Transport and Infrastructure Advisory Committee Meeting

A Transport and Infrastructure Advisory

Committee Meeting of Byron Shire Council will be held as follows:

|

Venue

|

Conference Room, Station Street, Mullumbimby

|

|

Date

|

Thursday, 10 October 2019

|

|

Time

|

9.00am

|

Phillip

Holloway

Director Infrastucture Services I2019/1602

Distributed 03/10/19

What is a “Conflict of Interests” - A conflict of

interests can be of two types:

Pecuniary - an interest that a person has in a matter because of a reasonable

likelihood or expectation of appreciable financial gain or loss to the person

or another person with whom the person is associated.

Non-pecuniary – a private or personal interest that a Council

official has that does not amount to a pecuniary interest as defined in the Code

of Conduct for Councillors (eg. A friendship, membership of an association,

society or trade union or involvement or interest in an activity and may

include an interest of a financial nature).

Remoteness – a person does not have a pecuniary interest in a matter

if the interest is so remote or insignificant that it could not reasonably be

regarded as likely to influence any decision the person might make in relation

to a matter or if the interest is of a kind specified in the Code of Conduct

for Councillors.

Who has a Pecuniary Interest? - a person has a pecuniary interest in a

matter if the pecuniary interest is the interest of the person, or another

person with whom the person is associated (see below).

Relatives, Partners - a person is taken to have a pecuniary interest in a

matter if:

§ The person’s

spouse or de facto partner or a relative of the person has a pecuniary interest

in the matter, or

§ The person, or a

nominee, partners or employer of the person, is a member of a company or other

body that has a pecuniary interest in the matter.

N.B. “Relative”, in relation to a person means any of the

following:

(a) the

parent, grandparent, brother, sister, uncle, aunt, nephew, niece, lineal

descends or adopted child of the person or of the person’s spouse;

(b) the

spouse or de facto partners of the person or of a person referred to in

paragraph (a)

No Interest in the Matter - however, a person is not taken to have a

pecuniary interest in a matter:

§ If the person is

unaware of the relevant pecuniary interest of the spouse, de facto partner,

relative or company or other body, or

§ Just because the

person is a member of, or is employed by, the Council.

§ Just because the

person is a member of, or a delegate of the Council to, a company or other body

that has a pecuniary interest in the matter provided that the person has no

beneficial interest in any shares of the company or body.

Disclosure and participation in meetings

§ A Councillor or a

member of a Council Committee who has a pecuniary interest in any matter with

which the Council is concerned and who is present at a meeting of the Council

or Committee at which the matter is being considered must disclose the nature

of the interest to the meeting as soon as practicable.

§ The Councillor or

member must not be present at, or in sight of, the meeting of the Council or

Committee:

(a) at any

time during which the matter is being considered or discussed by the Council or

Committee, or

(b) at any

time during which the Council or Committee is voting on any question in

relation to the matter.

No Knowledge - a person does not breach this Clause if the person did

not know and could not reasonably be expected to have known that the matter

under consideration at the meeting was a matter in which he or she had a

pecuniary interest.

Non-pecuniary Interests - Must be disclosed in meetings.

There are a broad range of options available for managing conflicts &

the option chosen will depend on an assessment of the circumstances of the

matter, the nature of the interest and the significance of the issue being

dealt with. Non-pecuniary conflicts of interests must be dealt with in at

least one of the following ways:

§ It may be appropriate

that no action be taken where the potential for conflict is minimal.

However, Councillors should consider providing an explanation of why they

consider a conflict does not exist.

§ Limit involvement if

practical (eg. Participate in discussion but not in decision making or

vice-versa). Care needs to be taken when exercising this option.

§ Remove the source of

the conflict (eg. Relinquishing or divesting the personal interest that creates

the conflict)

§ Have no involvement by

absenting yourself from and not taking part in any debate or voting on the

issue as of the provisions in the Code of Conduct (particularly if you have a significant

non-pecuniary interest)

RECORDING OF VOTING ON PLANNING MATTERS

Clause 375A of the Local Government Act 1993

– Recording of voting on planning matters

(1) In this section, planning

decision means a decision made in the exercise of a function of a council

under the Environmental Planning and Assessment Act 1979:

(a) including a decision

relating to a development application, an environmental planning instrument, a

development control plan or a development contribution plan under that Act, but

(b) not including the making of

an order under that Act.

(2) The general manager is

required to keep a register containing, for each planning decision made at a

meeting of the council or a council committee, the names of the councillors who

supported the decision and the names of any councillors who opposed (or are

taken to have opposed) the decision.

(3) For the purpose of maintaining

the register, a division is required to be called whenever a motion for a

planning decision is put at a meeting of the council or a council committee.

(4) Each decision recorded in

the register is to be described in the register or identified in a manner that

enables the description to be obtained from another publicly available

document, and is to include the information required by the regulations.

(5) This section extends to a

meeting that is closed to the public.

Transport and Infrastructure Advisory

Committee Meeting

BUSINESS OF MEETING

1. Apologies

2. Declarations of Interest

– Pecuniary and Non-Pecuniary

3. Adoption of Minutes from

Previous Meetings

3.1 Transport

and Infrastructure Advisory Committee Meeting held on 13 June 2019

3.2 Extraordinary

Transport and Infrastructure Advisory Committee Meeting held on 1 October 2019

4. Staff Reports

Infrastructure Services

4.1 Building

Asset Management Plan..................................................................................... 4

4.2 Sealed

Road Condition Survey update and Road Revaluation progress..................... 136

Staff Reports - Infrastructure Services 4.1

Staff Reports - Infrastructure Services

Report No. 4.1 Building

Asset Management Plan

Directorate: Infrastructure

Services

Report

Author: Craig

Purdy, Asset Engineer

File No: I2019/1413

Summary:

Council has completed a full audit and condition assessment

of all council buildings. From this data a draft Buildings Asset

Management Plan has been created for general fund buildings.

|

RECOMMENDATION:

That the Transport and Infrastructure Advisory

Committee (TIAC) recommend that the draft Buildings Asset Management Plan be

adopted by Council.

|

Attachments:

1 Draft

Buildings Asset Management Plan 2019 to 2029 General Fund (excluding Caravan

Parks), E2019/37319 , page 7⇩

2 Buildings

Asset Management Plan Community Levels of Service Report 2019, E2019/39855 ,

page 107⇩

3 Buildings

Asset Management Plan Customer Levels of Service Infographic, E2019/39854 ,

page 133⇩

Background:

The Buildings

Asset Management Plan (E2019/37319) includes 166 buildings from the

general fund assets class (this excludes Caravan Parks where funds are

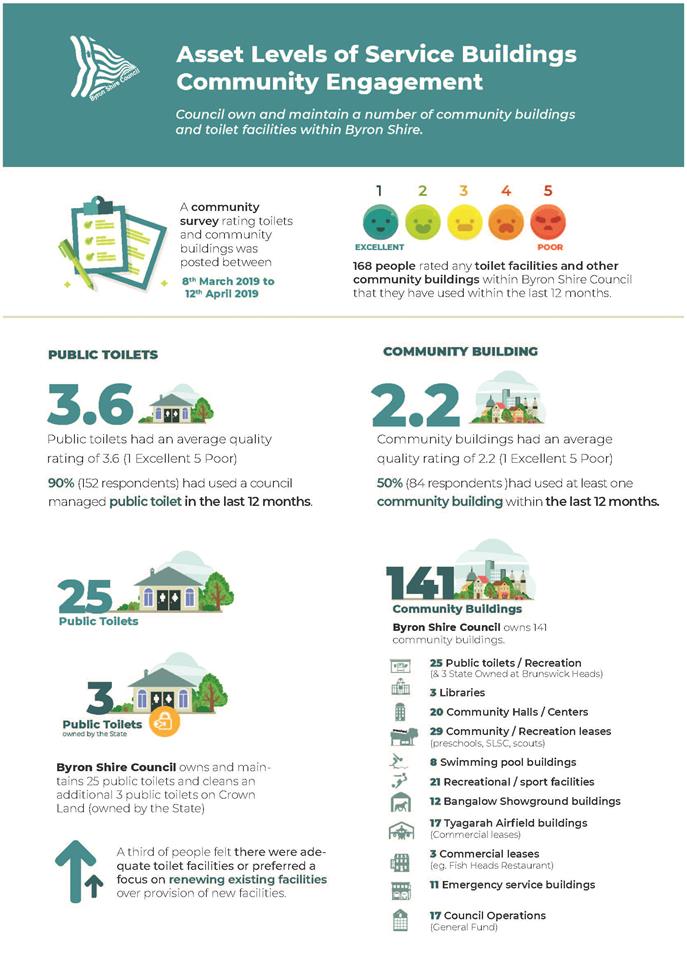

restricted and 3 State owned toilets at Brunswick Heads[1]). These include: public toilets, libraries,

community halls, community / recreation leases, swimming pool, recreation,

Bangalow showgrounds, Tyagarah airfield, commercial leases, emergency services

and Council operation buildings.

A

condition and defect audit was conducted in 2018/19 where 1,600 defects were

identified to prepare a Maintenance Plan and over 12,000 components were

condition assessed and modelled to develop an optimised Capital Works Plan.

|

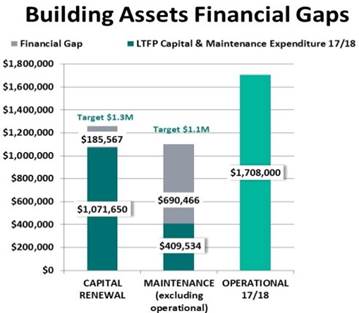

Our

present funding levels are insufficient to continue to provide existing

services at current levels in the medium term. This conclusion is made

from predictive modelling the current Long Term Financial Plan. Asset

modelling has established an annual capital

renewal gap of $185,567 and annual maintenance target of $1.1M.

There is a once off defect maintenance gap of $1.9M.

|

|

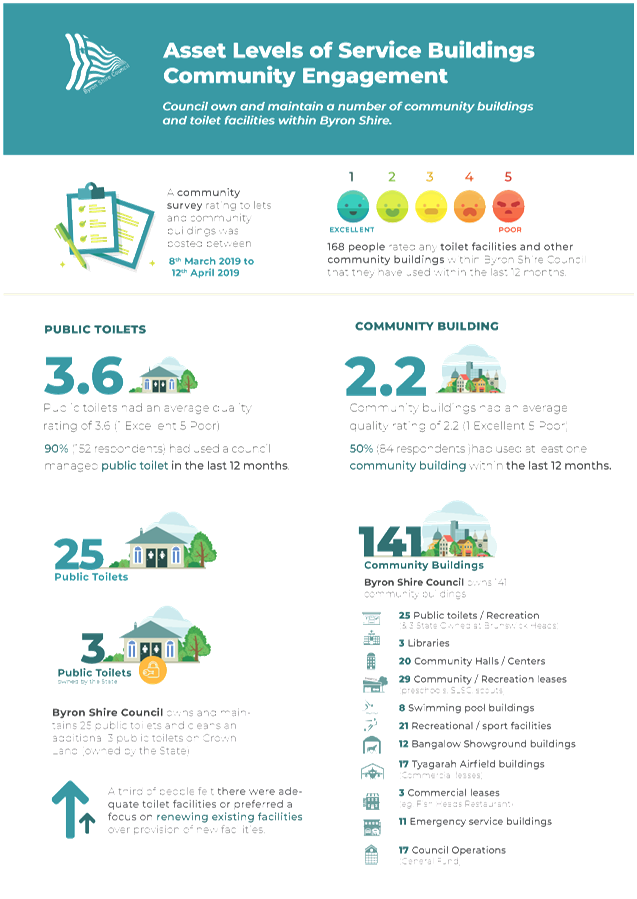

The

community were engaged and rated the ‘quality’ of the public

toilets at 3.6 and community buildings at 2.2 (1 excellent – 5 very

poor). The average ‘technical condition’ of the public toilets is

3.0 and the community buildings 3.3. There are 30% of the buildings in

a poor to very poor condition.

|

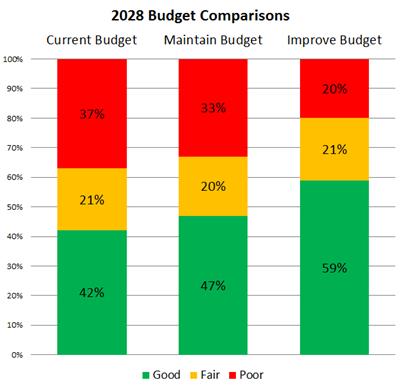

Three funding scenarios were modelled:

Scenario

1 – “Deteriorate” current Long Term Financial Plan

Scenario

2 – “Holding” budget

Scenario

3 – “Improve” budget

The

identified financial gaps indicate building condition and associated service

levels are already falling. This is evident with 30% of buildings in a

poor condition. For example, 1 statutory, 57 safety/

environmental/security defects and 94 structural defects identified. The

funding gaps, whilst challenging, are comparatively small relative to the gap

in roads funding.

Consultation:

The community have been engaged to measure the performance

and importance of the public toilets and community buildings via an online

survey from 8 March to 12 April 2019. The Community Buildings Customer

Levels of Service Survey results can be found in E2019/39855 and E2019/39854.

