Audit, Risk and Improvement Committee Meeting

An Audit, Risk and Improvement Committee

Meeting of Byron Shire Council will be held as follows:

|

Venue

|

Meeting Room 1, Station Street, Mullumbimby

|

|

Date

|

Thursday, 14 November 2019

|

|

Time

|

11:30am

|

Vanessa Adams

Director Corporate and

Community Services I2019/1879

Distributed 07/11/19

What is a “Conflict of Interests” - A conflict of

interests can be of two types:

Pecuniary - an interest that a person has in a matter because of a reasonable

likelihood or expectation of appreciable financial gain or loss to the person

or another person with whom the person is associated.

Non-pecuniary – a private or personal interest that a Council

official has that does not amount to a pecuniary interest as defined in the Code

of Conduct for Councillors (eg. A friendship, membership of an association,

society or trade union or involvement or interest in an activity and may

include an interest of a financial nature).

Remoteness – a person does not have a pecuniary interest in a matter

if the interest is so remote or insignificant that it could not reasonably be

regarded as likely to influence any decision the person might make in relation

to a matter or if the interest is of a kind specified in the Code of Conduct

for Councillors.

Who has a Pecuniary Interest? - a person has a pecuniary interest in a

matter if the pecuniary interest is the interest of the person, or another

person with whom the person is associated (see below).

Relatives, Partners - a person is taken to have a pecuniary interest in a

matter if:

§ The person’s

spouse or de facto partner or a relative of the person has a pecuniary interest

in the matter, or

§ The person, or a

nominee, partners or employer of the person, is a member of a company or other

body that has a pecuniary interest in the matter.

N.B. “Relative”, in relation to a person means any of the

following:

(a) the

parent, grandparent, brother, sister, uncle, aunt, nephew, niece, lineal

descends or adopted child of the person or of the person’s spouse;

(b) the

spouse or de facto partners of the person or of a person referred to in

paragraph (a)

No Interest in the Matter - however, a person is not taken to have a

pecuniary interest in a matter:

§ If the person is

unaware of the relevant pecuniary interest of the spouse, de facto partner,

relative or company or other body, or

§ Just because the

person is a member of, or is employed by, the Council.

§ Just because the

person is a member of, or a delegate of the Council to, a company or other body

that has a pecuniary interest in the matter provided that the person has no

beneficial interest in any shares of the company or body.

Disclosure and participation in meetings

§ A Councillor or a

member of a Council Committee who has a pecuniary interest in any matter with

which the Council is concerned and who is present at a meeting of the Council

or Committee at which the matter is being considered must disclose the nature

of the interest to the meeting as soon as practicable.

§ The Councillor or

member must not be present at, or in sight of, the meeting of the Council or

Committee:

(a) at any

time during which the matter is being considered or discussed by the Council or

Committee, or

(b) at any

time during which the Council or Committee is voting on any question in

relation to the matter.

No Knowledge - a person does not breach this Clause if the person did

not know and could not reasonably be expected to have known that the matter

under consideration at the meeting was a matter in which he or she had a

pecuniary interest.

Non-pecuniary Interests - Must be disclosed in meetings.

There are a broad range of options available for managing conflicts &

the option chosen will depend on an assessment of the circumstances of the

matter, the nature of the interest and the significance of the issue being

dealt with. Non-pecuniary conflicts of interests must be dealt with in at

least one of the following ways:

§ It may be appropriate

that no action be taken where the potential for conflict is minimal.

However, Councillors should consider providing an explanation of why they

consider a conflict does not exist.

§ Limit involvement if

practical (eg. Participate in discussion but not in decision making or vice-versa).

Care needs to be taken when exercising this option.

§ Remove the source of

the conflict (eg. Relinquishing or divesting the personal interest that creates

the conflict)

§ Have no involvement by

absenting yourself from and not taking part in any debate or voting on the

issue as of the provisions in the Code of Conduct (particularly if you have a significant

non-pecuniary interest)

RECORDING OF VOTING ON PLANNING MATTERS

Clause 375A of the Local Government Act 1993

– Recording of voting on planning matters

(1) In this section, planning

decision means a decision made in the exercise of a function of a council

under the Environmental Planning and Assessment Act 1979:

(a) including a decision

relating to a development application, an environmental planning instrument, a

development control plan or a development contribution plan under that Act, but

(b) not including the making of

an order under that Act.

(2) The general manager is

required to keep a register containing, for each planning decision made at a meeting

of the council or a council committee, the names of the councillors who

supported the decision and the names of any councillors who opposed (or are

taken to have opposed) the decision.

(3) For the purpose of

maintaining the register, a division is required to be called whenever a motion

for a planning decision is put at a meeting of the council or a council

committee.

(4) Each decision recorded in

the register is to be described in the register or identified in a manner that

enables the description to be obtained from another publicly available

document, and is to include the information required by the regulations.

(5) This section extends to a

meeting that is closed to the public.

Audit, Risk and Improvement Committee Meeting

BUSINESS OF MEETING

1. Apologies

2. Declarations of Interest

– Pecuniary and Non-Pecuniary

3. Adoption of Minutes from

Previous Meetings

3.1 Audit,

Risk and Improvement Committee Meeting held on 10 October 2019

4. Staff Reports

Corporate and Community Services

4.1 A

New Risk Management and Internal Audit Framework - Discussion Paper................. 4

4.2 2018/2019

Financial Statements................................................................................... 126

5. Confidential Reports

Corporate and Community Services

5.1 Confidential - Update on IT Actions...................................................................... 242

5.2 Confidential - Audit Progress Report -

November 2019....................................... 243

5.3 Confidential - Business Continuity and

Risk Management - Update.................... 244

5.4 Confidential - Pay Parking Audit Review.............................................................. 245

5.5 Confidential - Grants Management Audit

Review................................................ 246

Staff Reports - Corporate and Community Services 4.1

Staff Reports - Corporate and Community

Services

Report No. 4.1 A

New Risk Management and Internal Audit Framework - Discussion Paper

Directorate: Corporate

and Community Services

Report

Author: Heather

Sills, Corporate Governance Officer

Emma Fountain, Strategic Risk

& Business Continuity Coordinator

File No: I2019/1636

Summary:

The Local Government Act 1993 was amended in August

2016 to require each council and joint organisation in NSW to appoint an audit,

risk and improvement committee (ARIC).

The Office of Local Government (OLG) has developed a draft

internal audit and risk management framework to support and inform the

operations of ARICs. The proposed framework is based on international standards

and the experience of Australian and NSW Government public sector agencies who

have already implemented risk management and internal audit and has been

adapted to reflect the unique needs and structure of NSW councils and joint

organisations.

OLG has issued a discussion paper, “A New Risk Management and Internal Audit

Framework for Local Councils in NSW” which sets out the

proposed framework in detail and a “snapshot” guide that summarises

its key elements. The OLG are seeking submissions on the framework by 31

December 2019.

|

RECOMMENDATION:

That the Audit Risk and Improvement Committee:

1. Considers

the discussion paper, “A New Risk Management and Internal Audit

Framework for Local Councils in NSW”

2. Makes

a submission to the Office of Local Government during the submission period

covering the considerations outlined in this report

|

Attachments:

1 A new risk

management and internal audit framework for local councils in NSW - discussion

paper, E2019/76198 , page 10⇩

2 A new risk

management and internal audit framework for local councils in NSW - snapshot

guide, E2019/76197 , page 116⇩

REPORT

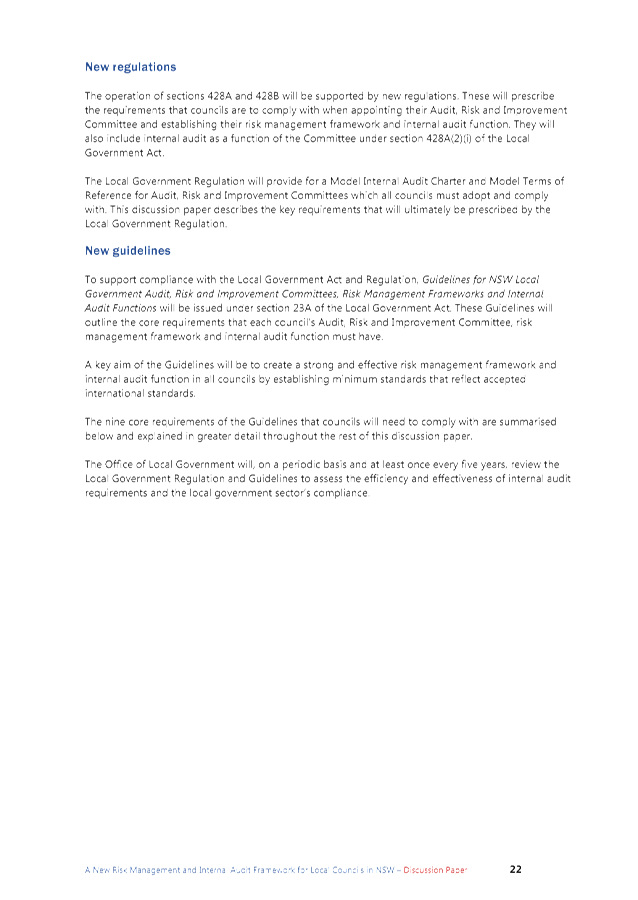

The Local Government Regulation

will provide for a Model Internal Audit Charter and Model Terms of Reference

for Audit, Risk and Improvement Committees which all councils must adopt and

comply with. The discussion paper describes the key requirements that will

ultimately be prescribed by the Local Government (General) Regulation

2005.

The NSW Government’s

objective is to ensure that councils have:

· an independent ARIC that adds value to the council

· a robust risk management framework

· an effective internal audit function

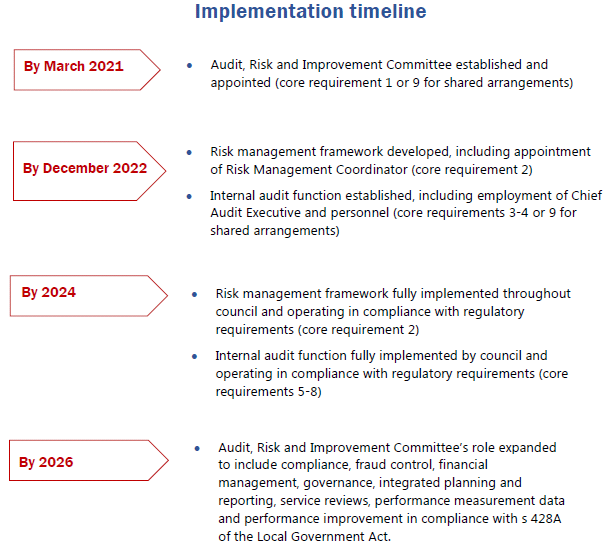

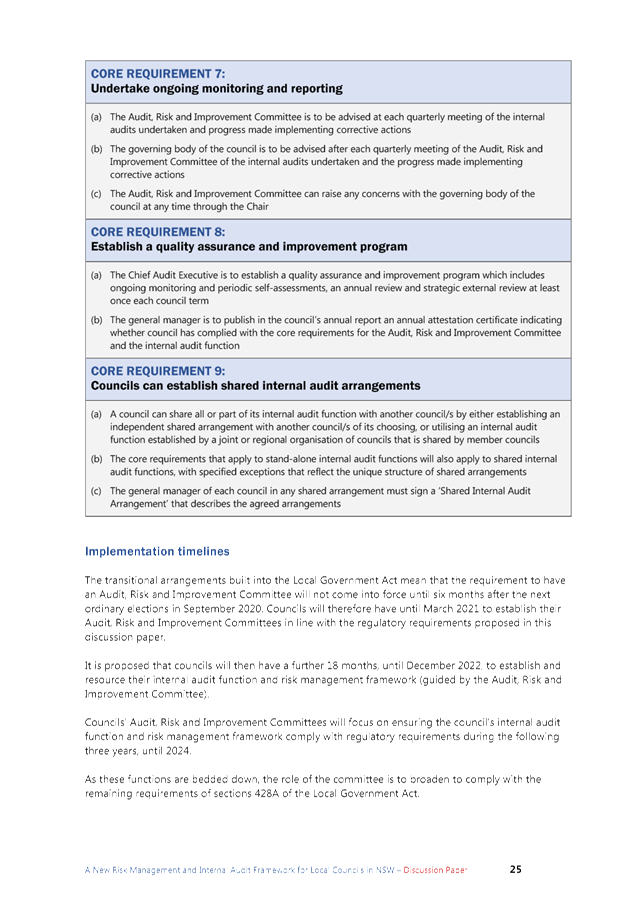

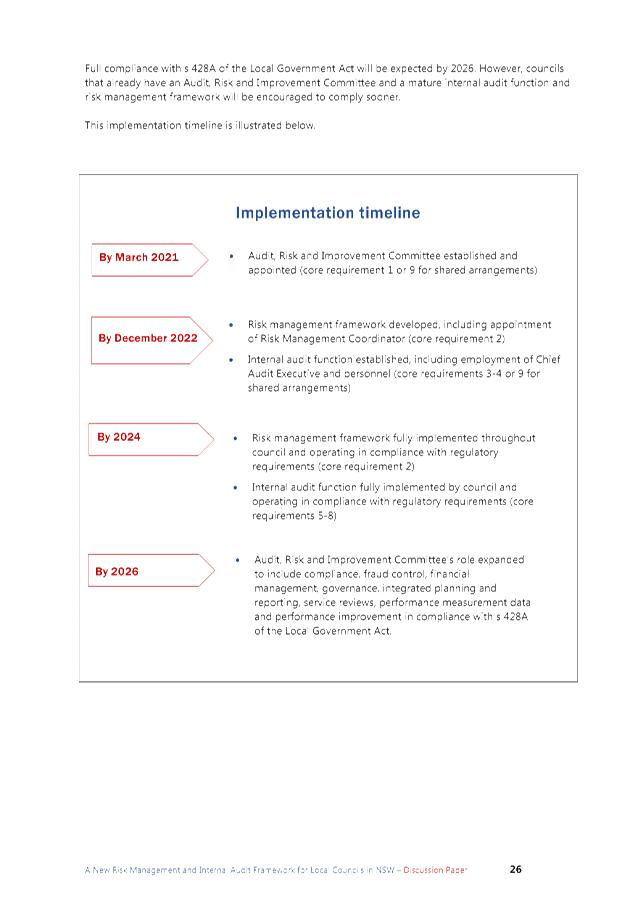

Councils will have until March

2021 to establish their Audit, Risk and Improvement Committees in line with the

regulatory requirements proposed in the discussion paper. It is proposed that

councils will then have a further 18 months, until December 2022, to establish

and resource their internal audit function and risk management framework

(guided by the Audit, Risk and Improvement Committee).

It is expected that over time, as

resources allow, the role of each Council’s Audit, Risk & Improvement

Committee will be expanded to include compliance, fraud control, financial

management, governance, integrated planning and reporting, service reviews and

performance management, with full compliance achieved by 2026.

