.

Section 418(1) of the Local Government Act 1993 requires

Council to fix a date for the Meeting at which it proposes to present its

audited Financial Statements, together with the Auditor’s Reports, to the

public, and must give public notice of the date so fixed. This

requirement must be completed within five weeks after Council has received the

Auditors Reports i.e. prior to 5 December 2019.

Financial Considerations

There are no direct financial implications associated with

this report as the report does not involve any future expenditure of Council

funds but it is a report advising the financial outcomes of Council during the

2018/2019 financial year which are identified in this report and attachments.

Consultation and Engagement

Section 420 of the Local Government Act 1993 requires

Council to provide the opportunity for the public to submit submissions on the

Financial Statements. Submissions are to be submitted within seven days

of the Financial Statements being presented to the public. In the case of

the 2018/2019 Financial Statements, the closing date for submissions will be 5

December 2019.

Public Access relating to items

on this Agenda can be made between 9.00am and 10.30am on the day of the

Meeting. Requests for public access should be made to the General Manager

or Mayor no later than 12.00 midday on the day prior to the Meeting.

Public Access relating to items

on this Agenda can be made between 9.00am and 10.30am on the day of the

Meeting. Requests for public access should be made to the General Manager

or Mayor no later than 12.00 midday on the day prior to the Meeting.