Staff Reports - Infrastructure Services 4.1 - Attachment 1

Byron Shire Council

Byron Shire Council

Buildings

Asset

Asset

Management

Plan

October

2019

Table of contents

Summary. 5

1. Executive Summary. 6

The

Purpose of the Plan. 6

Asset

Description. 6

Levels

of Service. 6

Future

Demand. 7

Lifecycle

Management Plan. 7

Financial

Summary. 7

Asset

Management Practices. 9

Monitoring

and Improvement Program.. 9

2. Purpose. 11

What

is Asset Management?. 11

Objective

of Asset Management 11

Benefit

of Asset Management 11

Related

Council Documents. 12

3. Current Position. 13

Building

Asset Stock. 13

Building

licenses and leases. 14

Emergency

Services (Rural Fire Services and SES) 14

Sports

Facility Buildings. 14

Swimming

Pool Buildings. 14

Tyagarah

Airfield. 14

Section

355 Committees. 15

Public

Toilets. 16

Replacement

Cost of Council’s Buildings Assets. 17

Present

Condition of Council’s Building Assets. 17

Building

Hierarchy. 19

4. Levels of Service. 21

Technical

Levels of Service. 21

Community

Levels of Service. 22

Community

Levels of Service Survey Key Findings. 23

Community

Hall Utilisation. 24

Levels

of Service Summary. 24

5. Future Demand. 27

Demand

Forecast 27

Demand

Management Plan. 27

New

Assets from Growth. 28

6. Asset Management Practices. 29

Financial

Systems. 29

Inspection

Processes. 29

Asset

Management Systems. 29

Changes

in Technology. 29

Accounting

Framework. 30

Standards

and Guidelines. 31

Risk

Management 31

7. Lifecycle Management Plan. 31

Asset

Capacity and Performance. 32

Useful

Lives and Unit Rates. 32

Asset

Valuations. 33

Asset

Condition. 33

8. Maintenance Plan. 33

Maintenance

and Inspection Program.. 34

Public

Toilet Future Maintenance Expenses. 35

Maintenance

Challenges. 36

9. Renewal Plan. 37

Renewal

Prioritisation. 37

Impact

of Deferring Renewal Works. 39

Managing

the Risks and Renewal Challenges. 40

Asbestos. 40

10. New and Upgrade Plan. 41

Selection

Criteria. 41

Developer

Contributions. 41

Forecast

Upgrade/New Expenditure. 41

11. Disposal of Assets. 42

Critical

assets. 42

12. Financial Summary. 43

Funding

Strategy. 43

Financial

Challenges and Gaps. 45

Financial

Useful lives. 45

13. Improvement Plan. 50

Glossary. 52

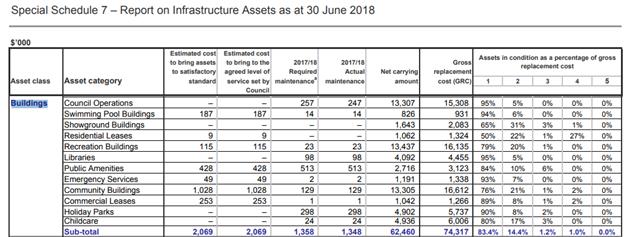

14. APPENDIX A Special Schedule 7 –

Buildings at 30 June 2018. 56

15. APPENDIX B – Licences & Leases. 57

16. APPENDIX C – Overall Building

Condition. 58

17. APPENDIX D – Capital Works Plan (3

years only) 59

18. APPENDIX E – Asset Levels of Service

Community Engagement 63

19. References. 90

Figures

Figure

1 Asset Management simplified. 11

Figure

2 Building Asset Stock. 13

Figure

3 Overall breakdown of depreciated replacement cost for Building Assets. 17

Figure

4 Building Assets by condition. 18

Figure

5 Building overall condition. 18

Figure

6 Customer & Technical Rating Comparison. 22

Figure

7 Public Toilet Technical Condition vs Customer Quality. 23

Figure

8 Customer Levels of Service Quality Ratings. 23

Figure

9 Community Hall Monthly Utilisation. 24

Figure

10 Top 3 Community Priorities (BSC Survey, 2016) 27

Figure

11 Asset Management Systems and Elements. 30

Figure

12 Asset life cycle stages. 31

Figure

13 Useful life consumption from financial register 32

Figure

14 Asset condition over useful life. 33

Figure

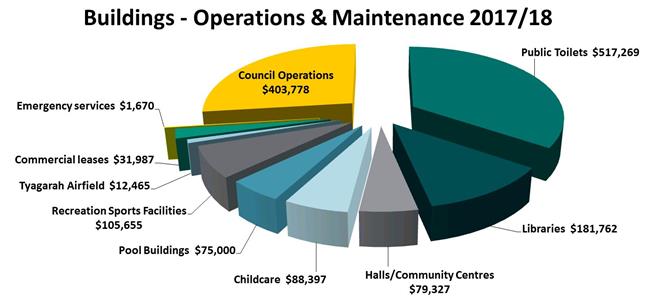

15 Buildings Operations & Maintenance Actuals 2017/18. 36

Figure

16 Capital Modelling Scenarios Compared. 38

Figure

17 Modelling Scenario 10 Year Condition Comparisons. 39

Figure

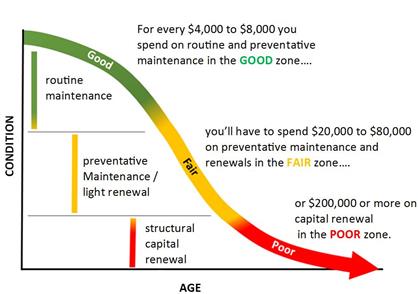

18 Building Deterioration and Maintenance Curve. 39

Figure

19 Maintenance & Capital Long Term Financial Plan (LTFP) 43

Figure

20 Useful Lives vs Capital Value Record. 45

Figure

21 Asset Maintenance Ratio General Fund SS7. 49

Figure

22 Infrastructure Backlog Ratio General Fund SS7. 49

Tables

Table

1 Related Council Documents. 12

Table

2 Public Toilet – Customer Levels of Service. 16

Table

3 Condition Grading Model 18

Table

4 Level of Service by Asset Category. 21

Table

5 Buildings Levels of Service – Community & Technical 25

Table

6 NSW population projections regional LG data. 27

Table

7 Demand management plan summary. 28

Table

8 Building Assets useful lives. 32

Table

9 Building asset valuation data (SS7 30 June 18) 33

Table

10 Maintenance & Inspection Program.. 34

Table

11 Public Toilet Operational and Maintenance over 3 years. 35

Table

12 Public toilet Operational and Maintenance tasks. 35

Table

13 Asset Predictor© Modelling Buildings. 38

Table

14 Critical Assets and Service Level Objectives. 42

Table

15 Capital Funding Assetic Predictor© Scenario 1 Deteriorate. 44

Table

16 Maintenance Funding LTFP vs Predictor© Modelling. 44

Table

17 Financial Gaps. 45

Table

18 Asset Consumption Ratios. 46

Table

19 Asset Sustainability Ratio Figures. 47

Table

20 Asset Renewal Funding Ratio Figures. 48

Table

21 Improvement actions summary. 50

Summary

Summary

The Buildings

Asset Management Plan (BAMP) includes 166 building from the general fund

assets class (this excludes Caravan Parks which funds are restricted and 3

State owned toilets at Brunswick Heads[2]).

They are: public toilets, libraries, community halls, community / recreation

leases, swimming pool, recreation, Bangalow showgrounds, Tyagarah airfield,

commercial leases, emergency services and Council operation buildings.

A

condition and defect audit was conducted in 2018/19 where 1,600 defects were

identified to prepare a Maintenance Plan and 12,000 components were condition

assessed and modelled to develop an optimised Capital Works Plan.

Our

present funding levels are insufficient to continue to provide existing

services at current levels in the medium term. This conclusion is made from

predictive modelling the current Long Term Financial Plan. Asset modelling has established an annual capital renewal gap of $185,567

and annual maintenance target of $1.1M. There is a once off defect

maintenance gap of $1.9M.

The community were engaged and rated the

‘quality’ of the public toilets at 3.6 and community buildings at

2.2 (1 excellent – 5 very poor). The average ‘technical

condition’ of the public toilets is 3.0 and the community buildings 3.3.

There are 30% of the buildings in a poor to very poor condition.

The community were engaged and rated the

‘quality’ of the public toilets at 3.6 and community buildings at

2.2 (1 excellent – 5 very poor). The average ‘technical

condition’ of the public toilets is 3.0 and the community buildings 3.3.

There are 30% of the buildings in a poor to very poor condition.

Three

scenarios were modelled:

Scenario

1 – “Deteriorate” current Long Term Financial Plan

Scenario

2 – “Holding” budget

Scenario 3 – “Improve” budget

Scenario 3 – “Improve” budget

Financial

gap indicates service levels are already falling. This is evident with 30 %

buildings in a poor condition. For example, 1 statutory, 57 safety/

environmental/security defects and 94 structural defects identified.

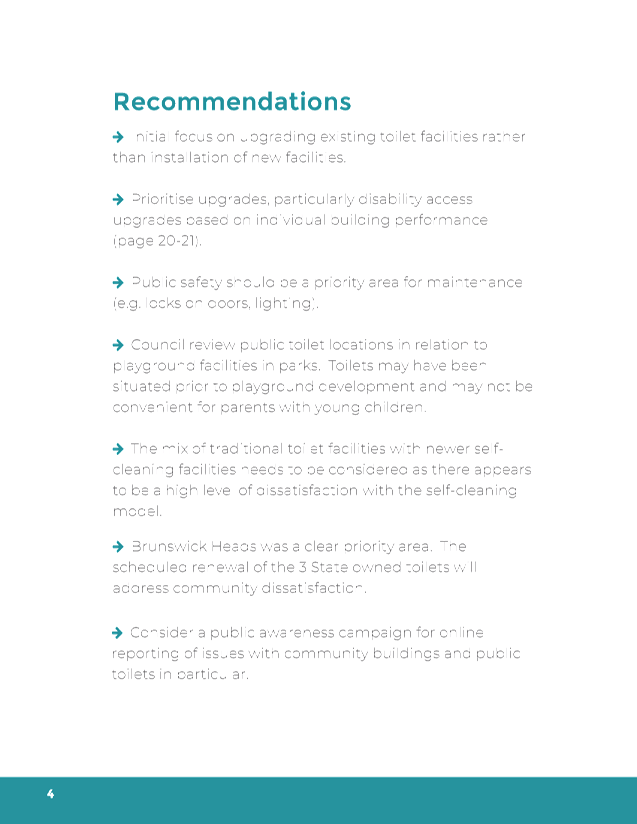

The

next step is to work on the improvement plan which will focus on:

· prioritise asset renewals over new or building upgrades

· address missing maintenance and inspection gaps such as

gutter maintenance

· plan public toilet renewals over the next 10 years with

consistent effort utilising the technical condition reports and community engagement

feedback

· utilise the optimised capital works plan

· address lease and licence gaps

· improve clarity of inspection and maintenance

responsibilities internally and externally

· optimise operational expenditures to increase available

funds for maintenance

1. Executive Summary

The Purpose of the Plan

Asset management planning is a comprehensive process to

ensure delivery of services from infrastructure is provided in a financially

sustainable manner.

This asset management plan details information about

infrastructure assets including actions required to provide an agreed level of

service in the most cost effective manner while outlining associated risks. The

plan defines the services to be provided, how the services are provided and

what funds are required to provide the services over a 10-year planning period.

The purpose of this Buildings Asset Management Plans is to inform the Byron

Shire Council’s Long Term Financial Plan.

Asset Description

Byron Shire

Council’s (BSC) building assets enable the community to access and enjoy

a range of services and facilities that Byron has to offer. It has an asset

replacement value of $74.3 million for buildings, as at 30 June 18. The

efficient management of the building assets is vital to the community. Buildings

are defined as being a roof structure with walls; they do not include shelter

or shade structures. This Buildings Asset Management Plan (BAMP) includes the

following 166 building categories from the general fund assets class

(this excludes Caravan Parks which funds are restricted and 3 State owned

toilets at Brunswick Heads[3]):

Levels of Service

Our present

funding levels are insufficient to continue to provide existing services at

current levels in the medium term. This conclusion is made from predictive

modelling the current Long Term Financial Plan (Refer to 1.6 Financial

Summary).

The main

services consequences are:

è Public toilets maintenance service will not improve to a

standard that the community expect.

è Public toilet capital renewal is possible over the long

term if current toilets are replaced with low cost kit style toilets and not

expensive self-cleaning toilets like those in Byron Main Beach Park.

è Community buildings have insufficient funds to accommodate

renewal requirements and no new or upgrading of facilities.

è Some building categories have no dedicated funds for

maintenance or capital renewals e.g. Bangalow Showground, Tyagarah Airfield,

and Emergency Services.

è Upgrades and new assets will rely upon grant funding.

Future Demand

The main demands

for new services are created by:

è Population growth

è Changing community expectations

è Development

è Changes in demographic

è Strategic network extensions and upgrades

These will be

managed through a combination of managing existing assets, upgrading of

existing assets and providing new assets to meet demand and demand management.

Demand management practices include non-asset solutions, insuring against risks

and managing failures.

è Fund priority works by seeking grant funding and

implementing the Developer Contributions Plan

è Educate the community on the costs associated with

maintaining current service levels and increased costs required with increased

assets

è Consult with community on options and funding requirements.

è Inform community and manage expectations. Communicate

levels of service and financial capacity to balance infrastructure priorities

with what the community is prepared to fund.

è Monitor and manage development controls.

è Undertake infrastructure planning taking into account land

use changes.

Lifecycle Management Plan

What does it Cost?