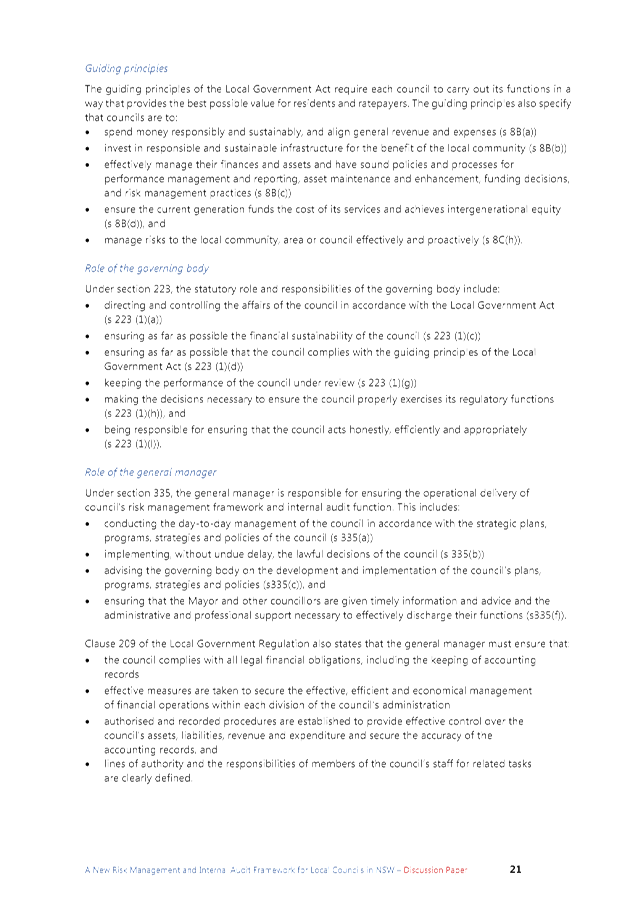

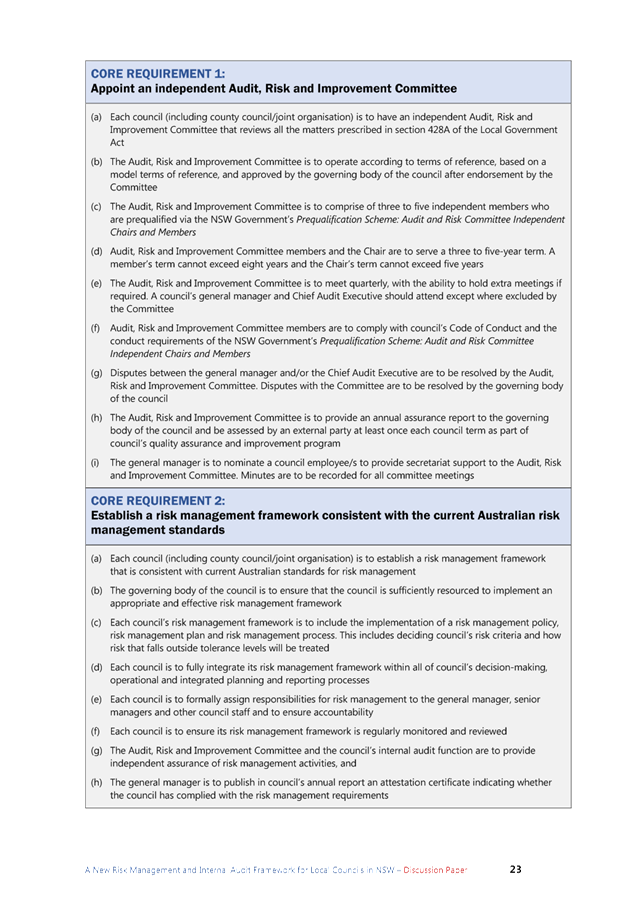

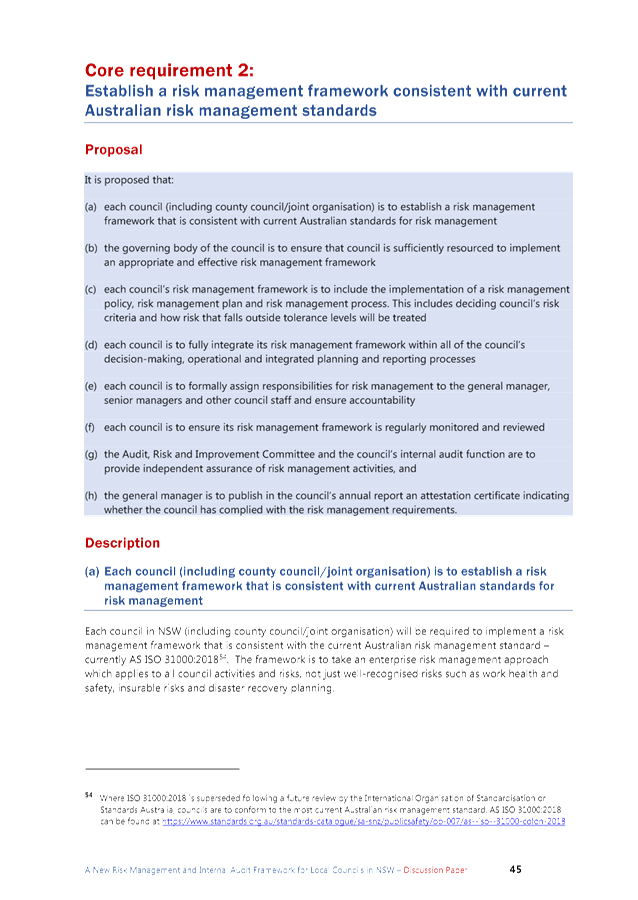

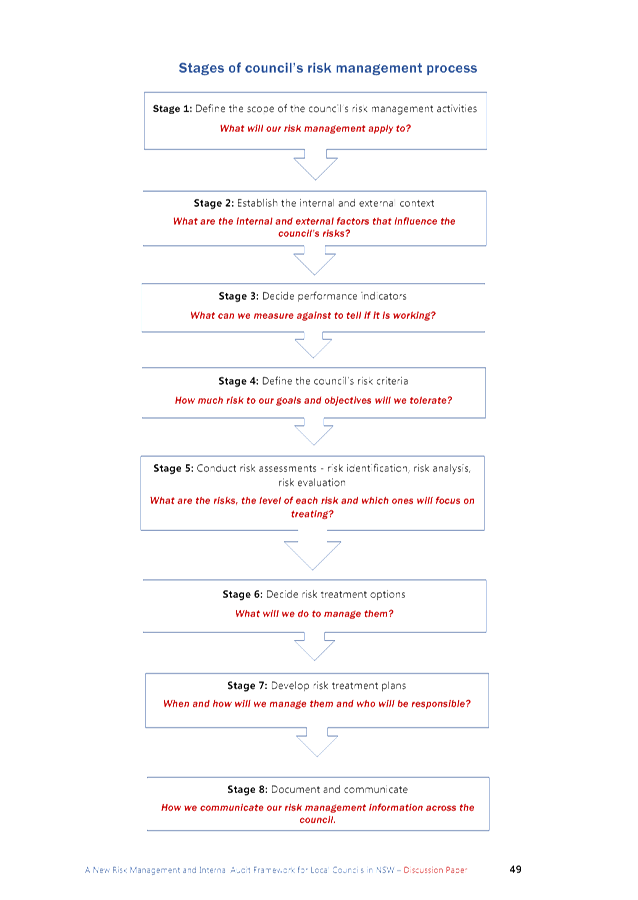

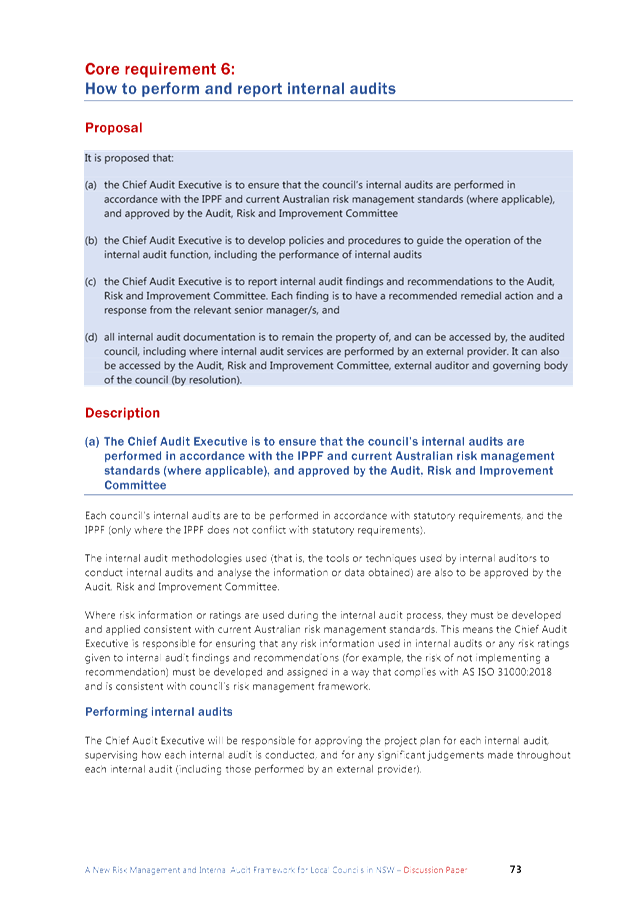

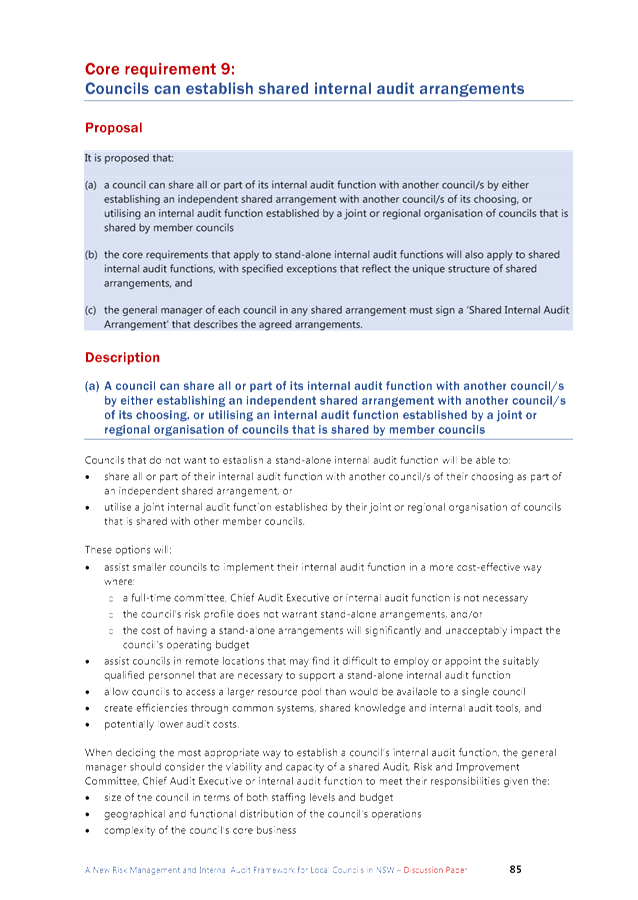

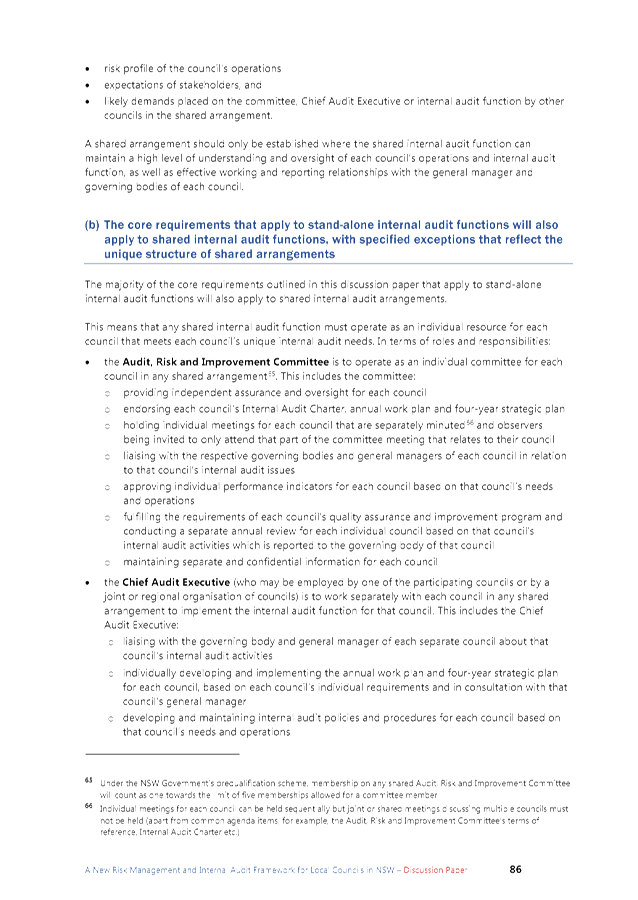

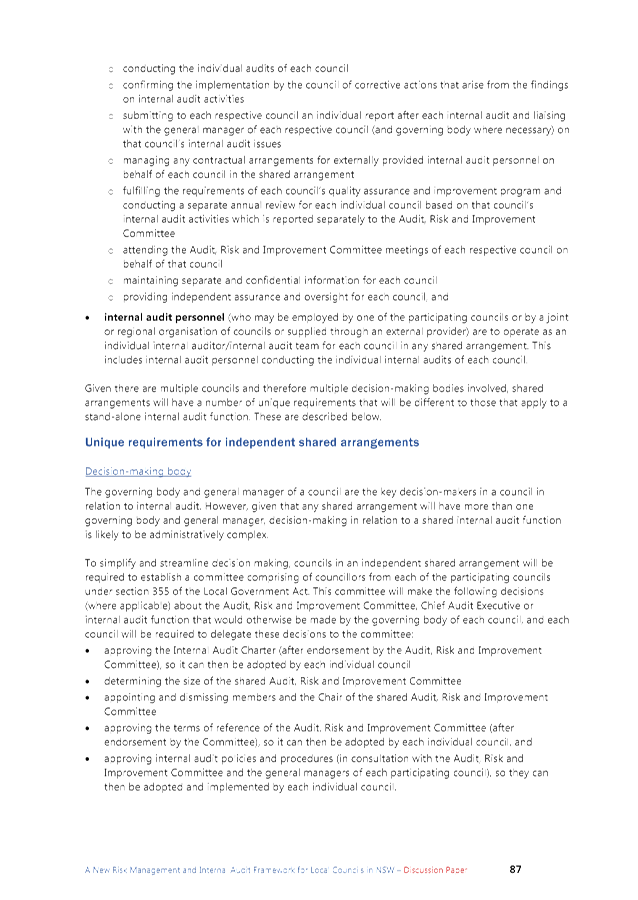

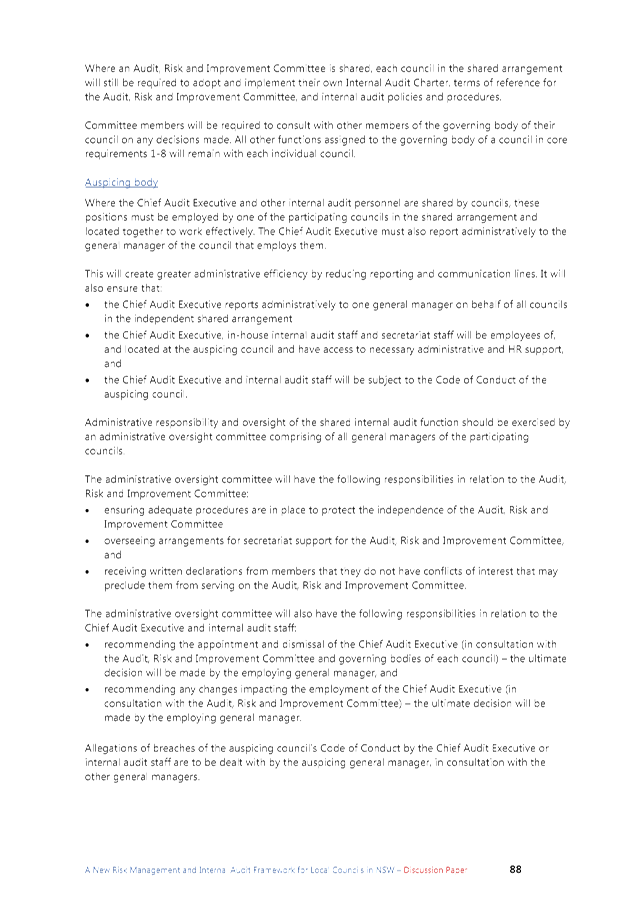

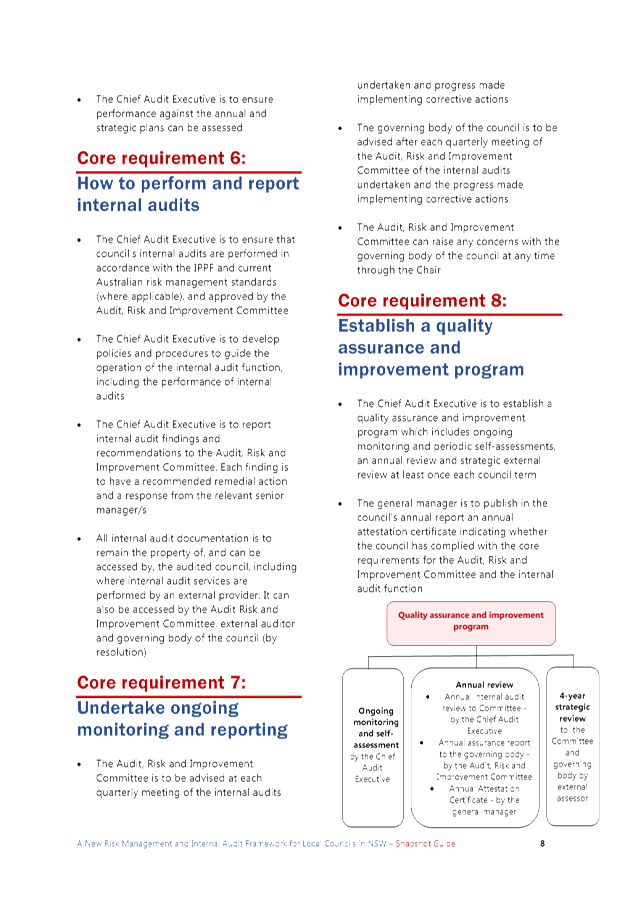

Core Requirements

The discussion paper outlines nine core requirements that

councils will be required to comply with when establishing their Audit, Risk

and Improvement Committee, risk management framework and internal audit

function.

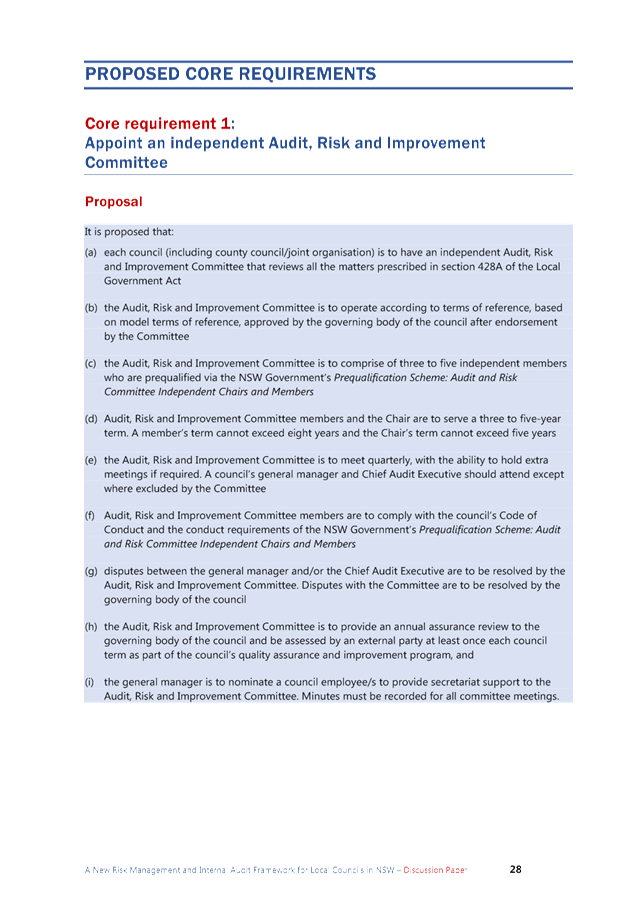

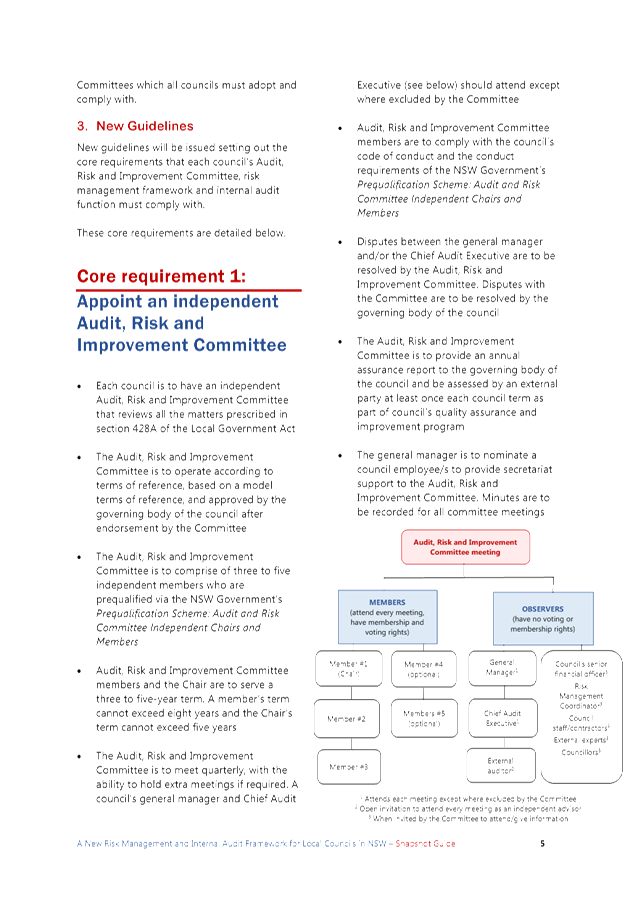

Core requirement 1: Appoint an

independent Audit, Risk and Improvement Committee (must be independent members

from prequalified panel (i.e. no Councillors))

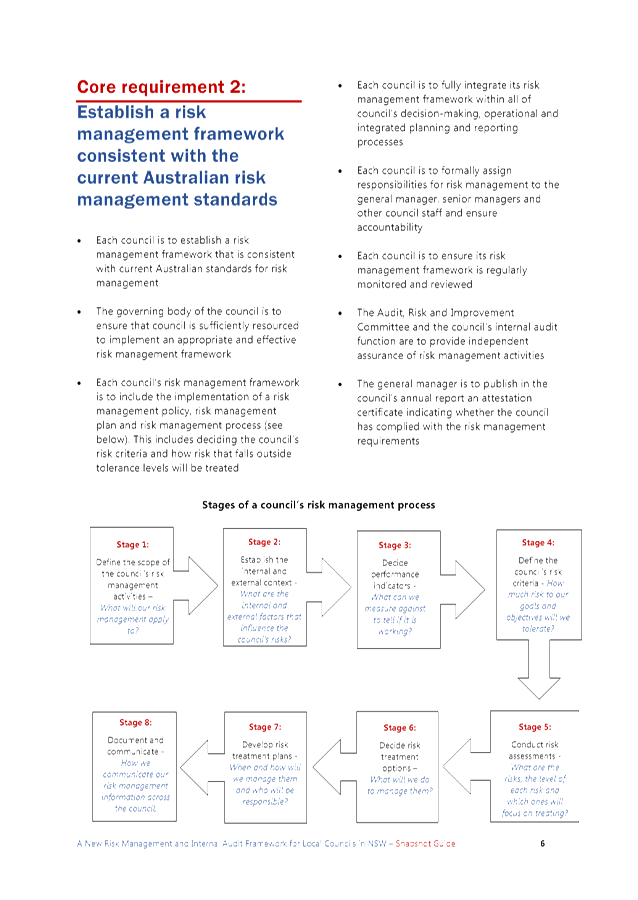

Core requirement 2: Establish a risk

management framework consistent with current Australian risk management

standards

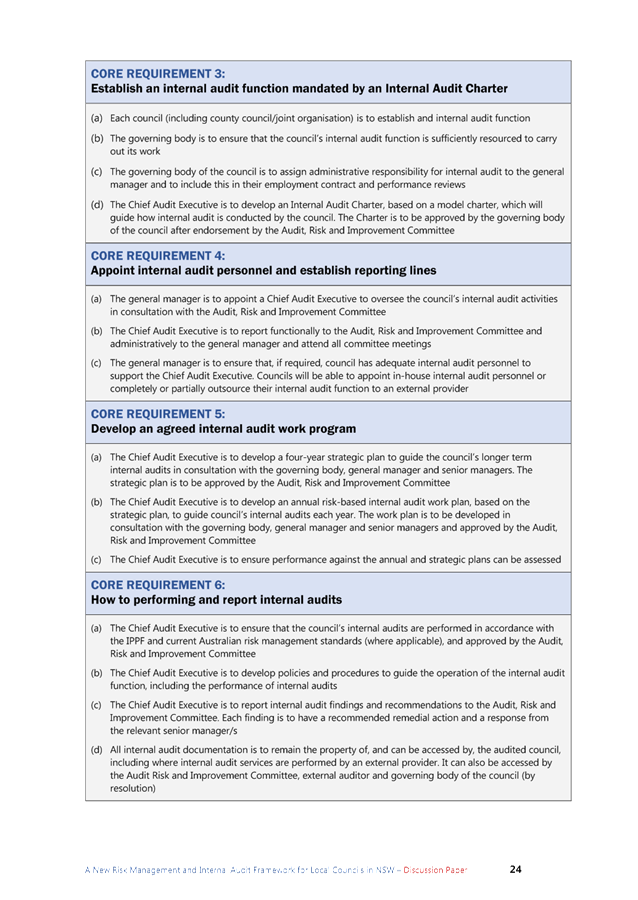

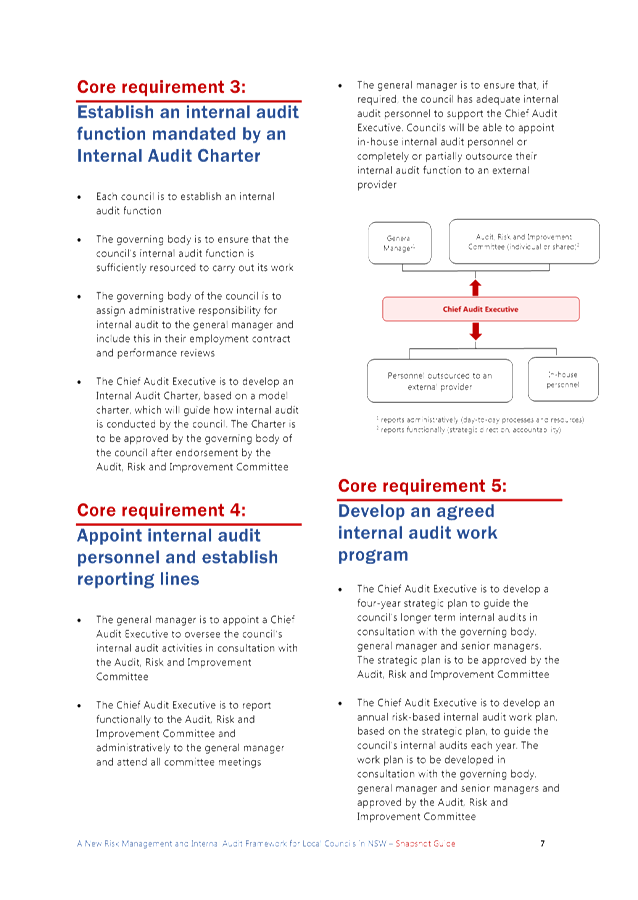

Core requirement 3: Establish an internal

audit function mandated by an Internal Audit Charter

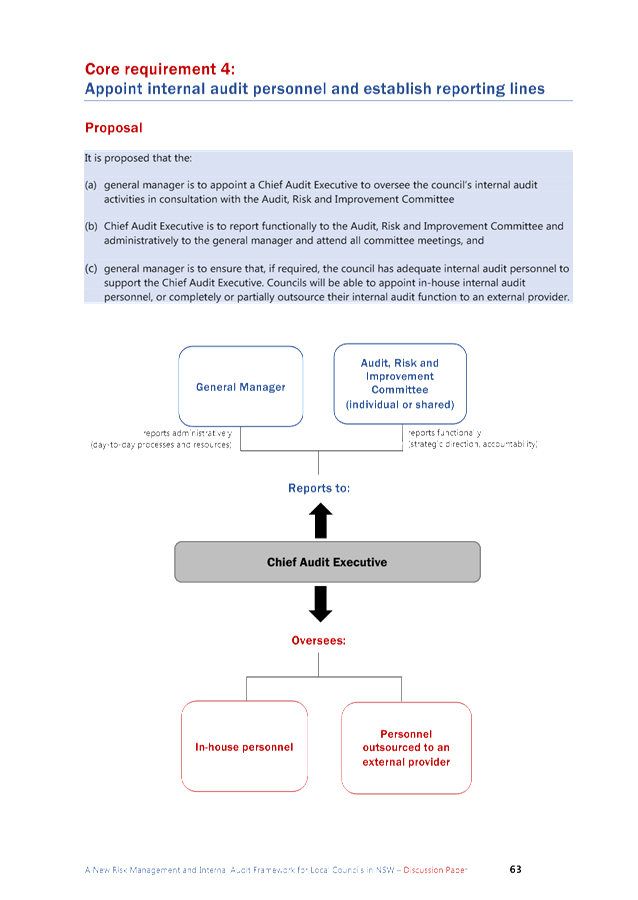

Core requirement 4: Appoint internal

audit personnel and establish reporting lines

Core requirement 5: Develop an agreed

internal audit work program

Core requirement 6: How to perform and

report internal audits

Core requirement 7: Undertake ongoing

monitoring and reporting

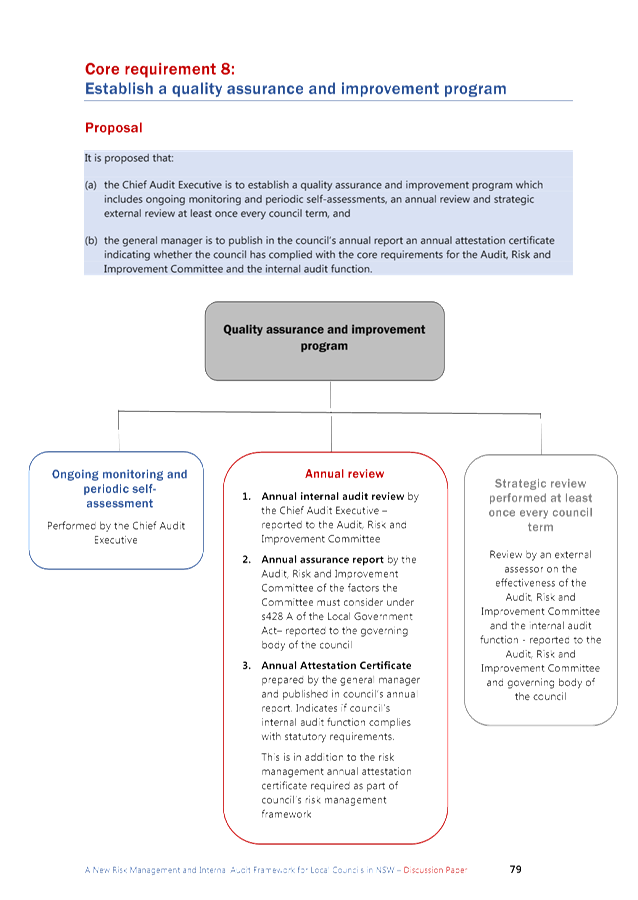

Core requirement 8: Establish a quality

assurance and improvement program

Core requirement 9: Councils can

establish shared internal audit arrangements

Key considerations from the

discussion paper

Implications for Joint

Organisation

The framework will apply to

councils, county councils, and joint organisations, therefore there will be a

requirement for the Northern Rivers Joint Organisation to have an ARIC. There

are potential opportunities to establish a shared ARIC with the joint

organisation and its member councils.