The

projected outlays necessary to provide the services covered by this Asset

Management Plan (AMP) includes operations, maintenance, renewal, upgrade and

new assets over the 10-year planning period is $2,589,760 on average per

year.

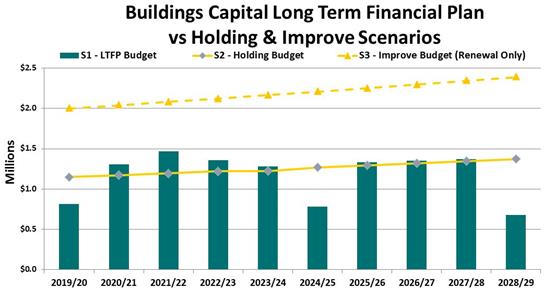

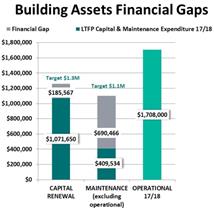

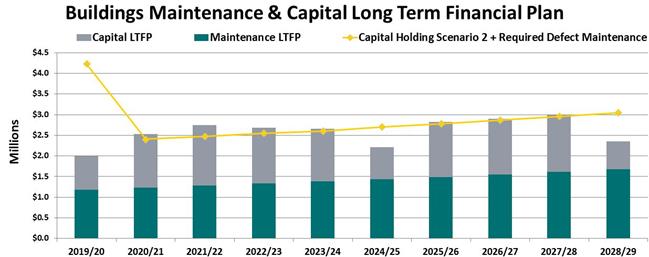

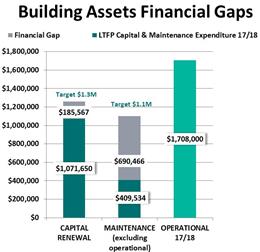

Financial Summary

What

we will do?

In the

financial year of 2017/18 Council spent $409,534 on maintenance, $1,708,000

on operational activities. It spent $1,543,790 on capital renewals

and upgrades for building assets. Based on the Assetic Predictor©

modelling for capital renewals only needs average at $1.3M over

10 years to hold / maintain the overall condition of the building portfolio.

This work is for capital renewal of assets only and does not account for new or

upgrades to building assets.

Estimated

available funding for this period is $1,074,650 annually in the long

term financial plan. This is insufficient to sustain the current level of

service.

The

infrastructure reality is that what is funded in the long term financial plan

is not going to hold / maintain the assets and overall the condition will

decline with current funding. The emphasis of the Asset Management Plan is to

communicate the consequences that this will have on the service provided and

risks, so that decision making is “informed”. The modelling scenarios

in this plan needs to inform the Council’s Long Term Financial Plan.

The

allocated funding leaves a shortfall of $185,567 on average per year of the projected expenditure required

to provide services in this plan compared with planned expenditure currently

included in the Long Term Financial Plan (LTFP).

A complete audit of the buildings and has identified 1,600 identified defects

to bring assets to a satisfactory standard. This is estimated at $1.9

million and is currently unfunded[4].

This is shown in the Projected Maintenance /

Operational and Capital Expenditure and the Financial Gaps figures over the

page with the maintenance gap illustrated in the first year.

Projected Maintenance

/ Operating and Capital Expenditure

Financial

gap indicates service levels are already falling. This is evident with 30 %

buildings in a poor condition. For example, 1 statutory, 57

safety/environmental/security defects and 94 structural defects

identified.

We plan to provide Building services for the following:

è Operation, maintenance and renewal of buildings to meet

service levels set by in annual budgets.

è In 2019/20 Council has allocated $60,000 to the Brunswick

Memorial Hall for a commercial kitchen upgrade. This is the only capital

upgrade within the 10-year planning period.

What we cannot do?

We currently do not

allocate enough funding to sustain these services at the desired standard or to

provide all new services being sought. Works and services that cannot be

provided under present funding levels are:

è Upgrade or provide new buildings

Managing the Risks?

Our present

funding levels are insufficient to continue to manage risks in the medium term.

The main risk

consequences are:

è Gutters and downpipe replacement is not being addressed

when needed resulting in water damage to the internal and or external walls.

è Roof replacement not complete when needed resulting in

water damage to the ceiling, fitout and fittings, and carpets. This can cause

mould damage and require relocation of users until addressed e.g. Mullumbimby

Administration Building.

è Programmed asbestos replacement to comply with Australian

Standards e.g. replacing internal wall sheeting, soffits, eaves, and flooring

in community Halls etc. (Marvel Hall)

è Closing of buildings such as public toilets that become

unsafe for use.

è Air condition systems requiring replacement increase

reactive maintenance and operational costs e.g. Mullumbimby Administration

Building

è Public toilets that are reaching overall poor condition are

still operational, however, the community are very dissatisfied with the level

of service. This is a perceived public perception is a risk.

è Budgets are not allocated to building categories as defined

in this plan. As such deferred renewals are likely and maintenance issues not

being addressed.

We will

endeavour to manage these risks within available funding by:

è Maintaining an asbestos register

è Amend leases and licences to ensure general maintenance

e.g. gutters cleaning is detailed

è Review brining forward air condition renewals at

Mullumbimby Administration Building

è Provide high risk defects for maintenance repairs

Asset Management Practices

Our systems to

manage assets include:

è Authority Asset Register, Capital Value Record Module and

Work Orders

è Asbestos Register

è Geographical Information Systems to identify and map all

buildings

è A contracted centralised Fire Protection web services

è Predictor© Modelling to inform the long term capital

works program

è Reflect mobile solutions to inspect assets

Since the 2019

asset inspection assets requiring renewal/replacement are identified from

defect repairs in the Building Maintenance Plan and 10 year capital from the

modelling software. This is to improve the process and apply a planned asset

management response.

Monitoring

and Improvement Program

The next steps resulting

from this asset management plan to improve asset management practices are:

è Specialised inspections as required e.g. asbestos, pest

extermination

è Further refine renewal forecasts based on condition audits

using Assetic Predictor© to provide continuous improvement

è Council approval/endorsement of this Plan to communicate

levels of service and a commitment to process improvement

è Develop unit rates to calculate required maintenance for

all asset sub-types e.g. gutters, roof, carpet, roller doors etc.

è Formalise the new, renewal and disposal policies,

è Test current levels of service to determine if

they’re achievable

It should be

noted that this Asset Management Plan is not a stand-alone document and is

closely related to Council’s Strategic Asset Management Plan and other

significant Council documents. Council will measure the effectiveness and

application of the asset management plan through:

è Stakeholder consultation

è Regular condition and maintenance inspections

è Continued use of Assetic Predictor© to predict renewal

requirements

è Continuous review and improvement to asset management

practices

è Key Performance Indicators (KPI) monitoring and recording

of customer levels of service

Key Findings

The financial challenge is to address the one off defect

maintenance gap of $1.9M.

Asset modelling has established an annual capital renewal gap of $185,567 &

annual maintenance target of $1.1M.

To “hold / maintain” the overall building portfolio

condition

the average capital renewal needs to be $1.3M annually.

The actual maintenance budget averages at $410,000 (excluding operational costs).

The buildings had an operational cost of $1,708,000 in 2017/18.

Asset Management needs to balance Levels

of Service & whole of life cycle costs.

30% of buildings are in a poor condition.

The community rated the quality of

Public toilets 3.6 & community buildings 2.2.

The technical condition of public

toilets 3.0 & community buildings 3.3

(1 Excellent and 5 Very Poor)

The community expectation of Public

Toilets is higher than what

current budgets can afford over the Long Term Financial Plan.

Asset management systems are well

established & integrated,

however, work is required in the Work

Order system to improve splits between maintenance and operational costings.

Byron leads asset management with the

latest technology and innovation.

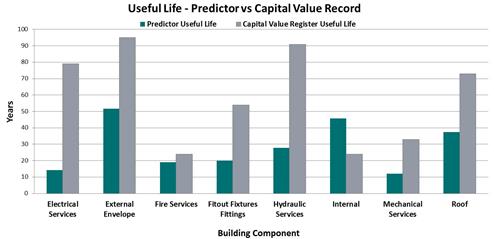

The average ‘useful life’ is lower than industry standard

due to deferred renewals and reduced

preventative maintenance.

Spending on building upgrades reduces

the ability to optimise on required capital renewals, this results in deferring on renewals

and will result in higher future capital expenditure.

There are 19 items identified in the Improvement Plan.

2.

Purpose

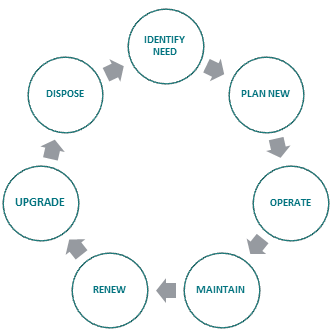

What is Asset Management?

Asset

management is the planning, acquisition, operation, maintenance, renewal and

disposal of assets. In simple terms, asset management is about the way in which

assets are looked after, both on a day-to-day basis (i.e. maintenance and

operations) and in the medium to long-term (i.e. capital renewal and forward

planning). Asset management ensures that Council’s assets are capable of

providing services, of an agreed quality, in a sustainable manner, for present

and future communities.

This

asset management plan is prepared to meet legislative and organisational

requirements for sustainable service delivery and to inform long term financial

planning and reporting.

Objective of Asset Management

Good

asset management takes a proactive approach to asset maintenance and planning

in order to avoid costly and dangerous asset failure.

This

asset management plan aims to meet the required levels of service in the most

cost-effective way for present and future communities (Figure 1).

Asset Management needs to balance Levels of Service

and

whole of life cycle costs.

Figure 1 Asset Management

simplified

Benefit of Asset Management

Asset

management delivers benefits in improved accountability, sustainable service

delivery, risk reduction and financial management and forecasting.

Improving

Council’s asset management practices will enable optimised spending by

doing more with less through knowing what assets we own, what condition

they’re in and by monitoring the effect of our actions.

Doing more with less.

Related

Council Documents

This

Buildings Asset Management Plan sets out the implementation of Council’s

Asset Management Strategy for the long-term management of its building assets

in a financially responsible manner. It determines recommended service levels,

inspection regimes and proactive maintenance routines to keep the building

assets in safe and serviceable conditions. In order to do this effectively,

other Council policies, strategies and plans have been considered to determine

their impact on this Asset Management Plan and ensure overall alignment.

Table 1 Related Council Documents

|

Key

Council Documents

|

Relationship

|

|

Strategic

Asset Management Plan (SAMP) - E2016/100839

|

Outlines

the framework for the management of Byron Bay Council’s General Fund

Infrastructure assets to deliver Council’s Vision.

|

|

Halls

and Venues Guidelines for S355 Committees and Boards (E2016/79739)

|

Outlies

the guidelines for hall volunteers maintenance responsibilities etc.

|

|

Byron

Shire Developer Contribution Plan 2012 (Section 94) - E2015/540

|

Links

to Future Demand, Section 6.

|

|

IPART

Determination of Council’s Application for Special Variation for

2017-18 – E2017/54521

|

Links

to the Financial Statement Projections and Funding Strategy, Section 13.

|

|

IPART

Application of Councils Special Variation for 2017-18 – E2017/15274

|

Links

to the Customer Levels of Service tables, Section 5.

|

|

Workforce

Plan 2017-2021 – E2017/19709

|

Links

to Renewal, New and Upgrade Plan.

|

|

Long

Term Financial Plan 2016-2026 – E2017/8695

|

Links

to the Financial Statement Projections and Funding Strategy, Section 13.

|

|

Transport

and Infrastructure Advisory Committee

|

Defines

the adopted sealed roads levels of service

|

|

Community

Consultation and Engagement Report – Funding our Future - E2017/80803

|

Document

that relays the key findings of the communities’ expectations of

council, it was created for the community engagement and awareness strategy

for the Special Rate Variation.

|

|

Final

Published Byron Shire Council Financial Statements 30 June 2018 (E2018/85029)

|

Useful

Lives

|

|

Buildings

Maintenance Plan 2019 (E2019/20878).

|

Building

Maintenance Plan Section 8.

|

|

Community

Buildings Customer Levels of Service Survey E2019/39855 and E2019/39854

|

Customer

Levels of Service Section 4

|

3.

Current Position

Building Asset Stock

Byron

Council manages 166 general fund buildings. This Asset Management Plan takes

into consideration all Council building assets as follows and excludes 3

toilets that are State Owned at Brunswick Heads[5].

Figure 2 Building Asset Stock

Building licenses and leases

Council

has 5 licenses and 36 leases over sites that contain buildings (Appendix B). In

some cases there may be multiple leases for one building when rooms are

separately leased. Many of the leases are ‘holding over’ which

means they operate on a month to month basis.

For

lease buildings Council is responsible for the building structure. Prior to a

lease being prepared an inspection is carried out and a “dilapidation

report” prepared.

Council

holds a lease as a monthly tenant with the State Rail Authority for the Rural

Fire Service Fire Station Billinudgel. The terms of the lease require

Council to maintain and keep the premises in good and substantial condition and

repair, and fence appropriately.

Emergency Services (Rural Fire Services

and SES)

Council

has 11 Emergency Services buildings on its land and has management

responsibility for all 11 buildings. However, the maintenance responsibilities

are not defined by a lease or licenses which details these responsibilities, as

per the Maintenance Plan, Section 8.

Sports Facility Buildings

Council

has 20 individual sporting facility buildings across 10 sports fields. Council

does not issue leases or licences to users, however a Sports Field User

Agreement is signed at the change of seasons. In this document the ‘Facility’

means the change rooms, toilets, canteen, kiosk and clubhouse. The

Agreement detail users’ maintenance responsibilities and states that all

structural, electrical switchboards, roof harness and fire activities are the

responsibility of Council. As per the Maintenance Plan, Section 8 (Table 10), the

‘Sports Field User Agreement’ should define responsibilities for

the following maintenance activities:

· Window cleaning

· On site management systems & grease traps

· Painting

· Roller doors/gates

· Roof and gutter cleaning

· Back flow prevention devices

This

item has been added to the Improvement Plan, Section 13.

Swimming Pool Buildings

Council

has 2 swimming pool facilities located at Byron Bay and Mullumbimby. These

facilities operate under 3 year contracts. The responsibilities are defined as

per the Maintenance Plan, Section 8.

Tyagarah Airfield

Council

has 17 buildings at the airfield with 16 that have commercial leases and one

with a Hire Agreement (the Aero Club next to the disused hanger). These

commercial leases are all “holding over” until such time

that Council determines the long term strategic plan for the facility (Appendix

B Lease List).

Section 355 Committees

Thirteen

Council buildings are managed by Section 355 Committees with authority

delegated by Council under S377 of the Local Government Act. They manage

bookings, hiring, collection of hire fees and bonds, and undertake minor

maintenance. All finances are managed via a monthly reconciliation to Council.

The

buildings are:

1. Bangalow

A & I Hall

2. Bangalow

Showground

3. Brunswick

Heads Memorial Hall

4. Brunswick

Valley Community Centre

5. Durrumbul

Hall

6. Heritage

House Bangalow

7. Lone

Goat Gallery

8. Marvell

Hall

9. Mullumbimby

Civic Hall

10. Ocean

Shores Community Centre

11. South

Golden Beach Hall

12. Suffolk

Park Community Hall

13. Bangalow

Heritage House

General

Terms of Reference

· To maximise income and promote optimum usage of the

facility.

· To care for and maintain the facility, through responsible

day to day management.

· To ensure the safety of the patrons, contractors and

volunteers at the facility.

· To provide short and long-term strategic marketing

direction for the facility.

· To ensure compliance with Council policies and all relevant

legislation.

· To ensure compliance with Council's adopted fees and

charges, Work, Health and Safety and other legislation relevant to the

operations of the facility.

· To provide recommendations to Council for function

improvements and/or upgrades to the facilities.

· To source and secure grant funding opportunities for Council's

consideration.

· To plan and undertake fund raising activities as required.

· To develop procedures for equity of access to the

facilities for the local community.

· To ensure that negative impacts on the environment and

neighbours are minimised.

· To strive for a "break-even" or profitable annual

financial position (after all operational, short and long-term maintenance,

building insurance and other costs).

Asset

maintenance responsibilities are detailed in Section 8, of the Halls and Venues

Guidelines for S355 Committees and Boards (E2016/79739). Simply the committees

are responsible for general maintenance and Council is responsible for

structural long term capital renewals as well as health and safety

requirements, accessibility and inclusion, compliance matters, asset protection

(asset management planning e.g. re-roofing, external painting, structural

inspections etc., security, and regular fire equipment inspection).

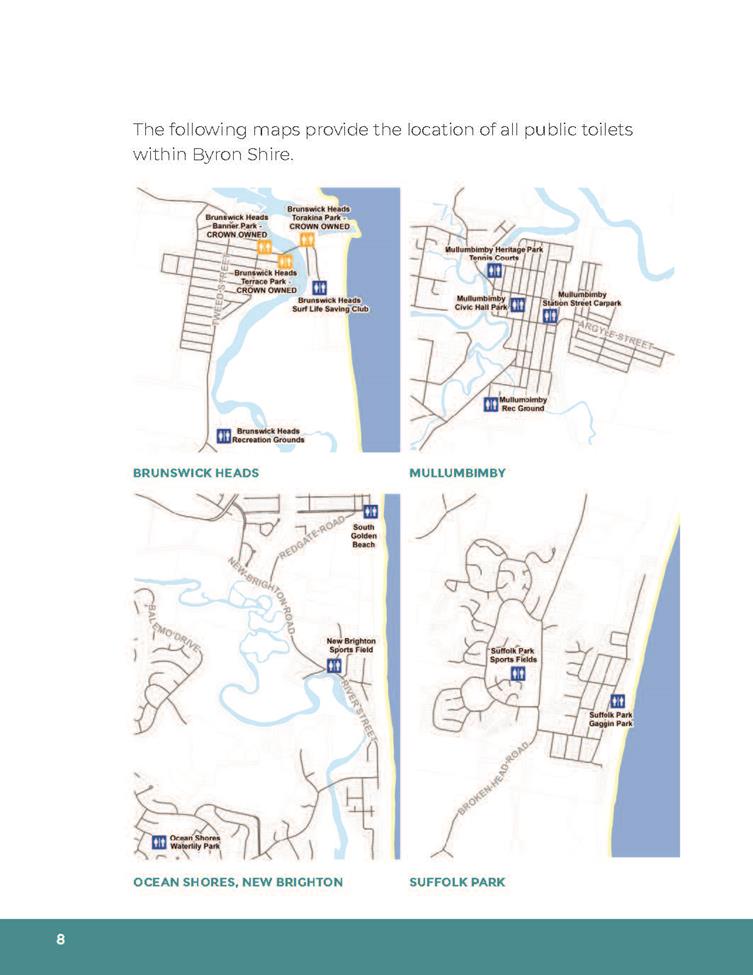

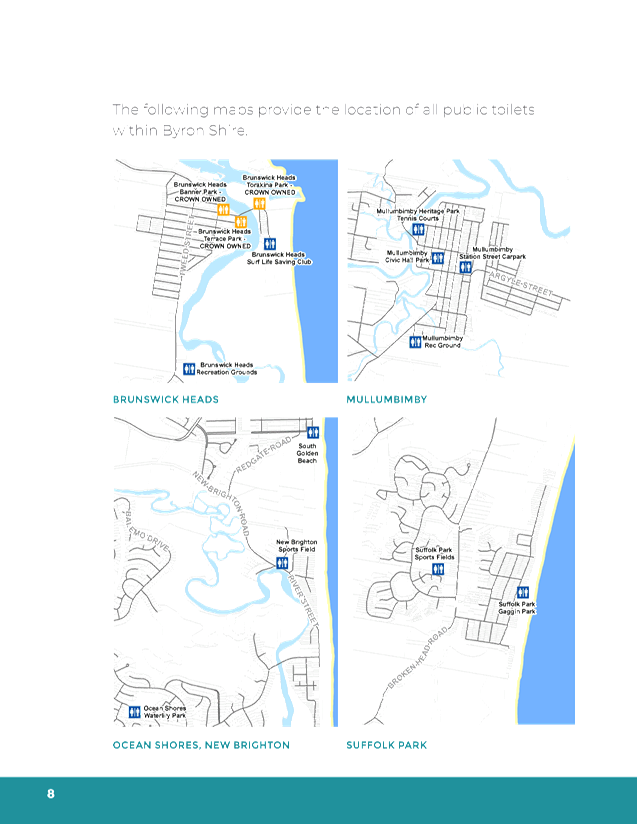

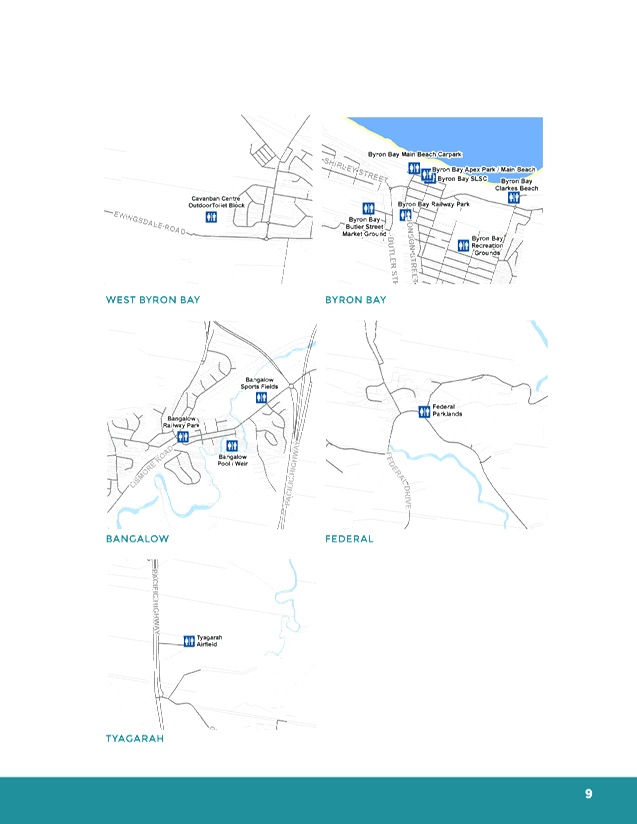

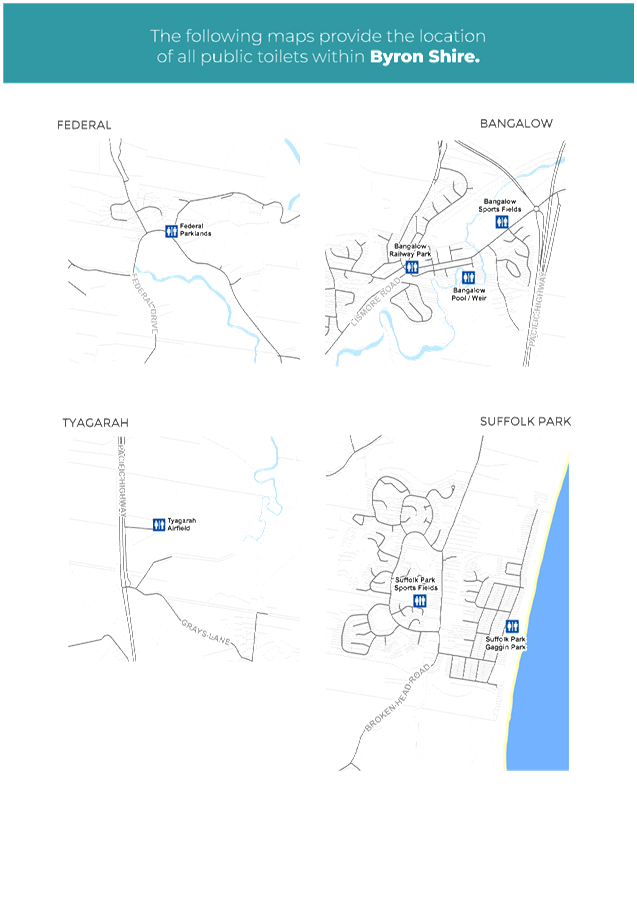

Public Toilets

Council

has 28 public toilets. There are 3 Crown owned public toilets at Brunswick

Heads, Torikina, Banner Park and The Terrace. The community perceives these as

Council owned and managed toilets. However these toilets are only cleaned by

Council and long term capital renewal is the responsibility of the Reflections

Holiday Park Board. Associated issues have been noted in the Improvement Plan,

Section 13.

Management

of the Council public toilets is split across Council departments. Cleaning is

managed by Utilities Services, daily maintenance such as

hygiene/plumbing/vandalism etc. is managed by Social & Cultural Planning

and building ownership sits with Open Spaces. Responsibility for long term

capital management is not currently defined by the organisation. Customer

levels of service vary depending upon location and usage. Six public toilets

are not currently Disability Access Act (DDA) compliant. This is detailed in

Table 2 below.

Table 2 Public Toilet –

Customer Levels of Service

|

Toilet

|

Manual Cleaning Service Frequency

|

Hygiene Services Frequency

|

Level of Service (1-5)

|

DDA

|

|

Brunswick Heads Banner Park - CROWN OWNED

|

Daily,

twice daily in peek

|

Monthly

|

1

|

YES

|

|

Brunswick Heads Terrace Park - CROWN OWNED

|

Daily,

twice daily in peek

|

Monthly

|

1

|

YES

|

|

Brunswick Heads SLSC - CROWN BSC

|

Daily,

twice daily in peek

|

Monthly

|

1

|

NO

|

|

Byron Bay Clarkes Beach - CROWN BSC

|

Daily,

twice daily in peek

|

Monthly

|

1

|

YES

|

|

Brunswick Heads Torakina Park - CROWN OWNED

|

Daily,

twice daily in peek

|

Monthly

|

1

|

YES

|

|

Byron Bay Main Beach Carpark - CROWN BSC

|

Daily,

twice daily in peek

|

Monthly

|

1

|

YES

|

|

Byron Bay SLSC - CROWN BSC

|

Daily,

twice daily in peek

|

Monthly

|

1

|

YES

|

|

Byron Bay Apex Park/Main Beach - CROWN BSC (Exeloo self cleaning

every 500 uses)

|

Daily,

twice daily in peek

|

Twice Weekly

|

1

|

YES

|

|

Byron Bay Railway Park

(Exeloo self cleaning every 500 uses)

|

Daily,

twice daily in peek

|

Twice Weekly

|

1

|

YES

|

|

Byron Bay Apex Park/Main Beach - CROWN BSC (Exeloo self cleaning

every 500 uses)