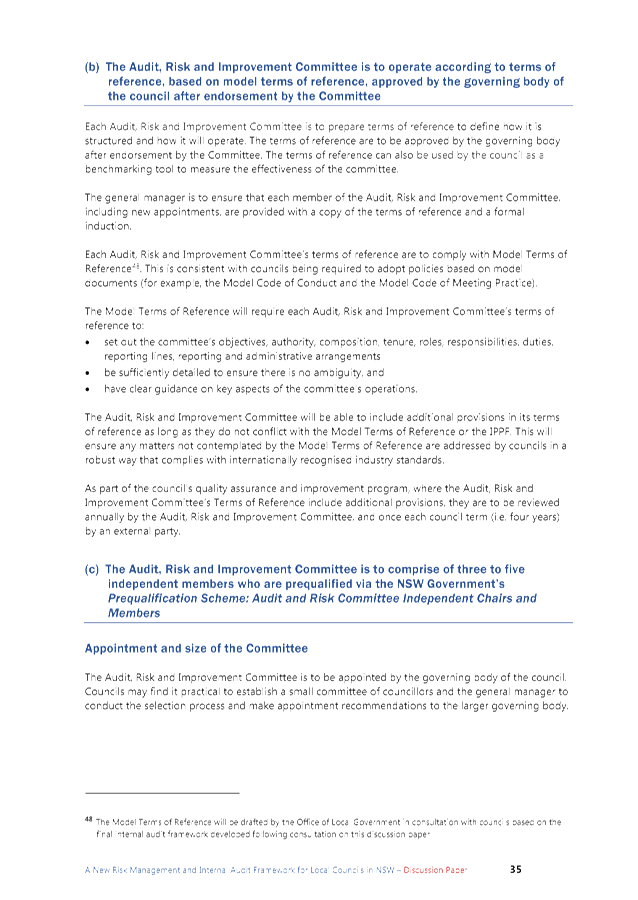

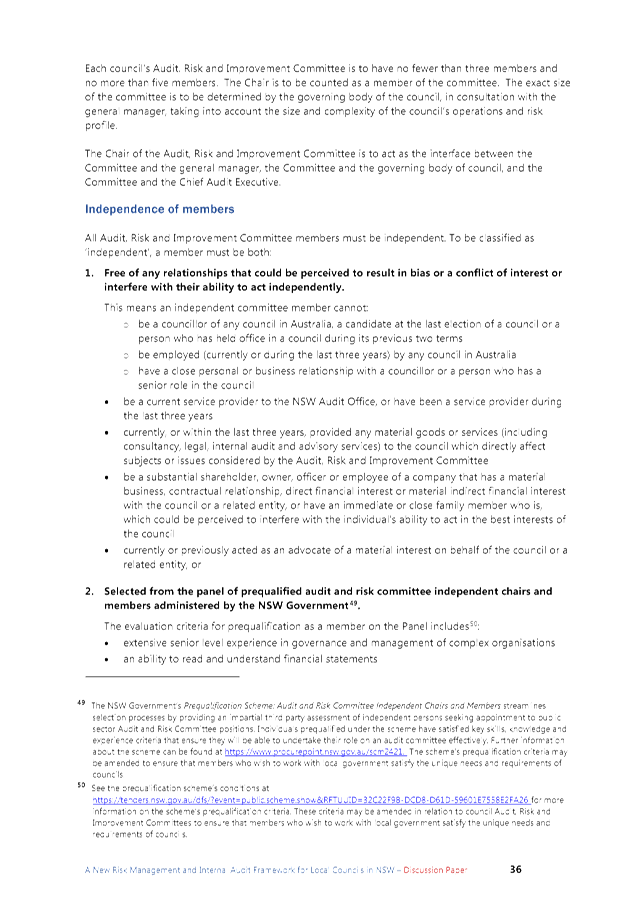

Implications for Membership

The ARIC is to comprise of three to five independent members who

are prequalified via the NSW Government’s Prequalification Scheme:

Audit and Risk Committee Independent Chairs and Members.

ARIC members and the Chair are to serve a three to five-year term.

A member’s term cannot exceed eight years and the Chair’s term

cannot exceed five years

All ARIC members must be

independent. To be classified as ‘independent’, a member must be:

1. Free of any relationships that could be

perceived to result in bias or a conflict of interest or interfere with their

ability to act independently

2. Selected from the panel of prequalified

audit and risk committee independent chairs and members administered by the NSW

Government.

Further details on specific

exclusions and requirements are provided on page 36-37 of attachment 1, but

notably, under the new regulations, Councillors would not be members of the

Audit, Risk, and Improvement Committee.

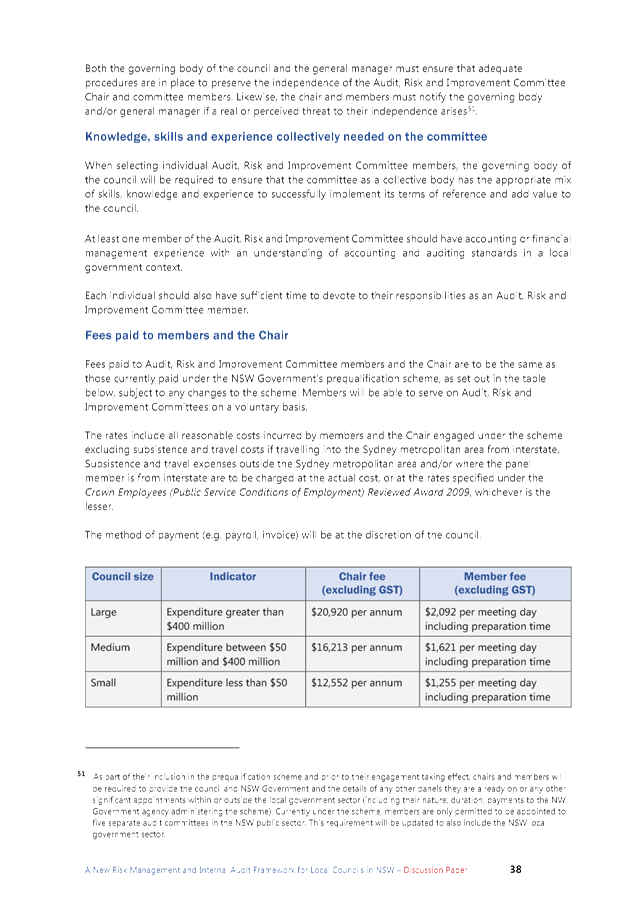

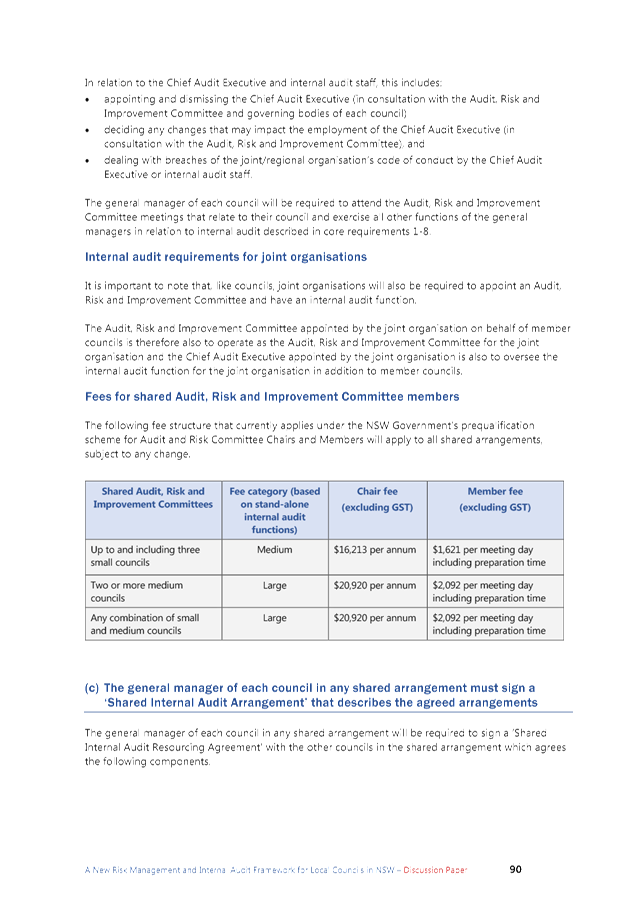

The discussion paper outlines

recommended fees to be paid to Audit, Risk, and Improvement Committee members,

while noting that members will be able to serve on Audit, Risk, and Improvement

Committees on a voluntary basis. The suggested member fee for a council the

size of Byron Shire is $1,621 per meeting date including preparation time and

$16,213 per annum for the Chair.

Reporting Lines

ARIC is to have direct and

unrestricted access to the General Manager, senior management and staff and

contractors of the council in order to perform its role. ARIC is also to have

direct and unrestricted access to the council resources and information it

needs to perform its role.

The General Manager is to appoint

a Chief Audit Executive to oversee internal audit activities. CAE is to report

functionally to ARIC and administratively to the GM.

An Annual Assurance Report to the

governing body of the council is to be prepared and be assessed by an external

party at least once each council term.

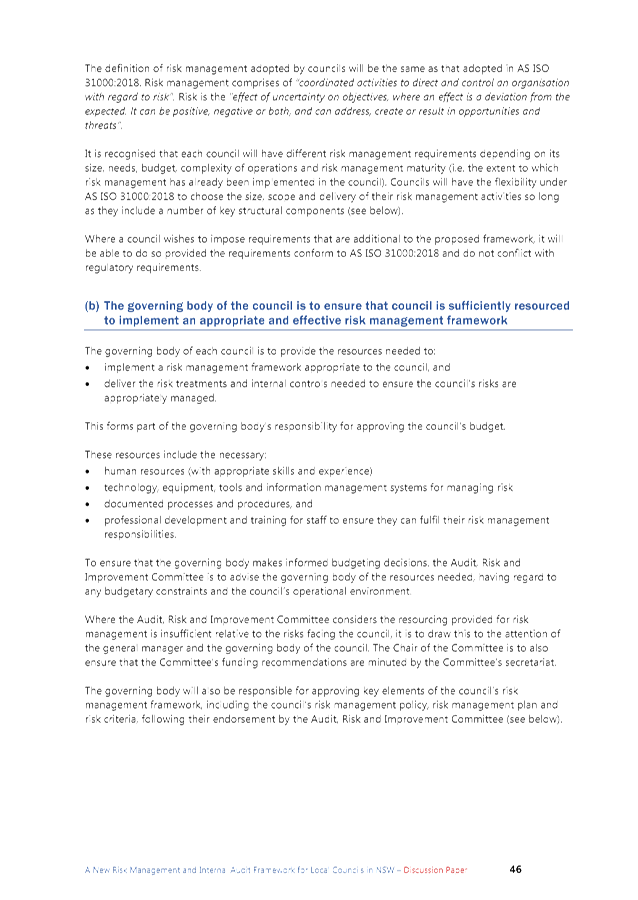

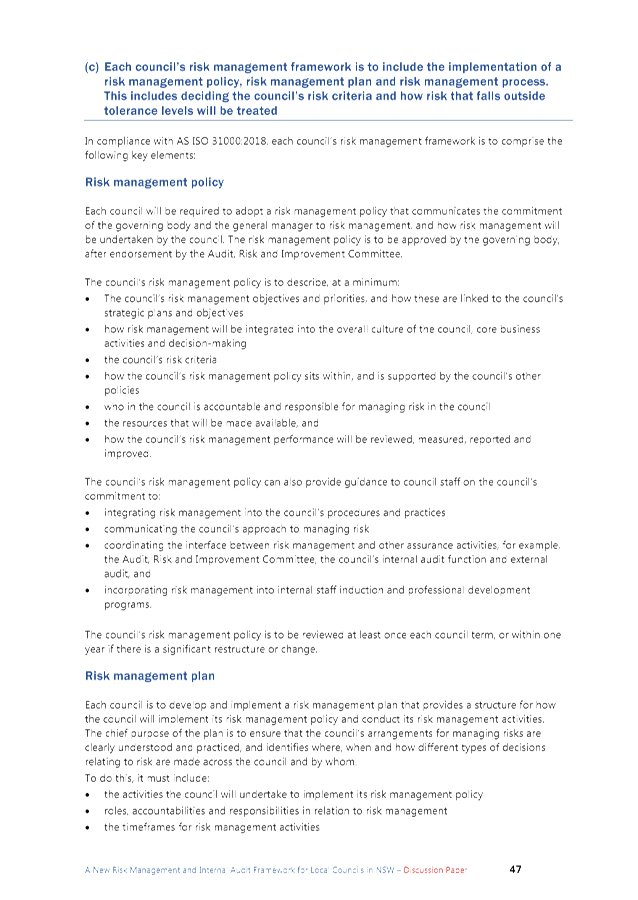

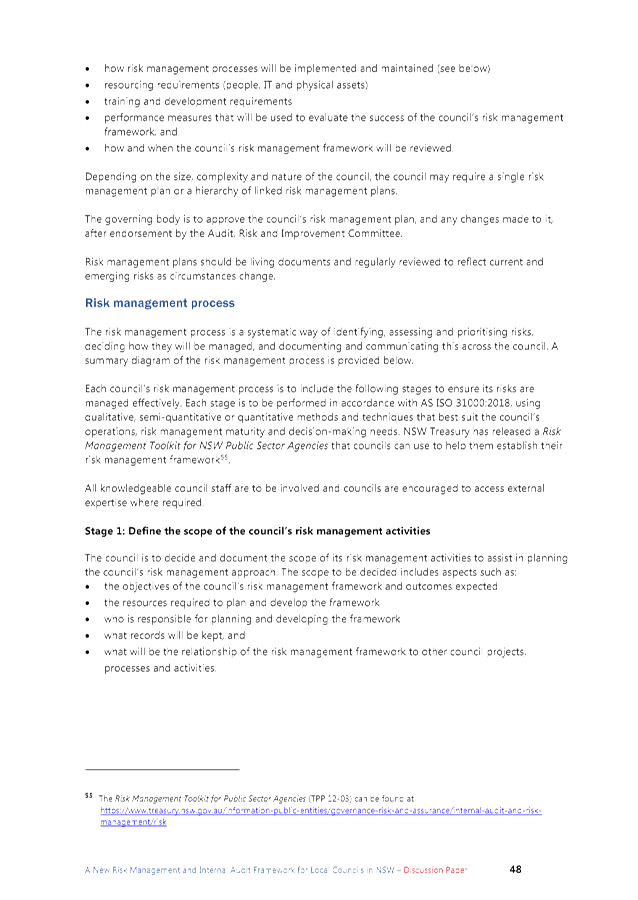

Implications for Risk Management

Council is required to establish a risk management framework

that is consistent with current Australian standards for risk management which

includes the implementation of a risk management policy, risk management plan

and risk management process.

Council is to fully integrate risk management into its

decision making, operational and integrated planning and reporting processes

and formally assign risk management responsibilities to the GM, senior managers

and other council staff and ensure accountability.

The General Manager is to appoint a Risk Management

Coordinator who will be responsible for the operational activities required to

implement the risk management framework and provide specialist risk management

skills and knowledge. The Risk Management Coordinator will report directly to

the GM or other member of senior management of Council in relation to

Council’s risk management function.

The risk management framework is to be regularly monitored

and reviewed, with ARIC providing independent assurance of risk management

activities.

The GM is to attest to Council’s compliance with the

risk management requirements in the Annual Report.

Next steps

Submissions to the Office of Local

Government (OLG) are to be made in writing by 31 December 2019. OLG has

suggested consideration of the following questions to inform submissions:

· Will the proposed framework achieve the outcomes sought?

· What challenges do you see for your council when

implementing the proposed framework?

· Does the proposed framework include all important elements

of an effective internal audit and risk framework?

· Is there anything you don’t like about the proposed

framework?

· Can you suggest improvements to the proposed framework?

Subject to comments from the

Committee, the following draft feedback is proposed:

|

Will the proposed framework

achieve the outcomes sought?

|

· The

proposed framework will assist Council in developing an effective internal

audit and risk management framework, noting that Byron already has a number

of the measures in place

|

|

What challenges do you see

for your council when implementing the proposed framework?

|

· Councillors

have a valuable role on ARIC which provides them with opportunities to

understand the audit and risk process and monitor outcomes. Council believes

that to lose this opportunity would be detrimental

· Sourcing

ARIC members that meet the independence and prequalification requirements

· Rotating

ARIC members

· What

is the process if Council rejects recommendations from the ARIC?

|

|

Does the proposed framework

include all important elements of an effective internal audit and risk framework?

|

· Council

considers the proposed framework covers all important elements of an

effective internal audit and risk management framework

|

|

Is there anything you

don’t like about the proposed framework?

|

· Council

is supportive of the proposed framework and is on track to meet the

requirements within the proposed timeframes

|

|

Can you suggest improvements

to the proposed framework?

|

· Council

submits that consideration should be given to creating a sliding scale for

payment of fees to ARIC members during the transition phase, commensurate

with the actual functions performed. There is an expectation that the role of

the ARIC will expand over time to cover a range of functions with full

compliance achieved by 2026 but there is no differentiation in the fees

between an established ARIC that is or will be fully compliant ahead of the

proposed timelines and an ARIC that has a limited focus whilst Council is

developing its internal functions in line with its resources and

capabilities.

|

STRATEGIC CONSIDERATIONS

Community Strategic Plan and

Operational Plan

|

CSP Objective

|

L2

|

CSP Strategy

|

L3

|

DP Action

|

L4

|

OP Activity

|

|

Community

Objective 5: We have community led decision making which is open and

inclusive

|

5.6

|

Manage

Council’s resources sustainably

|

5.6.7

|

Develop and

embed a proactive risk management culture

|

5.6.7.4

|

Manage Audit,

Risk and Improvement program including coordinating committee recommendations

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Legal/Statutory/Policy Considerations

The operation of sections 428A and 428B of the Local

Government Act will be supported by new regulations in the Local

Government (General) Regulation 2005.

Financial Considerations

Not applicable at this stage.

Consultation and Engagement

ET considered this report at its 30 October 2019 meeting and

noted the above feedback.

Staff Reports - Corporate and Community Services 4.1 - Attachment 1

Staff Reports - Corporate and Community Services 4.1 - Attachment 2

Staff Reports - Corporate and Community Services 4.2

Report No. 4.2 2018/2019

Financial Statements

Directorate: Corporate

and Community Services

Report

Author: James

Brickley, Manager Finance

File No: I2019/1843

Summary:

This item provides the Audit, Risk and Improvement Committee

with a report on the external audit for the financial year ended 30 June 2019.

It covers the financial results for Council for the 2018/2019 financial year

and the 2019 Audit Engagement Closing Report in respect of the audit provided

by the NSW Audit Office.

The 2018/2019 Financial Statements were to be considered by

the Audit, Risk and Improvement Committee on 10 October 2019 but as the audit

was not finalised by this date, the Meeting was cancelled. Council

adopted the 2018/2019 Financial Statements at its Ordinary Meeting held on 24

October 2019 through resolution 19-542 and will be presenting them

to the public at the Ordinary Meeting to be held on 28 November 2019.

|

RECOMMENDATION:

That the Audit, Risk and Improvement Committee notes

the report on the 2018/2019 Financial Statements and the 2019 Audit

Engagement Closing Report received from the NSW Audit Office.

|

Attachments:

1 Published

2018/2019 Financial Statements, E2019/78804

, page 135⇩

2 Confidential

- 2019 Audit Engagement Closing Report, E2019/80719

REPORT

This report has been prepared to brief the Audit, Risk and

Improvement Committee on the external audit for the financial year ended 30

June 2019. The report covers the financial results for Council It covers the

financial results for Council for the 2018/2019 financial year and the 2019

Audit Engagement Closing Report in respect of the audit provided by the NSW

Audit Office.

The 2018/2019 Financial Statements were to be considered by

the Audit, Risk and Improvement Committee on 10 October 2019 but as the audit

was not finalised by this date, the Meeting was cancelled. Council

adopted the 2018/2019 Financial Statements at its Ordinary Meeting held on 24

October 2019 via resolution 19-542 and will be presenting them to the

public at the Ordinary Meeting to be held on 28 November 2019. Council

received a presentation from the External Auditor at its Ordinary Meeting held

on 24 October 2019. The presentation was made by Mr Adam Bradfield from Thomas

Noble and Russell as the representative firm for the Audit Office of NSW.

The 2018/2019 Financial Statements were lodged with the

Office of Local Government on 25 October 2019.

The Financial Statements and Auditor’s Reports are a

statutory requirement and provide information on the financial performance of

Council over the previous twelve-month period.

The Final 2018/2019 Financial Statements are provided at

Attachment 1 with brief explanations for the contents of Attachment 1 as

follows:

General Purpose Financial

Statements

These Statements provide an overview of the operating result, financial

position, changes in equity and cash flow movement of Council as at 30 June

2019 on a consolidated basis with internal transactions between Council’s

General, Water and Sewerage Funds eliminated. The notes included within these

reports provide details of major items of income and expenditure with

comparisons to the previous financial year. The notes also highlight the cash

position of Council and indicate which funds are externally restricted (i.e.

may be used for a specific purpose only), and those that may be used at

Council’s discretion.

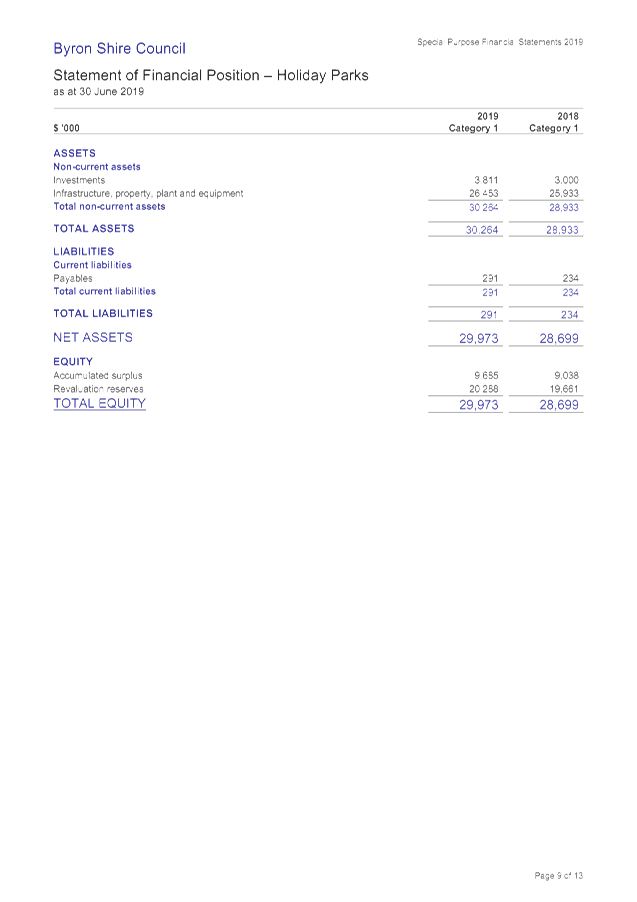

Special Purpose Financial Statements

These Statements are a result of the implementation of the National

Competition Policy and relate to those aspects of Council’s operations

that are business oriented and compete with other businesses with similar

operations outside the Council. Mandatory disclosures in the Special Purpose

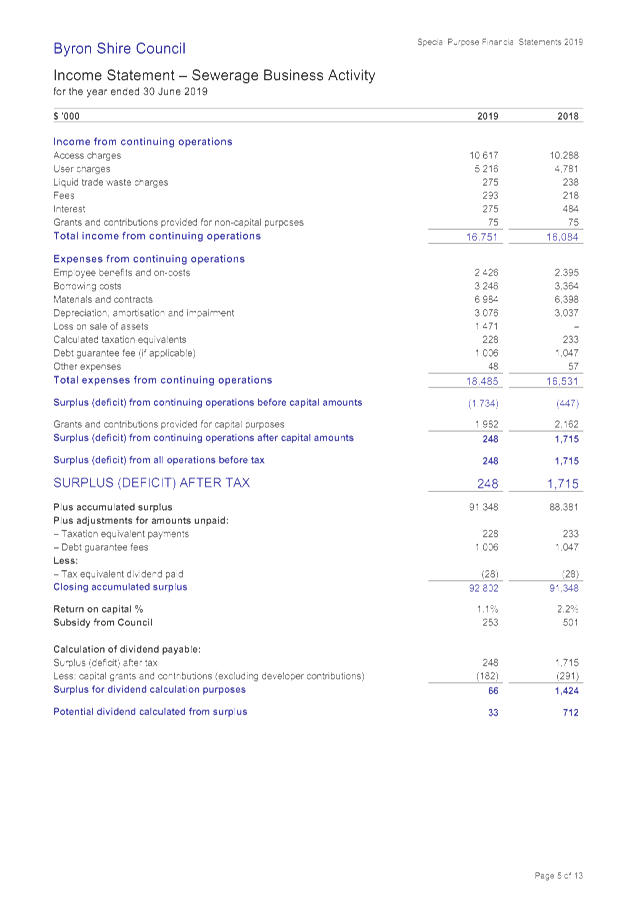

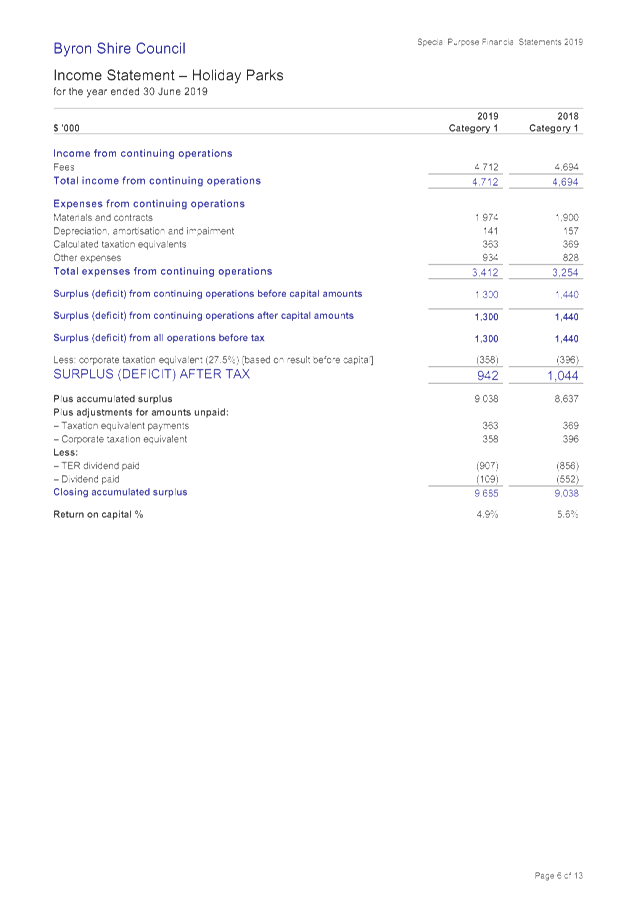

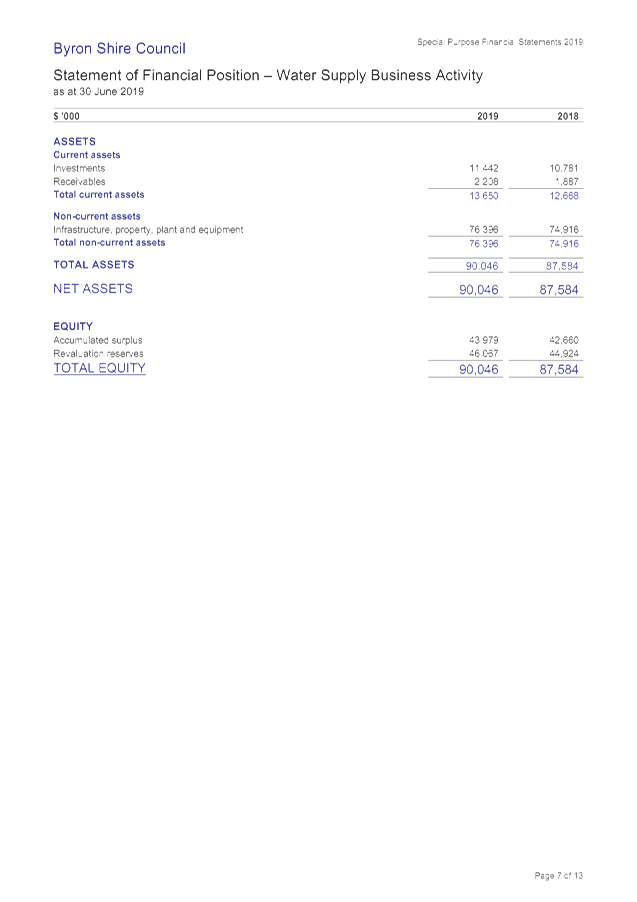

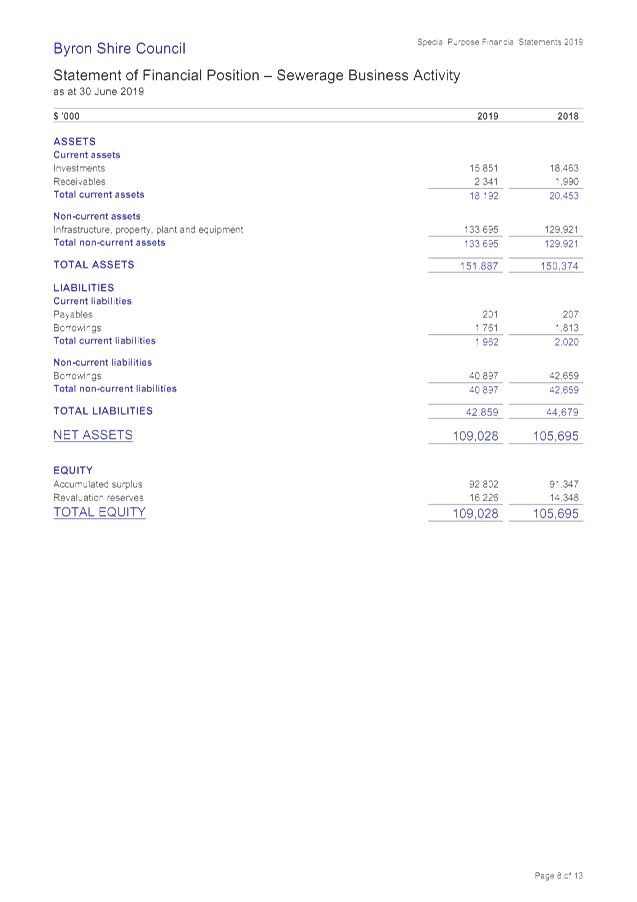

Financial Reports are Water and Sewerage. Additional disclosure relates

to Council business units that Council deems ‘commercial’. In

this regard Council has traditionally reported its Caravan Park Operations

(Suffolk Beachfront Holiday Park and First Sun Holiday Park) on a combined

basis. These financial reports must also classify business units in the

following categories:

· Category 1 –

operating turnover is greater than $2million

· Category 2 –

operating turnover is less than $2million

All of Council’s business units are classed as

Category 1 with all having operating turnover greater than $2 million.

Another feature of the Special Purpose Financial Reports is

to build taxes and charges where not physically incurred into the financial

results to measure the results on a level playing field with other

organisations operating similar businesses, who are required to pay these

additional taxes and charges. These taxes and charges include:

· Land tax – Council

is normally exempt from this tax so notional land tax is applied.

· Income tax –

Council is exempt from income tax and in regard to these reports, company

tax. Any surplus generated has a notional company tax applied to it.

· Debt guarantee fees

– Generally due to the low credit risk associated with Councils, Councils

can often borrow loan funds at lower interest rates then the private

sector. A debt guarantee fee inflates the borrowing costs by

incorporating a notional cost between interest payable on loans at the interest

rate borrowed by Council and one that would apply commercially.

In regard to the Special Purpose Financial Reports, these

are prepared on a non consolidated basis or in other words grossed up to

include any internal transactions with the General Fund.

Special Schedules

These schedules are prepared essentially for use by the Australian Bureau

of Statistics, the NSW Grants Commission, the Office of Local Government, and

are primarily used to gather information for comparative purposes. Special

Schedules 3 to 6 are also used by the Department of Primary Industries (NSW

Office of Water) in analysing the performance of the Water and Sewer Funds and

are also non consolidated and grossed up including internal transactions.

Special Schedule 7 (now called a Report on Infrastructure) provides an

approximate value of what funds are needed for the maintenance and renewal of

Council assets in comparison to what is currently allocated in the budget.

Special Schedule 2 is also included, which is a disclosure regarding

Council’s compliance with General Rate revenue raising and rate

pegging. Special Schedule 2 is also subject to separate external audit

aside from the financial statements.

The Special Schedules are no longer published from the

2018/2019 financial year following revision of the Local Government Code of

Accounting Practice. They are still prepared but lodged separately to the

Office of Local Government via the Financial Data Return. Given they are

no longer published, they are not included in Attachment 1. Aside from Special

Schedule 2, they have never been subject to external audit.

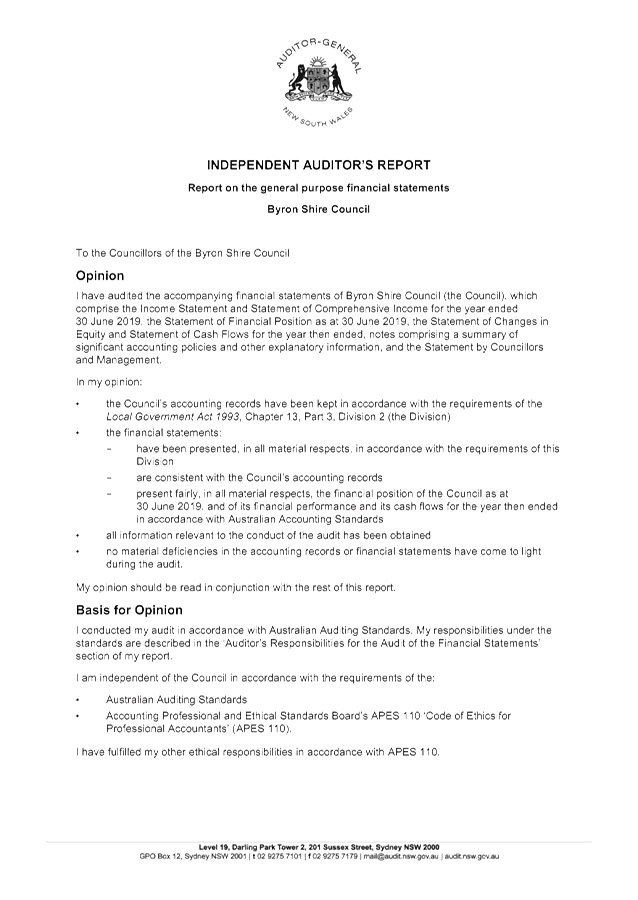

Auditors Reports on the

Financial Statements

Council’s auditors, the Auditor General of NSW (NSW Audit Office) and

its representative firm Thomas Noble and Russell, have completed their audit of

the 2018/2019 Financial Statements. All matters identified during the

audit have been adjusted and included in the 2018/2019 Financial Statements (if

required) included at Attachments 1. The Auditor’s Reports cover:

· A report on the

conduct of the audit. This report states the financial statements have been

audited with an opinion. For the year ended 30 June 2019 the opinion is

unmodified. In addition, this report outlines significant audit issues

and observations, and an analysis of the major aspects of the financial

statements.

· An Audit

Engagement Closing Report. This report (Confidential Annexure 2) does not

form part of the Financial Statements but is provided to assess audit findings,

usually prior to signing the Audit Representation Letter and the Statements by

Council and Management. This report is provided specifically for the Audit,

Risk and Improvement Committee for consideration but given the sequence of

events for the 2018/2019 Financial Statements, this was not able to be achieved

prior to signing the Financial Statements. Confidential Annexure 2 would

normally have been provided to the 10 October 2019 Audit, Risk and Improvement

Committee.

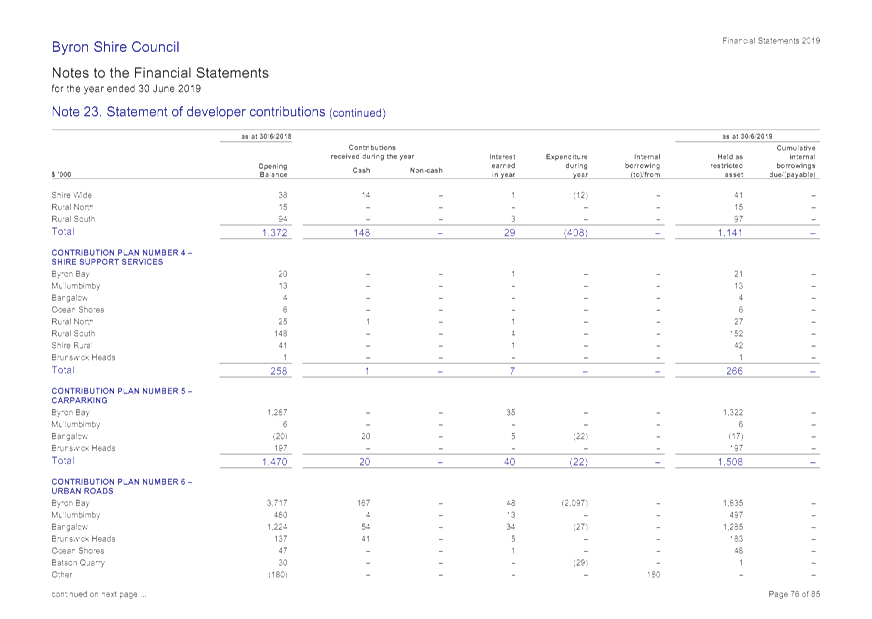

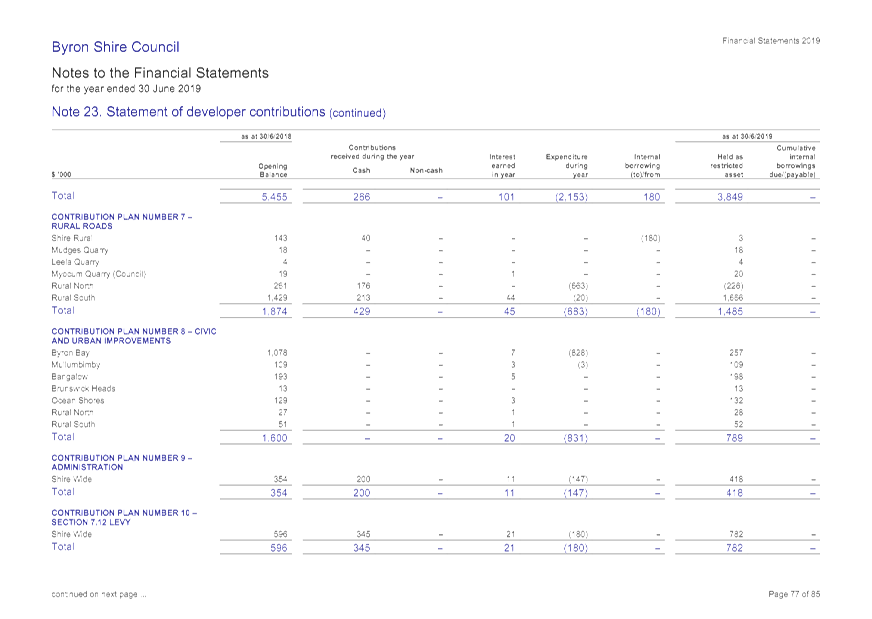

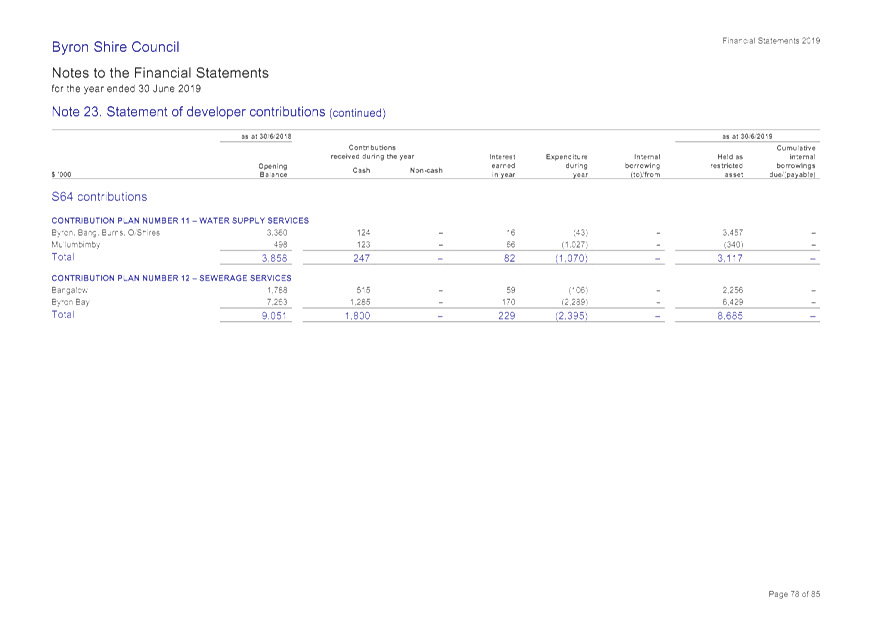

Specific Items relating to 2018/2019 Financial Statements

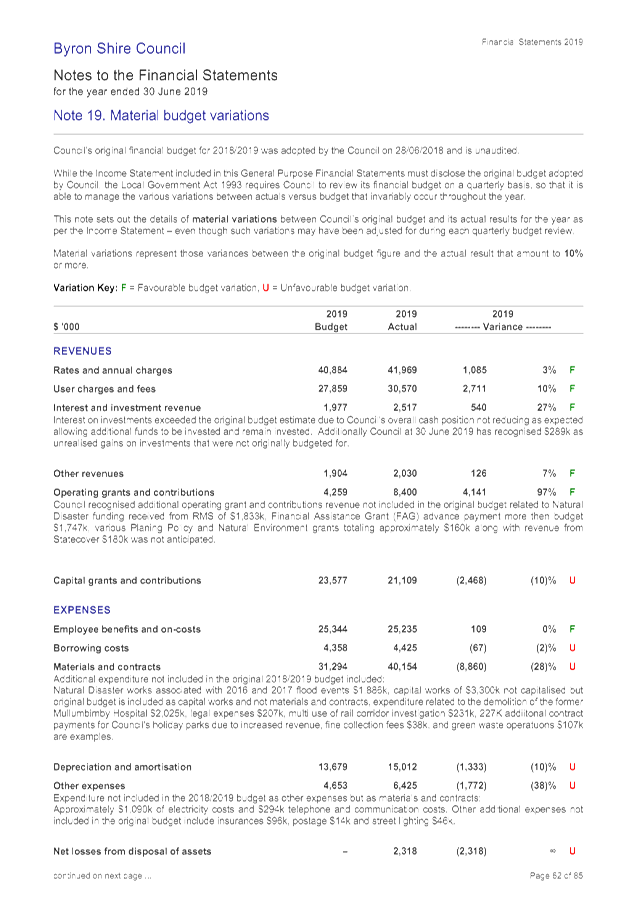

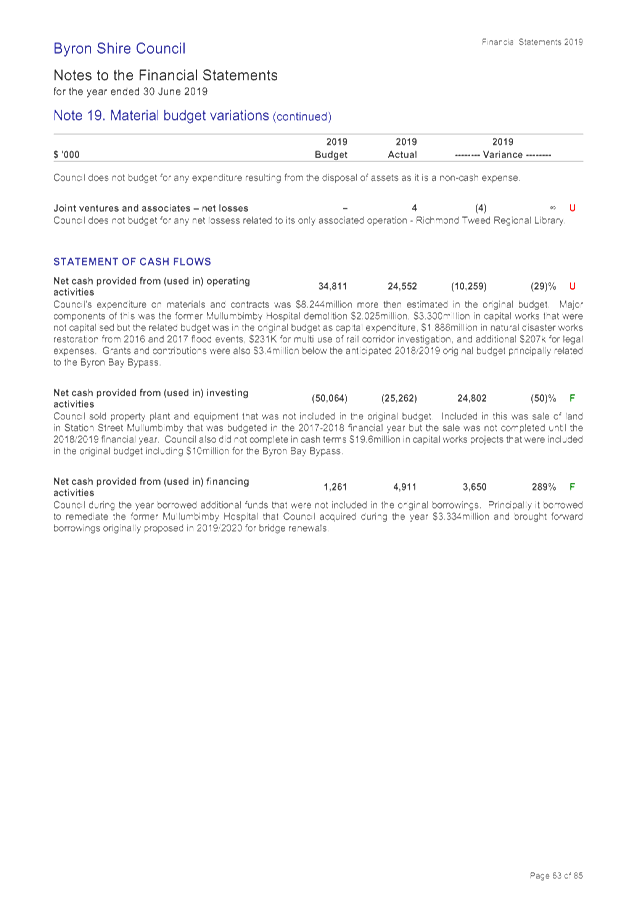

The 2018/2019 Financial Statement results have been impacted

by the following items that require explanation:

· Operating

Result from Continuing Operations

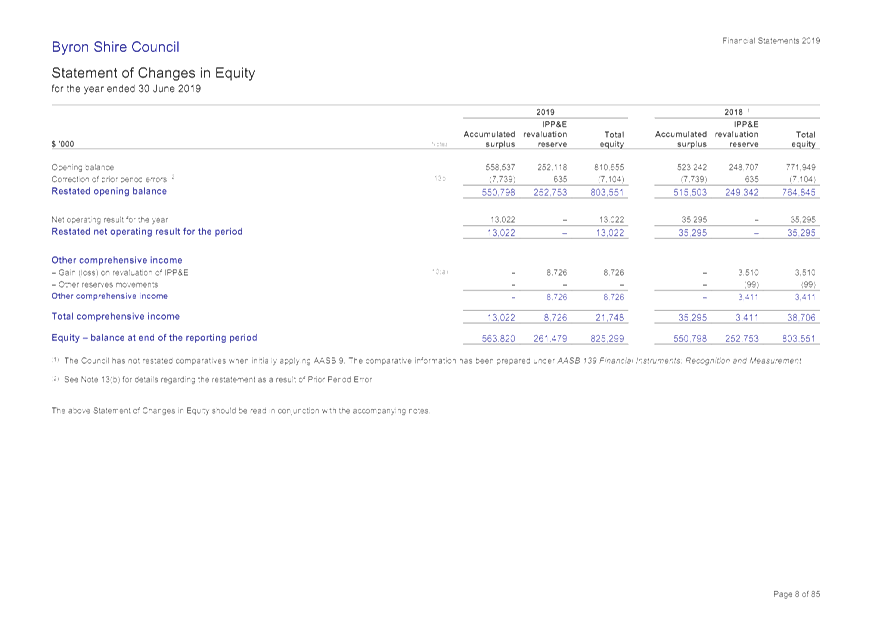

The 2018/2019 financial year has seen a positive overall

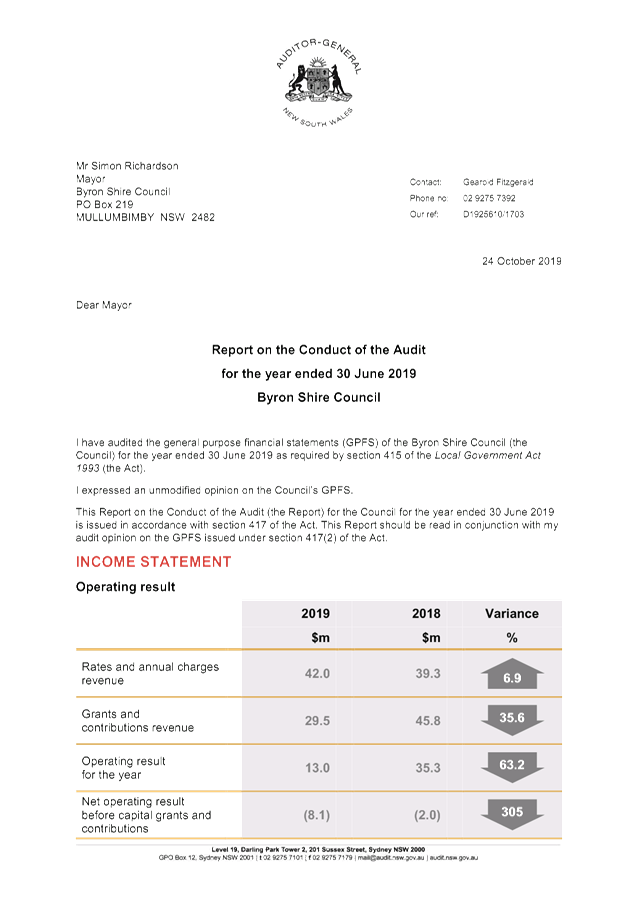

financial result. Council recorded a $13.022million surplus which, while less

than the $35.295million surplus in 2017/2018, is still nevertheless a surplus.

This result incorporates the recognition of capital revenues such as capital

grants and contributions for specific purposes and asset dedications amounting

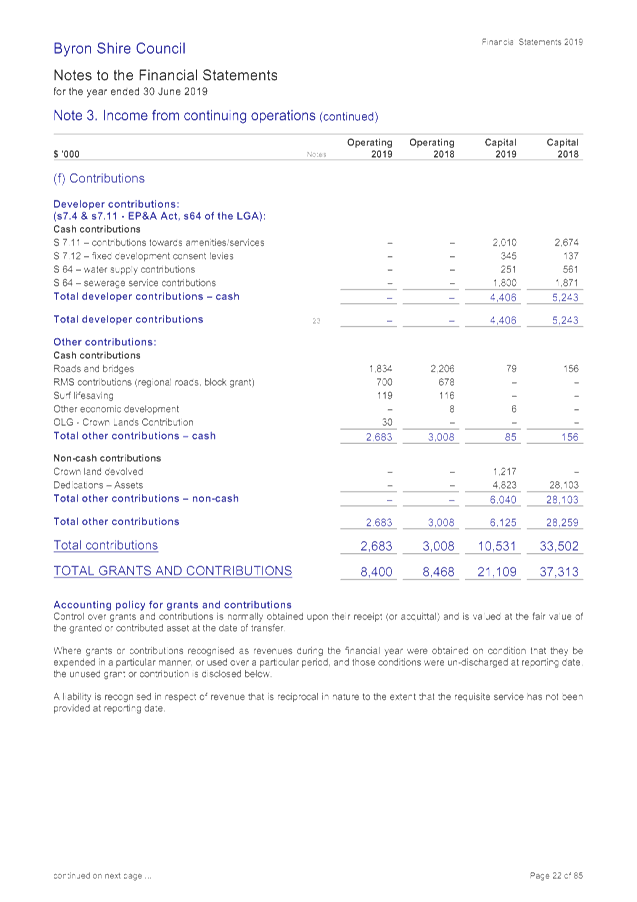

to $21.109 million compared to $37.314million in 2017/2018. Capital grants and

contributions in 2017/2018 were significantly influenced by the transfer of

assets to Council from the Old Pacific Highway that was not repeated in

2018/2019.

A more important indicator is the operating result before

capital grants and contributions. This result was a deficit of $8.087 million

in 2018/2019 compared to a deficit of 2.018million in 2017/2018 representing a

decrease of $6.069million between financial years. This indicates

Council’s operating expenditures exceeded its operating revenues. Whilst

operating revenues excluding capital grants and contributions grew by

$2.383million, overall operating expenses grew by $8.452million.

With reference to the Income Statement to the General

Purpose Financial Reports included at Attachment 1, the following table

indicates the major changes between 2018/2019 and 2017/2018 by line item:

|

Item

|

Change between 2018/2019 and 2017/2018 $’000

|

Change

Outcome

|

Comment

|

|

Income

|

|

|

|

|

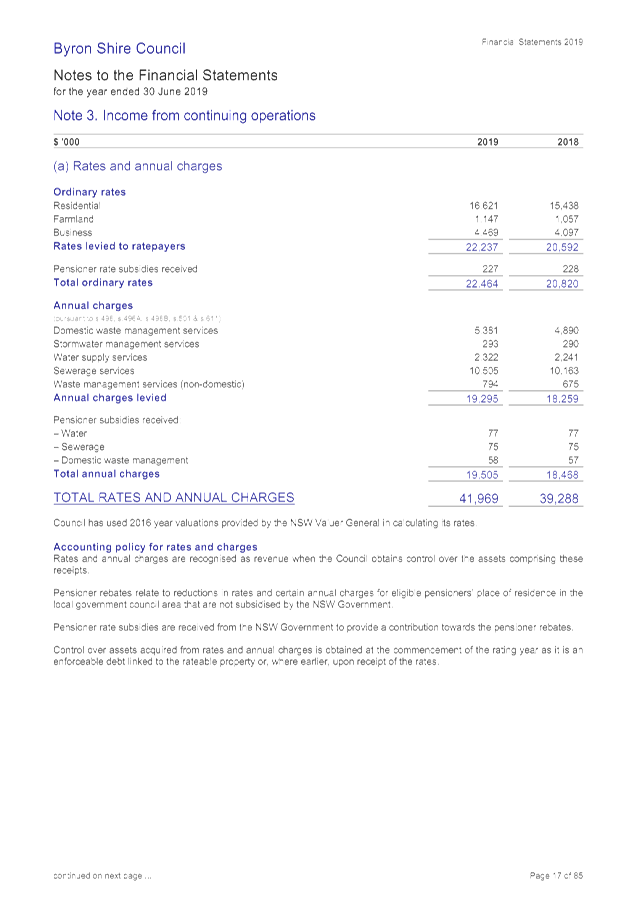

Rates & Annual Charges

|

+$2,681

|

Increase

|

Reflects imposition of the

second year of the 7.50% Special Rate Variation and changes in annual charges

from Council’s adopted 2018/2019 Revenue Policy

|

|

User Charges and Fees

|

+$626

|

Increase

|

Major changes include

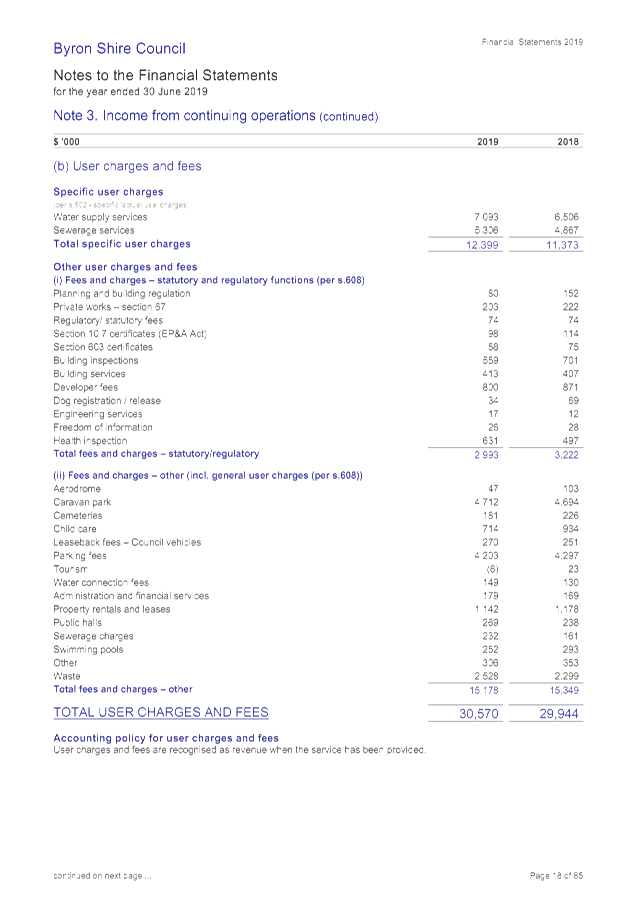

additional $1,026k revenue for water and sewer user charges, increase in

waste fees $229K and a decline in statutory/regulatory fees of $229k. Further

information is available in Note 3(b) to Attachment 1.

|

|

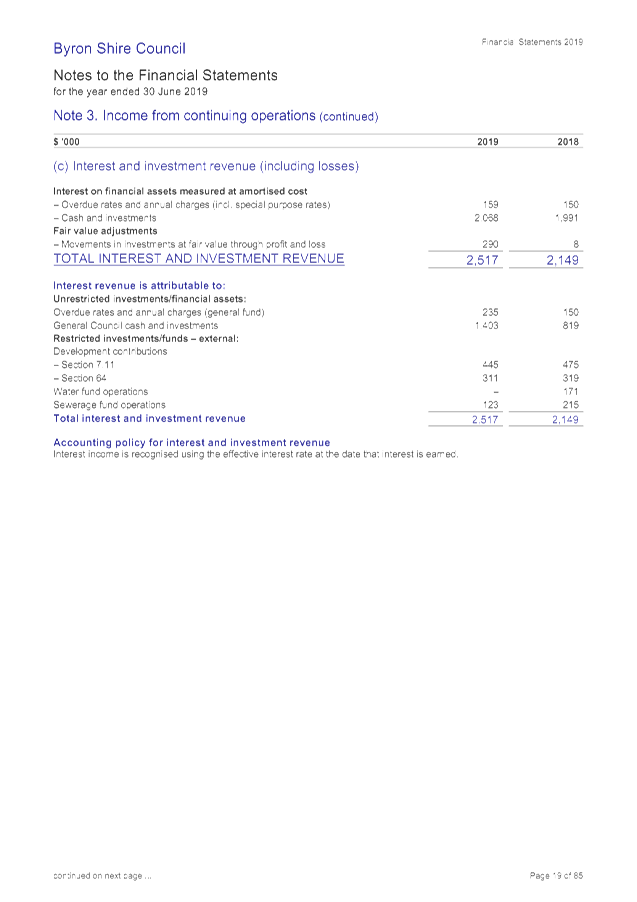

Interest and Investment

Revenue

|

+$368

|

Increase

|

Council’s cash

position did not decline as expected which enabled more funds to be invested

even though interest rates have continued to decline. Council also realised a

$290k fair value gain on its investments.

|

|

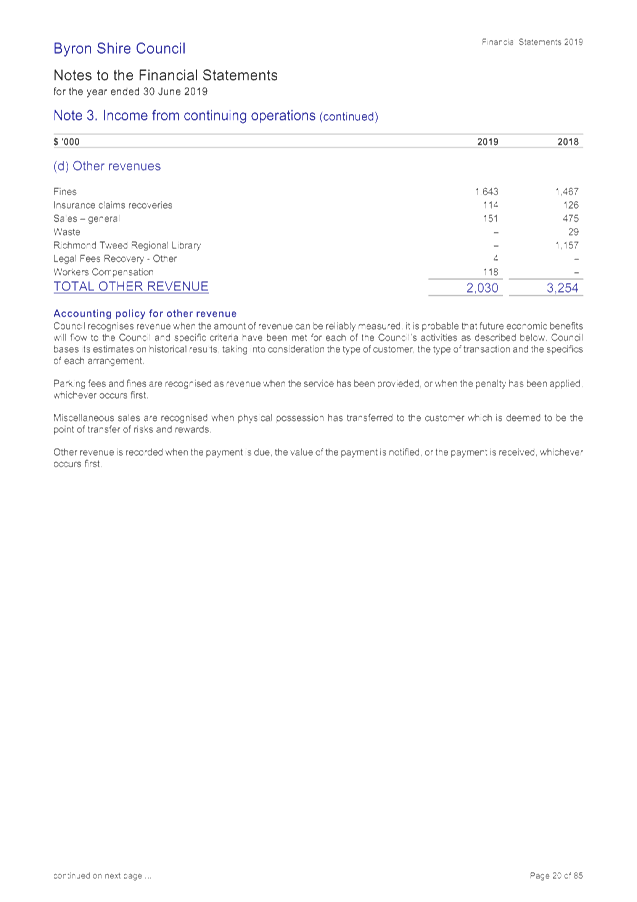

Other Revenues

|

-$1,224

|

Decrease

|

Increase of $176k for

fines, but major change was the once off recognition of share in Richmond

Tweed Regional Library $1,157k in 2017/2018 that was not repeated in

2018/2019.

|

|

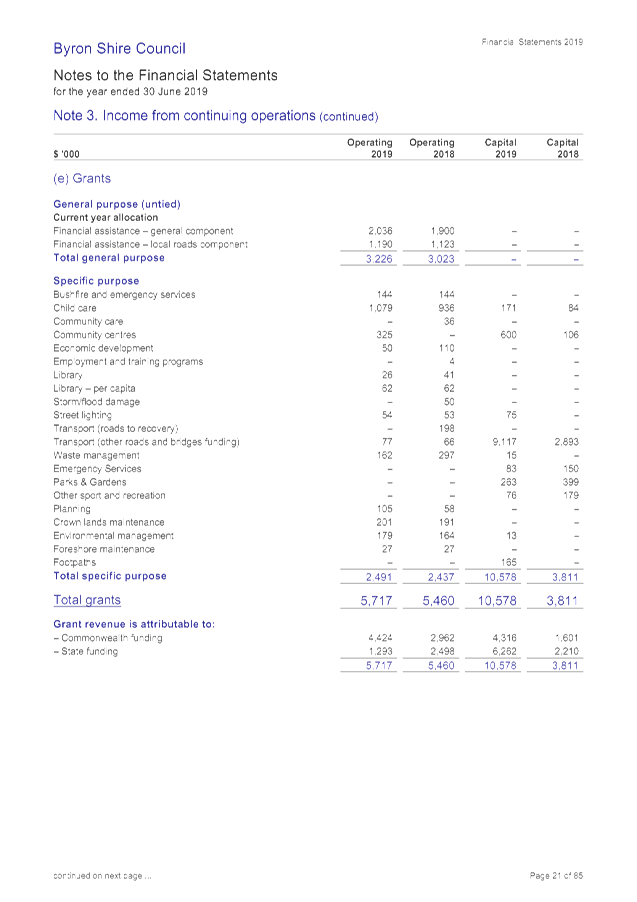

Grants & Contributions

– Operating

|

-$68

|

Decrease

|

Overall operating grants

increased by $257k including 205k increase in the Financial Assistance Grant but

contributions reduced by $325k. Further information is available in

Note 3€ and Note 3(f) to Attachment 1.

|

|

Grants & Contributions

– Capital

|

-$16,204

|

Decrease

|

Capital grants increased

$6,767k mainly for roads and bridges funding but capital contributions

revenue decreased $22,971k. Reduction in capital contributions is due

to reduced asset dedication revenue that was significant in 2017/2018 from

the dedication of former Pacific Highway assets.

|

|

Total Income Change

|

-$13,821

|

Decrease

|

|

|

|

|

|

|

|

Expenditure

|

|

|

|

|

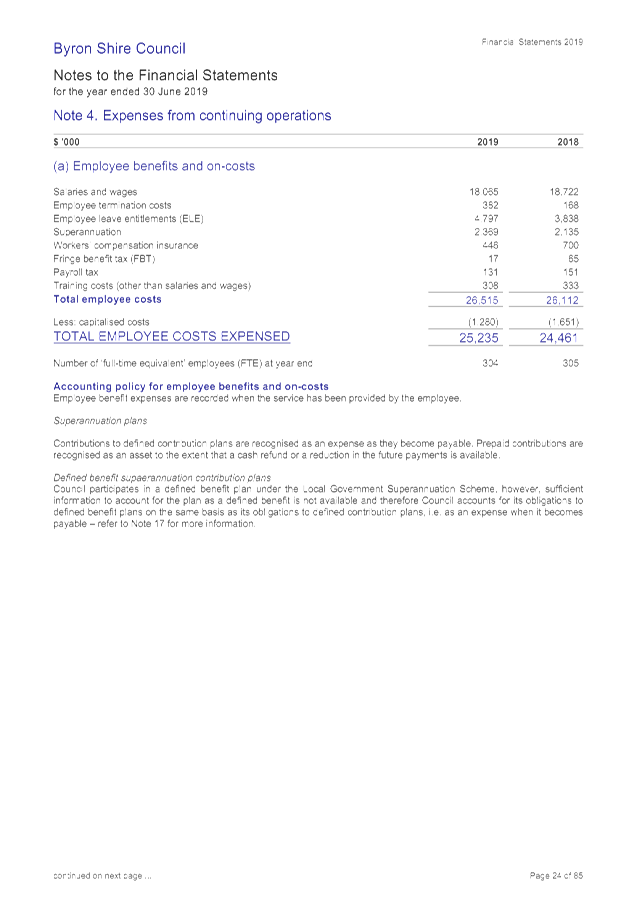

Employee Benefits and

Oncosts

|

+$774

|

Increase

|

Increased leave entitlement

expenses of $959k reflecting emphasis on controlling leave balances and

impact of declining interest rates on present value of liability

calculations. There was a decrease of $371k of employee costs capitalised on

capital works in 2018/2019 compared to 2017/2018 and gross salary and wages

$657k. More information is provided at Note 4(a) to Attachment 1.

|

|

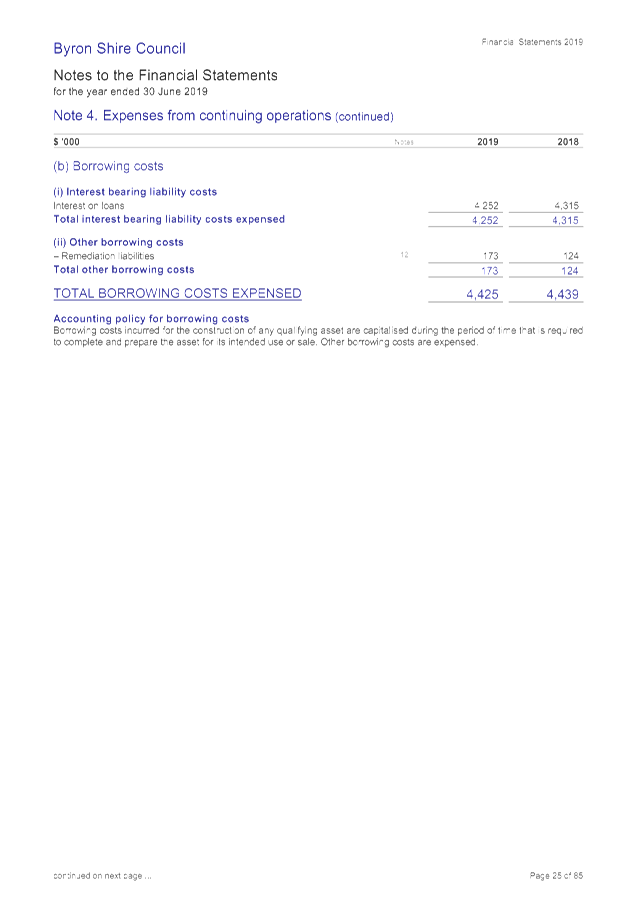

Borrowing Costs

|

-$14

|

Decrease

|

Results from Council

gradually repaying loans and not borrowing significant new loans. New

loans of $7.669million borrowed at end of 2018/2019 financial year.