|

Daily,

twice daily in peek

|

Twice Weekly

|

1

|

YES

|

|

Suffolk Park Gaggin Park

|

Daily

|

Monthly

|

2

|

YES

|

|

South Golden Beach

|

Daily

|

Monthly

|

2

|

YES

|

|

Bangalow Railway Park

|

Daily

|

Monthly

|

2

|

YES

|

|

Bangalow Pool / Weir

|

Daily

|

Monthly

|

2

|

YES

|

|

Mullumbimby Civic Hall Park

|

Daily

|

Monthly

|

2

|

YES

|

|

Byron Bay Recreation Grounds

|

Daily

|

Monthly

|

2

|

NO

|

|

Mullumbimby Rec Ground - CROWN BSC

|

Daily

|

Monthly

|

2

|

NO

|

|

Mullumbimby Station Street Carpark

|

Daily,

twice daily in peek

|

Monthly

|

2

|

YES

|

|

Bangalow Sports Fields - Community Land

|

Daily

|

Monthly

|

2

|

YES

|

|

New Brighton Sports Field

|

Daily

|

Monthly

|

2

|

YES

|

|

Ocean Shores Waterlily Park

|

Weekly

|

Monthly

|

3

|

YES

|

|

Mullumbimby Heritage Park Tennis Courts

|

Weekly

|

Monthly

|

3

|

YES

|

|

Brunswick Heads Recreation Grounds - CROWN BSC

|

Weekly

|

Monthly

|

3

|

YES

|

|

Federal Parklands - CROWN BSC

|

Weekly

|

Monthly

|

3

|

NO

|

|

Suffolk Park Sports Fields

|

Weekly

|

Monthly

|

3

|

YES

|

|

Tyagarah Airfield

|

Weekly

|

Monthly

|

3

|

NO

|

|

Byron Bay Butler Street Market Ground

|

Weekly

- Wednesdays

|

Monthly

|

3

|

NO

|

|

Cavanbah Centre (Sth Toilet Block)

|

Weekly

|

Monthly

|

3

|

YES

|

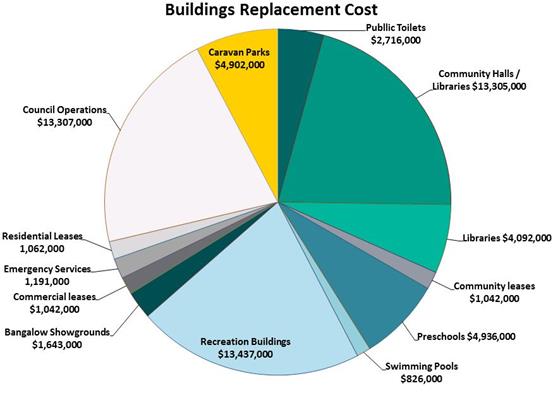

Replacement Cost of Council’s

Buildings Assets

The

replacement value of Council’s building asset portfolio is $74.3

million with a written down cost of $62.7 million. The annual

depreciation is $993,863 as at 30 June 2018. The break-up of

Council’s Building asset portfolio by replacement value is illustrated in

the following diagram.

Figure 3 Overall breakdown of

depreciated replacement cost for Building Assets

Present Condition of Council’s

Building Assets

The

work undertaken to develop this Plan identified 1523 defects. By understanding

the condition of Council’s assets and the various types of impact that

affect them, Council is better placed to seek to maintain a level of service

that meets community expectations and minimise the risk of asset failure. Asset

failures can lead to legal liability if Council is found to have acted

unreasonably in the management of its assets.

There

are many reasons why assets fail/deteriorate to the point where they do not

meet performance standards and community expectations, including e.g. a lack of

maintenance. The following identify the asset criticality categories based on

the identified defects:

· Functional (874) e.g. clearing of gutters, water damage, rotting

timbers

· Aesthetics (497) e.g. water damage, mould, holes, graffiti,

cracked tiles

· Structural (94) e.g. beam corrosion, movement, column

cracks, timber rotting

· Safety/Environmental/Security (57) e.g. Disability access

non compliance, trip hazards, window locks not working, missing fire

extinguisher, exit not illuminated, asbestos

· Statutory (1) e.g. loose wires on Byron Surf Club veranda

Each

building element was individually condition assessed then an overall condition

was determined for each building using a complex weighted average condition

score. Refer to Appendix C for this formula calculation. Table 3 Condition

Grading Model, is a general condition grading model that explains each

description of condition using a 1 to 5 grading score that is consistent across

all asset types in Council.

Table 3 Condition Grading Model

|

Condition Grading

|

Description of Condition

|

|

1

|

Excellent: Asset in excellent condition. No maintenance required.

|

|

2

|

Good:

Asset is in good condition

with limited signs of wear. Only requires cyclic maintenance and is not

requiring special attention.

|

|

3

|

Fair:

Asset is in useable

condition with extensive signs of wear. Asset requires some attention

to prevent further deterioration and to return it to a condition so that it requires

only cyclic maintenance.

|

|

4

|

Poor:

Asset is in poor condition

or is faulty. It needs urgent attention to return it to a useable condition

and or significant renewal/rehabilitation is required to reduce risk.

|

|

5

|

Very Poor: Asset has

failed or is at the end of its life or is physically unsound or poses

significant risk. It requires replacement and is beyond rehabilitation.

|

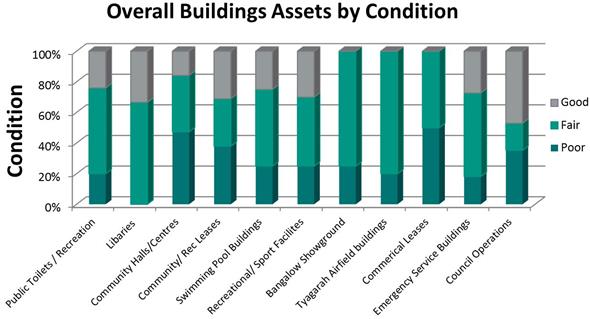

A

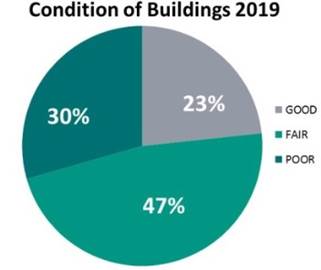

simplified model derived from Table 3 is set out in Figure 4 below. Condition

Excellent (1) and Good (2) have been combined into GOOD, and Poor (4) and Very

Poor (5) into POOR.

Figure 4 Building Assets by

condition

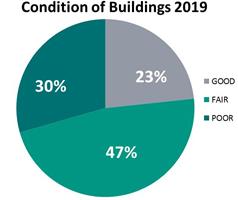

Figure 5 Building overall condition

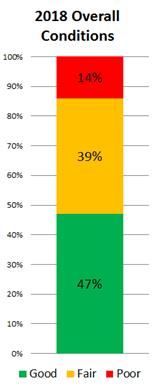

Overall

23% of Council’s buildings are in Good condition, 47% in Fair condition

and 30% in Poor condition (Figure 5). It is recommended that Council’s

strategic focus over the next 10 years should be on reducing the percentage in

poor condition.

30 % of buildings are in poor condition

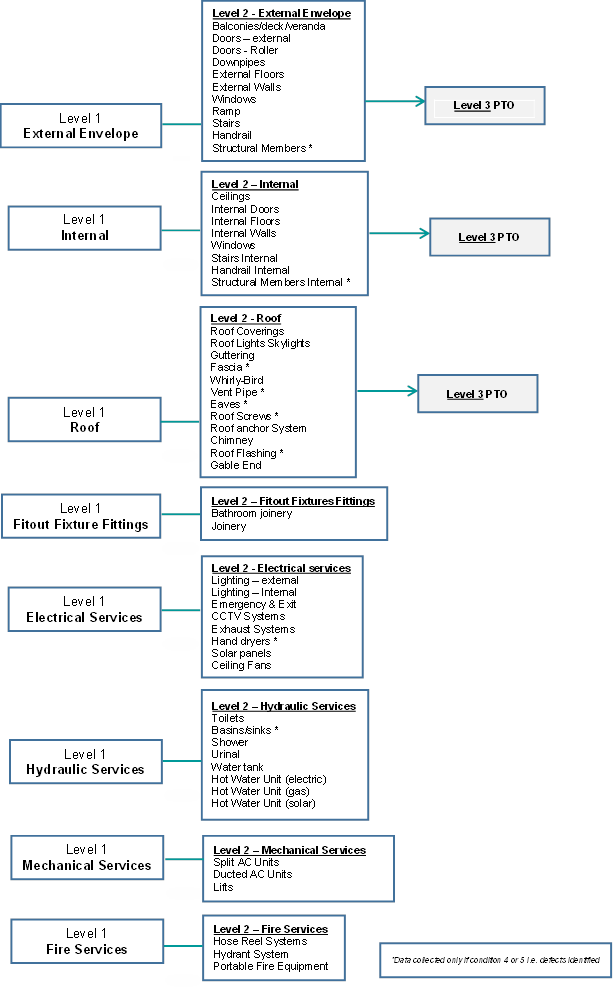

Building Hierarchy

Buildings are categorised into

Buildings are categorised into

the

following 3 levels. As the useful

lives

of elements differ, this

has

asset and financial implications.

4. Levels

of Service

A key

objective of this Asset Management Plan is to identify the current

‘Levels of Service’ (LoS) provided by Council’s asset

portfolio. The levels of service defined in this section will be used to:

· Clarify the level of service that our customers should

expect.

· Identify works required to meet these levels of service.

· Identify the costs and benefits of the services offered.

· Enable Council and customers to discuss and assess the

suitability, affordability and equality of the existing service level and to

determine the impact of increasing or decreasing this level in future.

The

levels of service for these Building Assets are based on legislative

requirements, customer research and expectations, and Council’s strategic

goals. There are two tiers of levels of service; Customer Levels of Service and

Technical Levels of Service.

Technical Levels of Service

Technical

Levels of Service are long term, tactical tools developed to measure, monitor

and manage functions of service over time with regard to quality of assets

managed, quantities of assets contributed or constructed, operational and

capital expenditure (Table 4 Level of Service by Asset Category).These

technical measures relate to the allocation of resources to service activities

that the organisation undertakes to best achieve the desired community outcomes

and demonstrate effective organisational performance. Legislative requirements,

infrastructure standards and industry guides combine to strongly influence

Technical Levels of Service. The following are also defined:

· New Assets, upgraded or reconstructed assets

· Maintenance – intervention points and responsiveness

Table 4 Level of Service by Asset Category

|

Level

Of Service

|

Importance Rating

|

Category

Primary Function / facility types

|

Score

|

|

1

|

High

|

Libraries

Child

care centres & preschools

Council

Administration Offices

Public

Toilet – Brunswick, Byron & Mullumbimby CBD’s

(cleaned daily & twice in peek periods)

|

>21

|

|

2

|

Medium High

|

Halls

(dependant on use)

Swimming

Pool Buildings

Public Toilets – High

visitation areas (cleaned daily)

|

10 - 15

|

|

3

|

Medium

|

Halls

(dependant on use)

Public

Toilets – moderate visitation (cleaned weekly)

Council

Operations - manned depots

Showground

Office Buildings

Tyagarah Airfield

|

5 - 9

|

|

4

|

Medium Low

|

Show

ground stalls, pavilions

Council

operations – unmanned

|

>1

|

|

5

|

Low

|

Storage

sheds & Garages

|

= 0

|

LoS =

(Development x Frequency) + Population (Refer to Appendix C for more detail).