Interest impact of this loan will be realised commencing in 2019/2020 and

refinancing of significant sewerage loan in December 2019.

|

|

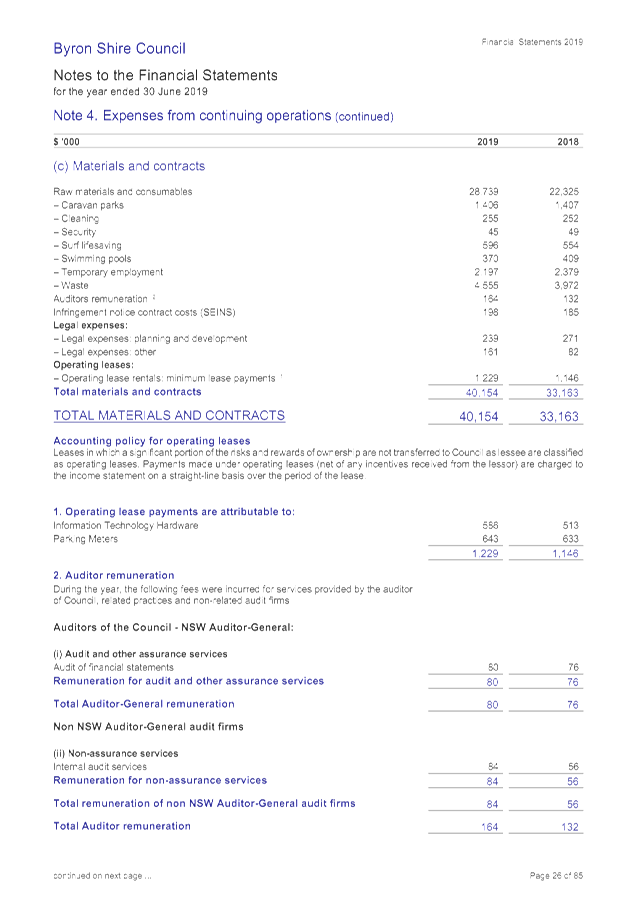

Materials & Contracts

|

+$6,991

|

Increase

|

Raw materials and contracts

increased of $6,414k. Major contributor to this was former Mullumbimby

Hospital demolition $2,025k, natural disaster works $1,886k and capital

expenditure $3,300k not capitalised. Other changes can be found at Note 4(b)

to Attachment 1.

|

|

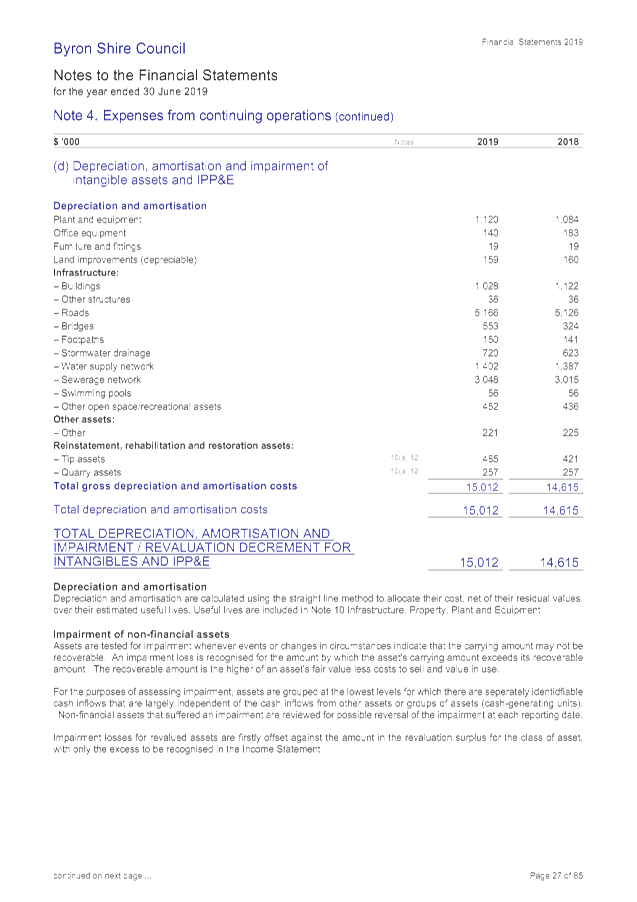

Depreciation

|

+$397

|

Increase

|

Respective changes between

asset classes are outlined at Note 4(d) to Attachment 1. Essentially

small incremental increases in each asset class.

|

|

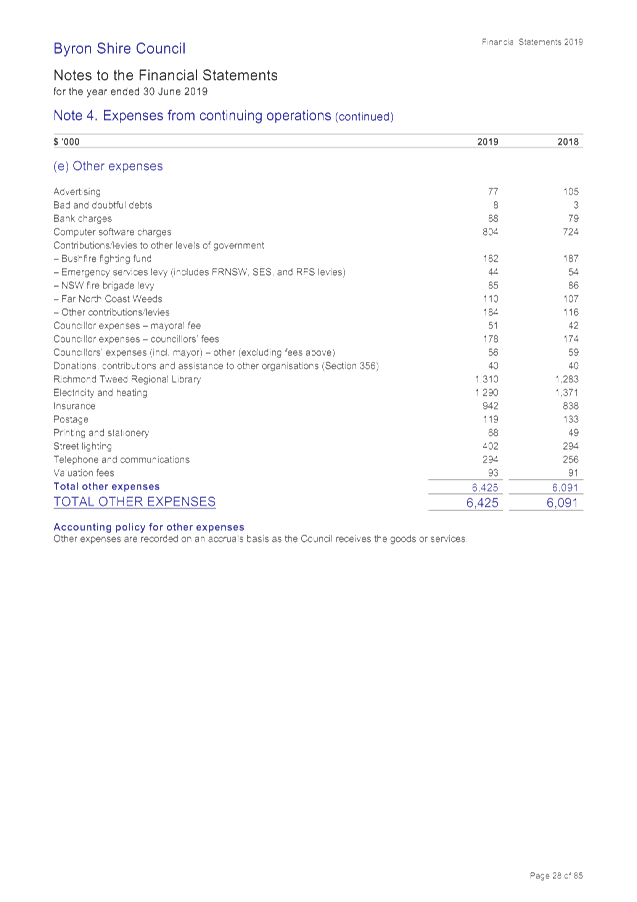

Other Expenses

|

+$334

|

Increase

|

Overall increase but there

were variations in line items as disclosed at Note 4(e) to Attachment 1. Most

significant item was street lighting $108k.

|

|

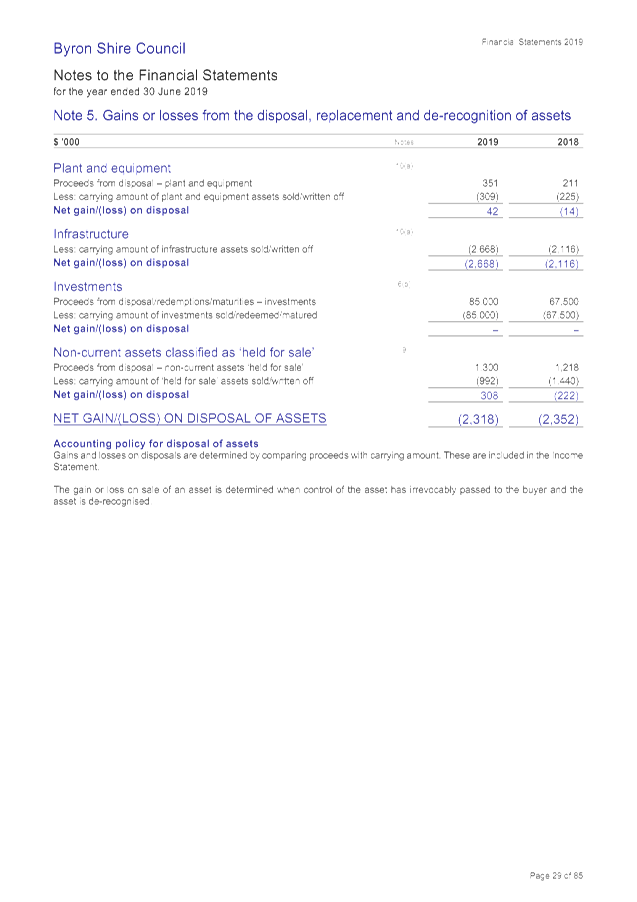

Net Losses from Disposal of

Assets

|

-$34

|

Decrease

|

Reflection of the written

down value of assets disposed at the end of financial year and is contingent

upon the extent of assets disposed and their written down value at the time

of disposal which can vary. For 2018/2019, Council has more disposals than

gains including the disposal of infrastructure $2,668k, plant and equipment

$42k gain and gain on sale of land $308k. Further details can be found at

Note 5 to Attachment 1

|

|

Net share of interests in

associates

|

+4

|

Increase

|

Recognition of

Council’s share of the operating result of Richmond Tweed Regional

Library for 2018/2019

|

|

Total Expenditure Change

|

+$8,452

|

Increase

|

|

|

|

|

|

|

|

Change in Result

|

-$22,273

|

Decrease

|

Decrease in overall surplus

between financial years.

|

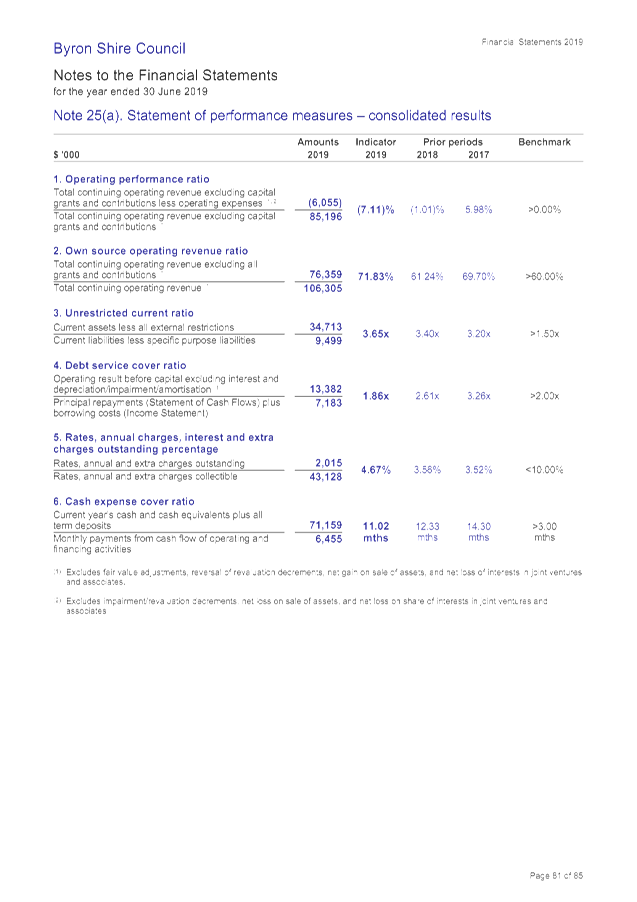

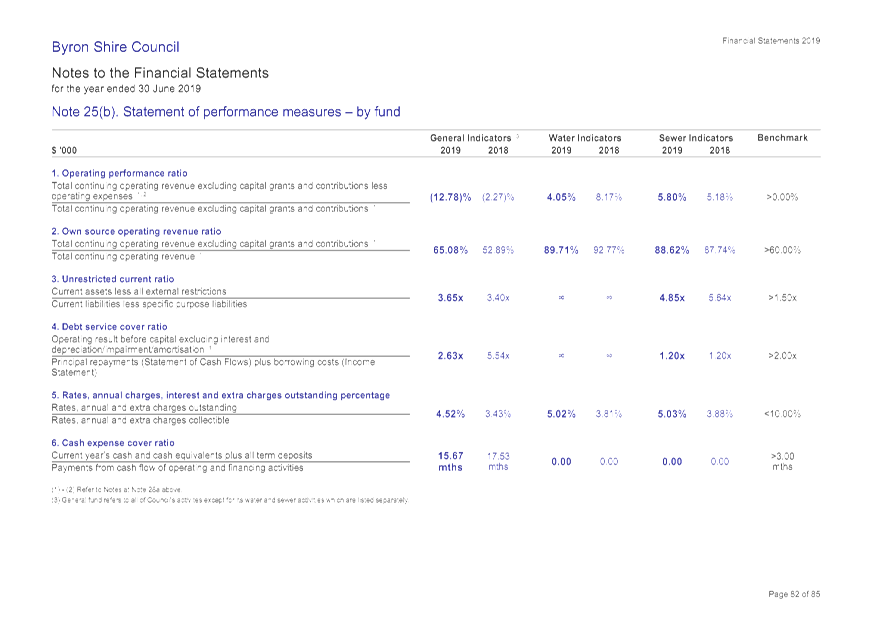

Following from the operating results, are the performance

ratios at Note 25 to the General Purpose Financial Statements. These have

been derived following the financial assessments undertaken by NSW Treasury

Corporation on all NSW Councils in 2012, and are now incorporated into the

latest update to the Code of Accounting Practice and Financial Reporting that

determines the content of Council’s Financial Statements. These ratios

present either a stable or improving result for Council except for the

following:

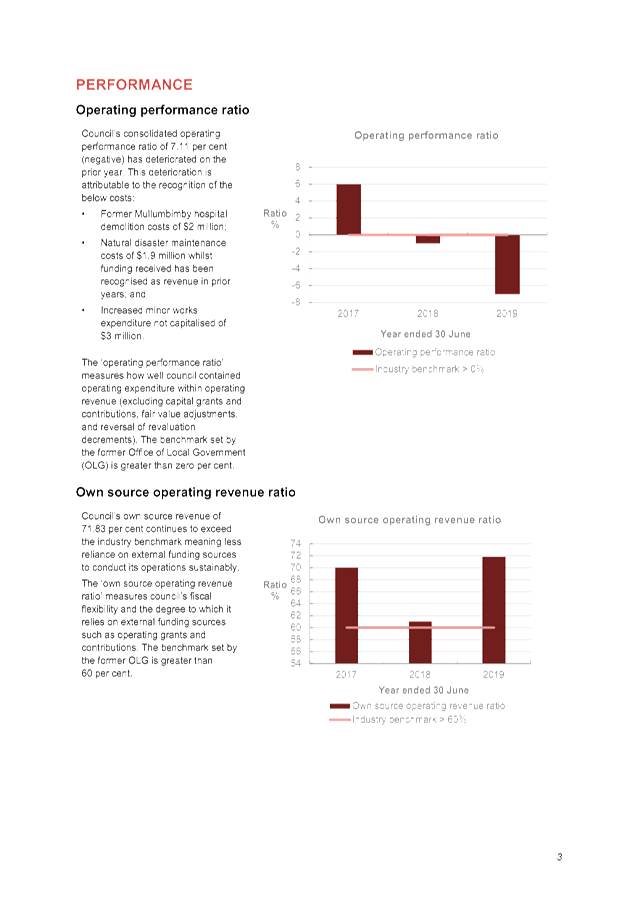

1. Operating

Performance Ratio is a reflection of the operating result of Council. The

benchmark is to be greater than 0% but in 2017/2018 Council’s ratio was

-1.01% and in 2018/2019 it was -7.11%. This ratio was impacted by some

one-off items i.e. demolition costs of the former Mullumbimby Hospital, however

Council will look to improve this result back towards the benchmark.

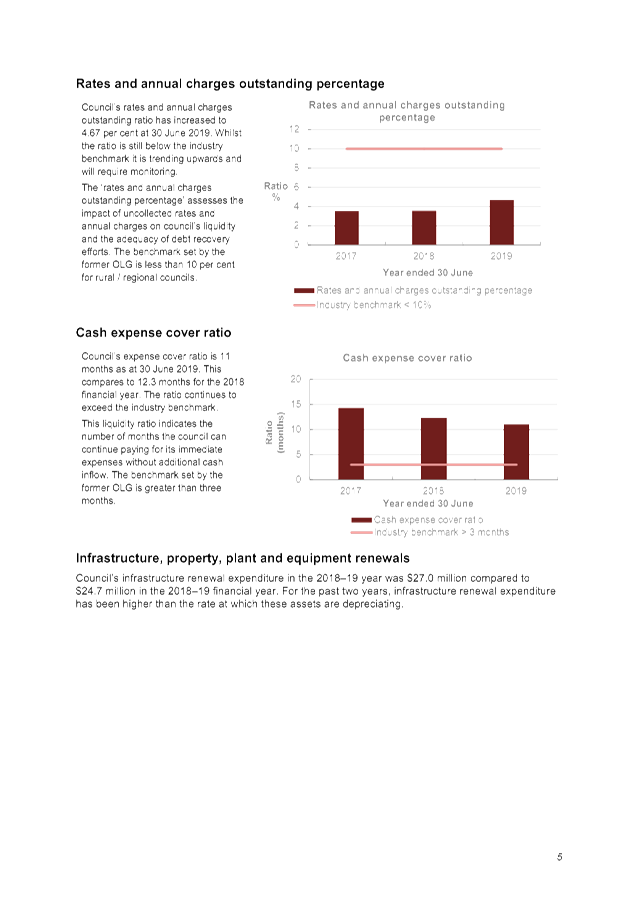

2. Outstanding,

Rates and Annual Charges – Whilst still well within benchmark ,this ratio

has increased given the compounding from the ongoing implementation of the

2017/2018 Special Rate Variation. This means that the increasing annual

charges, as well as the current economic climate, are impacting the capacity of

ratepayers to pay. Council also changed its Debt Recovery Policy during

the 2018/2019 financial year and this ratio will be closely monitored going forward.

· Asset

Revaluations

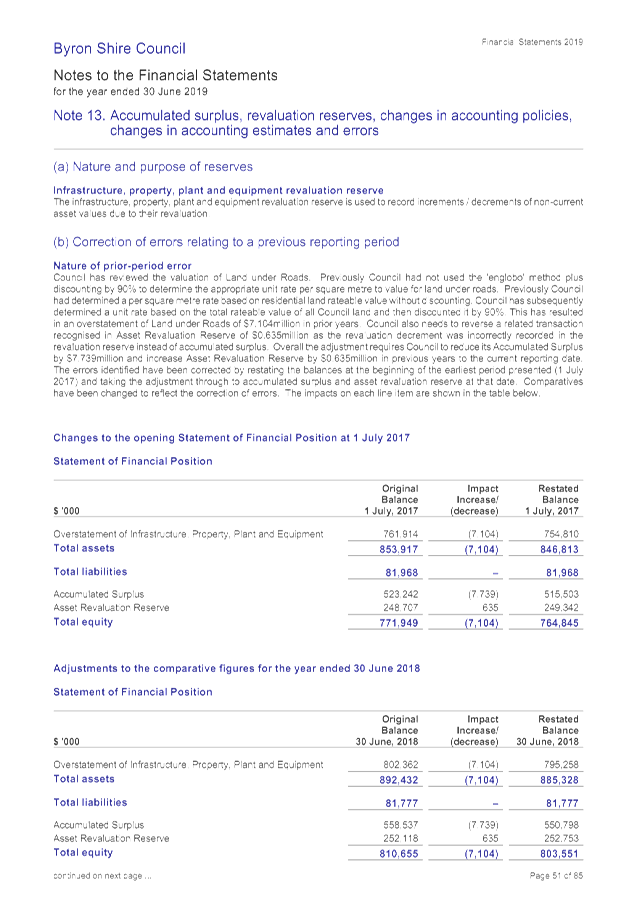

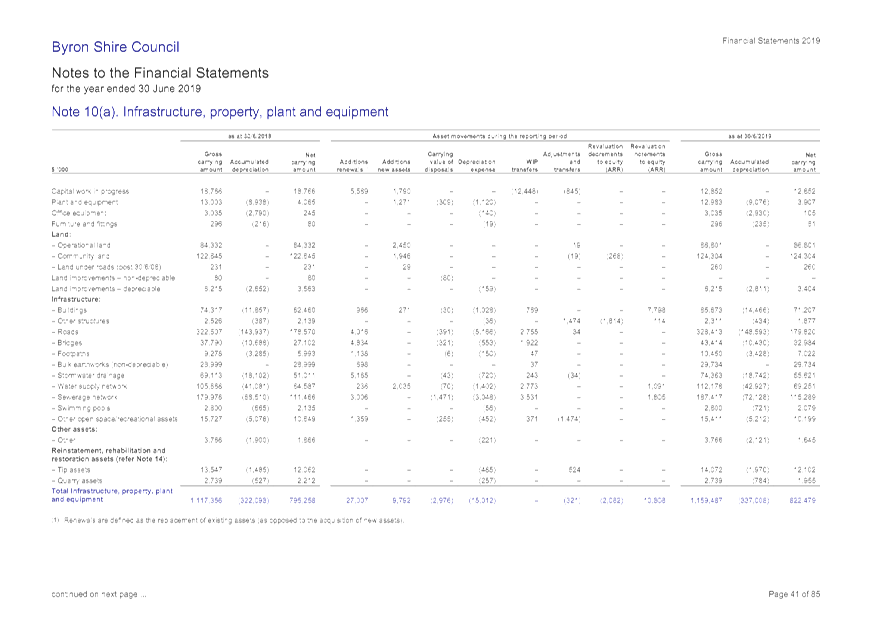

During 2018/2019, there was no revaluation of assets except

for the indexation of Water and Sewerage Assets which is compulsory. Council

also indexed the valuation of its buildings even though this was not

compulsory.

For the upcoming 2019/2020 financial year, Council will need

to consider the revaluation of Roads and Drainage assets given these assets

have not been revalued since 2015 and are due for revaluation.

· Asset

Recognition

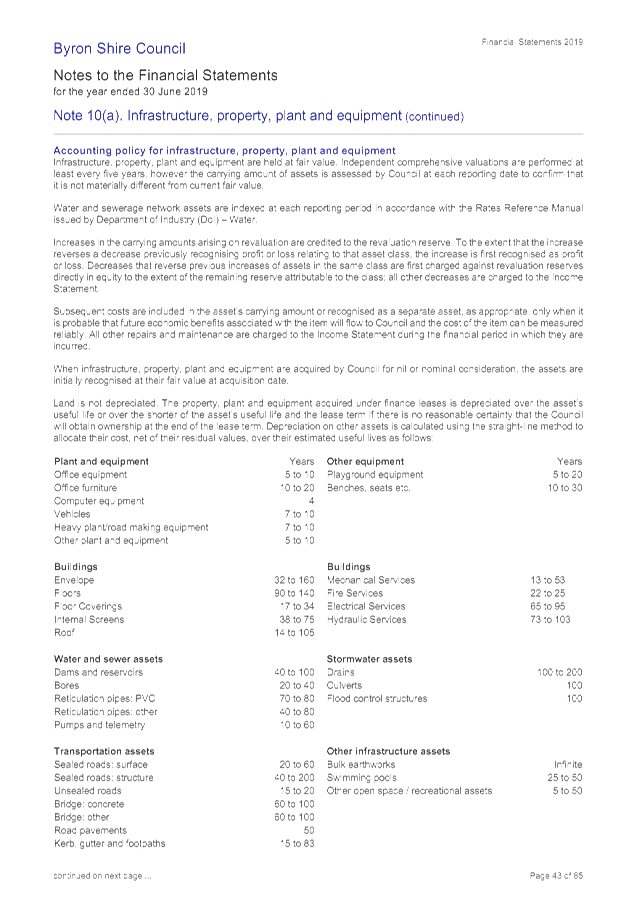

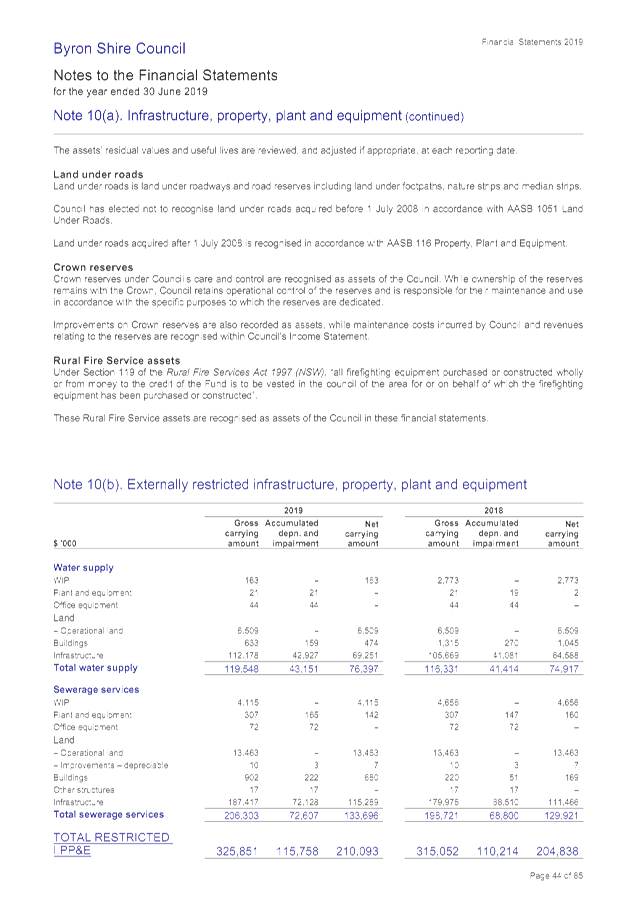

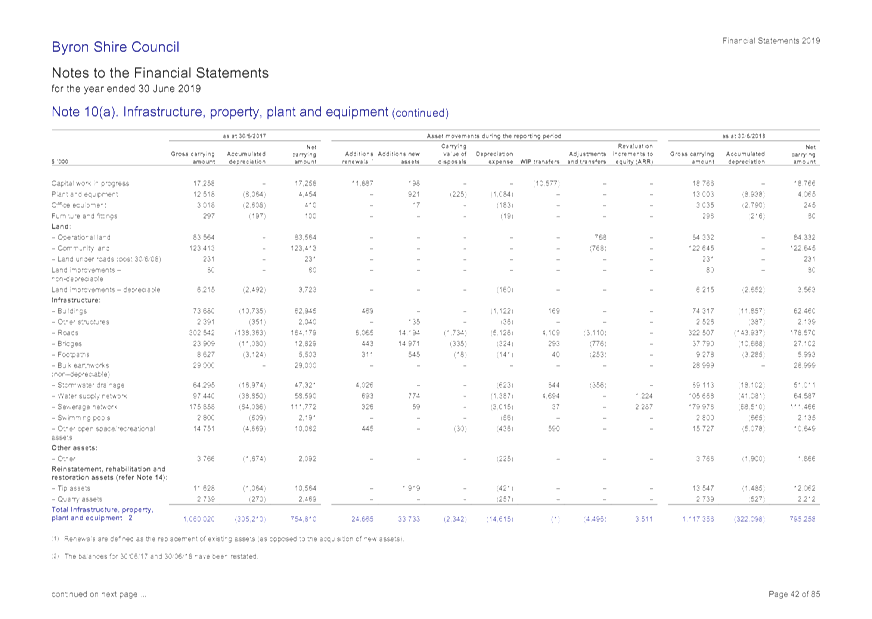

As indicated at Note 10 to the Council’s financial

statements, Council expended $27.007million on asset renewals and $9.792million

on new assets. The extent of asset renewals is significant and demonstrates

ongoing commitment in that area. The depreciation expense of Council’s

assets for 2018/2019 was $15.012million so it is pleasing to see the extent of

asset renewal recognised was significantly more then the financial realisation

via depreciation of the consumption of Council’s assets.

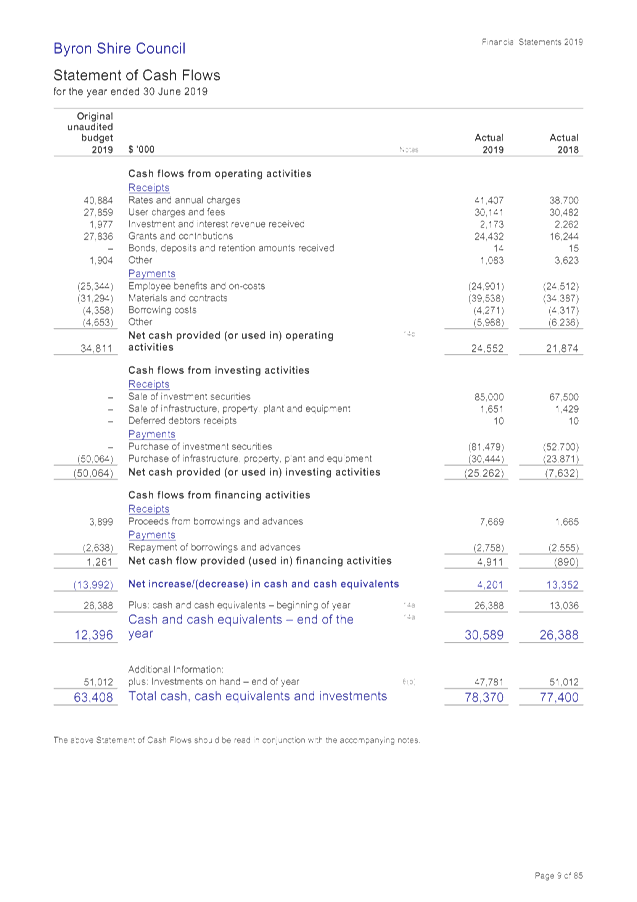

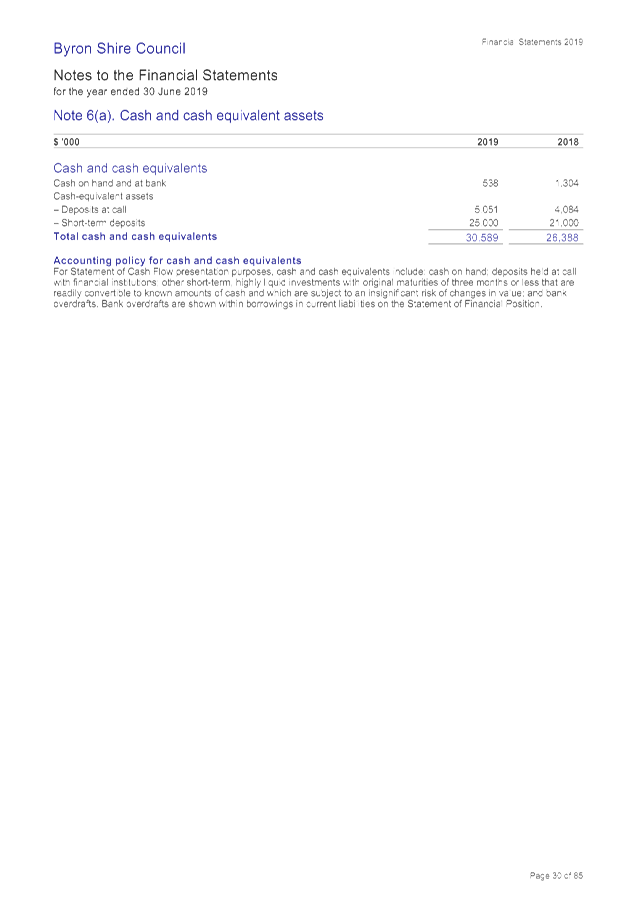

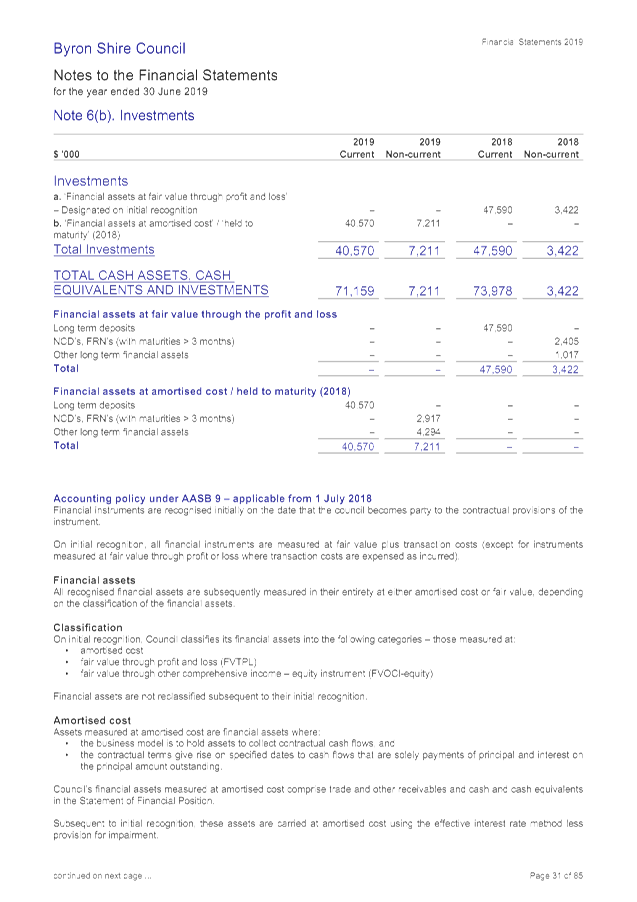

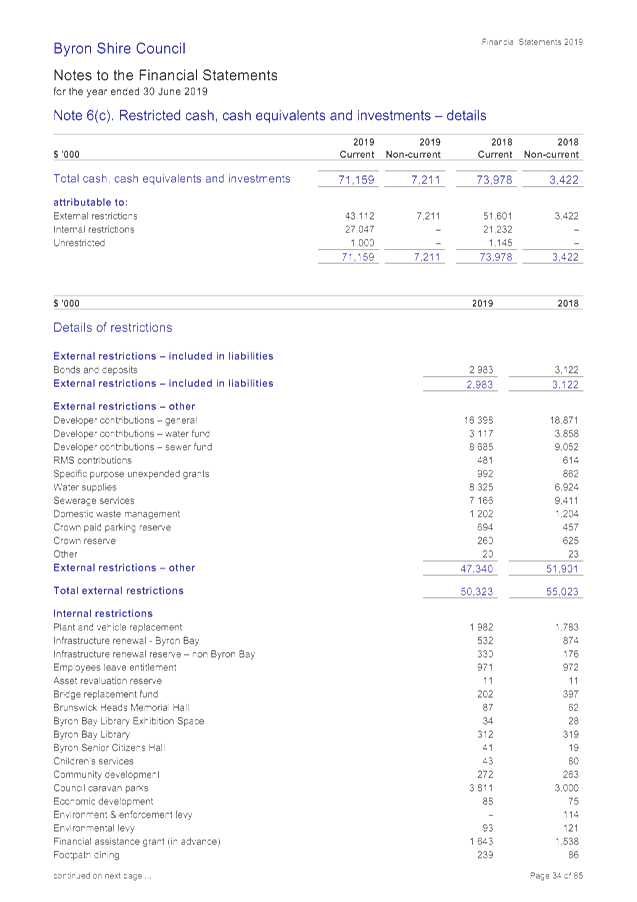

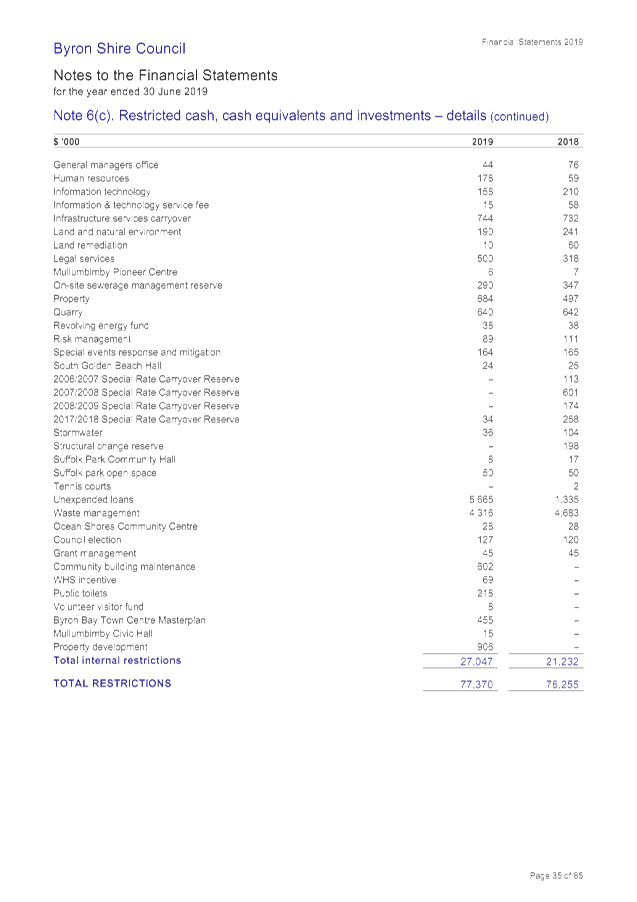

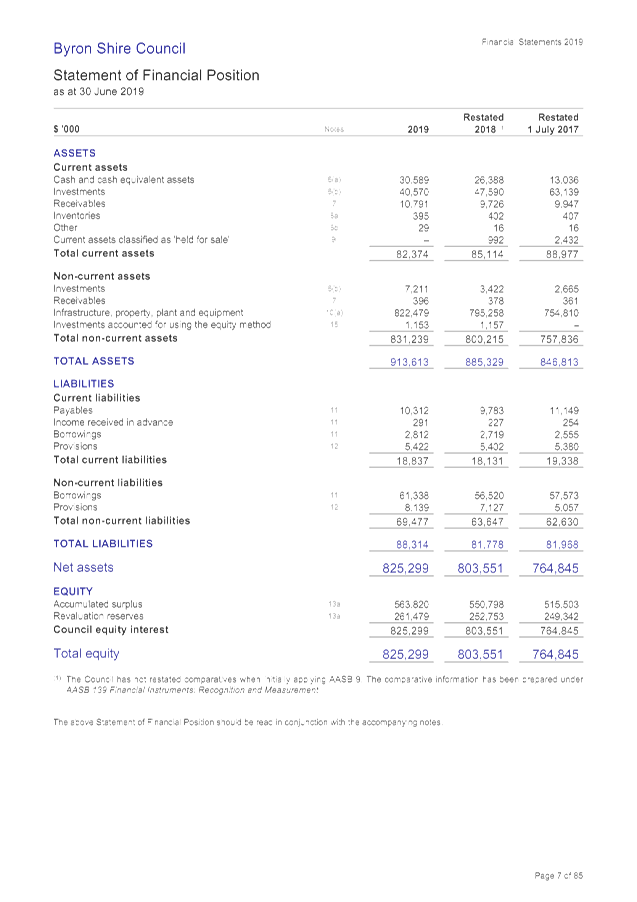

· Cash and

Investments

As at 30 June 2019 (detailed at Note 6 to the financial

statements) Council has maintained $1.000million in unrestricted cash and

investments being a reduction of $0.145million compared to 2017/2018.

This is an ongoing pleasing result and Council has been able to maintain

another one of its short term financial goals of reaching an unrestricted cash

balance of $1million. All other cash and investments totalling

$77.370million are restricted for specific purposes. Overall the cash and

investment position of Council increased by $0.970million during the year.

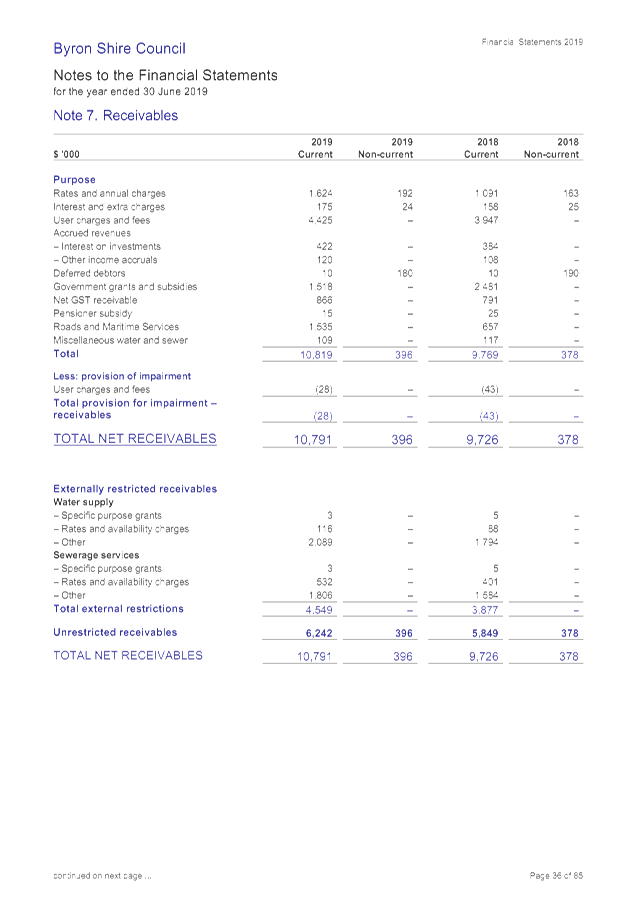

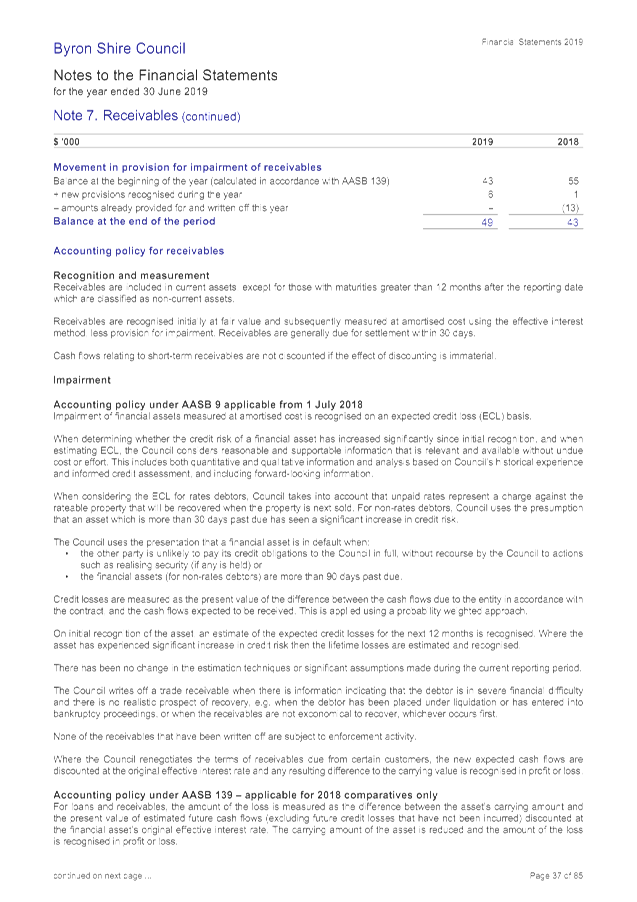

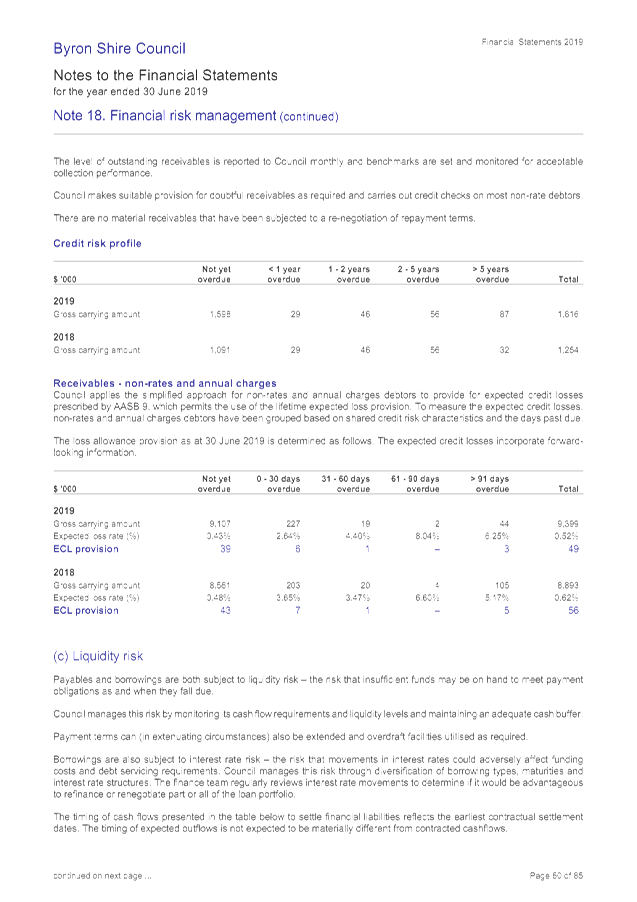

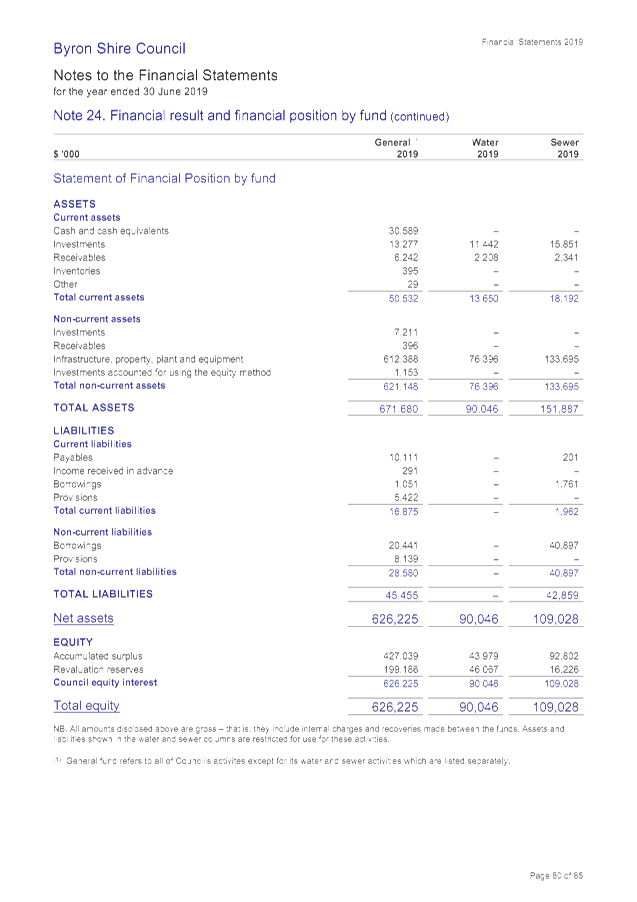

· Receivables

As at 30 June 2019 (detailed at Note 7 to the financial

statements) Council was due $11.187million in receivables. Of this amount

$1.535million was due from Roads and Maritime Services for expenditure claims,

$0.866million from the Commonwealth Government for Goods and Services Tax and

$1.581million in Government grants and subsidies. Overall receivables increased

by $1.083million compared to the 2017/2018 financial year.