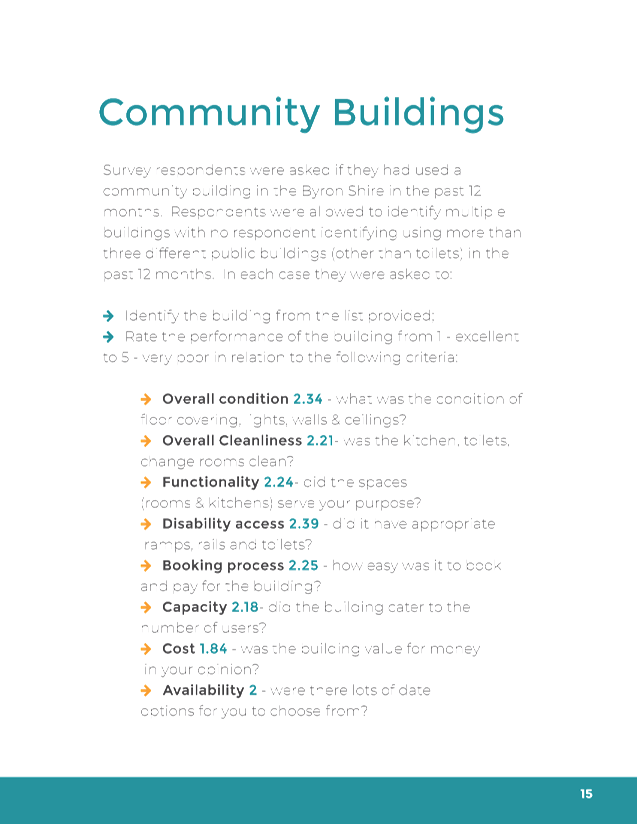

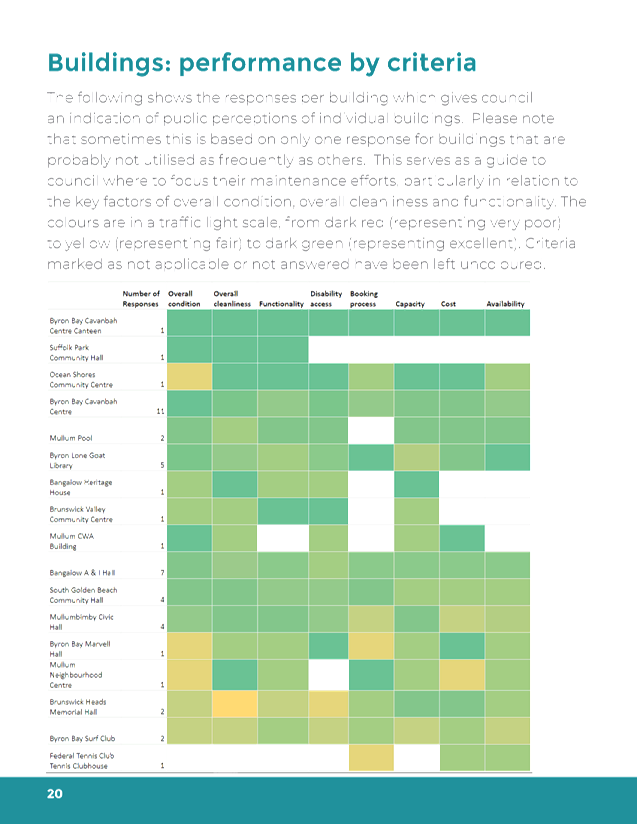

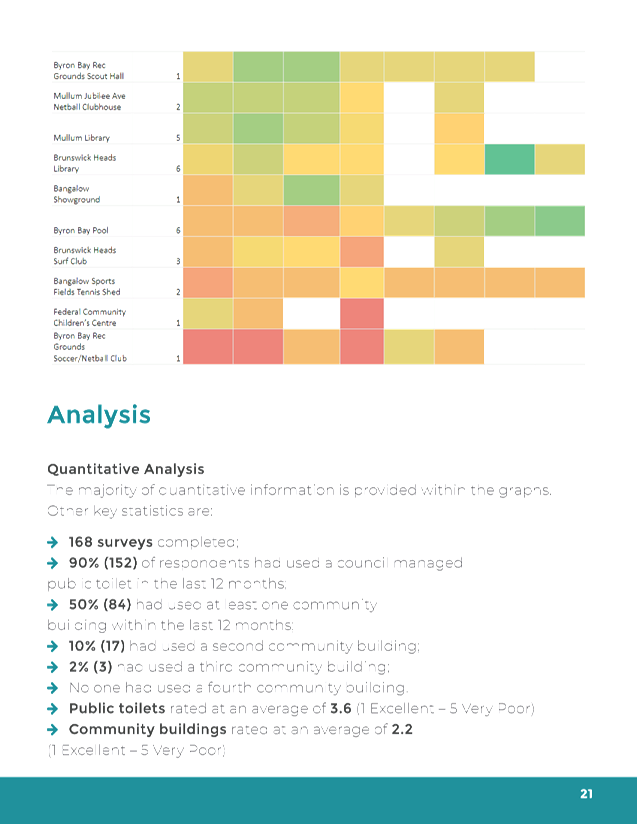

Community Levels of Service

Community

Levels of Service are a reflection of the Technical Levels of Service being

delivered to the community. They are derived through community engagement

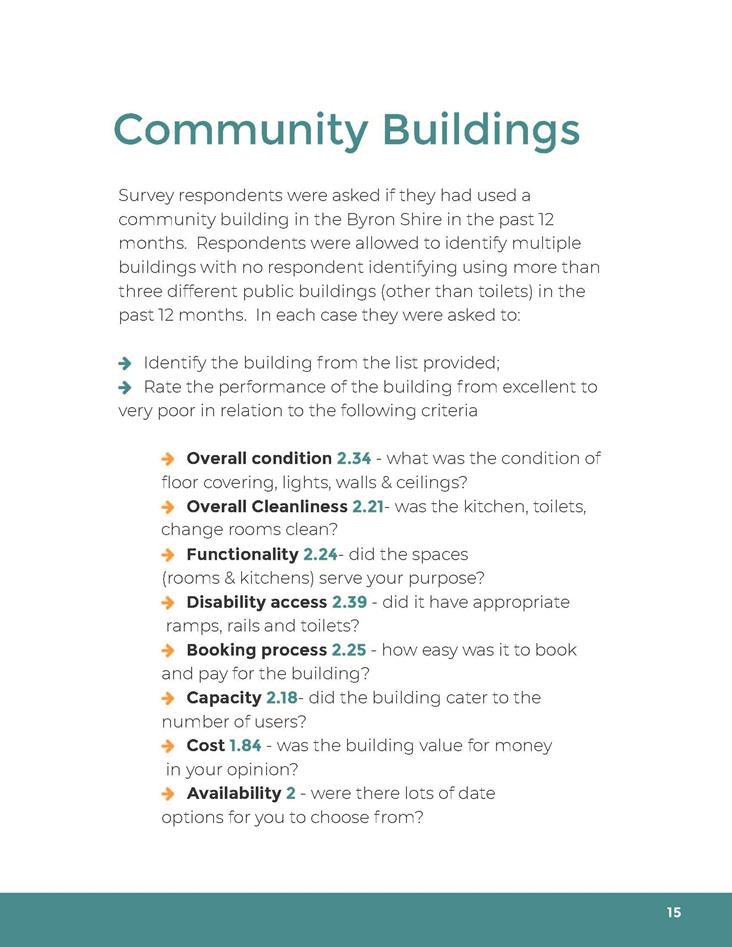

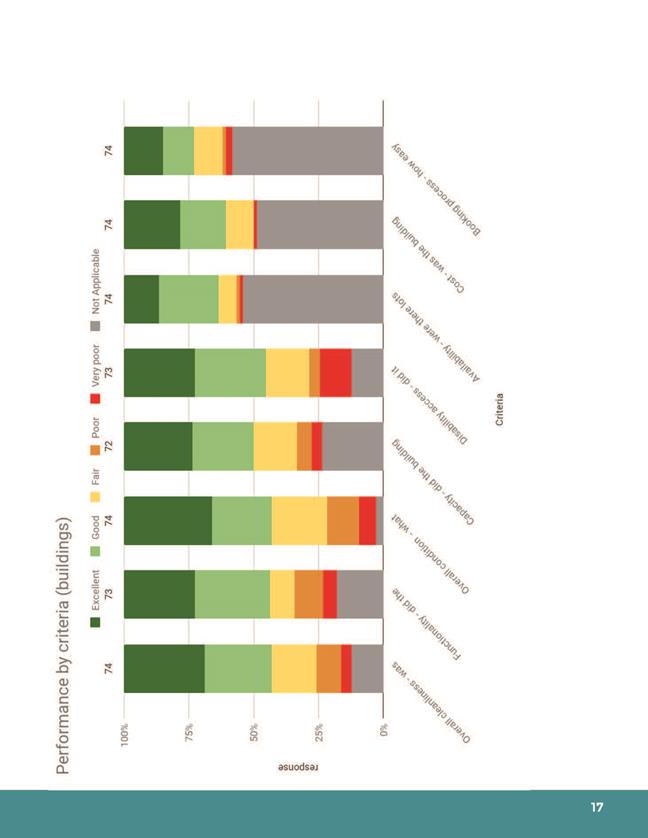

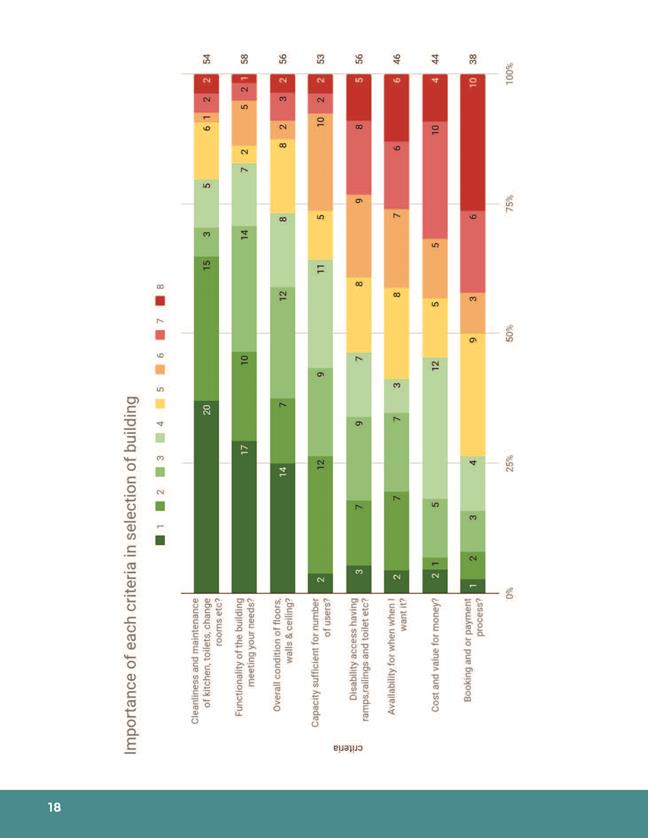

undertaken to better understand levels of satisfaction with service, service

utilisation and desired levels of service. Levels of Service may also be

derived from informal community feedback and complaints (see Table 5 on p 24).

Community

levels of service measures used in asset management planning are:

Quality How

good is the service?

Function Does

it meet users’ needs?

Capacity/Utilisation Is

the service usage appropriate to capacity?

A

Building Asset Management Survey was conducted to consult the community in

order to measure and rate the performance and importance of eight criteria

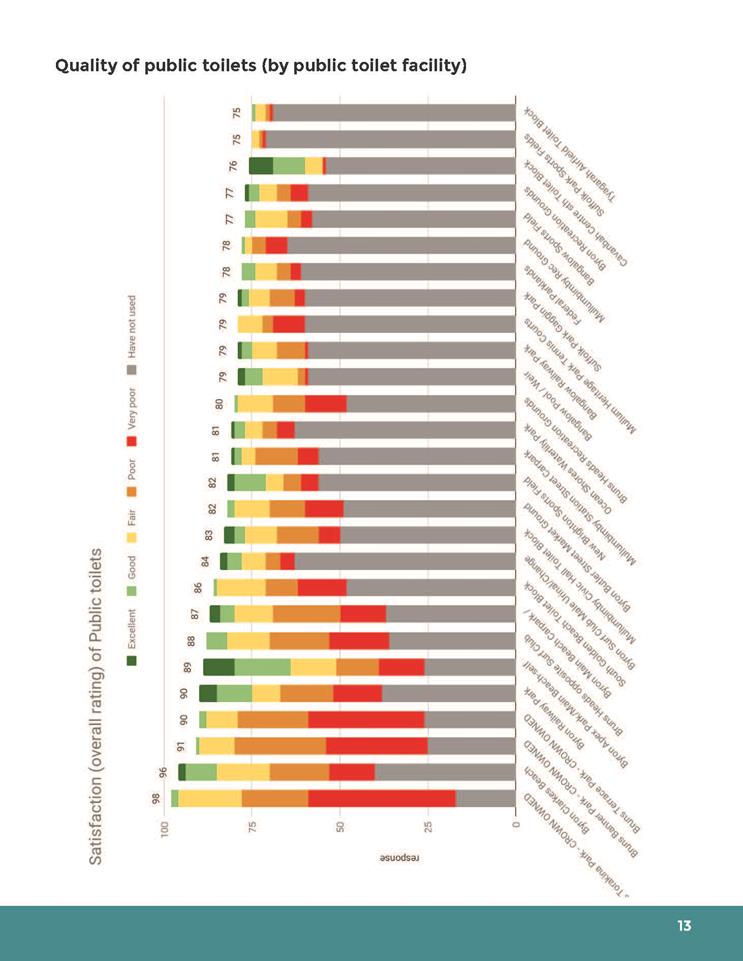

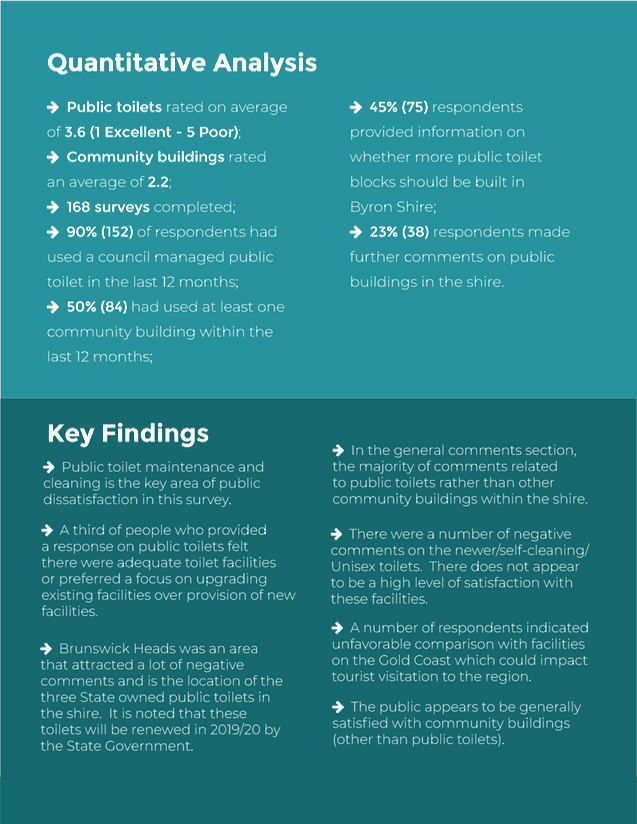

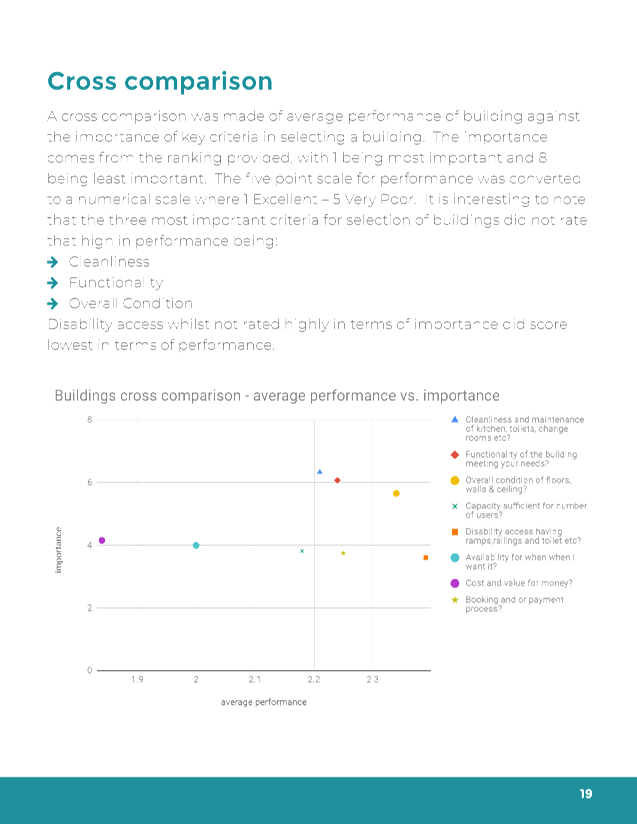

(Table 5). The Overall rating of toilets was 3.6 and community buildings

at 2.2 (1 Excellent to 5 Very Poor), indicating that generally the

community is satisfied with the community buildings. With respect to importance

the top three categories were:

è Cleanliness (Quality)

è Functionality

è Overall Condition (Quality)

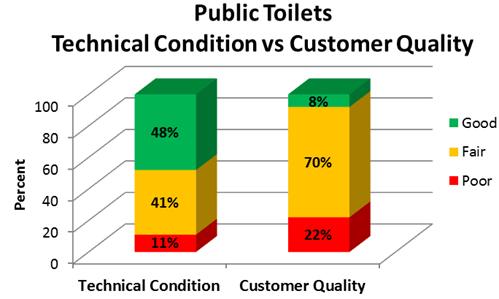

The

public toilet average ratings were compared. The average customer quality was

rated at 3.6 and technical condition at 3.0, refer to Figure 6Error! Reference source not found.. This indicates that the community expects a higher level

of service than Council provides. This is also relevant in terms of the survey

feedback in which respondents listed many requirements including: no graffiti,

baby change tables, paper towels, hand dryers, soap, single sex toilets as

opposed to multi-use cubicles, and no stainless steel toilets without seats

that are unpleasant in winter. The responses indicate the community prioritises

renewed modern and clean toilets above more toilets.

Figure 6 Customer & Technical Rating Comparison

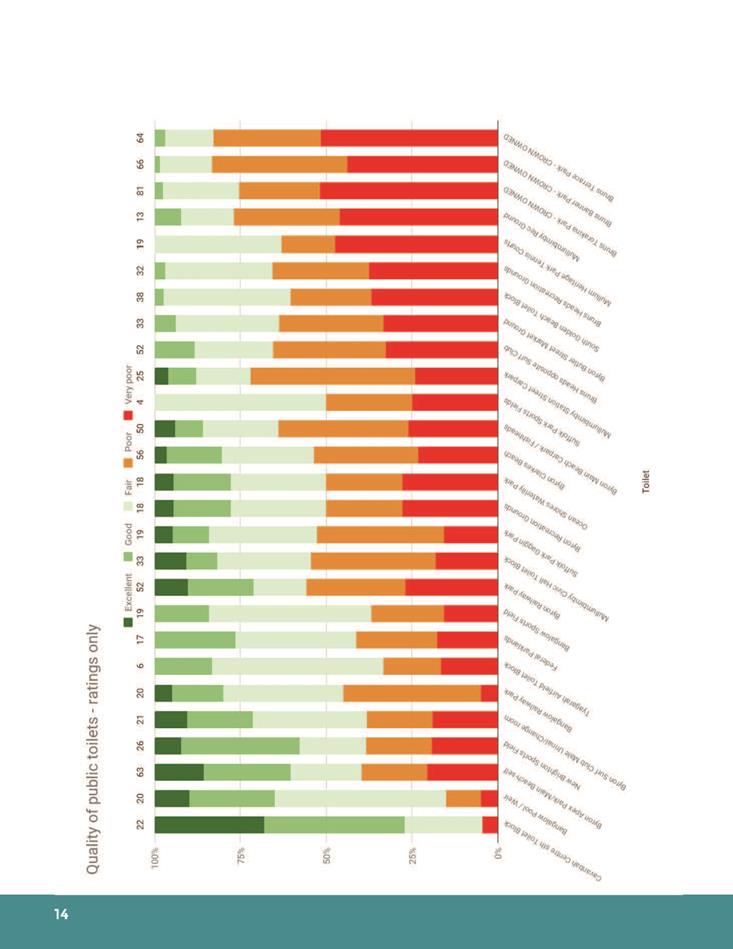

The

overall public toilet category has been ranked by condition and customer

quality into Good, Fair and Poor (Figure 7). Whilst results are similar, Figure

7 shows a mismatch between the Technical Levels of Service rating and the

customer quality rating.

Figure 7 Public Toilet Technical Condition vs Customer Quality

Figure 8 Customer Levels of Service Quality Ratings

The community rated the quality of public toilets 3.6 and community buildings 2.2

The technical condition rating of public toilets 3.0 and community buildings 3.3

(1 Excellent and 5 Very Poor)

Community Levels of Service Survey Key

Findings

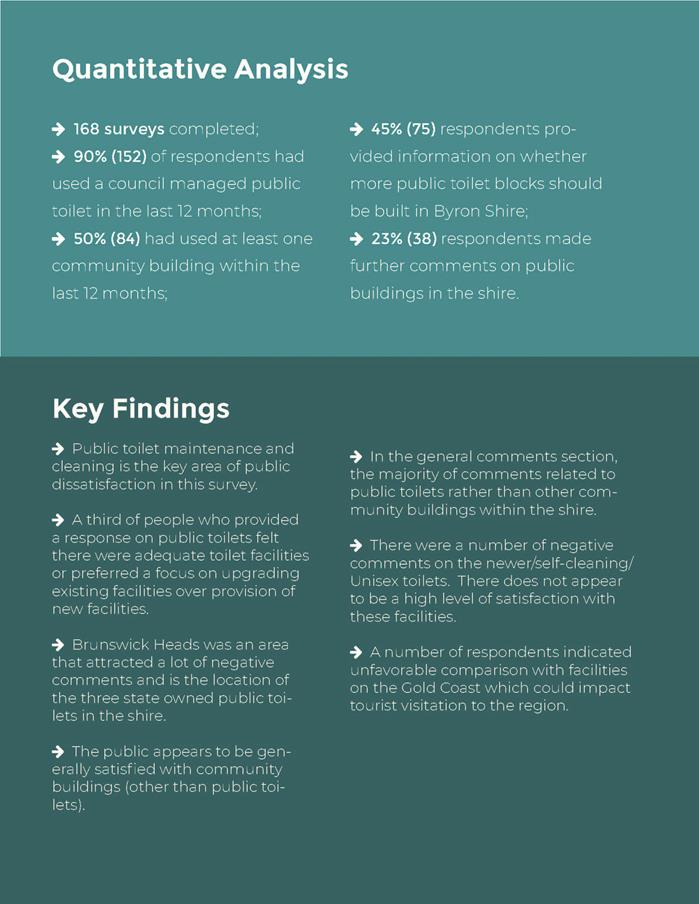

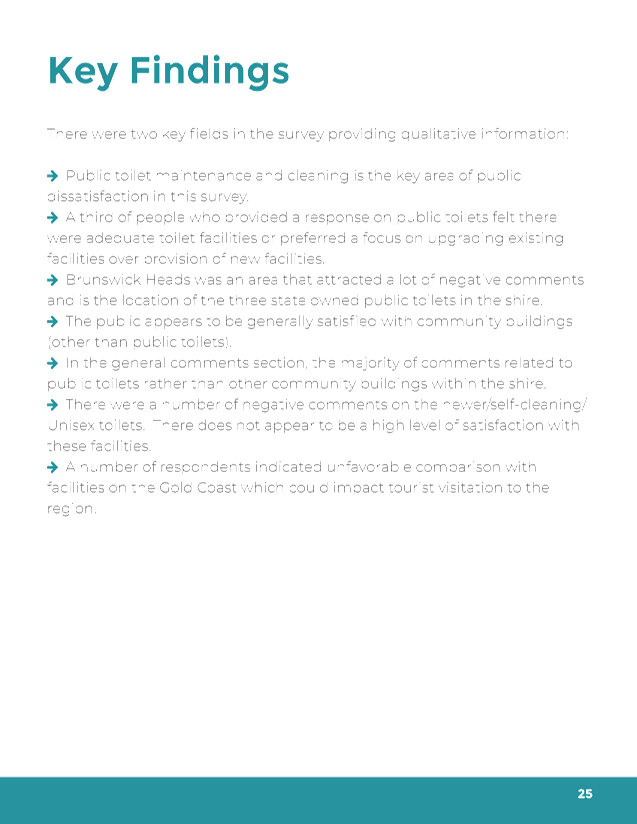

è Public toilet maintenance and cleaning is the key area of

public dissatisfaction.

è A third of people who provided a response on public toilets

felt there were adequate toilet facilities or preferred a focus on renewing or

upgrading existing facilities over provision of new facilities. Public safety

should be given priority e.g. locks on doors and lighting.

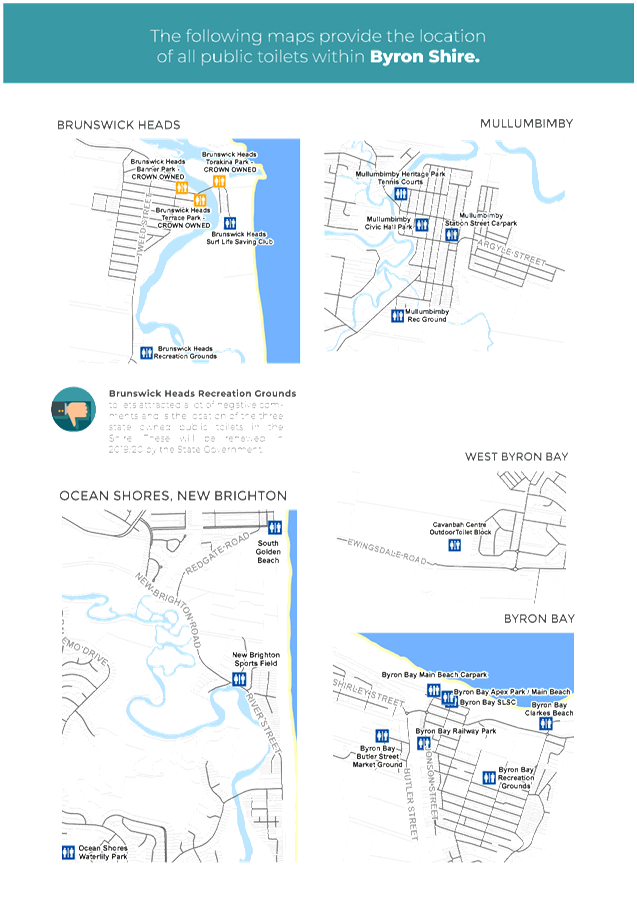

è Brunswick Heads attracted a lot of negative comments and is

the location of the 3 state owned public toilets in the Shire.

è The public appears to be generally satisfied with community

buildings with a quality rating of 2.2 (other than public toilets). Upgrades

were sought to improve disability access.

è In the general comments section the majority of comments

related to public toilets.

è There were a number of negative comments on the new

self-cleaning unisex toilets. There does not appear to be a high level of

satisfaction with these facilities.

è A number of respondents made unfavourable comparison with

facilities on the Gold Coast.

Refer

to Appendix E for the full Community

Engagement Report & Infographics

document.

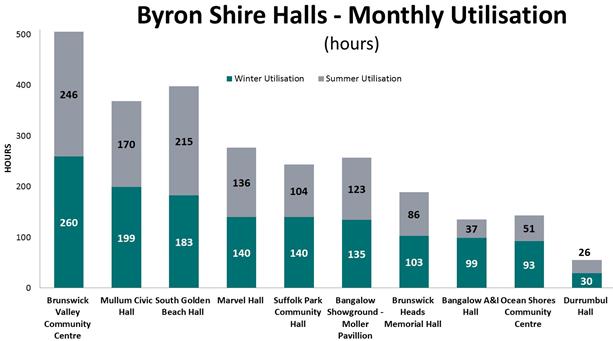

Community Hall Utilisation

Use of the community halls and centres has been analysed

over both summer and winter months using sample data from the online calendar

booking system. Figure 9 below clearly indicates that the Brunswick Valley

Community centre is being fully utilised with an average of 253 hours per month

with the Durrumbul Hall at the lowest with just 56 hours per month. When it

comes to measuring Customer Levels of Service, use of facilities is one of the

key criteria. This is a point in time snapshot and can be remeasured to assist

with Future Demand planning.

Figure 9 Community Hall Monthly Utilisation

(E2019/28051)

Together

the Community and Technical Levels of Service

provide detail on service performance, cost and whether service levels are

likely to stay the same, improve or deteriorate. Council’s current and

projected levels of service are documented below. These Key Performance

Indicators (KPI’s) for Levels of Service have been developed using the

following tools:

è Council’s Customer Request Management System

è Surveys – community satisfaction survey

è Focus Groups – Infrastructure and Transport Advisory

Committee

è Facebook feedback

è Inspections and condition assessments

The community expectation for Public Toilet service

levels is higher than

current budgets can accommodate in the medium term.

Levels of Service Summary

Council’s

present funding levels are insufficient to continue to provide existing

services at current levels in the medium term. This conclusion is made from

predictive modelling in the current Long Term Financial Plan (Refer Financial

Summary, Section 12). Funding levels therefore need to be reconsidered.

Table 5 Buildings Levels of Service – Community & Technical

|

COMMUNITY LEVELS OF SERVICE – PUBLIC TOILETS

|

|

Key

Performance Measure

|

Level

of Service

|

Performance

Measure Process

|

Performance

Target

|

Current

Performance

|

|

Performance rating

overall condition 1 to 5 (1 excellent – 5 very poor)

|

|

Quality

|

Satisfactory and suitable

public toilets

|

Customer Requests for public

toilets

|

<80 customer requests per

year public toilets (cleaning, plumbing, graffiti etc. per year)

|

118 Customer Requests per

year (2017/18)

|

|

Quality

|

Performance rating overall

condition 1 to 5

(1 excellent to 5 very poor)

|

Customer Levels of

Service Survey[6]

|

Not achieved Condition 3 -

Fair

|

3.6[7]

|

|

Capacity

|

Provide public toilets at

regular intervals across the CBD and Open Spaces

|

Customer requests / consultation

feedback1

|

Where renewal is required

consider location closer to playgrounds & recreational facilities as per

community survey.

|

Sufficient supply public

toilets across the shire.

|

|

|

|

COMMUNITY LEVELS OF SERVICE – COMMUNITY BUILDINGS

|

|

Key

Performance Measure

|

Level

of Service

|

Performance

Measure Process

|

Performance

Target

|

Current

Performance

|

|

Quality

|

Overall condition - what

was the condition of floor coverings, lights, walls & ceilings?

|

Customer Levels of

Service Survey

|

Achieved Condition 3 - Fair

|

2.34 4

|

|

Quality

|

Overall cleanliness - was the

kitchen, toilets, change rooms clean?

|

Customer Levels of

Service Survey)

|

Achieved

Condition 3 – Fair

|

2.214

|

|

Quality

|

Cost - was the building value

for money, in your opinion?

|

Customer Levels of

Service Survey

|

Achieved Condition 3 –

Fair

|

1.844

|

|

Function

|

Functionality - did the

spaces (rooms & kitchens) serve your purpose?

|

Customer Levels of

Service Survey

|

Achieved Condition 3 –

Fair

|

2.244

|

|

Function/ Accessibility

|

Disability access - did it

have appropriate ramps, rails and toilets

|

Customer Levels of

Service Survey

|

Achieved Condition 3 –

Fair

|

2.394

|

|

Capacity

|

Capacity - did the building

cater to the number of users?

|

Customer Levels of

Service Survey

|

Achieved Condition 3 – Fair

|

2.184

|

|

Available

|

Availability - were there

lots of date options for you to choose from?

|

Customer Levels of

Service Survey

|

Achieved Condition 3 - Fair

|

2.04

|

|

Ave. Rating

|

|

|

|

2.2

|

|

TECHNICAL LEVELS OF SERVICE – PUBLIC TOILETS

& GENERAL FUND BUILDINGS

|

|

Performance

Measure

|

Level of Service

|

Performance Measure Process

|

Performance Target

(Agreed Sustainable Position [8])

|

Current Performance [9] 2018

|

|

Operations

|

Buildings meet user’s

needs

|

Condition & safety

inspections

|

As per Maintenance Plan

(E2019/20878) and Table 10 Maintenance & Inspection Program

|

To be reviewed. Added to

Improvement Plan.

|

|

Buildings are clean

*Other buildings (emergency

services, residential, showgrounds, Commercial leases, airfield, community

leases, council operations, swimming pool)

|

Cleaning

responsibility/frequency

|

Buildings cleaning

responsibility as per Maintenance Plan, Section 8. Public Toilets refer Table

2 Public Toilet – Customer Levels of Service

|

Buildings cleaning

responsibility as per Maintenance Plan, Section 8. Public Toilets refer Table

2 Public Toilet – Customer Levels of Service

|

|

Budget Council Administration

Building

|

Total

$ “To be determined”

|

$291,383

|

|

Budget Cavanbah Centre

|

Total

$ “To be determined”

|

$

7,819

|

|

Budget Libraries

|

Total

$ “To be determined”

|

$137,352

|

|

Budget Public Toilets

|

Total

$ “To be determined”

|

$460,140

|

|

Budget Community Halls /

Centres

|

Total

$ “To be determined”

|

$ 44,407

|

|

Budget Recreational

Facilities

|

Total

$ “To be determined”

|

$ 70,223

|

|

Budget *Other Buildings

|

Total

$ “To be determined”

|

$ 98,871

|

|

|

Total

$ “To be determined”

|

(R2019/36175)

TOTAL

$1,110,196

|

|

Maintenance

|

Buildings are suitable for

purpose

*Other buildings (emergency

services, residential, showgrounds, Commercial leases, airfield, community

leases, council operations, swimming pool)

|

Reactive service requests

completed to schedule

|

TBD % defects made safe

within 5 working days

(Defect = Statutory,

Environmental & Safety)

TBD % of repairs within 30

working days

|

TBD e.g.

below: < 80% of defects made safe within 5 working days<60% of repairs

in 30 working days

|

|

Planned maintenance

activities accomplished from Maintenance Plan (Defects)

|

85% of planned maintenance

activities completed to schedule in accordance with component hierarchy

priority on Statutory, Environmental & Safety

|

To be determined e.g.

below:

<90% completed

|

|

Number of recorded defects in

condition 4, or 5 (poor to very poor)

|

1600 defects identified in

2019

(estimated at $1.46million)

|

$214,197 actual in 2018 to address

defects

|

|

Maintenance Administration

Building

|

$

51,796

|

$111,298

|

|

Maintenance Budget Cavanbah

Centre

|

$229,881

|

$ 15,589

|

|

Maintenance Budget Libraries

|

$

31,468

|

$ 44,410

|

|

Maintenance Budget Public

Toilets

|

$111,204

|

$ 57,129

|

|

Maintenance Budget Community

Halls

|

$429,050

|

$ 34,920

|

|

Maintenance Budget Recreation

|

$210,971

|

$ 35,432

|

|

Maintenance *Other buildings

|

$835,903

|

$110,757

|

|

|

TOTAL

$1,900,006

|

(R2019/36175)

TOTAL

$409,534

|

|

Buildings meet relevant

legislative requirements

|

Planned maintenance and

inspection program complete

|

As per planned and unplanned

maintenance response times (Maintenance Plan, Section 8) and individual

cleaning schedules

|

Safety/Environmental/Security

(57) e.g. Disability access non compliance, trip hazards, window locks,

missing fire extinguisher, exit not illuminated, asbestos. Statutory (1) e.g.

loose wires Byron Surf Club

|

|

Buildings meet user’s

needs

|

Condition of buildings

|

20 % of buildings in

condition 4 and 5

|

29 % of buildings in

condition 4 and 5

|

|

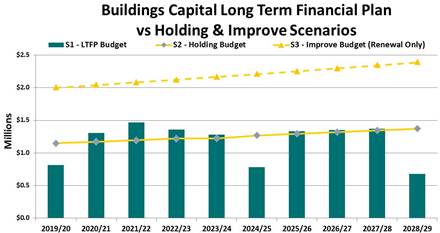

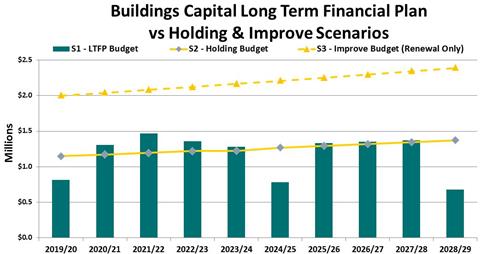

Renewal

|

Buildings meet user’s

needs. No new buildings planned in the next 10 years

|

Budget allocation of

$1,257,217 spent on renewals only

|

$1,257,217

(Average Annual “Hold/Maintain”

Scenario 2)

|

$1,074,650

(Average Annual

“Hold/Maintain” Scenario 1)

|

|

Upgrade/New

|

Brunswick Memorial Hall

– Commercial kitchen upgrade

|

Budget 19/20 $60,000 from

Capital Renewals & $60,000 from Committee

|

$0

|

$60,000

|

.

5. Future Demand

This

section evaluates potential factors affecting demand such as:

è Population growth

è Changing community expectations

è Development

è Changes in demographics

è Strategic network extensions, upgrades and additions

These

factors will affect the renewal and upgrade of the existing network which in

turn impacts maintenance and operational resourcing and budgeting.

Demand Forecast

Population

trends can be used as a guide in determining future demand. Information from

NSW Planning & Environment below indicates that Byron Shire is currently

experiencing growth, which is expected to continue (Table 6).

Table 6 NSW population

projections regional LG data

|

Forecast

Year

|

Change

between 2011 and 2036

|

|

2011

|

2016

|

2021

|

2026

|

2031

|

2036

|

Total

Change

|

Total

Increase Rate

|

|

30,700

|

32,400

|

33,850

|

35,250

|

36,650

|

37,950

|

7,250

|

1.24

|

This

population growth may see an increase in maintenance requirements across the

Building Asset network along with capital renewals and upgrades.

There

is also potential for increased developer contributed assets that will

alleviate some of the strains placed by an increase in population and the

corresponding expectations and requirements. However, this will also bring with

it a need for increased maintenance expenditure and resourcing as the assets

begin to age.

Demand Management Plan

The

demand for building assets is expected to increase proportional to population

growth. This also aligns with the expectations from the community where public

toilets scored in the top 3 priorities (Figure 10).

Figure 10 Top 3 Community

Priorities (BSC Survey, 2016)

Managing

the demand for services will involve both asset and non-asset solutions.

Non-asset

solutions put emphasis on providing a level of service without making changes

to the current asset stock. This includes reducing the level of service,

reducing demand for the service and educating the community to accept

appropriate asset condition.

Asset

solutions include the renewal, upgrade and creation of assets.

Key

drivers for demand that have been identified are shown below (Table 7).

Table 7 Demand management plan

summary

|

Demand

Driver

|

Impact

on Services

|

Demand

Management Plan

|

|

Capacity

· Population growth

· Tourism

|

Requirement

to upgrade or expand public toilets, community halls and sporting facilities

|

· Fund priority works by seeking grant funding and

implementing the Developer Contributions Plan

· Educate the community on the costs associated with

holding/maintaining current service levels and that increased assets mean

increased costs

|

|

Capital

/ Maintenance Works

· Asset growth

· Aging asset stock

· Expectation from community for quality building portfolio

· Increased costs associated with capital renewal in the

region. Trade /contractor demands.

|

Requirement

to upgrade facilities

|

· Consult with community on options and funding

requirements

· Inform community and manage expectations. Communicate

levels of service and financial capacity, to balance infrastructure

priorities with what the community is prepared to fund.

|

|

Development

· Increased development to accommodate increased population

and demand

|

Additional

infrastructure required to cope with demand

|

· Monitor and manage development controls

· Undertake infrastructure planning taking into account

land use changes

|

New Assets from Growth

The

purpose of the Development Contributions Plan 2012 (Amendment 3) (the

Plan) is to enable Byron Shire Council to request contributions from

developers. These contributions are expected to provide services that are

likely to be required as a result of development throughout Byron Shire. The

Plan also outlines the programmed work to be completed as part of the

expenditure of contributions, and is available on Council’s website (http://www.byron.nsw.gov.au/developer-contributions-plans).

The

Plan requires the carrying out of works or the payment of contributions to go

towards the provision, extension or augmentation of services and facilities

that will, or are likely to be, required as a consequence of development in

Byron Shire.

6.

Asset Management Practices

This

section outlines the decision-making tools currently used to determine long

term maintenance, renewal and upgrade expenditure for building assets. As a

result of Council restructuring, an asset team was formed in 2015. This now

consists of 4 full time staff dedicated to strategically managing assets. This

has provided the opportunity to increase capacity and scale to improve asset

management systems and technologies and is detailed in Figure 11 Asset

Management Systems and Elements.

Financial Systems

Council

currently uses Authority as the financial management and accounting system.

Inspection Processes

Council

completed a comprehensive audit of all buildings in 2019. This identified 1,600

defects that need to be addressed to bring assets to a satisfactory condition

in accordance with the standards. This audit used a mobile solution called Reflect™.

All roof tops were visually inspected using Council’s drone which

enabled inspection that would not otherwise have been affordable and

highlighted the need for improvements to general gutter maintenance. All

defects were detailed and photographed. The inspections also included detailed

condition assessments to the component level and the data used in the

Predictor© modelling software for the capital works programming.

Asset Management Systems

Council

uses Authority as the asset management system. Authority Asset Register

contains details of all Council assets, their attribute and condition

information. At present 37,000 (July 19) assets are linked to Council’s

corporate GIS system, which is used to show asset locations spatially in

conjunction with cadastral, topographic and aerial information.

Assetic

Predictor© was used to perform the strategic modelling prediction analysis

to determine the future strategies and capital expenditure plans detailed in

the Financial Summary section (Figure 11).

Asset management systems are well

established and integrated,

however, work is required in the Work