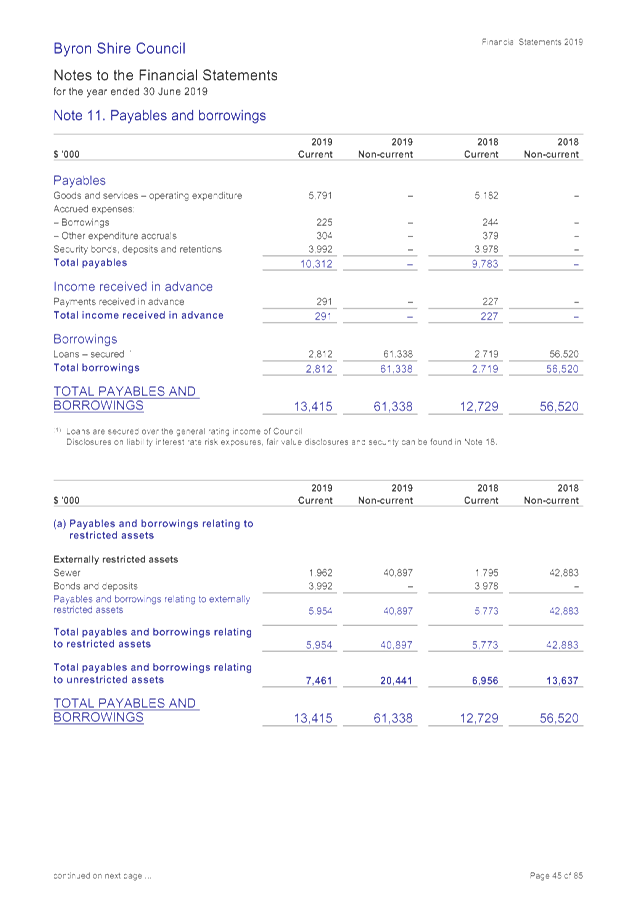

· Payables and

Provisions

At 30 June 2019 (detailed at Note 11 for payables and Note

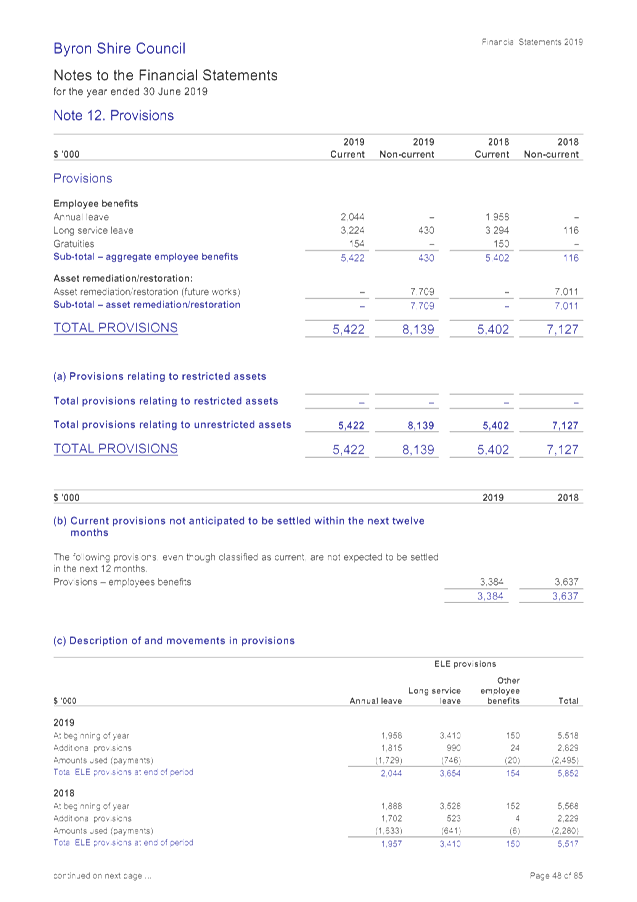

12 for provisions) total payables by Council were $10.603million including

$4.283million held in security bonds, deposits, retentions, payments received

in advance, $0.529million in accrued expenses and $5.791million payable to

suppliers. In addition at 30 June 2019, Council has accrued employee leave

entitlements valued at $5.852million. Specific employee leave entitlements

include $2.044million for annual leave, $3.654million for long service leave

and $0.154million for gratuities. In comparison to 2017/2018, total payables

increased $0.593million whereas total provisions for employee leave

entitlements increased $0.334million.

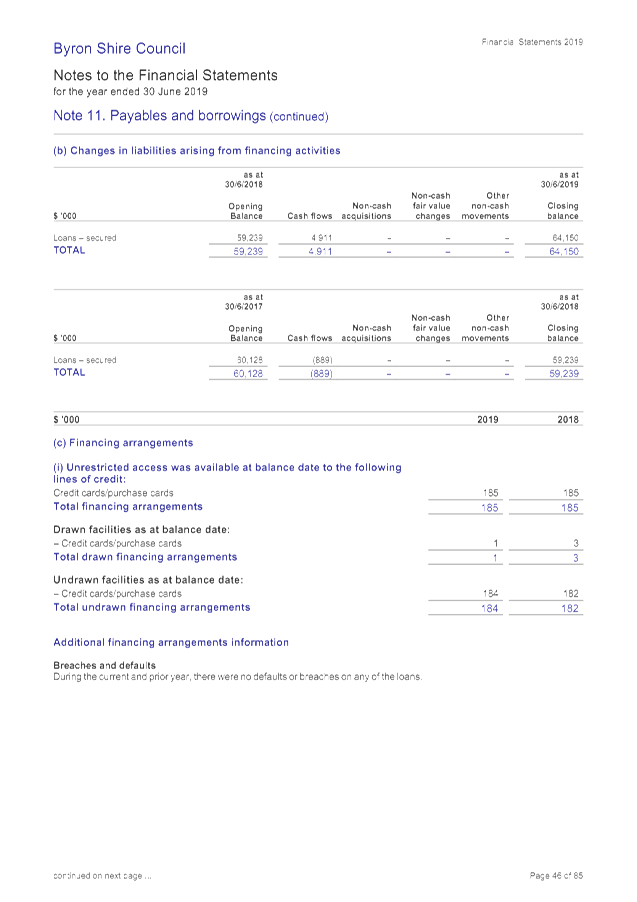

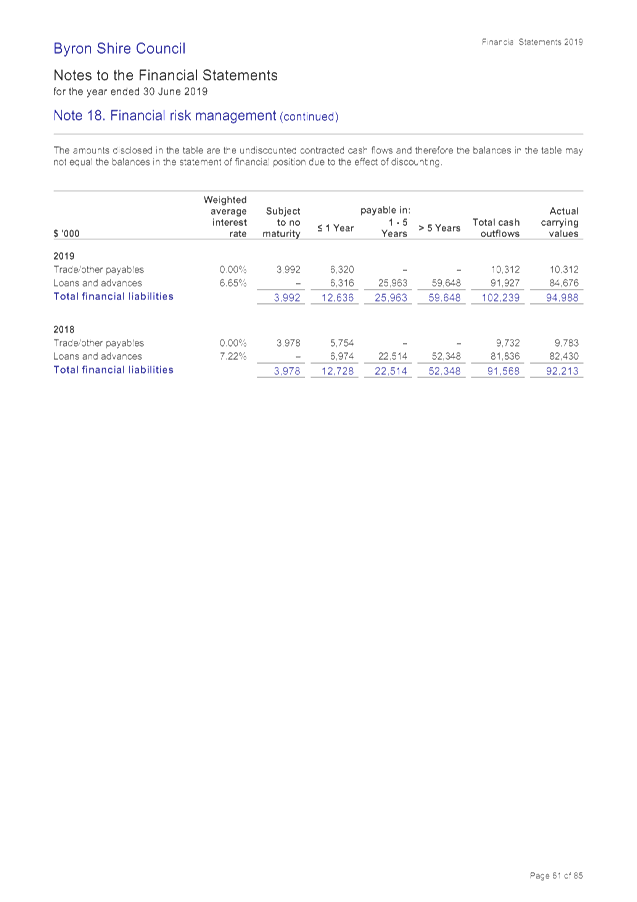

· Loan

Borrowings

During 2018/2019 Council

borrowed new loans of $7.669million and continued to make normal loan

repayments.

Council’s outstanding loans as at 30 June 2019 are

$64.15million. Total loan expenditure for 2018/2019 included interest of

$4.252million and principal payments of $2.758million. Total expenditure in

2018/2019 related to loan repayments was $7.010million or 8.20% of

Council’s revenue, excluding all grants and contributions.

The outstanding loans by Fund totalling $64.150million are

as follows:

· General Fund $21.492million

· Water Fund $0

– Water Fund is debt free

· Sewerage Fund $42.658million

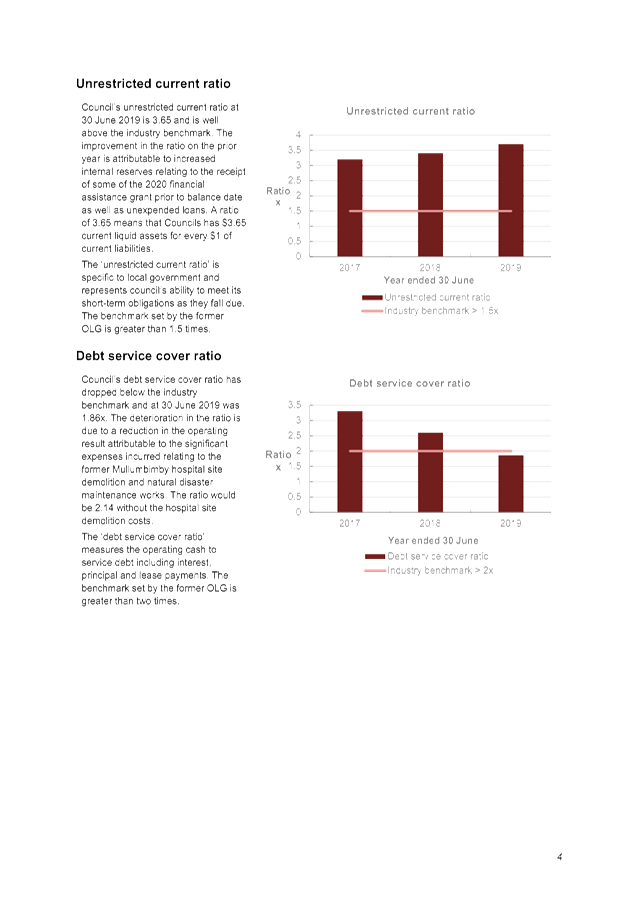

Liquidity

Council’s Statement of Financial Position (balance

sheet) indicates net current assets of $63.537million. It is on this basis, in

the opinion of the Responsible Accounting Officer, that the short term

financial position of Council remains in a satisfactory position and that

Council can be confident it can meet its payment obligations as and when they

fall due. That is, there is no uncertainty as to Council being considered a

‘going concern’. In addition, Council’s cash expense

cover ratio is at 11.02 months whereas the minimum benchmark is 3 months.

Council exceeds this benchmark by nearly four times.

Council’s Unrestricted Current Ratio has improved to

3.65 demonstrating Council has $3.65 in unrestricted current assets compared to

every $1.00 of unrestricted current liabilities.

On a longer term basis Council will need to consider its

financial position carefully. Nevertheless in isolation, the financial results

for 2018/2019 continue to present a ‘stable’ financial position.

Every effort will be made to manage the trend towards operational deficits

before capital grants and contributions.

STRATEGIC CONSIDERATIONS

Community Strategic Plan and

Operational Plan

|

CSP Objective

|

L2

|

CSP Strategy

|

L3

|

DP Action

|

L4

|

OP Activity

|

|

Community

Objective 5: We have community led decision making which is open and

inclusive

|

5.5

|

Manage

Council’s finances sustainably

|

5.5.2

|

Ensure the

financial integrity and sustainability of Council through effective planning

and reporting systems (SP)

|

5.5.2.2

|

Complete annual

statutory financial reports

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Legal/Statutory/Policy

Considerations

Section 413(2)(c) of the Local Government Act 1993 and

Regulation 215 of the Local Government (General) Regulation 2005 require

Council to form an opinion on the financial statements. Specifically

Council needs to sign off an opinion on the Financial Statements regarding

their preparation and content as follows:

In this regard the Financial Statements have been prepared in

accordance with:

· The Local Government Act

1993 (as amended) and the Regulations made thereunder.

· The Australian

Accounting Standards and professional pronouncements.

· The Local Government

Code of Accounting Practice and Financial Reporting.

And the content to the best of knowledge and belief:

· Presents fairly the

Council’s operating result and financial position for the year.

· Accords with

Council’s accounting and other records.

· Management is not aware

of any matter that would render the Financial Statements false or misleading in

any way.

Section 416(1) of the Local Government Act 1993, requires a

Council’s annual Financial Statements to be prepared and audited within

four (4) months of the end of that financial year i.e. on or before 31 October

2019.

Section 417(4) of the Local

Government Act 1993 requires, as soon as practicable after completing the

audit, the Auditor must send a copy of the Auditor’s Reports to the

Departmental Chief Executive and to the Council.

Section 417(5) of the Local

Government Act 1993 requires Council, as soon as practicable after receiving

the Auditor’s Reports, to send a copy of the Auditor’s Reports on

the Council’s Financial Statements, together with a copy of the

Council’s audited Financial Statements, to the Departmental Chief

Executive before 7 November 2019.

Section 418(1) of the Local Government Act 1993 requires

Council to fix a date for the Meeting at which it proposes to present its

audited Financial Statements, together with the Auditor’s Reports, to the

public, and must give public notice of the date so fixed. This

requirement must be completed within five weeks after Council has received the

Auditors Reports i.e. prior to 5 December 2019.

Financial Considerations

There are no direct financial implications associated with

this report as the report does not involve any future expenditure of Council

funds but it is a report advising of Council’s financial outcomes

during the 2018/2019 financial year which are identified in this report and

attachments.

Consultation and Engagement

Section 420 of the Local Government Act 1993 requires

Council to provide the opportunity for the public to submit submissions on the

Financial Statements. Submissions are to be submitted within seven days

of the Financial Statements being presented to the public. In the case of

the 2018/2019 Financial Statements, the closing date for submissions will be 5

December 2019.

Staff Reports - Corporate and Community Services 4.2 - Attachment 1

Confidential Reports - Corporate and Community Services 5.1

Confidential Reports - Corporate and Community

Services

Report No. 5.1 Confidential - Update on IT Actions

Directorate: Corporate

and Community Services

Report

Author: Phil

Pountney, Manager Business Systems and Technology

Colin Baker, Business Systems and

Technology Coordinator

File No: I2019/1691

Summary:

This report provides a summary of

all open actions with their current status and expected due dates.

RECOMMENDATION:

1. That

pursuant to Section 10A(2)(f) of the Local Government Act, 1993, Council

resolve to move into Confidential Session to discuss the report Update on IT

Actions.

2. That

the reasons for closing the meeting to the public to consider this item be that

the report contains:

a) details

of systems and/or arrangements that have been implemented to protect council,

councillors, staff and Council property

3. That

on balance it is considered that receipt and discussion of the matter in open

Council would be contrary to the public interest, as:

Exposes information security

risk an vulnerabilities that could assist threats in the environment to expose

Council data and systems to those without authorisation.

Confidential Reports - Corporate and Community Services 5.2

Report No. 5.2 Confidential - Audit Progress Report -

November 2019

Directorate: Corporate

and Community Services

Report

Author: Heather

Sills, Corporate Governance Officer

File No: I2019/1841

Summary:

This report presents the

Internal Audit Outstanding Actions Report – November 2019 prepared by Council

and the Internal Auditor, O’Connor Marsden and Associates (OCM).

The activity report contains

the remaining outstanding recommendations from each audit review conducted by

Council’s previous internal audit provider as well as recommendations

from recently completed audit reviews conducted by OCM.

RECOMMENDATION:

1. That

pursuant to Section 10A(2)(d)i of the Local Government Act, 1993, Council

resolve to move into Confidential Session to discuss the report Audit Progress

Report - November 2019.

2. That

the reasons for closing the meeting to the public to consider this item be that

the report contains:

a) commercial

information of a confidential nature that would, if disclosed prejudice the

commercial position of the person who supplied it

3. That

on balance it is considered that receipt and discussion of the matter in open

Council would be contrary to the public interest, as:

nature and content of audit

report is for operational purposes

Attachments:

1 Internal

Audit Activity Report - November 2019, E2019/81972

Confidential Reports - Corporate and Community Services 5.3

Report No. 5.3 Confidential - Business Continuity and

Risk Management - Update

Directorate: Corporate

and Community Services

Report

Author: Emma

Fountain, Strategic Risk & Business Continuity Coordinator

File No: I2019/1853

Summary:

The purpose of this report is to provide an update on the

Business Continuity and Risk Management frameworks.

RECOMMENDATION:

1. That

pursuant to Section 10A(2)(f) of the Local Government Act, 1993, Council

resolve to move into Confidential Session to discuss the report Business

Continuity and Risk Management - Update.

2. That

the reasons for closing the meeting to the public to consider this item be that

the report contains:

a) details

of systems and/or arrangements that have been implemented to protect council,

councillors, staff and Council property

3. That

on balance it is considered that receipt and discussion of the matter in open

Council would be contrary to the public interest, as:

Risk management

Attachments:

1 Risk

management strategy, E2019/81410

2 Risk

management action plan, E2019/74957

3 DRAFT

Strategic Risk Register, E2019/75039

4 DRAFT

Operational Risk Register, E2019/75045

Confidential Reports - Corporate and Community Services 5.4

Report No. 5.4 Confidential - Pay Parking Audit Review

Directorate: Corporate

and Community Services

Report

Author: Anna

Vinfield, Manager Corporate Services

File No: I2019/1857

Summary:

Council’s Internal Auditors, O’Connor Marsden

and Associates (OCM), conducted an internal audit review of Pay Parking during October

2019. Their report is at Confidential Attachment 1.

This audit received a review rating of ‘weak’

and it identified one high and three medium risks. Agreed recommendations and

actions are included in the Confidential Attachment.

RECOMMENDATION:

1. That

pursuant to Section 10A(2)(d)i of the Local Government Act, 1993, Council

resolve to move into Confidential Session to discuss the report Pay Parking

Audit Review.

2. That

the reasons for closing the meeting to the public to consider this item be that

the report contains:

a) commercial

information of a confidential nature that would, if disclosed prejudice the

commercial position of the person who supplied it

3. That

on balance it is considered that receipt and discussion of the matter in open

Council would be contrary to the public interest, as:

nature and content of audit

report is for operational purposes

Attachments:

1 Pay

Parking Audit Review, E2019/81748

Confidential Reports - Corporate and Community Services 5.5

Report No. 5.5 Confidential - Grants Management Audit

Review

Directorate: Corporate

and Community Services

Report

Author: Anna

Vinfield, Manager Corporate Services

File No: I2019/1858

Summary:

Council’s Internal Auditors, O’Connor Marsden

and Associates (OCM), conducted an internal audit review of Grant Management during

October 2019. Their report is at Confidential Attachment 1.

This audit received a review rating of

‘satisfactory’ and it identified two medium risks. Agreed

recommendations and actions are included in the Confidential Attachment.

RECOMMENDATION:

1. That

pursuant to Section 10A(2)(d)i of the Local Government Act, 1993, Council

resolve to move into Confidential Session to discuss the report Grants

Management Audit Review.

2. That

the reasons for closing the meeting to the public to consider this item be that

the report contains:

a) commercial

information of a confidential nature that would, if disclosed prejudice the

commercial position of the person who supplied it

3. That

on balance it is considered that receipt and discussion of the matter in open

Council would be contrary to the public interest, as:

nature and content of audit

report is for operational purposes

Attachments:

1 Review of

Grant Management - October 2019, E2019/81617